Polycarbonate Sheet Market Size and Growth

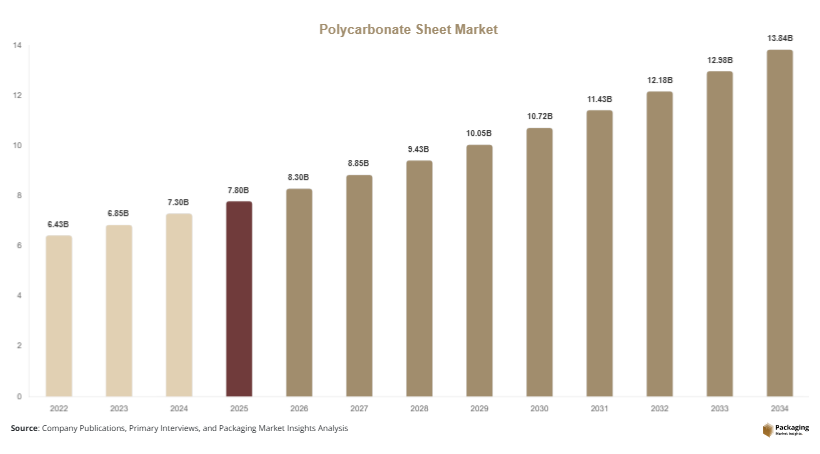

The polycarbonate sheet market was valued at USD 7.8 billion in 2025 and is projected to reach USD 8.3 billion in 2026. By 2034, the market is expected to reach USD 13.9 billion, registering a CAGR of 6.6% during 2025–2034. The polycarbonate sheet market is experiencing stable growth due to increasing demand from construction, automotive, electronics, agriculture, and industrial sectors. Polycarbonate sheets are widely used because of their high impact resistance, lightweight properties, optical clarity, thermal insulation, and weather durability. These sheets are increasingly replacing glass and acrylic materials across commercial and industrial applications.

Rapid urbanization and infrastructure development are among the primary factors driving market growth. Polycarbonate sheets are extensively used in roofing systems, skylights, facades, partitions, and greenhouses because they provide durability along with light transmission efficiency. The construction industry in Asia Pacific, the Middle East, and Latin America continues to adopt lightweight building materials to reduce structural load and improve energy efficiency. Increasing commercial construction projects and public infrastructure investments are contributing significantly to product demand.

Key Highlights

- Asia Pacific dominated the market with a 39.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Solid polycarbonate sheets led the type segment with a 36.4% share.

- Virgin polycarbonate material dominated with a 68.7% share.

- Construction applications led the end-use segment with 44.3% share.

- The US remained the dominant country with a market size of USD 1.7 billion in 2025 and USD 1.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Polycarbonate Sheets

Sustainability trends are influencing the development and adoption of recyclable polycarbonate sheets across construction and industrial sectors. Manufacturers are increasingly introducing recycled-content polycarbonate products to reduce environmental impact and align with green building standards. Construction companies are focusing on sustainable materials that support energy efficiency and waste reduction goals. Polycarbonate sheets are becoming popular because they offer long service life, thermal insulation, and recyclability.

For example, commercial infrastructure projects in Europe and North America are integrating recyclable roofing and glazing materials to meet energy certification requirements. Polycarbonate manufacturers are also investing in closed-loop recycling systems to recover industrial plastic waste. Future demand for eco-friendly construction materials and stricter environmental regulations are expected to strengthen the adoption of recyclable polycarbonate sheets across global markets.

Rising Use of Multiwall Polycarbonate Sheets in Agriculture

The growing expansion of greenhouse farming is increasing demand for multiwall polycarbonate sheets in agricultural applications. These sheets provide superior insulation, UV resistance, and durability compared to traditional greenhouse covering materials. Controlled-environment farming operations are increasingly adopting polycarbonate systems to improve crop productivity and reduce weather-related risks.

Countries such as China, the Netherlands, Spain, and India are investing in advanced greenhouse infrastructure to support food security and high-value crop production. Multiwall sheets help maintain stable internal temperatures while reducing energy consumption in agricultural facilities. Future agricultural modernization initiatives and climate-controlled farming technologies are expected to create strong demand for advanced polycarbonate sheet products over the coming years.

Market Drivers

Growing Construction and Infrastructure Activities

Increasing construction activities worldwide are significantly driving demand for polycarbonate sheets. Urbanization and infrastructure modernization projects are encouraging the use of lightweight and durable building materials in residential, commercial, and industrial structures. Polycarbonate sheets are widely used in skylights, roofing panels, stadium covers, partitions, and facades because of their high impact strength and weather resistance.

For example, commercial construction projects in Asia Pacific and the Middle East increasingly use polycarbonate roofing systems in airports, malls, and public transportation facilities. The material also improves natural lighting and energy efficiency, reducing electricity consumption in buildings. As governments continue investing in infrastructure expansion, demand for polycarbonate sheet solutions is expected to increase steadily.

Rising Demand for Lightweight Automotive Materials

The automotive industry is increasingly adopting polycarbonate sheets to reduce vehicle weight and improve fuel efficiency. Polycarbonate materials offer high impact resistance and design flexibility, making them suitable for automotive glazing, lighting systems, and sunroof applications. Electric vehicle manufacturers are especially focused on lightweight materials that improve battery efficiency and driving range.

Automotive manufacturers in Germany, China, Japan, and the United States are integrating polycarbonate components into next-generation vehicle platforms. The material also supports modern vehicle aesthetics and aerodynamic designs. As vehicle production and EV adoption continue to rise globally, automotive demand for polycarbonate sheet products is expected to expand substantially during the forecast period.

Market Restraint

Fluctuating Raw Material Prices and Environmental Concerns

Volatility in raw material prices remains a major restraint for the polycarbonate sheet market. Polycarbonate resin production depends heavily on petrochemical feedstocks such as bisphenol-A and phosgene derivatives. Changes in crude oil prices, supply chain disruptions, and transportation costs directly affect manufacturing expenses for polycarbonate sheet producers. These fluctuations can reduce profitability and create pricing uncertainty for end users.

Environmental concerns related to plastic waste and chemical safety regulations also present challenges for market growth. Some countries are introducing stricter policies regarding the use and disposal of plastic-based products, increasing compliance costs for manufacturers. For example, certain European regulations regarding chemical additives and recycling standards are encouraging companies to redesign product formulations. Smaller manufacturers may face difficulties investing in sustainable production technologies and recycling infrastructure. In addition, competition from alternative materials such as acrylic sheets and tempered glass may limit growth in cost-sensitive applications. Although demand remains stable, these pricing and environmental factors may slow market expansion in regions with strict regulatory frameworks.

Market Opportunities

Expansion of Smart Green Building Projects

The growing adoption of smart green buildings is creating strong opportunities for polycarbonate sheet manufacturers. Modern commercial and residential buildings increasingly use transparent and energy-efficient materials to improve indoor lighting and reduce energy consumption. Polycarbonate sheets are becoming popular in sustainable architecture because they provide thermal insulation, durability, and lightweight installation benefits.

Green building projects in North America, Europe, and Asia Pacific are integrating polycarbonate facades, skylights, and roofing systems to achieve energy certification standards. Smart city initiatives and eco-friendly urban development programs are expected to increase product demand over the next decade. Manufacturers focusing on UV-resistant and recyclable polycarbonate solutions are likely to benefit from this transition toward sustainable construction materials.

Growth in Industrial Safety and Security Applications

Industrial safety applications are emerging as an important opportunity area for the polycarbonate sheet market. Polycarbonate sheets are widely used in machine guards, safety shields, riot barriers, protective glazing, and industrial partitions because of their high impact resistance and transparency. Manufacturing industries increasingly require durable safety materials to comply with workplace safety regulations.

For example, industrial facilities and transportation hubs are adopting impact-resistant polycarbonate barriers for worker protection and security infrastructure. Demand for protective transparent materials has also increased in healthcare facilities and public spaces. Future investments in industrial automation, factory modernization, and public safety infrastructure are expected to support long-term demand for specialized polycarbonate sheet products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.8 Billion |

| Market Size in 2026 | USD 8.3 Billion |

| Market Size in 2034 | USD 13.9 Billion |

| CAGR | 6.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Solid polycarbonate sheets dominated the type segment with a 36.4% market share in 2024. These sheets are widely used in commercial construction, industrial safety, transportation infrastructure, and glazing applications because of their high transparency and impact resistance. Solid sheets provide excellent durability while remaining significantly lighter than glass. Commercial buildings, railway stations, airports, and industrial facilities increasingly adopt solid polycarbonate sheets for roofing and protective barriers. Their resistance to UV radiation and weather exposure also makes them suitable for long-term outdoor applications. Construction companies prefer these sheets because they reduce installation costs and improve structural flexibility compared to traditional glass materials.

Multiwall polycarbonate sheets are projected to witness the fastest CAGR of 7.4% during the forecast period. These sheets provide superior thermal insulation and lightweight performance, making them highly suitable for greenhouse farming, skylights, and energy-efficient building systems. Agricultural applications are rapidly expanding because multiwall structures help maintain stable indoor temperatures while reducing energy usage. The growing focus on sustainable construction and controlled-environment agriculture is expected to drive strong demand for multiwall polycarbonate products. Manufacturers are also developing advanced coatings and UV-resistant technologies to improve product lifespan and performance.

By Material

Virgin polycarbonate material held the dominant market share of 68.7% in 2024 because of its superior clarity, strength, and durability. Virgin-grade polycarbonate sheets are widely used in automotive glazing, commercial construction, industrial equipment, and transparent roofing systems where high optical performance is required. Manufacturers prefer virgin materials because they offer consistent quality and strong resistance to impact and environmental conditions. Industrial sectors requiring safety glazing and protective barriers also depend heavily on virgin polycarbonate sheets due to strict performance requirements. Increasing infrastructure development and industrial modernization projects continue to support demand for high-quality virgin polycarbonate products.

Recyclable polycarbonate materials are expected to grow at the fastest CAGR of 7.8% during the forecast period. Rising environmental concerns and sustainability initiatives are encouraging manufacturers to adopt recycled-content thermoplastics in construction and industrial applications. Recyclable materials help reduce carbon emissions and lower production waste while maintaining adequate mechanical performance. Governments and commercial developers are increasingly prioritizing eco-friendly building materials to meet sustainability goals. Advances in recycling technologies and closed-loop production systems are expected to improve the commercial viability of recycled polycarbonate sheets over the coming years.

By End-Use

Construction applications accounted for the largest market share of 44.3% in 2024 due to widespread use in roofing, skylights, facades, partitions, and architectural glazing systems. Polycarbonate sheets are increasingly replacing glass in commercial and industrial buildings because they offer lower weight, higher impact resistance, and better thermal insulation. Urban infrastructure projects and modern architectural designs are increasing the use of transparent lightweight materials across transportation hubs, malls, and public buildings. Builders also prefer polycarbonate sheets because they improve energy efficiency by allowing natural light transmission while reducing heating and cooling costs.

Automotive applications are expected to register the fastest CAGR of 7.5% during the forecast period. Automakers are increasingly integrating polycarbonate materials into windows, panoramic roofs, headlamp covers, and electric vehicle components to reduce overall vehicle weight. Lightweight thermoplastic materials improve fuel efficiency and support EV battery performance. Automotive manufacturers are also adopting polycarbonate sheets because they allow greater design flexibility and aerodynamic optimization. As global electric vehicle production expands, demand for automotive-grade polycarbonate materials is expected to increase substantially.

Polycarbonate Sheet Market Segmentations

By Type

- Solid Polycarbonate Sheets

- Multiwall Polycarbonate Sheets

- Corrugated Polycarbonate Sheets

- Textured Polycarbonate Sheets

By Material

- Virgin Polycarbonate

- Recycled Polycarbonate

- UV-Protected Polycarbonate

- Flame-Retardant Polycarbonate

By End-User

- Building & Construction

- Automotive & Transportation

- Electrical & Electronics

- Agriculture

- Industrial Manufacturing

Regional Analysis

North America

North America accounted for 24.2% of the polycarbonate sheet market share in 2025 and is projected to grow at a CAGR of 6.1% during the forecast period. The region benefits from strong demand across construction, automotive, and industrial applications. Commercial renovation projects and infrastructure modernization initiatives are increasing the use of lightweight glazing and roofing materials. Polycarbonate sheets are widely adopted in stadiums, airports, industrial facilities, and transportation infrastructure due to their impact resistance and energy efficiency. Growing investments in electric vehicle production are also supporting demand for automotive-grade polycarbonate components across the region.

The United States remains the dominant country in North America due to its advanced construction sector and rising adoption of sustainable building materials. Commercial real estate developers are increasingly integrating transparent roofing systems and energy-efficient skylights into office buildings and retail complexes. The country is also witnessing strong growth in greenhouse farming projects, particularly in states with controlled-environment agriculture investments. Automotive manufacturers are expanding the use of lightweight thermoplastics to meet fuel efficiency standards and improve electric vehicle performance.

Europe

Europe held 23.4% of the global polycarbonate sheet market in 2025 and is expected to register a CAGR of 6.3% through 2034. Strict energy efficiency regulations and increasing adoption of green building materials are supporting regional market growth. Polycarbonate sheets are widely used in commercial roofing, facade systems, and industrial safety applications across European countries. The region also benefits from rising investments in greenhouse farming infrastructure and public transportation modernization projects. Manufacturers are focusing on recyclable and UV-resistant polycarbonate products to comply with sustainability standards.

Germany dominates the European market because of its strong industrial manufacturing base and advanced automotive sector. Automotive manufacturers are increasingly using polycarbonate materials in glazing and lighting systems to reduce vehicle weight. Germany is also investing in sustainable construction projects that require durable and energy-efficient building materials. The expansion of smart city projects and public infrastructure upgrades is further supporting demand for high-performance polycarbonate sheets across commercial and industrial applications.

Asia Pacific

Asia Pacific dominated the polycarbonate sheet market with a 39.8% share in 2025 and is projected to grow at a CAGR of 7.2% during the forecast period. Rapid urbanization, expanding construction activities, and rising industrial production are major growth factors across the region. Countries such as China, India, Japan, and South Korea are investing heavily in commercial infrastructure, transportation systems, and residential housing projects. Polycarbonate sheets are increasingly used in roofing, partitions, agricultural greenhouses, and industrial glazing applications because of their durability and lightweight characteristics.

China remains the leading country in Asia Pacific due to large-scale infrastructure development and strong manufacturing capabilities. The country has witnessed substantial investments in public transportation projects, industrial parks, and commercial buildings, increasing demand for advanced construction materials. Chinese greenhouse farming operations are also expanding rapidly to improve agricultural productivity and food security. India is emerging as another important growth market because of rising urban housing demand and increasing infrastructure investments under smart city development programs.

Middle East & Africa

The Middle East & Africa region accounted for 6.1% of the polycarbonate sheet market in 2025 and is expected to grow at a CAGR of 5.9% during the forecast period. Rising infrastructure investments and increasing adoption of modern construction materials are supporting regional market growth. Polycarbonate sheets are widely used in commercial roofing systems, stadium projects, and industrial facilities because they provide heat resistance and durability in extreme weather conditions. Governments across the region are investing in tourism infrastructure, airports, and commercial developments that require lightweight and weather-resistant materials.

Saudi Arabia dominates the regional market because of large-scale urban development projects and industrial diversification initiatives. The country is investing heavily in commercial real estate, entertainment infrastructure, and transportation modernization programs. Polycarbonate sheets are increasingly used in architectural glazing, walkways, and industrial safety systems across these projects. Demand for energy-efficient construction materials is expected to rise further as regional governments focus on sustainable urban development and infrastructure modernization.

Latin America

Latin America represented 6.5% of the global polycarbonate sheet market in 2025 and is forecasted to grow at the fastest CAGR of 7.1% during the forecast period. Expanding commercial construction activities and increasing greenhouse farming adoption are major factors supporting regional growth. Countries such as Brazil, Mexico, and Argentina are investing in agricultural modernization and industrial infrastructure development. Polycarbonate sheets are increasingly used in agricultural greenhouses, warehouse roofing, and public infrastructure projects due to their affordability and weather resistance.

Brazil remains the dominant country in Latin America because of its expanding agricultural sector and growing infrastructure investments. Greenhouse farming operations are increasing demand for UV-resistant multiwall polycarbonate sheets to improve crop productivity. Industrial manufacturers are also adopting impact-resistant transparent materials for factory safety systems and industrial glazing applications. Mexico is witnessing rising demand from automotive manufacturing and commercial construction sectors, creating additional opportunities for polycarbonate sheet suppliers.

Competitive Landscape

The polycarbonate sheet market is moderately competitive, with major manufacturers focusing on product innovation, sustainability initiatives, and regional capacity expansion. Companies are investing in UV-resistant coatings, recyclable materials, and advanced extrusion technologies to strengthen their market positions. Strategic partnerships with construction companies, greenhouse developers, and automotive manufacturers are becoming increasingly important for long-term growth.

SABIC remains a leading player in the market because of its extensive polycarbonate material portfolio and strong global manufacturing network. The company focuses on lightweight and sustainable thermoplastic solutions for construction and automotive applications. Covestro AG continues expanding its high-performance sheet product line for industrial and transportation sectors. Palram Industries is strengthening its position through greenhouse and architectural glazing solutions across international markets.

Teijin Limited is investing in lightweight automotive-grade polycarbonate materials to support electric vehicle production. Mitsubishi Chemical Group is focusing on recyclable thermoplastic innovations and advanced industrial safety applications. Market competition is expected to intensify as manufacturers expand sustainable product offerings and regional production capabilities.

Key Players List

- SABIC

- Covestro AG

- Palram Industries Ltd.

- Teijin Limited

- Mitsubishi Chemical Group Corporation

- Trinseo PLC

- Excelite

- Gallina India

- Arla Plast AB

- Plazit-Polygal Group

- Brett Martin Ltd.

- SafPlast Company

- Koscon Industrial S.A.

- DS Smith Plc

- Ug-Plast Inc.