Plastic Compounding Market Size and Growth

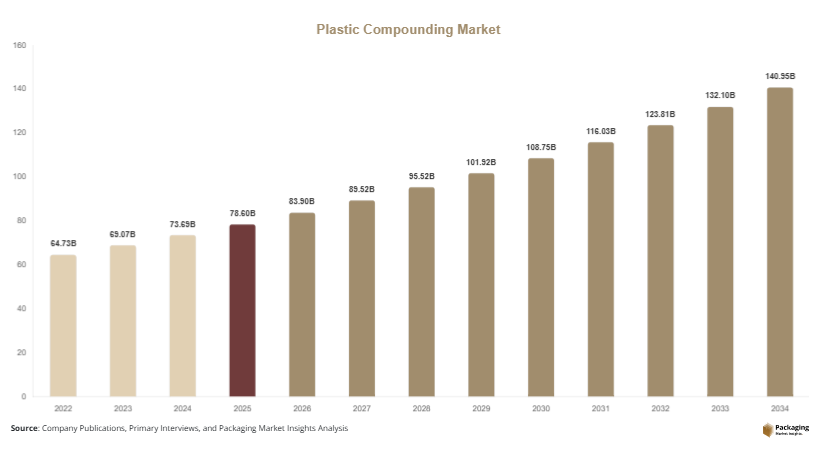

The global plastic compounding market was valued at USD 78.6 billion in 2025 and is projected to reach USD 83.9 billion in 2026. By 2034, the market is forecast to expand to USD 149.8 billion, registering a CAGR of 6.7% during 2025–2034. This expansion is being driven by rising industrial material substitution, increasing adoption of lightweight polymers in transportation, and growing customization needs across packaging and electronics manufacturing. One major growth factor is automotive electrification, where battery enclosures, thermal insulation components, and lightweight structural materials increasingly rely on engineered compounds. Another important driver is rapid infrastructure development, particularly in Asia Pacific and the Middle East, where compounded plastics are widely used in pipes, fittings, insulation panels, cable coatings, and modular building materials. A third major factor is the expansion of circular polymer processing, where recyclate-based compounds are being tailored for commercial and industrial use.

Healthcare and electronics applications are also contributing to growth. Medical-grade compounds with sterilization resistance are gaining wider adoption, while conductive compounds and flame-retardant formulations are expanding in advanced electrical systems. Increasing investments in compounding facilities near manufacturing hubs are improving production economics and enabling localized formulation development.

Key Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.5%.

- Polypropylene compounds led the type segment with a 31.8% share.

- Engineering plastics dominated the material segment with a 48.6% share.

- Automotive applications led the end-use segment with 28.7% share.

- The US remained the dominant country with a market size of USD 13.6 billion in 2025 and USD 14.4 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Recycled and Circular Polymer Compounds

A major trend shaping the plastic compounding market is the increasing adoption of recycled-content and circular polymer compounds across industrial sectors. Manufacturers are developing advanced formulations that incorporate post-industrial and post-consumer recycled plastics without significantly compromising performance. This shift is being supported by improved compatibilizers, stabilizers, and reinforcement additives that restore mechanical strength, thermal resistance, and processability. Packaging manufacturers are increasingly using recycled polypropylene compounds for rigid packaging applications, while automotive suppliers are incorporating recycled polyamide compounds in interior and semi-structural parts. This trend reduces raw material dependency, supports corporate sustainability targets, and aligns with tightening environmental regulations. Over the next decade, circular compounding will become a core growth pillar as industrial buyers prioritize lower-carbon material sourcing and recycled-content certification.

Rise of High-Performance Application-Specific Compounds

Another important trend is the development of highly customized application-specific compounds engineered for precise performance requirements. Industries increasingly require materials optimized for thermal stability, chemical resistance, electrical conductivity, lightweighting, flame retardancy, and dimensional consistency. Compounders are responding by creating targeted formulations for EV battery systems, medical devices, electronics miniaturization, and advanced industrial equipment. For example, conductive polymer compounds are gaining traction in electronic housings and EV charging systems, while glass-fiber reinforced engineering compounds are expanding in structural automotive applications. Precision compounding is improving manufacturing efficiency because end users receive ready-to-process material systems with predictable behavior. Future market growth will increasingly favor compounders that offer custom formulation capabilities rather than commodity-grade blended plastics.

Market Drivers

Increasing Lightweight Material Demand in Transportation

One of the strongest growth drivers in the plastic compounding market is rising demand for lightweight materials across automotive, aerospace, and commercial transportation sectors. Vehicle manufacturers are replacing heavier metal components with reinforced plastic compounds to improve fuel efficiency, increase electric vehicle range, and reduce emissions. Compounded plastics deliver weight savings while maintaining mechanical strength, corrosion resistance, and design flexibility. For instance, mineral-filled polypropylene compounds are widely used in dashboards and interior panels, while reinforced polyamide compounds are increasingly used in under-the-hood components requiring heat resistance. Electric vehicle battery systems are also expanding the use of flame-retardant engineering compounds. This shift is creating sustained long-term demand for specialized compounded materials globally.

Rapid Growth in Electrical and Electronics Manufacturing

The expansion of electrical and electronics manufacturing is another major driver fueling market growth. Plastic compounds are extensively used in wire insulation, switchgear, appliance housings, connectors, circuit protection systems, and semiconductor packaging support components. Flame-retardant compounds, conductive polymer blends, and heat-resistant engineered compounds are seeing particularly strong demand. Consumer electronics miniaturization is increasing the need for materials with dimensional precision and thermal management capability. Industrial automation systems are also boosting consumption of durable electrical-grade compounds. Countries expanding electronics manufacturing capacity, particularly in Asia Pacific, are generating strong regional demand for advanced compounded materials, supporting investments in specialty compounding production facilities.

Market Restraint

Volatility in Raw Material Pricing and Additive Costs

A major restraint affecting the plastic compounding market is volatility in raw polymer resin prices and specialty additive costs. Base polymers such as polypropylene, polyethylene, polyamide, ABS, and engineering thermoplastics are strongly influenced by crude oil price fluctuations, feedstock availability, and supply chain disruptions. In addition, specialty additives including flame retardants, UV stabilizers, impact modifiers, conductive fillers, and reinforcing fibers often face pricing pressure due to supply concentration and regulatory restrictions. This volatility creates uncertainty for compound manufacturers operating on tight industrial margins.

For example, sharp increases in polymer feedstock pricing can reduce profitability for long-term supply contracts where compound pricing is fixed. Automotive suppliers and packaging manufacturers often resist immediate price pass-through, forcing compounders to absorb short-term cost increases. Specialty compounds are particularly exposed because formulation complexity increases dependency on imported additives and engineered fillers. Supply disruptions in mineral fillers, glass fiber reinforcement materials, and specialty performance chemicals can also slow production cycles.

The restraint is especially visible in emerging markets where smaller compounders have limited procurement leverage. Many regional players struggle to maintain stable inventory economics, affecting competitiveness. While long-term supplier agreements and vertical integration strategies are helping large manufacturers manage this risk, raw material cost instability remains a structural challenge that may limit short-term market expansion.

Market Opportunities

Expansion of Electric Vehicle Material Ecosystems

Electric vehicle manufacturing presents a major opportunity for the plastic compounding market because EV platforms require highly specialized lightweight and thermally stable materials. Battery housings, cable systems, insulation layers, connectors, cooling modules, and charging infrastructure components increasingly depend on engineered compounds. Flame-retardant polyamide blends, conductive thermoplastics, and reinforced polypropylene compounds are seeing rising demand in EV manufacturing supply chains. As battery production scales globally, demand for compounds offering heat management, structural integrity, and chemical resistance will increase significantly. Compounders that develop EV-specific material platforms are likely to benefit from long-term supply contracts and strong volume growth.

Growth of Bio-Based and Hybrid Compound Formulations

The growing market for bio-based polymers and hybrid sustainable formulations offers another strong opportunity. Compound manufacturers are increasingly blending renewable feedstocks, recycled plastics, natural fibers, and specialty additives to create lower-carbon alternatives for conventional plastic materials. Wood-plastic composites, cellulose-reinforced thermoplastics, and starch-based blended compounds are finding applications in packaging, furniture, construction, and consumer products. Large brands are testing hybrid compounds that maintain industrial durability while reducing fossil-based resin content. Over time, sustainability-driven product differentiation will expand premium compound categories, creating new revenue opportunities for innovation-focused manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.6 Billion |

| Market Size in 2026 | USD 83.9 Billion |

| Market Size in 2034 | USD 149.8 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polypropylene compounds dominated the plastic compounding market in 2024 with a 31.8% market share. Their dominance is primarily linked to broad industrial versatility, cost efficiency, lightweight characteristics, and excellent processability across injection molding, extrusion, and thermoforming applications. Polypropylene compounds are extensively used in automotive interiors, appliance housings, packaging systems, furniture components, battery casings, and consumer products. Their compatibility with mineral fillers, glass fiber reinforcement, impact modifiers, and colorants allows manufacturers to tailor properties for specific applications. Automotive OEMs continue to prefer polypropylene compounds for interior trims and lightweight structural applications due to their balance of durability and economics. Packaging manufacturers also favor these compounds because they offer strong chemical resistance and recyclability.

Thermoplastic elastomer (TPE) compounds are the fastest-growing type segment and are projected to expand at a CAGR of 7.9% through 2034. Their growth is driven by rising demand for flexible yet durable materials across healthcare, consumer goods, automotive sealing systems, wearable electronics, and soft-touch product designs. TPE compounds provide elasticity similar to rubber while maintaining thermoplastic processing efficiency, enabling large-scale manufacturing flexibility. Their recyclability is improving sustainability appeal, while innovations in bio-based TPE formulations are widening application potential. Demand for lightweight vibration-dampening materials in EV manufacturing and flexible cable insulation systems will further support long-term segment expansion.

By Material

Engineering plastics led the material segment in 2024 with a 48.6% share, driven by increasing industrial reliance on high-performance compounds capable of withstanding mechanical stress, heat exposure, and chemical environments. Materials such as polyamide, polycarbonate, ABS blends, PBT compounds, and specialty reinforced polymers are widely used in electrical systems, industrial machinery, automotive under-the-hood applications, and medical equipment. Their superior dimensional stability and strength-to-weight ratio make them suitable replacements for metal in precision applications. For instance, reinforced nylon compounds are increasingly used in cooling systems and structural automotive parts, while polycarbonate blends dominate electrical housings and transparent durable components. Strong growth in electronics and industrial automation is reinforcing segment dominance.

Recycled polymer compounds are forecast to be the fastest-growing material segment at a CAGR of 8.4% during the forecast period. Demand is accelerating as industries seek lower-carbon materials without sacrificing processing performance. Advances in polymer sorting, odor reduction, contamination control, and additive stabilization are improving the quality of recycled compounds. Packaging companies, furniture manufacturers, and appliance producers are increasingly specifying recycled-content compounds in procurement contracts. Automotive interior applications are also adopting recycled polypropylene and recycled ABS compounds. As circular manufacturing expands globally, recycled compounds are expected to shift from value-driven substitutes to strategically preferred industrial materials.

By End-Use

Automotive dominated the end-use segment in 2024 with a 28.7% market share, supported by the sector’s continuous push toward lightweighting, energy efficiency, design flexibility, and component integration. Compounded plastics are extensively used in dashboards, door panels, underbody shields, air intake systems, cable insulation, battery modules, and thermal management components. Reinforced engineering plastics increasingly replace metals in semi-structural parts due to corrosion resistance and easier processing. EV adoption is broadening demand for flame-retardant and conductive specialty compounds. Vehicle manufacturers are also integrating recycled-content compounds into interiors to meet sustainability targets. This broad material requirement keeps automotive at the center of global compound demand.

Electrical & electronics is projected to be the fastest-growing end-use segment, expanding at a CAGR of 7.6% through 2034. Growth is driven by consumer electronics expansion, smart appliances, industrial electrification, data infrastructure investment, and renewable energy systems. High-performance compounds are increasingly required for connectors, insulation layers, control panels, semiconductor support structures, battery management systems, and thermal-resistant housings. Flame-retardant halogen-free compounds are seeing wider use due to regulatory requirements, while conductive compounds are growing in high-density electronic assemblies. Increasing electrification across industrial equipment and mobility infrastructure will continue to create strong long-term demand.

Plastic Compounding Market Segmentations

By Type

- Polypropylene Compounds

- Thermoplastic Elastomer Compounds

- Polyamide Compounds

- Polycarbonate Compounds

- PVC Compounds

- Specialty Compounds

By Material

- Engineering Plastics

- Commodity Plastics

- High-Performance Plastics

- Recycled Polymer Compounds

- Bio-Based Polymer Compounds

By End-User

- Automotive

- Electrical & Electronics

- Packaging

- Construction

- Consumer Goods

- Healthcare

- Industrial Equipment

Regional Analysis

North America

North America accounted for 23.8% of the plastic compounding market share in 2025 and is projected to expand at a CAGR of 5.9% through 2034. The region maintains a mature industrial polymer ecosystem supported by advanced automotive manufacturing, aerospace engineering, packaging innovation, and high-value electronics production. Demand for specialty compounds is rising due to increasing adoption of lightweight materials in transportation and growing need for flame-retardant and conductive compounds in electrical systems. The U.S. and Canada are also seeing increased use of recycled-content compounds as sustainability targets reshape procurement patterns. Investment in domestic polymer processing capacity and additive manufacturing-compatible compounds is further strengthening regional market depth.

The United States remains the dominant country in North America, supported by its extensive manufacturing base and strong research capabilities in advanced materials science. A unique growth driver in the U.S. is the rapid expansion of EV battery manufacturing clusters, where compounded plastics are increasingly used in battery casings, insulation systems, thermal barriers, and charging infrastructure. Automotive OEM partnerships with material suppliers are accelerating innovation in reinforced engineering compounds. In addition, industrial reshoring is creating fresh demand for localized compound development, particularly in specialty medical, aerospace, and industrial automation applications.

Europe

Europe represented 25.4% of the global plastic compounding market in 2025 and is expected to register a CAGR of 6.1% during the forecast period. The regional market is characterized by strong regulatory influence, circular economy policies, and widespread adoption of engineered compounds in automotive, electrical infrastructure, and industrial manufacturing. Demand is increasingly shifting toward recyclable compounds, halogen-free flame-retardant materials, and low-emission polymer systems. Construction modernization and renewable energy infrastructure are also contributing to higher demand for cable compounds, pipe compounds, and weather-resistant polymer blends. Europe’s packaging sector is gradually integrating high-performance recycled compounds in rigid and flexible formats.

Germany leads the European market due to its dominant automotive supply chain, industrial equipment manufacturing, and polymer engineering expertise. A unique growth driver in Germany is the rapid integration of high-performance thermoplastic compounds into industrial machinery electrification. Advanced robotics, smart manufacturing systems, and modular industrial electronics increasingly rely on conductive, durable, and lightweight compounds with long operational lifecycles. German manufacturers are also accelerating development of bio-based engineering compounds for industrial-grade applications, reinforcing Europe’s innovation-driven compounding ecosystem.

Asia Pacific

Asia Pacific dominated the plastic compounding market with a 39.1% share in 2025 and is projected to grow at a CAGR of 7.2% through 2034. Rapid industrialization, strong packaging demand, infrastructure development, and expanding manufacturing capacity continue to position the region as the largest global consumer of compounded plastics. Construction compounds, automotive-grade plastics, consumer electronics materials, and packaging compounds are all witnessing robust demand growth. Regional governments are investing heavily in domestic chemical processing, industrial parks, and manufacturing localization, which is supporting large-scale compounding capacity expansion. The rise of smart appliances and industrial automation systems is also driving specialty polymer demand.

China remains the dominant country in Asia Pacific due to its massive manufacturing output and integrated petrochemical value chain. A unique growth driver in China is the expansion of high-speed electronics manufacturing, where precision plastic compounds are increasingly used in connectors, protective casings, thermal insulation systems, and semiconductor support components. Local material producers are scaling advanced compounding facilities focused on engineered polymers and recycled-content compounds. In addition, China’s rapid EV manufacturing expansion is generating substantial demand for structural and flame-resistant specialty compounds across battery systems and vehicle interiors.

Middle East & Africa

The Middle East & Africa accounted for 6.8% of the plastic compounding market in 2025 and is forecast to grow at a CAGR of 6.4% during 2025–2034. The market is expanding steadily as petrochemical diversification strategies encourage downstream plastics manufacturing across Gulf economies. Demand is increasing in packaging, infrastructure pipes, wire insulation, industrial coatings, and lightweight construction materials. Rising urbanization in major African economies is also boosting demand for compounded plastics in consumer goods, water management systems, and electrical installations. Industrial parks focused on polymer conversion and regional logistics advantages are attracting investment in local compounding facilities.

Saudi Arabia is the dominant country in the region, supported by abundant feedstock access, strong petrochemical infrastructure, and industrial diversification initiatives. A unique growth driver is the rapid development of large-scale modular construction projects that require durable compounded plastics for piping systems, insulation materials, cable sheathing, and architectural panels. The country is also increasing production of specialty polymer compounds designed for harsh climatic conditions, including UV-resistant and heat-stable materials suited for outdoor infrastructure applications, creating specialized regional demand.

Latin America

Latin America held 4.9% of the plastic compounding market share in 2025 and is expected to record the fastest CAGR of 7.5% through 2034. Market growth is being supported by rising industrialization, packaging demand, automotive assembly expansion, and infrastructure modernization. Food packaging, agricultural films, electrical insulation compounds, and lightweight industrial materials are seeing rising adoption across key economies. Increased foreign investment in regional manufacturing and expanding domestic conversion industries are strengthening local compound demand. Governments are also promoting recycling ecosystems, which is increasing opportunities for circular polymer compounds in packaging and consumer goods applications.

Brazil remains the dominant country in Latin America due to its large industrial base and expanding plastics conversion sector. A unique growth driver in Brazil is the rapid growth of agricultural plastics and equipment manufacturing, where compounded materials are increasingly used in irrigation systems, greenhouse films, storage systems, and lightweight machinery components. Bio-based resin blending is also gaining traction due to Brazil’s strong agricultural feedstock availability, supporting innovation in hybrid sustainable compounds for commercial industrial use.

Competitive Landscape

The plastic compounding market is moderately consolidated, with global leaders competing on formulation innovation, geographic expansion, sustainability integration, and application-specific material development. LyondellBasell Industries remains the market leader due to its broad polymer portfolio, advanced compounding capabilities, and strong relationships across automotive, packaging, and industrial manufacturing sectors. The company continues investing in circular polymer technologies and recycled compound development to strengthen its market position.

BASF SE focuses on engineered compounds designed for automotive electrification, industrial durability, and sustainable processing systems. SABIC is expanding specialty polymer compounds with improved heat resistance and lightweight performance for electronics and mobility applications. Dow Inc. is increasingly emphasizing advanced recyclable compounds and high-performance packaging material systems. Covestro AG remains active in specialty polycarbonate compounds and lightweight industrial materials.

Competitive strategies include acquisition of regional compounders, vertical integration into recycling feedstocks, development of bio-based formulations, and creation of EV-specific material platforms. Companies are also establishing localized technical centers near manufacturing hubs to accelerate custom compound development and shorten customer lead times.

Key Players List

- LyondellBasell Industries

- BASF SE

- SABIC

- Dow Inc.

- Covestro AG

- RTP Company

- Asahi Kasei Corporation

- Celanese Corporation

- Mitsubishi Chemical Group

- Avient Corporation

- Ravago Manufacturing

- Teknor Apex Company

- LANXESS AG

- Borealis AG

- ExxonMobil Chemical

- DuPont

- Solvay

- Kingfa Science & Technology