Cross Linked Polyethylene Market Size and Growth

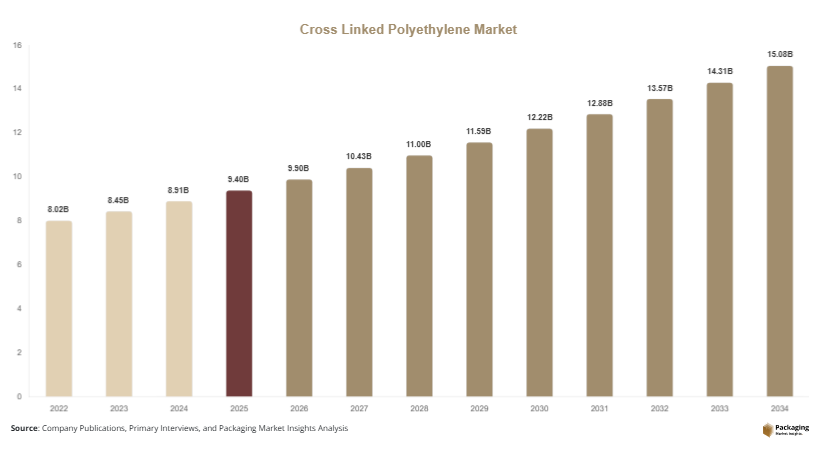

The global cross linked polyethylene market was valued at USD 9.4 billion in 2025 and is estimated to reach USD 9.9 billion in 2026. The market is projected to reach USD 15.8 billion by 2034, expanding at a CAGR of 5.4% during the forecast period from 2025 to 2034. The market is witnessing stable growth due to increasing demand for durable piping systems, expanding wire and cable insulation applications, and rising adoption of advanced polymer materials across construction, automotive, and industrial sectors. Cross linked polyethylene, commonly referred to as PEX, is widely used because of its superior thermal resistance, chemical stability, flexibility, and mechanical strength compared to conventional polyethylene materials.

The construction industry remains one of the largest consumers of cross linked polyethylene products. Rising residential and commercial construction activities across Asia Pacific, North America, and the Middle East are driving demand for PEX pipes used in plumbing, radiant heating, and water distribution systems. The growing focus on energy-efficient buildings and long-lasting infrastructure solutions is further supporting market expansion. In addition, governments across emerging economies are investing heavily in water supply modernization projects, increasing the use of durable polymer piping systems.

Key Market Insights

- Asia Pacific dominated the market with a 41.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.1%.

- Peroxide cross linked polyethylene led the type segment with a 38.6% share.

- High-density polyethylene materials dominated with a 46.9% share.

- Plumbing and piping applications led the end-use segment with 44.7% share.

- The US remained the dominant country in North America with a market size of USD 1.8 billion in 2025 and USD 1.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of PEX Piping Systems in Sustainable Construction

The cross linked polyethylene market is experiencing increasing demand for PEX piping systems in sustainable and energy-efficient construction projects. Builders and infrastructure developers are replacing traditional copper and galvanized steel pipes with PEX materials because of their flexibility, corrosion resistance, and lower installation costs. PEX pipes also reduce leakage risks and improve long-term operational performance in residential and commercial water distribution systems.

Several construction companies across North America and Europe are integrating radiant floor heating systems using cross linked polyethylene pipes to improve energy efficiency in modern buildings. Urban housing projects in Asia Pacific are additionally adopting lightweight piping systems to reduce maintenance expenses and improve plumbing reliability. This trend is expected to strengthen as governments continue implementing green building standards and energy conservation regulations.

Over the forecast period, the adoption of recyclable and low-emission polymer materials in building construction is likely to create additional opportunities for PEX manufacturers. Companies investing in advanced pipe manufacturing technologies may benefit from rising infrastructure modernization activities globally.

Increasing Use of Cross Linked Polyethylene in Electric Vehicle Infrastructure

The market is witnessing growing use of cross linked polyethylene materials in electric vehicle charging systems, battery insulation, and high-performance automotive wiring applications. Cross linked polyethylene offers strong thermal stability, electrical insulation, and resistance to environmental stress, making it suitable for advanced electrical systems used in EVs and renewable energy infrastructure.

Automotive manufacturers are increasingly using XLPE-insulated cables in electric vehicles to improve safety and operational durability under high-temperature conditions. Renewable energy projects such as solar and wind power installations are also driving demand for cross linked polyethylene cable insulation due to its weather resistance and long service life.

For example, several Asian and European cable manufacturers are expanding production capacities for XLPE-insulated power cables used in EV charging stations and smart grid infrastructure. Future demand is expected to rise further as governments accelerate investments in electrification and renewable energy networks worldwide.

Market Drivers

Expansion of Construction and Water Infrastructure Projects

Rapid growth in residential construction, commercial development, and water infrastructure modernization is a major driver supporting the cross linked polyethylene market. Governments across emerging economies are investing heavily in urban water supply systems, sanitation projects, and smart city infrastructure, increasing demand for durable piping materials.

Cross linked polyethylene pipes are increasingly preferred because they offer flexibility, corrosion resistance, and reduced maintenance compared to metal pipes. The material also supports faster installation, which lowers labor costs for construction companies. Rising urban populations in India, China, Indonesia, and Middle Eastern countries are accelerating the need for modern plumbing and water transportation systems.

For example, large-scale residential housing projects in Southeast Asia are increasingly adopting PEX piping systems for hot and cold water distribution applications. Infrastructure rehabilitation projects in the United States and Europe are additionally replacing aging metal pipelines with polymer-based systems. These developments continue to strengthen long-term market demand across construction and utility industries.

Growing Demand for High-Performance Wire and Cable Insulation

The increasing need for advanced electrical infrastructure and high-performance cable systems is another major growth driver for the cross linked polyethylene market. XLPE insulation is widely used in medium-voltage and high-voltage power cables because of its superior dielectric strength, thermal resistance, and durability.

The expansion of renewable energy projects, electric vehicle charging infrastructure, and industrial automation systems has accelerated demand for reliable cable insulation materials. Cross linked polyethylene cables are increasingly used in solar farms, wind power facilities, railway networks, and underground power transmission systems.

Countries such as China, Germany, the United States, and India are investing heavily in renewable energy transmission infrastructure and smart grid modernization projects. Several cable manufacturers are also expanding XLPE cable production capacities to meet rising electricity demand and industrial electrification trends. These factors are expected to support continued market growth through 2034.

Market Restraint

Fluctuating Raw Material Prices and Recycling Challenges

Fluctuating raw material prices remain a significant restraint for the cross linked polyethylene market. The production of cross linked polyethylene relies heavily on petrochemical feedstocks and polyethylene resins, which are influenced by crude oil price volatility and global supply chain conditions. Rising energy and transportation costs can increase manufacturing expenses and reduce profit margins for polymer producers.

Recycling challenges also create operational difficulties for manufacturers. Unlike conventional thermoplastics, cross linked polyethylene has a thermoset-like structure after cross linking, making recycling more complex and expensive. Environmental concerns regarding plastic waste management and disposal regulations are placing additional pressure on manufacturers to develop sustainable processing technologies.

For example, infrastructure and construction companies in Europe are increasingly required to comply with strict waste reduction regulations affecting polymer-based materials. Smaller manufacturers may face financial limitations in adopting advanced recycling technologies and sustainable production systems. In addition, disruptions in resin supply chains can impact pricing stability and material availability across global markets.

These factors may limit market penetration in cost-sensitive regions and create challenges for long-term sustainability goals within the polymer industry.

Market Opportunities

Expansion of Renewable Energy and Smart Grid Infrastructure

The rapid expansion of renewable energy generation and smart grid infrastructure presents significant opportunities for the cross linked polyethylene market. XLPE-insulated power cables are increasingly used in solar parks, offshore wind farms, and high-voltage transmission networks due to their excellent insulation performance and weather resistance.

Governments across North America, Europe, and Asia Pacific are investing heavily in clean energy infrastructure to reduce carbon emissions and improve electricity reliability. These projects require advanced cable systems capable of operating efficiently under high thermal and environmental stress conditions.

Several power transmission companies are adopting underground XLPE cable systems to reduce maintenance costs and improve urban power distribution reliability. Future opportunities are expected in offshore renewable energy projects, electric vehicle charging networks, and grid modernization programs. Manufacturers investing in advanced insulation technologies may benefit from strong long-term demand across the global energy sector.

Rising Demand for Lightweight and Corrosion-Resistant Industrial Materials

Industrial manufacturers are increasingly adopting lightweight and corrosion-resistant polymer materials to improve operational efficiency and reduce maintenance expenses. Cross linked polyethylene is gaining popularity in chemical processing plants, mining operations, and industrial fluid transportation systems due to its durability and chemical resistance.

Industrial sectors in Latin America, the Middle East, and Asia Pacific are investing in modern piping infrastructure to improve manufacturing productivity and reduce operational downtime. Cross linked polyethylene systems also provide improved performance in harsh environments where traditional metal materials are susceptible to corrosion.

Future growth opportunities are expected in industrial wastewater treatment systems, agricultural irrigation infrastructure, and advanced fluid management applications. The increasing focus on sustainable industrial operations and efficient material handling systems is likely to support continued demand for cross linked polyethylene products worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.4 Billion |

| Market Size in 2026 | USD 9.9 Billion |

| Market Size in 2034 | USD 15.8 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Peroxide cross linked polyethylene dominated the cross linked polyethylene market in 2024 with a market share of 38.6%. This segment remains highly preferred because peroxide cross linking provides superior thermal resistance, flexibility, and mechanical strength compared to alternative cross linking methods. PEX-a materials produced through peroxide processing are extensively used in plumbing systems, radiant heating applications, and industrial piping networks. Construction companies prefer peroxide cross linked polyethylene because it offers better crack resistance and easier installation in residential and commercial buildings. The segment also benefits from increasing adoption in hot water distribution systems where durability and pressure resistance are essential. Manufacturers across North America and Europe continue investing in advanced peroxide processing technologies to improve production efficiency and material consistency. In addition, the growth of sustainable building projects and infrastructure modernization programs continues to strengthen long-term demand for high-performance PEX-a materials globally.

Electron beam cross linked polyethylene is expected to register the fastest CAGR of 6.4% during the forecast period. This growth is driven by rising demand for advanced cable insulation and industrial applications requiring enhanced electrical performance and chemical resistance. Electron beam cross linking provides improved precision and faster processing compared to conventional methods, making it suitable for high-performance electrical and automotive applications. Several manufacturers are increasingly using electron beam technology in EV charging cables, renewable energy systems, and aerospace wiring applications. The expansion of electric mobility infrastructure and smart grid projects is further accelerating segment growth. Future demand is expected to increase as industries adopt lightweight and durable polymer insulation systems capable of operating under extreme environmental conditions. Manufacturers investing in automated electron beam processing facilities are likely to strengthen market competitiveness over the coming years.

By Material

High-density polyethylene materials accounted for the largest market share of 46.9% in 2024 due to their superior strength, durability, and chemical resistance. HDPE-based cross linked polyethylene products are extensively used in plumbing pipes, industrial fluid systems, and electrical insulation applications because they provide excellent pressure resistance and long service life. The construction industry remains a major consumer of HDPE-based PEX systems for residential and commercial water transportation networks. Industrial manufacturers also rely on HDPE materials in mining, chemical processing, and wastewater management applications where corrosion resistance is critical. The material’s compatibility with advanced cross linking technologies and large-scale production systems further supports market dominance. Infrastructure projects across Asia Pacific and North America continue to increase demand for durable HDPE-based polymer systems designed for long-term operational performance and reduced maintenance requirements.

Low-density polyethylene materials are projected to witness the fastest CAGR of 5.8% through 2034 due to increasing demand for flexible insulation materials and lightweight industrial products. LDPE-based cross linked polyethylene is widely used in wire and cable insulation applications where flexibility and electrical performance are essential. Automotive manufacturers are increasingly adopting LDPE-based XLPE materials in electric vehicle wiring systems and battery insulation components. The segment is also benefiting from growing renewable energy infrastructure projects requiring durable cable insulation systems. Several manufacturers are developing advanced LDPE formulations with improved heat resistance and environmental durability to support next-generation industrial applications. Future opportunities are expected in smart electronics, renewable power systems, and lightweight automotive components as industries continue shifting toward advanced polymer materials.

By End-Use

Plumbing and piping applications dominated the cross linked polyethylene market in 2024 with a market share of 44.7%. Cross linked polyethylene pipes are increasingly replacing traditional copper and steel piping systems because of their flexibility, corrosion resistance, and lower installation costs. Residential construction projects remain the largest consumers of PEX pipes used in hot and cold water distribution systems, radiant heating systems, and underfloor heating applications. Commercial buildings, hospitals, and hotels are also adopting PEX piping solutions to improve operational efficiency and reduce maintenance requirements. The growing focus on sustainable building construction and energy-efficient infrastructure continues to strengthen segment growth. Governments across Asia Pacific, North America, and Europe are investing in water infrastructure modernization programs that support long-term demand for durable polymer piping systems. Manufacturers are additionally developing leak-resistant and antimicrobial PEX piping technologies to improve performance across residential and industrial applications.

Wire and cable applications are expected to register the fastest CAGR of 6.2% during the forecast period due to increasing investments in renewable energy, smart grid infrastructure, and electric vehicle charging networks. XLPE-insulated cables are widely used in high-voltage transmission systems, industrial machinery, automotive wiring, and underground power distribution networks because of their strong thermal and electrical insulation properties. Renewable energy projects such as solar parks and offshore wind farms are significantly increasing demand for durable cable insulation systems capable of operating in harsh environmental conditions. Several cable manufacturers are expanding production capacities for XLPE-insulated cables to support global electrification initiatives. Future growth opportunities are expected in smart transportation systems, industrial automation, and advanced energy storage infrastructure as governments continue prioritizing sustainable power transmission networks.

Cross Linked Polyethylene Market Segmentations

By Type

- Peroxide Cross Linked Polyethylene

- Silane Cross Linked Polyethylene

- Electron Beam Cross Linked Polyethylene

By Material

- High-Density Polyethylene

- Low-Density Polyethylene

- Medium-Density Polyethylene

By End-User

- Plumbing & Piping

- Wire & Cable

- Automotive

- Industrial Applications

- Healthcare Applications

Regional Analysis

North America

North America accounted for 23.8% of the global cross linked polyethylene market share in 2025 and is projected to expand at a CAGR of 4.9% through 2034. The region benefits from strong residential construction activity, infrastructure modernization projects, and growing demand for advanced plumbing systems. PEX pipes are widely used across the United States and Canada because of their flexibility, freeze resistance, and lower installation costs compared to copper piping systems. The market is also supported by increasing renewable energy investments and expansion of electrical transmission infrastructure using XLPE-insulated cables. In addition, rising adoption of energy-efficient radiant heating systems continues to strengthen regional demand for cross linked polyethylene products.

The United States remained the dominant country within the regional market due to strong housing development and utility infrastructure upgrades. One important growth driver is the replacement of aging metal water distribution pipelines with durable polymer piping systems. Several U.S. municipalities are investing in smart water infrastructure projects designed to reduce leakage and maintenance costs. The expansion of electric vehicle charging networks and renewable energy installations is also increasing demand for XLPE-insulated power cables. Canada continues supporting regional growth through investments in cold-climate plumbing systems and energy transmission projects across remote industrial regions.

Europe

Europe represented 21.4% of the global cross linked polyethylene market in 2025 and is expected to grow at a CAGR of 5.1% during the forecast period. The region continues to witness increasing adoption of sustainable building materials and energy-efficient heating systems. Cross linked polyethylene pipes are extensively used in radiant floor heating systems and residential plumbing applications because of their thermal efficiency and long service life. Environmental regulations promoting energy conservation and low-maintenance infrastructure are encouraging builders to adopt advanced polymer materials across construction projects.

Germany emerged as the leading market in Europe due to its strong industrial base and growing renewable energy sector. A major growth driver is the expansion of underground power transmission infrastructure using XLPE-insulated cables. German utility companies are increasingly replacing conventional cable systems with high-performance polymer-insulated alternatives to improve grid reliability and transmission efficiency. France and the United Kingdom are also witnessing rising adoption of PEX piping systems in sustainable housing developments and commercial renovation projects. Scandinavian countries continue investing in district heating systems utilizing cross linked polyethylene piping technologies.

Asia Pacific

Asia Pacific dominated the cross linked polyethylene market with a 41.2% share in 2025 and is forecast to expand at a CAGR of 5.9% through 2034. Rapid urbanization, industrialization, and infrastructure development remain major growth drivers in the region. Countries such as China, India, Japan, South Korea, and Indonesia are investing heavily in residential housing, water distribution networks, and electrical infrastructure projects, increasing demand for cross linked polyethylene products.

China remained the dominant country in Asia Pacific due to extensive infrastructure construction and strong industrial manufacturing output. One unique growth driver is the rapid expansion of renewable energy transmission networks using XLPE-insulated high-voltage cables. Chinese cable manufacturers are significantly increasing production capacities to support solar and wind energy projects across urban and rural regions. India is additionally experiencing strong growth in plumbing and sanitation infrastructure linked to smart city development initiatives. Southeast Asian countries are also investing in industrial piping systems and utility modernization projects requiring durable polymer materials.

Middle East & Africa

The Middle East & Africa accounted for 6.9% of the global cross linked polyethylene market share in 2025 and is projected to expand at a CAGR of 5.3% during the study period. Growth in the region is primarily supported by rising infrastructure investments, industrial expansion, and increasing water management projects. Gulf countries are increasingly adopting cross linked polyethylene pipes for desalination plants, residential construction, and district cooling systems due to their resistance to harsh climatic conditions and chemical exposure.

Saudi Arabia remained the dominant market within the region because of extensive infrastructure development and utility modernization programs. One key growth driver is the expansion of water distribution and irrigation systems linked to large-scale urban development projects. Construction companies in the country are increasingly using PEX piping systems in residential complexes, hotels, and commercial facilities. The United Arab Emirates is additionally witnessing rising demand for XLPE-insulated cables used in renewable energy and transportation infrastructure projects. South Africa continues supporting regional demand through mining and industrial fluid transportation applications.

Latin America

Latin America held 6.7% of the global cross linked polyethylene market share in 2025 and is expected to register the fastest CAGR of 6.1% during the forecast period. The market is benefiting from rising residential construction activities, expanding industrial infrastructure, and increasing investments in utility modernization projects across Brazil, Mexico, Chile, and Colombia. Cross linked polyethylene products are increasingly used in water supply systems, electrical transmission projects, and industrial processing facilities because of their corrosion resistance and lower maintenance requirements.

Brazil emerged as the leading market within the region due to strong infrastructure spending and growing industrial production. One important growth driver is the expansion of agricultural irrigation systems utilizing durable polymer piping materials. Brazilian infrastructure developers are increasingly replacing metal pipes with PEX systems to reduce operational costs and improve long-term performance. Mexico is also witnessing rising demand for XLPE cable insulation linked to automotive manufacturing expansion and industrial electrification projects. Regional governments continue investing in utility modernization programs supporting long-term demand growth across construction and energy sectors.

Competitive Landscape

The cross linked polyethylene market is moderately competitive with global polymer manufacturers and specialty material suppliers competing across construction, electrical, automotive, and industrial applications. Companies are focusing on product innovation, production capacity expansion, sustainable material development, and strategic partnerships to strengthen market presence.

Dow Inc. is considered one of the leading companies due to its strong polyethylene technology portfolio and extensive global distribution network. The company continues investing in advanced cross linking technologies and recyclable polymer solutions designed for infrastructure and electrical applications.

Borealis AG has expanded its PEX material production capabilities to support growing demand from plumbing and energy sectors. LyondellBasell Industries focuses on high-performance polymer materials for wire insulation and industrial piping systems. SABIC is strengthening its sustainable polymer portfolio through investments in recyclable polyethylene technologies. ExxonMobil Chemical continues developing advanced resin formulations for energy and automotive applications.

Manufacturers are increasingly collaborating with infrastructure developers, cable producers, and automotive suppliers to expand application areas for cross linked polyethylene materials. Investments in automation, renewable energy infrastructure, and advanced insulation technologies are expected to remain key competitive strategies throughout the forecast period.

Key Players List

- Dow Inc.

- Borealis AG

- LyondellBasell Industries

- SABIC

- ExxonMobil Chemical

- Hanwha Solutions

- Arkema S.A.

- Solvay S.A.

- LG Chem

- Westlake Corporation

- Mitsui Chemicals

- PolyOne Corporation

- Avient Corporation

- INEOS

- Chevron Phillips Chemical