Recycled Plastic Packaging Market Size and Growth

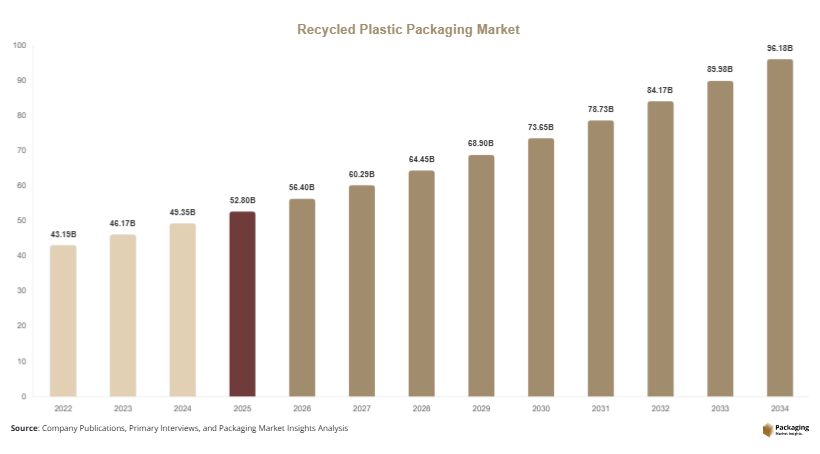

The global recycled plastic packaging market size was valued at USD 52.8 billion in 2025 and is projected to reach USD 56.4 billion in 2026. The market is expected to attain approximately USD 96.7 billion by 2034, registering a CAGR of 6.9% during the forecast period (2025–2034). Increasing investments in circular economy initiatives and government regulations promoting recycled materials are contributing significantly to market expansion.

The recycled plastic packaging market is witnessing significant expansion as industries increasingly adopt sustainable packaging solutions to reduce environmental impact and comply with evolving regulatory requirements. Recycled plastic packaging utilizes post-consumer and post-industrial plastic waste to create packaging products for food, beverages, personal care, healthcare, and industrial applications. Growing awareness regarding plastic waste management, advancements in recycling technologies, and rising commitments from global brands to increase recycled content are accelerating market growth worldwide.

Key Market Highlights

- Asia Pacific dominated the market with a 36.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.8%.

- Bottles led the type segment with a 31.8% share.

- Recycled PET dominated the material segment with a 42.6% share.

- Food & beverage applications led the end-use segment with a 44.3% share.

- The US remained the dominant country with a market size of USD 8.9 billion in 2025 and USD 9.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Food-Grade Recycled Plastics

Food-grade recycled plastics are gaining substantial traction as packaging manufacturers seek sustainable alternatives without compromising safety and performance. Technological improvements in recycling processes have enabled the production of high-quality recycled PET and HDPE suitable for direct food contact applications. Beverage companies are increasingly launching bottles containing high percentages of recycled content to meet sustainability commitments. For example, several global beverage brands now use packaging with more than 50% recycled plastic content in selected product lines. Looking forward, continued innovation in food-grade recycling technologies is expected to improve material quality, increase supply availability, and expand adoption across food and beverage packaging applications.

Growth of Chemical Recycling Technologies

Chemical recycling is emerging as a significant trend within the recycled plastic packaging market. Unlike conventional mechanical recycling, chemical recycling breaks plastics into molecular components, allowing the production of recycled materials with properties comparable to virgin plastics. Packaging companies are investing in chemical recycling partnerships to secure high-quality recycled feedstocks. For example, consumer goods manufacturers are collaborating with recycling technology providers to develop closed-loop packaging systems. Future growth in chemical recycling capacity is expected to increase recycled material availability, improve circularity, and support compliance with stricter recycled-content regulations across multiple packaging sectors.

Market Drivers

Corporate Sustainability Commitments and Circular Economy Goals

Corporate sustainability initiatives are among the strongest drivers of the recycled plastic packaging market. Major consumer brands have established ambitious targets to increase recycled content in packaging and reduce dependence on virgin plastics. This creates a direct cause-and-effect relationship where sustainability commitments drive procurement of recycled plastic materials. For instance, multinational food and beverage companies have announced packaging strategies focused on increasing post-consumer recycled content across product portfolios. As more organizations adopt circular economy frameworks, demand for recycled plastic packaging is expected to rise substantially, creating long-term growth opportunities for recyclers and packaging manufacturers.

Government Regulations Supporting Recycled Content Usage

Governments worldwide are implementing policies designed to reduce plastic waste and promote recycling. Regulations requiring minimum recycled content in packaging are becoming increasingly common across developed and emerging economies. These policies encourage manufacturers to integrate recycled plastics into packaging products. For example, several countries have introduced taxes on virgin plastics and incentives for recycled material adoption. Such measures increase the economic attractiveness of recycled plastic packaging solutions. As regulatory frameworks continue to evolve, demand for compliant packaging materials is expected to strengthen throughout the forecast period.

Market Restraint

Inconsistent Quality and Supply of Recycled Plastic Materials

A key restraint affecting the recycled plastic packaging market is the inconsistency in the quality and availability of recycled plastic feedstocks. Packaging applications often require materials with specific performance characteristics, and variations in recycled resin quality can create manufacturing challenges. Factors such as contamination, inadequate collection systems, and differences in recycling processes contribute to material inconsistency.

The impact is particularly significant in food-grade and healthcare packaging applications, where strict quality standards must be maintained. For example, packaging manufacturers may encounter difficulties sourcing sufficient quantities of high-quality recycled PET to meet customer requirements. Supply shortages can lead to higher material costs and reduced production efficiency. Although investments in recycling infrastructure and advanced sorting technologies are helping improve material quality, supply chain constraints remain a challenge. Addressing these issues will be essential for sustaining long-term market growth and supporting broader adoption of recycled plastic packaging solutions.

Market Opportunities

Expansion of Closed-Loop Recycling Systems

Closed-loop recycling systems present substantial opportunities for market participants. These systems enable packaging materials to be collected, processed, and reused in new packaging applications, supporting circular economy objectives. Consumer brands are increasingly partnering with recyclers and waste management companies to establish closed-loop supply chains. For example, beverage companies are investing in bottle-to-bottle recycling programs to secure reliable sources of recycled PET. Future opportunities are expected to emerge as collection infrastructure improves and digital tracking technologies enhance material traceability. Such developments will support higher recycling rates and greater adoption of recycled packaging materials.

Rising Demand in Emerging Consumer Markets

Emerging markets offer significant growth potential for recycled plastic packaging suppliers. Rapid urbanization, rising incomes, and expanding retail sectors are increasing demand for packaged products across Asia Pacific, Latin America, and Africa. Governments in these regions are introducing sustainability initiatives aimed at reducing plastic waste and encouraging recycling. Packaging manufacturers can capitalize on these trends by establishing local recycling facilities and developing affordable recycled packaging solutions. Future growth opportunities are expected to be driven by expanding consumer goods production, increasing environmental awareness, and improvements in waste collection infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 52.8 Billion |

| Market Size in 2026 | USD 56.4 Billion |

| Market Size in 2034 | USD 96.7 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Bottles dominated the market in 2024, accounting for approximately 31.8% of total market share. This segment leads due to extensive use across beverage, personal care, household, and pharmaceutical packaging applications. Recycled plastic bottles are widely adopted because they offer durability, lightweight performance, and compatibility with established recycling systems. Beverage companies remain among the largest consumers of recycled PET bottles as they work toward sustainability targets. For example, bottled water and soft drink manufacturers increasingly utilize packaging containing high percentages of recycled content. The availability of mature bottle recycling infrastructure further supports segment dominance. Continued growth in beverage consumption and sustainability initiatives is expected to sustain demand throughout the forecast period.

Flexible packaging is projected to be the fastest-growing type segment, expanding at a CAGR of 8.2% through 2034. Growth is being driven by increasing demand for lightweight packaging solutions that reduce transportation costs and material consumption. Advances in recycled film technologies are enabling greater use of recycled content in pouches, wraps, and bags. Future opportunities are expected to emerge from food packaging, e-commerce applications, and consumer goods sectors as manufacturers seek more sustainable flexible packaging alternatives.

By Material

Recycled PET (rPET) accounted for approximately 42.6% of market share in 2024, making it the dominant material segment. Recycled PET offers excellent clarity, strength, and recyclability, making it suitable for a wide range of packaging applications. Beverage bottles, food containers, and personal care packaging frequently utilize rPET due to its performance characteristics and availability. Numerous consumer brands have committed to increasing rPET content in packaging to meet environmental targets. Investments in bottle collection systems and recycling technologies continue to strengthen segment growth. The development of food-grade rPET is further expanding application opportunities across the packaging industry.

Recycled polypropylene (rPP) is expected to be the fastest-growing material segment, registering a CAGR of 7.9% through 2034. Growth is supported by increasing demand for durable packaging solutions and improvements in polypropylene recycling technologies. Applications in food packaging, healthcare products, and household goods are expanding as material quality improves. Future growth is expected to be supported by regulatory incentives and increased investments in polypropylene recovery systems.

By End-Use

Food & Beverage dominated the end-use segment in 2024 with approximately 44.3% market share. The segment benefits from strong demand for sustainable packaging solutions and increasing use of recycled plastics in beverage bottles, food containers, and packaging films. Regulatory requirements encouraging recycled-content packaging are further supporting adoption. Food and beverage companies continue investing in recyclable and recycled packaging formats to improve environmental performance. The segment's large packaging volumes make it a significant contributor to overall market demand.

Healthcare packaging is projected to be the fastest-growing end-use segment, registering a CAGR of 8.0% during the forecast period. Growth is driven by increasing demand for sustainable medical packaging, pharmaceutical containers, and healthcare product packaging. Advances in recycled plastic quality and regulatory approvals are enabling broader adoption within healthcare applications. Future growth is expected to be supported by sustainability initiatives among healthcare providers and pharmaceutical manufacturers.

Recycled Plastic Packaging Market Segmentations

By Type

- Bottles

- Containers

- Trays

- Flexible Packaging

- Other Packaging Formats

By Material

- Recycled PET (rPET)

- Recycled HDPE (rHDPE)

- Recycled Polypropylene (rPP)

- Recycled LDPE (rLDPE)

- Other Recycled Plastics

By End-User

- Food & Beverage

- Personal Care & Cosmetics

- Healthcare

- Household Products

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 28.1% of the global recycled plastic packaging market share in 2025 and is projected to grow at a CAGR of 6.4% through 2034. The region benefits from advanced recycling infrastructure, strong sustainability commitments from consumer goods companies, and increasing regulatory support for recycled-content packaging. Food and beverage manufacturers are actively increasing recycled resin usage to meet environmental goals. Investments in chemical recycling facilities and material recovery systems continue to strengthen the regional market. Growing consumer demand for sustainable packaging solutions further supports adoption across retail, healthcare, and personal care sectors.

The United States dominates the North American market. A unique growth driver is the expansion of state-level recycled-content mandates for beverage containers and consumer packaging products. Several major brands are introducing packaging with higher percentages of post-consumer recycled plastics to comply with regulations and enhance sustainability performance. This trend is encouraging investments in domestic recycling capacity and creating stable demand for recycled packaging materials across the country.

Europe

Europe represented approximately 26.4% of the global market share in 2025 and is expected to register a CAGR of 6.6% during the forecast period. The region benefits from stringent environmental regulations, well-established recycling systems, and strong consumer awareness regarding sustainability. Packaging manufacturers are increasingly incorporating recycled plastics to comply with circular economy objectives and packaging waste directives. The growth of food-grade recycled plastics and investments in advanced sorting technologies continue supporting market expansion. Demand remains particularly strong in food, beverage, and personal care packaging applications.

Germany leads the European market. A unique growth driver is the country's highly developed deposit return system, which supports efficient collection and recycling of plastic packaging materials. Beverage producers increasingly utilize recycled PET sourced through these collection networks. The growing emphasis on closed-loop recycling and resource efficiency is expected to reinforce Germany's leadership position within the European market.

Asia Pacific

Asia Pacific dominated the global market with a 36.9% share in 2025 and is forecast to expand at a CAGR of 7.3% through 2034. Rapid industrialization, rising consumer spending, and increasing environmental awareness are driving demand for recycled plastic packaging throughout the region. Governments are introducing regulations to reduce plastic waste and encourage recycling investments. The expansion of consumer goods manufacturing and food processing industries further contributes to market growth. Investments in recycling infrastructure across China, India, Japan, and Southeast Asia are enhancing regional supply capabilities.

China remains the dominant country in Asia Pacific. A unique growth driver is the country's large-scale investment in domestic recycling and circular economy initiatives. Packaging manufacturers are increasingly utilizing recycled plastics to meet sustainability requirements and improve resource efficiency. The expansion of e-commerce and packaged food industries is also creating significant demand for recycled packaging materials. These factors continue to support strong market growth across the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.8% of global market share in 2025 and is projected to grow at a CAGR of 7.0% through 2034. Increasing awareness of plastic waste management, expanding retail sectors, and government sustainability initiatives are supporting market development. Demand for packaged consumer goods continues to rise as urbanization and population growth accelerate across the region. Investments in recycling facilities and waste collection systems are improving recycled material availability. The market is also benefiting from growing interest in sustainable packaging among multinational brands operating in the region.

The United Arab Emirates is the dominant country in the region. A unique growth driver is the implementation of national sustainability programs focused on waste reduction and recycling. Retailers and consumer goods manufacturers are increasingly adopting recycled plastic packaging to align with environmental objectives. The growing focus on circular economy practices is expected to create further opportunities for packaging suppliers.

Latin America

Latin America held approximately 3.8% of global market share in 2025 and is expected to register the fastest CAGR of 7.8% during the forecast period. Growth is driven by increasing consumer goods production, expanding retail networks, and rising environmental awareness. Governments are introducing policies that encourage recycling and reduce dependence on virgin plastics. Packaging manufacturers are responding by increasing investments in recycled material processing facilities. The growth of food and beverage industries is also generating strong demand for sustainable packaging solutions.

Brazil dominates the Latin American market. A unique growth driver is the country's extensive informal recycling sector, which contributes significantly to plastic waste collection and recovery. Packaging companies are partnering with recycling organizations to secure recycled feedstocks and improve supply chain sustainability. This collaborative approach is expected to support long-term market development and increased adoption of recycled packaging materials.

Competitive Landscape

The recycled plastic packaging market is characterized by increasing competition among packaging manufacturers, recyclers, and material suppliers. Amcor plc is recognized as a leading participant due to its extensive sustainable packaging portfolio, global manufacturing network, and investments in recycled material technologies.

Other prominent companies include Berry Global Inc., Sealed Air Corporation, ALPLA Group, and Sonoco Products Company. These organizations are expanding recycled-content offerings, investing in advanced recycling partnerships, and developing innovative packaging solutions to meet sustainability requirements. Strategic collaborations between packaging companies and recyclers have become increasingly common as organizations seek secure access to recycled feedstocks.

Recent competitive developments include investments in chemical recycling facilities, acquisitions of recycling businesses, and expansion of food-grade recycled resin production capacity. Companies are also focusing on lightweight packaging designs and circular economy initiatives to strengthen market positioning. Sustainability performance and recycled-content capabilities are expected to remain key competitive differentiators throughout the forecast period.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- ALPLA Group

- Sonoco Products Company

- Plastipak Holdings Inc.

- Gerresheimer AG

- AptarGroup Inc.

- DS Smith Plc

- Mondi Group

- Silgan Holdings Inc.

- Constantia Flexibles

- Coveris Holdings S.A.

- Greiner Packaging

- Veolia Environment S.A.

- Indorama Ventures Public Company Limited