Business To Business (B2B) Packaging Market Size and Growth

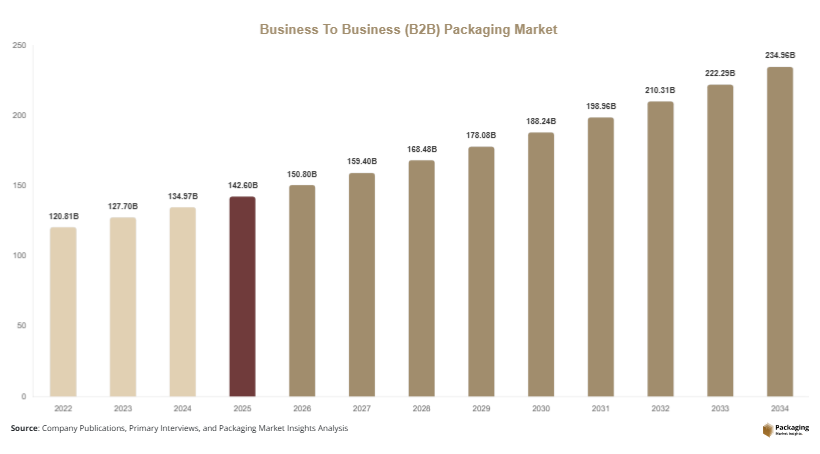

The global business to business (B2B) packaging market size is estimated at USD 142.6 billion in 2025 and is projected to reach USD 150.8 billion in 2026, driven by increased industrial output, rising cross-border logistics, and growing demand for protective and bulk packaging solutions. Over the forecast period 2025–2034, the market is expected to reach approximately USD 245.3 billion by 2034, registering a CAGR of 5.7%. The Business To Business B2B Packaging Market is experiencing consistent expansion as global trade, industrial supply chains, and manufacturing activities continue to scale.

One of the key growth factors is the expansion of global manufacturing and industrial production. Industries such as automotive, chemicals, electronics, and machinery rely heavily on standardized packaging formats for safe transportation and storage of raw materials and finished goods. B2B packaging plays a critical role in reducing product damage and optimizing supply chain efficiency.

Key Highlights:

The market size reached USD 142.6 billion in 2025 and is projected to reach USD 245.3 billion by 2034, reflecting steady expansion across global industrial supply chains. Growth is supported by increasing demand for efficient bulk handling and B2B distribution packaging systems.

It is expected to grow at a CAGR of 5.7% during 2025–2034, driven by continuous expansion in manufacturing output and cross-border logistics activities. The growth rate also reflects rising investments in industrial packaging automation and smart supply chain integration.

Strong demand from manufacturing, logistics, and industrial sectors continues to be a primary growth driver. These sectors rely heavily on durable, standardized packaging solutions for safe transportation and storage of bulk goods.

Rising adoption of reusable and sustainable packaging systems is reshaping procurement strategies across enterprises. Companies are increasingly shifting toward returnable packaging models to reduce operational costs and environmental impact.

Increasing use of smart tracking and automated packaging solutions is enhancing supply chain visibility and efficiency. Technologies such as RFID tagging, IoT-enabled packaging, and automated handling systems are becoming more common in large-scale B2B operations.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Returnable and Reusable Packaging Systems

A significant trend in the B2B packaging market is the increasing adoption of returnable and reusable packaging solutions. Industries are moving away from single-use packaging formats toward durable materials such as plastic pallets, metal containers, and reinforced bulk boxes. This shift is primarily driven by cost optimization and sustainability goals. Large manufacturers and logistics providers are investing in closed-loop packaging systems that allow repeated use across supply chains. These systems reduce packaging waste, improve operational efficiency, and lower long-term procurement costs. Automotive and electronics industries, in particular, are leading this transition due to their high-volume and high-value logistics requirements.

Integration of Smart Tracking and Digital Packaging Technologies

Another major trend is the integration of digital technologies such as RFID tags, QR codes, and IoT-enabled tracking systems into B2B packaging solutions. These technologies enable real-time visibility of shipments, improve inventory management, and enhance supply chain transparency. Companies are increasingly adopting smart packaging systems to reduce losses, prevent theft, and optimize logistics performance. The trend is especially strong in pharmaceuticals, chemicals, and high-value electronics industries, where tracking accuracy and regulatory compliance are critical. This digital transformation is reshaping traditional packaging into an intelligent supply chain asset.

Market Drivers

Expansion of Global Industrial and Manufacturing Activities

The steady expansion of industrial production across both developed and emerging economies is a key driver of the B2B packaging market. Manufacturing sectors such as automotive, machinery, chemicals, and electronics require reliable bulk packaging solutions for raw materials and finished goods. As global supply chains become more interconnected, the demand for standardized and durable packaging formats continues to increase. B2B packaging ensures product safety during transportation and storage, reducing losses and improving efficiency across logistics networks.

Growth of Global Trade and Logistics Networks

The rapid expansion of global trade and logistics infrastructure is another major growth driver. The rise of e-commerce B2B platforms, third-party logistics providers, and international shipping networks has increased the need for standardized packaging solutions. Packaging formats such as pallets, drums, crates, and containers are essential for efficient bulk transportation. The growing complexity of supply chains has further increased reliance on durable and reusable packaging systems that support large-scale industrial distribution.

Market Restraint

High Initial Investment for Reusable Packaging Systems

One of the key restraints in the B2B packaging market is the high initial investment required for reusable and smart packaging systems. While these solutions offer long-term cost savings, industries must invest significantly in durable materials, tracking technologies, and reverse logistics infrastructure.

This cost barrier limits adoption among small and medium-sized enterprises, particularly in developing regions. For example, implementing returnable packaging systems in automotive supply chains requires investment in tracking software, storage systems, and container management infrastructure, which increases upfront operational expenses.

Market Opportunities

Expansion of Sustainable Industrial Packaging Solutions

The growing emphasis on sustainability presents a major opportunity for the B2B packaging market. Companies are increasingly adopting recyclable, biodegradable, and reusable packaging materials to meet environmental regulations and corporate ESG goals. Industrial sectors are transitioning toward eco-friendly bulk packaging solutions that reduce carbon footprint and waste generation. This shift is expected to drive innovation in material science and packaging design, creating opportunities for advanced fiber-based and hybrid packaging systems.

Growth of Emerging Industrial Economies

Emerging economies in Asia Pacific, Latin America, and Africa present strong growth opportunities due to rapid industrialization and infrastructure development. Expanding manufacturing bases and logistics networks in these regions are increasing demand for standardized B2B packaging solutions. Government investments in industrial corridors, export zones, and supply chain modernization are further supporting market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 142.6 Billion |

| Market Size in 2026 | USD 150.8 Billion |

| Market Size in 2034 | USD 245.3 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

Pallets dominated the B2B packaging market in 2024, accounting for approximately 37% share. Their dominance is driven by widespread use across logistics, warehousing, FMCG, and manufacturing sectors. Pallets provide structural stability, ease of handling, and compatibility with automated storage systems, making them essential for bulk transportation and industrial supply chains. Their standardized design also supports global trade efficiency and reduces handling costs across long-distance logistics operations.

Intermediate Bulk Containers (IBCs) are expected to be the fastest-growing subsegment, expanding at a CAGR of 6.8%. Growth is driven by rising demand for safe, efficient, and reusable packaging solutions for liquid and granular materials in chemical, food, and pharmaceutical industries. Increasing focus on reducing leakage risks and improving bulk handling efficiency is further accelerating adoption of IBC systems.

By Material Type

Plastic-based packaging dominated in 2024 with approximately 44% share, supported by its durability, lightweight properties, and reusability in industrial applications. It is widely used across automotive, FMCG, and logistics sectors due to its cost efficiency and ability to withstand multiple handling cycles in supply chains.

Metal packaging is expected to be the fastest-growing segment, registering a CAGR of 6.3%. Growth is driven by increasing demand in chemical, oil & gas, and heavy industrial sectors where high durability, corrosion resistance, and safety compliance are essential for bulk transport and storage.

By End-Use Industry

Manufacturing dominated in 2024 with approximately 40% share, driven by strong demand from automotive, machinery, electronics, and industrial equipment sectors. These industries rely heavily on standardized packaging solutions to ensure safe storage and efficient transportation of components and finished goods.

Pharmaceuticals and chemicals are expected to be the fastest-growing segment, expanding at a CAGR of 6.9%. Growth is driven by strict regulatory requirements for safe handling, contamination prevention, and secure transportation of sensitive materials across global supply chains.

Business To Business (B2B) Packaging Market Segmentations

Product Type

- Pallets

- Intermediate Bulk Containers (IBCs)

- Crates and Containers

- Protective Industrial Packaging

- Corrugated Bulk Boxes

Material Type

- Plastic-based Packaging

- Metal Packaging

- Paper & Paperboard Packaging

- Wood Packaging

- Composite Materials

End-Use Industry

- Manufacturing

- Food & Beverage

- Pharmaceuticals & Chemicals

- Retail & E-commerce

- Automotive & Industrial Goods

Regional Analysis

North America

North America accounted for approximately 29% market share in 2025, with a projected CAGR of 5.6% during 2025–2034. The region benefits from advanced logistics infrastructure, strong manufacturing output, and high adoption of smart supply chain solutions across industrial sectors.

The United States dominates the regional market due to its large-scale industrial base and developed warehousing network. A key growth factor is the rapid integration of IoT-enabled tracking systems and automated warehouse packaging solutions across manufacturing and logistics operations.

Europe

Europe held approximately 28% market share in 2025, with a projected CAGR of 5.9% during the forecast period. The region is strongly influenced by sustainability regulations, circular economy policies, and strict industrial packaging standards.

Germany leads the European market due to its strong automotive and chemical manufacturing industries. A key growth factor is the EU’s circular economy framework, which is driving widespread adoption of reusable and returnable packaging systems across industrial supply chains.

Asia Pacific

Asia Pacific accounted for approximately 33% market share in 2025, with the highest CAGR of 6.4%. Growth is driven by rapid industrialization, expanding export-oriented manufacturing, and increasing logistics infrastructure investments.

China dominates the region due to its large-scale manufacturing ecosystem. A key growth factor is the expansion of cross-border trade and industrial supply chains supported by government-backed logistics and industrial corridor development.

Middle East & Africa

The region held approximately 6% market share in 2025, with a projected CAGR of 5.3%. Growth is supported by infrastructure development, rising industrial diversification, and expansion of logistics hubs.

The United Arab Emirates leads the region due to its strong re-export and logistics infrastructure. A key growth factor is increasing investment in industrial zones and trade facilitation projects that enhance packaging demand across supply chains.

Latin America

Latin America accounted for approximately 4% market share in 2025, with a projected CAGR of 5.5%. Growth is driven by FMCG expansion, industrial modernization, and increasing trade activity.

Brazil dominates the region due to its large manufacturing and agricultural export base. A key growth factor is rising adoption of standardized industrial packaging solutions to improve export efficiency and reduce logistics losses.

Competitive Landscape

The B2B packaging market is highly competitive, with companies focusing on durability, sustainability, and smart logistics integration. Key players are investing in reusable packaging systems, automation, and digital tracking technologies.

International Paper is a leading player in the market, supported by its extensive industrial packaging portfolio. Recently, the company expanded its reusable packaging solutions division to support logistics and manufacturing clients seeking sustainable supply chain optimization.

Key Players List

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- Sonoco Products Company

- Packaging Corporation of America

- Greif Inc.

- Berry Global Group

- Amcor Plc

- Sealed Air Corporation

- Huhtamaki Oyj

- Mauser Packaging Solutions

- Schoeller Allibert

- Nefab Group