Automotive Plastic Compounding Market Size and Growth

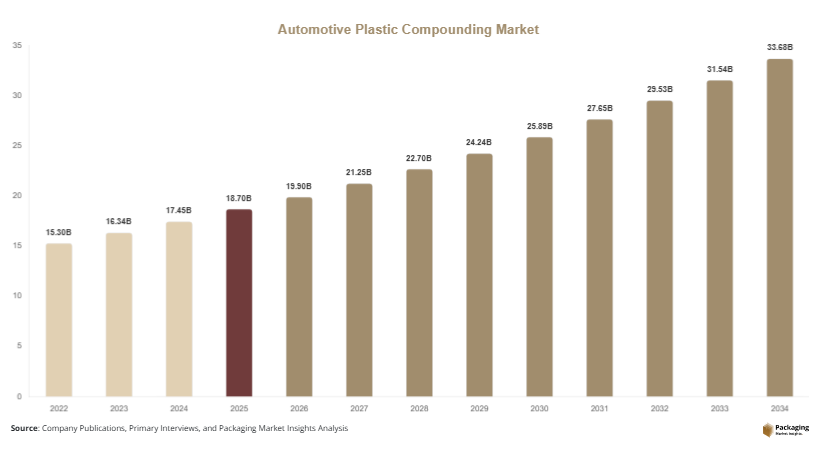

The automotive plastic compounding market was valued at USD 18.7 billion in 2025 and is projected to reach USD 19.9 billion in 2026. By 2034, the market is forecasted to reach USD 33.8 billion, expanding at a CAGR of 6.8% during 2025–2034. Automotive plastic compounds are engineered materials produced by blending polymers with additives, fillers, reinforcements, and stabilizers to improve thermal resistance, strength, flexibility, and durability. These compounds are widely used in dashboards, bumpers, door panels, under-the-hood components, seating systems, and electric vehicle battery housings. The automotive plastic compounding market is witnessing consistent expansion due to the growing demand for lightweight vehicle materials, increasing electric vehicle production, and rising fuel efficiency regulations across major automotive economies.

The increasing shift toward lightweight vehicles remains one of the strongest growth factors for the market. Automakers are replacing metal components with high-performance compounded plastics to reduce overall vehicle weight and improve fuel efficiency. A reduction of 10% in vehicle weight can improve fuel economy by nearly 6–8%, encouraging automakers to adopt polypropylene, polyamide, ABS, and polycarbonate compounds in structural and interior applications. The rapid transition toward electric vehicles has also accelerated demand for advanced plastic compounds because EV manufacturers require lightweight materials to extend battery range and improve thermal insulation.

Key Highlights

- Asia Pacific dominated the market with a 41.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Polypropylene compounds led the type segment with a 34.8% share.

- Thermoplastic materials dominated with a 63.5% share.

- Interior applications led the end-use segment with 39.7% share.

- The US remained the dominant country with a market size of USD 3.9 billion in 2025 and USD 4.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Recyclable and Sustainable Automotive Plastics

The automotive industry is increasingly shifting toward recyclable and sustainable plastic compounds as manufacturers focus on carbon reduction targets and circular economy practices. Automotive OEMs are integrating recycled polypropylene, recycled polyamide, and bio-based thermoplastics into vehicle interiors, trims, and non-structural components. Governments in Europe and North America are introducing stricter recycling standards, encouraging automakers to reduce dependency on virgin plastic materials. This trend is creating strong demand for compounded plastics that combine sustainability with mechanical performance.

For example, several electric vehicle manufacturers are using recycled plastic compounds in battery casings and seat components to improve environmental performance without compromising durability. Sustainable compounds also help automakers achieve lower lifecycle emissions. In the future, advancements in chemical recycling and bio-based resin technologies are expected to improve the commercial adoption of eco-friendly automotive compounds across premium and mass-market vehicles.

Increased Use of High-Performance Plastics in Electric Vehicles

Electric vehicle production is driving demand for high-performance plastic compounds with superior thermal stability, flame resistance, and lightweight characteristics. EV battery systems generate heat that requires advanced engineered plastics capable of maintaining safety and structural integrity. Polyamide, polycarbonate blends, and reinforced thermoplastics are increasingly replacing metal parts in battery enclosures and charging systems.

Automotive manufacturers are also using lightweight compounded plastics to improve battery efficiency and extend vehicle range. For instance, EV platforms developed in China, Germany, and the United States incorporate advanced polymer compounds in dashboards, underbody shields, and electronic housings. Future EV architectures will require even more sophisticated materials for autonomous systems and connected mobility applications. This trend is expected to create strong long-term demand for specialty automotive plastic compounds with multifunctional properties.

Market Drivers

Growing Demand for Lightweight Vehicles

The need to improve vehicle fuel efficiency and reduce emissions is driving automakers toward lightweight materials. Automotive plastic compounds help manufacturers lower vehicle weight while maintaining structural performance and design flexibility. Plastic compounds are replacing steel and aluminum in bumpers, instrument panels, engine covers, and seating systems because they offer lower weight and reduced manufacturing costs.

For example, global automakers are increasingly using glass-fiber-reinforced polypropylene compounds in SUVs and electric cars to reduce fuel consumption and improve handling. Government fuel economy regulations in the United States, Europe, Japan, and China are encouraging OEMs to adopt lightweight polymer solutions across vehicle categories. As automotive emission standards become stricter, demand for engineered plastic compounds is expected to rise significantly over the next decade.

Expansion of Electric Vehicle Manufacturing

The rapid growth of electric vehicle manufacturing is supporting the expansion of the automotive plastic compounding market. EV manufacturers require lightweight and thermally stable materials to optimize battery efficiency and vehicle performance. Plastic compounds are widely used in battery housings, charging connectors, cooling systems, and electronic modules because they provide insulation and corrosion resistance.

China, Germany, and the United States continue to increase EV production capacity through investments in battery plants and automotive assembly facilities. Automotive suppliers are responding by developing flame-retardant and heat-resistant polymer compounds specifically designed for EV applications. As EV adoption expands globally, automotive compound manufacturers are expected to experience rising demand for specialized engineering plastics across passenger and commercial vehicle segments.

Market Restraint

Volatility in Raw Material Prices

Fluctuating prices of petrochemical-based raw materials remain a significant restraint for the automotive plastic compounding market. Automotive compounds are manufactured using polymers such as polypropylene, polyethylene, ABS, and polyamide, which are derived from crude oil and natural gas feedstocks. Variations in crude oil prices directly affect resin production costs and create pricing instability for compound manufacturers.

Supply chain disruptions and geopolitical tensions have also increased transportation and procurement costs for plastic producers. Smaller manufacturers often struggle to maintain stable margins during periods of raw material inflation. For example, sudden increases in polypropylene resin prices have affected the profitability of automotive suppliers in Asia and Europe. High material costs may delay procurement decisions by automotive OEMs and reduce adoption rates among price-sensitive vehicle manufacturers. In addition, rising environmental concerns regarding plastic waste are increasing regulatory pressure on traditional petrochemical-based compounds. These factors may limit short-term market expansion, especially in regions with strict sustainability regulations and volatile industrial production cycles.

Market Opportunities

Development of Bio-Based Automotive Compounds

The growing emphasis on sustainable mobility is creating strong opportunities for bio-based automotive plastic compounds. Manufacturers are developing compounds using renewable feedstocks such as corn starch, sugarcane derivatives, and plant-based polyesters to reduce carbon emissions associated with vehicle production. These materials are gaining attention in automotive interiors, door trims, and dashboard applications.

Automakers are increasingly seeking sustainable alternatives that meet performance requirements while supporting environmental targets. Bio-based compounds also help manufacturers improve brand positioning among environmentally conscious consumers. Future developments in biodegradable engineering plastics and recycled polymer blends are expected to create new revenue streams for compound manufacturers serving the automotive industry.

Rising Automotive Production in Emerging Economies

Emerging automotive manufacturing hubs such as India, Vietnam, Mexico, and Indonesia are creating major opportunities for automotive plastic compound suppliers. Rapid urbanization, rising disposable income, and expanding middle-class populations are increasing vehicle ownership rates in these countries. Automotive OEMs are investing in regional manufacturing facilities to reduce production costs and improve market access.

As vehicle production increases, demand for cost-effective and lightweight plastic compounds is expected to rise across interior, exterior, and structural applications. Governments in emerging economies are also supporting domestic automotive production through industrial incentives and infrastructure development programs. The expansion of local EV manufacturing ecosystems will further increase opportunities for specialized automotive compounds in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.7 Billion |

| Market Size in 2026 | USD 19.9 Billion |

| Market Size in 2034 | USD 33.8 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polypropylene compounds dominated the type segment with a 34.8% market share in 2024. These compounds are widely used in automotive interiors, dashboards, bumpers, and door trims because of their lightweight structure, chemical resistance, and cost efficiency. Polypropylene compounds offer excellent moldability and impact resistance, making them suitable for high-volume automotive production. Automotive manufacturers increasingly prefer polypropylene due to its compatibility with recyclable formulations and reduced processing costs. Passenger vehicle manufacturers in Asia Pacific and Europe are integrating polypropylene compounds into lightweight vehicle architectures to improve fuel efficiency and lower emissions. The material also supports design flexibility and aesthetic customization, making it suitable for modern vehicle interiors.

Polyamide compounds are projected to witness the fastest CAGR of 7.4% during the forecast period. These compounds are increasingly used in electric vehicle battery systems, under-the-hood applications, and structural automotive components because of their thermal stability and mechanical strength. Automotive OEMs are adopting reinforced polyamide compounds in high-temperature environments where durability and flame resistance are critical. The growth of electric mobility and connected vehicles is expected to increase demand for advanced polyamide formulations in electronic systems and charging components. Future innovations in lightweight reinforced polyamides will further support market growth across premium and performance vehicle segments.

By Material

Thermoplastic materials held the dominant market share of 63.5% in 2024 due to their flexibility, recyclability, and ease of processing. Thermoplastics are widely used in automotive manufacturing because they can be reshaped and recycled without significant performance degradation. Common automotive thermoplastics include polypropylene, ABS, polycarbonate, and thermoplastic elastomers. These materials are used in interior panels, exterior trims, engine covers, and electrical housings. Automotive manufacturers prefer thermoplastics because they reduce vehicle weight while maintaining structural performance and aesthetic appeal. The growing shift toward lightweight vehicle platforms is further strengthening demand for thermoplastic compounds across passenger and commercial vehicle categories.

Recyclable bio-based compounds are expected to grow at the fastest CAGR of 8.1% during the forecast period. Automakers are increasingly focusing on sustainability targets and lifecycle emission reduction strategies, driving adoption of eco-friendly polymer materials. Bio-based compounds derived from renewable feedstocks are gaining popularity in vehicle interiors and non-structural applications. Automotive manufacturers are also incorporating recycled plastics into EV production to support circular economy initiatives. Advances in bio-polymer processing and material durability are expected to improve commercial scalability and create new opportunities for sustainable automotive compound manufacturers.

By End-Use

Interior applications accounted for the largest share of 39.7% in 2024 because modern vehicles increasingly rely on lightweight and visually appealing interior systems. Automotive plastic compounds are extensively used in dashboards, seating structures, door trims, center consoles, and infotainment housings. Consumers are demanding enhanced comfort, durability, and premium aesthetics, encouraging automakers to integrate advanced polymer compounds into interior designs. Soft-touch thermoplastics and reinforced polymers are becoming common in mid-range and luxury vehicles. Automotive OEMs are also using lightweight plastic compounds to reduce cabin weight and improve fuel efficiency without compromising safety standards.

Electric vehicle components are projected to grow at the fastest CAGR of 8.6% during the forecast period. The rapid global expansion of EV manufacturing is increasing demand for high-performance compounds used in battery housings, thermal management systems, and charging connectors. These compounds provide electrical insulation, flame resistance, and lightweight properties that are essential for EV performance. Governments worldwide are supporting EV adoption through subsidies and infrastructure development, encouraging automakers to increase production capacity. Future demand for autonomous electric vehicles is expected to further accelerate innovation in advanced automotive plastic compounds.

Automotive Plastic Compounding Market Segmentations

By Type

- Polypropylene Compounds

- Polyamide Compounds

- Polycarbonate Compounds

- ABS Compounds

- Thermoplastic Elastomer Compounds

By Material

- Thermoplastics

- Thermosets

- Recyclable Bio-Based Compounds

By End-User

- Interior Applications

- Exterior Applications

- Under-the-Hood Components

- Electric Vehicle Components

Regional Analysis

North America

North America accounted for 24.8% of the automotive plastic compounding market share in 2025 and is projected to grow at a CAGR of 6.2% during the forecast period. The region benefits from strong automotive manufacturing infrastructure, increasing electric vehicle adoption, and growing investment in lightweight vehicle technologies. Automakers in the United States and Canada are focusing on reducing vehicle emissions through advanced polymer integration. Rising demand for SUVs and electric pickup trucks is increasing the use of reinforced thermoplastics in structural and interior systems. The presence of established automotive OEMs and material innovation companies further supports regional market growth.

The United States remains the dominant country in North America due to strong electric vehicle investments and increasing adoption of sustainable automotive materials. Major automakers are expanding EV manufacturing facilities and integrating lightweight compounds into battery enclosures and interior components. Growing demand for autonomous vehicle systems is also increasing the use of specialty polymers in electronic housings and sensor systems. Automotive suppliers are partnering with compound manufacturers to develop high-performance recyclable plastics that comply with evolving environmental standards.

Europe

Europe held 22.9% of the global automotive plastic compounding market in 2025 and is expected to expand at a CAGR of 6.4% through 2034. The region is characterized by stringent emission regulations and strong sustainability initiatives across the automotive sector. European automakers are increasing the use of lightweight polymer compounds to improve fuel efficiency and reduce carbon emissions. The market is also benefiting from rising investments in electric vehicle production and battery manufacturing. Demand for high-performance engineering plastics is increasing across luxury vehicles, commercial vehicles, and EV platforms.

Germany dominates the European market because of its strong automotive manufacturing ecosystem and advanced material research capabilities. German automakers are integrating reinforced thermoplastics into premium vehicle designs to improve durability and weight reduction. Increasing EV exports and government-backed green mobility initiatives are further accelerating market growth. Automotive suppliers across Germany are investing in recycled and bio-based compounds to support sustainable vehicle production and strengthen compliance with European environmental directives.

Asia Pacific

Asia Pacific dominated the automotive plastic compounding market with a 41.6% share in 2025 and is forecasted to grow at a CAGR of 7.3% during the forecast period. Rapid automotive production, rising urbanization, and growing electric vehicle adoption are major factors driving regional growth. China, India, Japan, and South Korea are expanding automotive manufacturing capacity and increasing demand for lightweight materials. Automotive plastic compounds are widely used in passenger cars, two-wheelers, and electric vehicles due to their cost efficiency and design flexibility. Rising disposable incomes and increasing vehicle ownership are also supporting market expansion across emerging Asian economies.

China remains the leading country in Asia Pacific due to its large-scale automotive production and dominant electric vehicle manufacturing sector. The country has become a major hub for battery-powered vehicle exports and advanced automotive component production. Chinese automakers are increasingly using engineered plastic compounds in EV battery systems and lightweight vehicle platforms. Government incentives for new energy vehicles and domestic material innovation are encouraging local manufacturers to expand polymer compounding capabilities. India is also emerging as a high-growth market because of increasing automotive assembly investments and rising demand for fuel-efficient vehicles.

Middle East & Africa

The Middle East & Africa region accounted for 5.8% of the automotive plastic compounding market in 2025 and is expected to register a CAGR of 5.9% through 2034. Growing automotive imports, infrastructure development, and increasing industrial diversification are supporting regional demand for automotive compounds. The region is witnessing increasing adoption of plastic-based vehicle components in commercial transportation and passenger vehicles. Demand for durable and heat-resistant materials is particularly strong due to harsh climatic conditions. Governments are also investing in manufacturing diversification strategies to reduce dependency on oil-based economies.

Saudi Arabia is the dominant country in the region because of expanding automotive assembly activities and industrial investment initiatives. The country is promoting local manufacturing under economic diversification programs, creating opportunities for automotive material suppliers. Demand for lightweight commercial vehicles and logistics transportation is increasing the use of compounded plastics in vehicle interiors and under-the-hood systems. The growing presence of regional automotive suppliers is expected to support long-term market development across the Middle East.

Latin America

Latin America represented 4.9% of the global automotive plastic compounding market in 2025 and is anticipated to grow at the fastest CAGR of 7.1% during the forecast period. Rising automotive manufacturing activity in Brazil and Mexico is increasing demand for cost-effective lightweight materials. Automotive OEMs are expanding regional production capacity to support domestic and export vehicle demand. Increasing urban mobility needs and improving industrial investment conditions are further supporting market growth. The market is also benefiting from rising demand for fuel-efficient passenger vehicles and affordable electric mobility solutions.

Brazil dominates the Latin American market due to its strong automotive manufacturing base and growing vehicle export industry. Local automakers are increasing the use of polypropylene and ABS compounds in compact vehicles and commercial transportation fleets. Demand for flexible and impact-resistant materials is rising as manufacturers focus on vehicle durability and production efficiency. Mexico is also attracting investments from global automotive suppliers due to its strategic trade position and expanding EV production ecosystem.

Competitive Landscape

The automotive plastic compounding market is moderately consolidated, with global players focusing on sustainable material development, EV-specific compounds, and regional production expansion. Companies are investing heavily in research and development to create lightweight, recyclable, and heat-resistant compounds for next-generation automotive applications.

BASF SE remains the market leader due to its broad engineering plastics portfolio and strong partnerships with automotive OEMs worldwide. The company focuses on lightweight EV materials and sustainable polymer technologies. SABIC is strengthening its market position through advanced thermoplastic solutions designed for electric mobility and autonomous vehicle systems. LyondellBasell Industries continues expanding its polypropylene compound production to meet growing automotive demand in Asia and North America.

Covestro AG is investing in polycarbonate and polyurethane innovations for lightweight vehicle structures and battery protection systems. DuPont focuses on high-performance polyamide compounds for EV thermal management and electronic applications. Strategic collaborations between automakers and compound manufacturers are becoming increasingly common as the industry moves toward sustainable mobility and smart vehicle technologies.

Key Players List

- BASF SE

- SABIC

- LyondellBasell Industries Holdings B.V.

- Covestro AG

- DuPont de Nemours Inc.

- Asahi Kasei Corporation

- Celanese Corporation

- LANXESS AG

- Mitsubishi Chemical Group Corporation

- RTP Company

- Borealis AG

- ExxonMobil Corporation

- Dow Inc.

- Teknor Apex Company

- Kingfa Science & Technology Co., Ltd.