Petrochemical Packaging Market Size and Growth

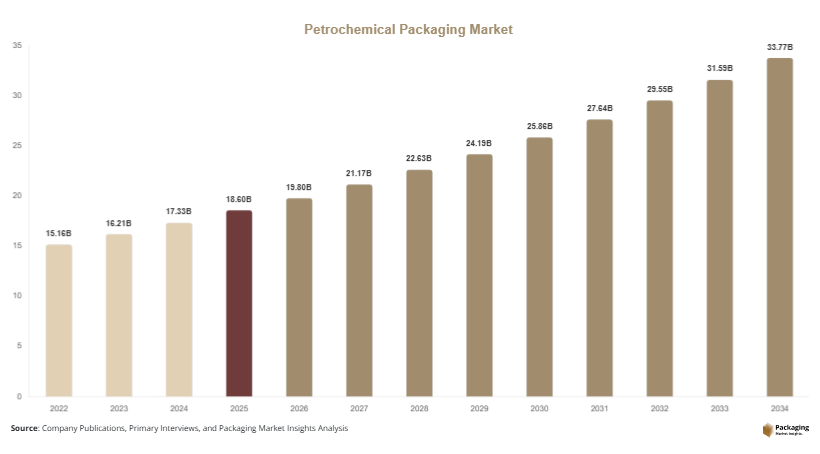

The global petrochemical packaging market size was valued at approximately USD 18.6 billion in 2025 and is projected to reach USD 19.8 billion in 2026. Over the forecast period, the market is expected to grow significantly, reaching nearly USD 33.7 billion by 2034, registering a CAGR of 6.9% from 2025 to 2034. Petrochemical packaging plays a critical role in ensuring safe storage, transportation, and handling of hazardous and non-hazardous chemicals across industrial supply chains. The petrochemical packaging market is experiencing steady expansion driven by the increasing demand for safe, durable, and efficient packaging solutions for chemicals and petrochemical products.

One of the major growth factors is the expansion of the global petrochemical industry, driven by increasing demand for plastics, polymers, and specialty chemicals. As production volumes rise, the need for reliable packaging solutions such as drums, intermediate bulk containers, and flexible bulk packaging increases. Another important factor is the growth in international trade of petrochemical products, which requires high-performance packaging that meets regulatory standards and ensures product integrity during long-distance transportation.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.5%.

- Drums led the type segment with a 31.4% share, while intermediate bulk containers are expected to grow at a CAGR of 7.8%.

- Plastic packaging dominated with a 56.7% share, while metal packaging is forecasted to grow at a CAGR of 6.5%.

- Chemical applications led the segment with 47.2% share, while specialty chemicals are expected to grow at a CAGR of 7.2%.

- China remained the dominant country with a market size of USD 5.3 billion in 2025 and USD 5.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising adoption of sustainable and reusable packaging solutions

The petrochemical packaging market is witnessing a shift toward sustainable and reusable packaging solutions. Companies are focusing on reducing environmental impact by adopting recyclable materials and reusable containers such as intermediate bulk containers and returnable drums. These solutions help reduce waste generation and improve supply chain efficiency. Manufacturers are also exploring bio-based plastics and lightweight materials to minimize carbon emissions. The integration of sustainability practices is becoming a key trend, as companies aim to align with regulatory requirements and corporate environmental goals. This trend is expected to drive innovation in packaging design and materials.

Increasing use of advanced materials and smart packaging technologies

Another important trend is the growing use of advanced materials and smart packaging technologies in petrochemical packaging. High-performance polymers and multi-layer materials are being developed to enhance durability and chemical resistance. Additionally, smart packaging solutions such as RFID tags and sensors are being integrated to monitor product conditions during transportation. These technologies help improve safety, traceability, and operational efficiency. The adoption of digital solutions in packaging is enabling better inventory management and reducing risks associated with chemical handling. This trend is expected to continue as companies focus on improving supply chain transparency.

Market Drivers

Expansion of the global petrochemical industry

The growth of the petrochemical industry is a major driver of the petrochemical packaging market. Increasing demand for petrochemical products such as plastics, synthetic fibers, and industrial chemicals is driving production volumes. This, in turn, creates a need for reliable packaging solutions to ensure safe storage and transportation. The expansion of petrochemical manufacturing facilities, particularly in emerging economies, is further supporting market growth. As production capacity increases, the demand for packaging solutions that can handle large volumes of chemicals is also rising.

Stringent safety and regulatory requirements

Strict regulations governing the handling and transportation of hazardous chemicals are driving the adoption of advanced packaging solutions. Regulatory authorities require packaging that meets specific safety standards to prevent leakage, contamination, and accidents. Compliance with these regulations is essential for companies operating in the petrochemical industry. As a result, there is a growing demand for high-quality packaging materials that provide durability and resistance to chemical reactions. These regulatory requirements are supporting the growth of the petrochemical packaging market.

Market Restraint

High cost of advanced and sustainable packaging solutions

One of the key challenges in the petrochemical packaging market is the high cost associated with advanced and sustainable packaging solutions. While eco-friendly and reusable packaging options offer long-term benefits, their initial costs can be higher compared to traditional packaging materials. This can limit adoption, particularly among small and medium-sized enterprises. Additionally, the cost of raw materials such as high-performance polymers and metals can fluctuate, impacting overall packaging costs. For example, the adoption of intermediate bulk containers requires significant investment in infrastructure and logistics systems. These cost-related challenges may hinder market growth to some extent.

Market Opportunities

Growth in emerging economies and industrial sectors

Emerging economies present significant opportunities for the petrochemical packaging market. Rapid industrialization and urbanization are driving demand for petrochemical products, leading to increased need for packaging solutions. Countries in Asia Pacific, Latin America, and the Middle East are investing in petrochemical infrastructure, creating opportunities for packaging manufacturers. The expansion of industries such as construction, automotive, and manufacturing is further supporting market growth. Companies are focusing on expanding their presence in these regions to capitalize on growing demand.

Development of innovative and customized packaging solutions

The development of innovative and customized packaging solutions is creating new growth opportunities in the market. Companies are focusing on designing packaging that meets specific requirements of different petrochemical products. Customized solutions such as anti-static packaging, corrosion-resistant materials, and temperature-controlled containers are gaining traction. These innovations help improve safety and efficiency in chemical handling. Additionally, the integration of digital technologies in packaging design is enabling better performance and traceability. This trend is expected to drive market growth in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.8 Billion |

| Market Size in 2034 | USD 33.7 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Drums dominated the petrochemical packaging market with a share of 31.4% in 2024. These packaging solutions are widely used due to their durability and ability to store large volumes of chemicals. Drums made from plastic and metal are commonly used in the industry for safe transportation and storage. Their cost-effectiveness and reusability are key factors contributing to their dominance. Additionally, advancements in drum design are improving their performance and safety.

Intermediate bulk containers are expected to grow at a CAGR of 7.8% during the forecast period. These containers offer higher storage capacity and efficiency compared to traditional packaging solutions. The increasing demand for bulk transportation of chemicals is driving their adoption. Their ability to be reused multiple times is also supporting their growth.

By Material

Plastic packaging accounted for the largest share of 56.7% in 2024. Plastic materials such as polyethylene and polypropylene are widely used due to their chemical resistance and lightweight properties. These materials are suitable for a wide range of petrochemical products. Additionally, plastic packaging is cost-effective and easy to handle, making it a preferred choice in the industry.

Metal packaging is expected to grow at a CAGR of 6.5% during the forecast period. Metal containers offer high strength and durability, making them suitable for hazardous chemicals. The increasing demand for secure packaging solutions is driving the adoption of metal packaging. Additionally, metal packaging is recyclable, supporting sustainability initiatives.

By Application

Chemical applications dominated the segment with a share of 47.2% in 2024. The increasing production of industrial chemicals is driving demand for packaging solutions. These applications require packaging that can withstand harsh conditions and prevent leakage. The growth of chemical industries is supporting the expansion of this segment.

Specialty chemicals are expected to grow at a CAGR of 7.2% during the forecast period. The increasing demand for high-value chemicals in industries such as electronics and pharmaceuticals is driving growth. These products require customized packaging solutions to maintain quality and safety. This trend is supporting segment growth.

Petrochemical Packaging Market Segmentations

By Product Type

- Drums

- Intermediate Bulk Containers

- Flexitanks

- Sacks & Bags

By Material

- Plastic

- Metal

- Paper & Paperboard

By Application

- Chemicals

- Petrochemical Products

- Specialty Chemicals

Regional Analysis

North America

North America accounted for approximately 24.8% of the petrochemical packaging market share in 2025 and is expected to grow at a CAGR of 6.5% during the forecast period. The region benefits from a well-established petrochemical industry and advanced logistics infrastructure. Increasing demand for chemical products across industries such as automotive and construction is supporting market growth. Additionally, strict regulatory frameworks regarding chemical safety are encouraging the adoption of high-quality packaging solutions.

The United States dominates the North American market due to its large-scale petrochemical production capacity. A unique growth factor in this region is the increasing adoption of smart packaging technologies. Companies are integrating digital tracking systems to improve supply chain efficiency and safety. This technological advancement is expected to support market growth in the coming years.

Europe

Europe held a market share of around 23.6% in 2025 and is projected to grow at a CAGR of 6.7%. The region’s focus on sustainability and environmental regulations is driving the adoption of eco-friendly packaging solutions. The presence of established chemical industries and advanced manufacturing capabilities is supporting market growth. Additionally, increasing investments in sustainable packaging technologies are contributing to market expansion.

Germany is a leading country in the European market due to its strong industrial base. A key growth factor is the implementation of strict environmental policies that encourage the use of recyclable and reusable packaging materials. These regulations are driving innovation in packaging solutions and supporting market growth.

Asia Pacific

Asia Pacific dominated the market with a share of 38.2% in 2025 and is expected to grow at a CAGR of 7.5%. Rapid industrialization and increasing demand for petrochemical products are driving market growth in the region. The expansion of manufacturing and construction industries is further supporting demand for packaging solutions. Additionally, government initiatives to boost industrial development are contributing to market expansion.

China is the dominant country in the region, supported by its large petrochemical production capacity. A major growth factor is the increasing export of petrochemical products, which requires efficient packaging solutions. This trend is driving demand for advanced packaging materials in the region.

Middle East & Africa

The Middle East & Africa region accounted for a market share of 7.1% in 2025 and is projected to grow at a CAGR of 7.2%. The region’s strong presence in the petrochemical industry is a key driver of market growth. Increasing investments in infrastructure and industrial development are supporting demand for packaging solutions. Additionally, the expansion of export activities is contributing to market growth.

Saudi Arabia is a leading country in this region due to its large oil and gas reserves. A unique growth factor is the development of petrochemical hubs that require advanced packaging solutions. These developments are expected to support market growth in the coming years.

Latin America

Latin America held a market share of 6.3% in 2025 and is expected to grow at the fastest CAGR of 7.5%. The region’s growing industrial sector and increasing demand for petrochemical products are driving market growth. The expansion of manufacturing activities is also contributing to increased demand for packaging solutions.

Brazil is the dominant country in Latin America, supported by its expanding industrial base. A key growth factor is the increasing investment in petrochemical production facilities. This is creating demand for efficient and durable packaging solutions, supporting market growth.

Competitive Landscape

The petrochemical packaging market is moderately competitive, with several global and regional players focusing on product innovation and expansion strategies. Companies are investing in advanced materials and sustainable packaging solutions to meet evolving industry requirements. Strategic partnerships and acquisitions are common approaches to strengthen market position and expand geographic presence.

Greif Inc. is considered a leading player in the market due to its extensive portfolio of industrial packaging solutions. The company recently expanded its production capacity for intermediate bulk containers to meet growing demand. Other key players are also focusing on developing eco-friendly packaging solutions and integrating digital technologies to enhance product performance.

Key Players List

- Greif Inc.

- Mauser Packaging Solutions

- Schutz GmbH & Co. KGaA

- Berry Global Inc.

- Amcor plc

- Mondi plc

- Sonoco Products Company

- Sealed Air Corporation

- DS Smith plc

- Time Technoplast Ltd.

- Hoover Ferguson Group

- Balmer Lawrie & Co. Ltd.

- Nefab Group

- Myers Industries Inc.

- Winpak Ltd.