Polystyrene Packaging Market Size and Growth

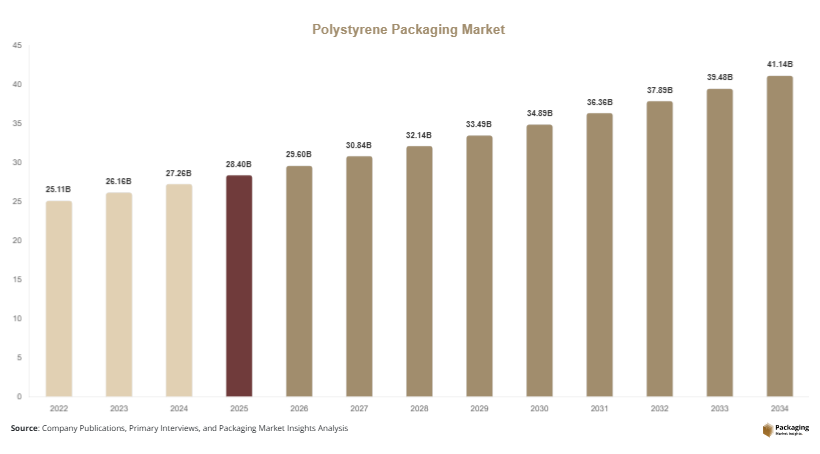

The global polystyrene packaging market size was valued at approximately USD 28.4 billion in 2025 and is projected to reach USD 29.6 billion in 2026. Over the forecast period, the market is expected to expand to USD 41.2 billion by 2034, registering a CAGR of 4.2% during 2025–2034. The polystyrene packaging market is witnessing stable growth due to its widespread use in protective packaging, food service applications, and industrial logistics. Polystyrene, known for its lightweight, insulating, and shock-absorbing properties, remains a preferred material across various industries.

The increasing demand for cost-effective and efficient packaging solutions is a key growth factor. Polystyrene packaging offers excellent protection against physical damage, making it suitable for fragile goods such as electronics and glassware. Additionally, its thermal insulation properties make it ideal for food packaging, particularly for hot and cold food items.

Key Highlights:

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 5.3%.

- Expanded polystyrene (EPS) led the type segment with a 57.6% share.

- Plastic-based polystyrene dominated with a 100% share.

- Food & beverage applications led the segment with 46.5% share.

- China remained the dominant country with a market size of USD 8.1 billion in 2025 and USD 8.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Recyclable and Circular Polystyrene Solutions

The shift toward recyclable and circular packaging solutions is a major trend in the polystyrene packaging market. Manufacturers are investing in advanced recycling technologies to address environmental concerns associated with polystyrene waste. Mechanical and chemical recycling methods are being developed to convert used polystyrene into reusable raw materials.

For example, companies in Europe and North America are implementing closed-loop recycling systems where used polystyrene packaging is collected, processed, and reused in new packaging products. This reduces landfill waste and supports sustainability goals.

In the future, the adoption of circular economy models is expected to increase, driven by regulatory pressures and consumer demand for eco-friendly packaging. This trend will encourage innovation and improve the environmental profile of polystyrene packaging.

Growth of Lightweight and High-Performance Packaging Designs

Another key trend is the development of lightweight and high-performance packaging designs. Manufacturers are focusing on reducing material usage while maintaining strength and durability. This approach helps lower production costs and transportation expenses.

For instance, innovations in foam molding technologies have enabled the production of thinner yet stronger polystyrene packaging. This is particularly beneficial in industries such as electronics and pharmaceuticals, where product protection is critical.

Looking ahead, advancements in material science are expected to further enhance the performance of polystyrene packaging. The integration of additives and improved manufacturing processes will enable the development of more efficient and sustainable packaging solutions.

Market Drivers

Expansion of Food Service and Takeaway Industry

The rapid growth of the food service and takeaway industry is a major driver of the polystyrene packaging market. Increasing urbanization and busy lifestyles have led to higher demand for convenient food options, boosting the use of disposable packaging.

Polystyrene containers are widely used in quick-service restaurants due to their affordability and insulation properties. For example, hot beverages and meals are often packaged in EPS containers to maintain temperature and quality during delivery. This cause-and-effect relationship is evident: as demand for takeaway food increases, the need for efficient packaging solutions rises, driving the growth of the polystyrene packaging market. The trend is expected to continue as food delivery services expand globally.

Growth of E-Commerce and Logistics Sector

The expansion of e-commerce is another significant driver. Online retail requires robust packaging solutions to protect products during shipping. Polystyrene packaging is widely used for cushioning and shock absorption, making it ideal for fragile items.

For instance, electronics companies use polystyrene foam inserts to secure products during transit, reducing the risk of damage. This not only improves customer satisfaction but also reduces return rates. As e-commerce continues to grow, the demand for protective packaging materials is expected to increase. This will drive innovation and support the expansion of the polystyrene packaging market.

Market Restraint

Environmental Concerns and Regulatory Restrictions

Environmental concerns related to polystyrene packaging pose a significant challenge to market growth. Polystyrene is non-biodegradable and contributes to plastic pollution, leading to increased regulatory scrutiny.

Several countries and regions have implemented restrictions on the use of polystyrene packaging, particularly in food service applications. For example, bans on single-use plastics have impacted the demand for polystyrene containers in certain markets. The impact of these regulations is substantial, as they encourage the adoption of alternative materials such as paper-based and biodegradable packaging. This can reduce the market share of polystyrene packaging and affect revenue growth. Despite these challenges, efforts to develop recyclable and sustainable polystyrene solutions are underway. However, regulatory pressures remain a key restraint for the market.

Market Opportunities

Development of Sustainable and Recyclable Polystyrene

The development of sustainable and recyclable polystyrene presents a significant opportunity for the market. Advances in recycling technologies are enabling the reuse of polystyrene waste, reducing environmental impact.

For example, chemical recycling processes can break down polystyrene into its मूल monomers, which can be reused to produce new packaging materials. This approach supports circular economy initiatives and improves sustainability. In the future, increased investment in recycling infrastructure and technology is expected to drive the adoption of sustainable polystyrene solutions. This will create new growth opportunities for market players.

Expansion in Emerging Economies

Emerging economies offer significant growth potential for the polystyrene packaging market. Rapid industrialization, urbanization, and rising consumer spending are driving demand for packaged goods in these regions.

For instance, countries in Asia Pacific and Latin America are witnessing increased consumption of packaged food and electronics, boosting the demand for polystyrene packaging. The growth of retail and e-commerce sectors further supports this trend. As these economies continue to develop, the demand for cost-effective packaging solutions is expected to rise. This will create new opportunities for market expansion and innovation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.4 Billion |

| Market Size in 2026 | USD 29.6 Billion |

| Market Size in 2034 | USD 41.2 Billion |

| CAGR | 4.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Expanded polystyrene (EPS) dominated the market in 2024, accounting for approximately 57.6% of the total share. EPS is widely used due to its lightweight, shock-absorbing, and insulating properties. It is commonly used in packaging for electronics, appliances, and food containers. For example, EPS foam is used to protect fragile items during transportation, reducing the risk of damage. Its cost-effectiveness and versatility make it a preferred choice across industries.

Extruded polystyrene (XPS) is the fastest-growing segment, with a projected CAGR of 4.8%. XPS offers higher strength and moisture resistance compared to EPS, making it suitable for specialized applications. For instance, XPS is used in industrial packaging and construction insulation. As demand for high-performance materials increases, the adoption of XPS is expected to grow.

By Material

Plastic-based polystyrene dominated the market in 2024 with a share of 100%, as polystyrene is inherently a plastic material. Its properties, such as durability and insulation, make it suitable for various packaging applications. For example, polystyrene is widely used in food containers and protective packaging.

Recycled polystyrene is the fastest-growing segment, with a CAGR of 5.0%. This growth is driven by increasing focus on sustainability and waste reduction. Companies are investing in recycling technologies to produce eco-friendly packaging solutions. For instance, recycled polystyrene is being used to create new packaging products, reducing environmental impact.

By End-Use

Food & beverage applications dominated the market in 2024, accounting for 46.5% of the total share. Polystyrene packaging is widely used in this sector due to its insulation properties and affordability. For example, takeaway containers and disposable cups are commonly made from polystyrene.

Electronics packaging is the fastest-growing segment, with a CAGR of 4.9%. The increasing demand for consumer electronics is driving the need for protective packaging solutions. For instance, polystyrene foam is used to secure electronic devices during shipping. As the electronics industry continues to grow, this segment is expected to expand.

Polystyrene Packaging Market Segmentations

By Type

- Expanded Polystyrene (EPS)

- Extruded Polystyrene (XPS)

By Material

- Virgin Polystyrene

- Recycled Polystyrene

By End-Use

- Food & Beverage

- Electronics

- Healthcare

- Consumer Goods

Regional Analysis

North America

North America accounted for approximately 22.8% of the global polystyrene packaging market share in 2025 and is projected to grow at a CAGR of 3.9% during the forecast period. The region is characterized by a mature packaging industry and strong demand from food service and e-commerce sectors. Growth is supported by the increasing adoption of protective packaging solutions for online retail. Additionally, technological advancements in packaging design are enhancing product performance and efficiency. However, regulatory restrictions on single-use plastics are influencing market dynamics, encouraging the development of recyclable alternatives.

The United States dominates the regional market, driven by its large consumer base and advanced logistics infrastructure. A key growth driver is the increasing demand for insulated packaging in food delivery services. For example, food delivery platforms rely on polystyrene containers to maintain temperature and quality during transit. This trend is expected to continue as online food ordering becomes more prevalent.

Europe

Europe held a market share of 27.6% in 2025 and is expected to grow at a CAGR of 3.7%. The region has a strong focus on sustainability and environmental regulations, which are shaping the polystyrene packaging market. Demand for packaging solutions is driven by the food and beverage industry, as well as industrial applications. Companies are investing in recycling technologies to comply with regulatory requirements and reduce environmental impact.

Germany is the dominant country in the region, supported by its robust manufacturing sector. A unique growth driver is the adoption of advanced recycling systems for polystyrene. For example, German companies are implementing closed-loop recycling processes to reduce waste and improve sustainability. This trend is expected to drive innovation and support market growth.

Asia Pacific

Asia Pacific emerged as the largest market with a 39.2% share in 2025 and is projected to grow at a CAGR of 4.6%. Rapid urbanization, industrialization, and population growth are driving demand for packaging solutions in the region. The expansion of the food service and e-commerce sectors is a major growth factor.

China dominates the regional market, driven by its large manufacturing base and growing consumer demand. A key growth driver is the increasing production of consumer electronics, which requires protective packaging. For example, polystyrene foam is widely used for cushioning electronic products during shipping. This trend is expected to continue as the electronics industry expands.

Middle East & Africa

The Middle East & Africa region accounted for 4.8% of the market share in 2025 and is expected to grow at a CAGR of 4.1%. The market is driven by increasing demand for packaged food and beverages, as well as growth in the construction and industrial sectors. Polystyrene packaging is widely used for insulation and protective applications.

South Africa is the leading country in the region, supported by its developing retail sector. A unique growth driver is the increasing demand for affordable packaging solutions in the food industry. For example, polystyrene containers are widely used for takeaway food due to their low cost and efficiency.

Latin America

Latin America held a market share of 5.6% in 2025 and is projected to grow at the fastest CAGR of 5.3%. The region is experiencing steady growth in demand for packaging solutions, driven by rising consumer spending and urbanization. The expansion of the food service and retail sectors is a key growth factor.

Brazil is the dominant country in the region, supported by its large population and growing economy. A key growth driver is the increasing demand for packaged food products. For instance, polystyrene packaging is widely used for food storage and transportation. This trend is expected to drive market growth in the coming years.

Competitive Landscape

The polystyrene packaging market is moderately consolidated, with several key players focusing on product innovation and sustainability. Companies are investing in advanced manufacturing technologies and recycling solutions to enhance their market position.

INEOS Styrolution is identified as a leading player in the market, known for its extensive product portfolio and global presence. The company focuses on developing sustainable polystyrene solutions and expanding its production capacity.

Other major players are adopting strategies such as mergers, acquisitions, and partnerships to strengthen their market presence. For example, companies are collaborating with recycling firms to improve sustainability and comply with regulations.

Recent developments include the introduction of recyclable polystyrene products and investments in circular economy initiatives. These strategies are expected to drive market growth and enhance competitiveness.

Key Players

- INEOS Styrolution

- TotalEnergies SE

- SABIC

- BASF SE

- Trinseo PLC

- Alpek S.A.B. de C.V.

- Americas Styrenics LLC

- Synthos S.A.

- Versalis S.p.A.

- Chi Mei Corporation

- LG Chem Ltd.

- Formosa Chemicals & Fibre Corporation

- Supreme Petrochem Ltd.

- Kumho Petrochemical Co., Ltd.

- Nova Chemicals Corporation