Tertiary Packaging Market Size and Growth

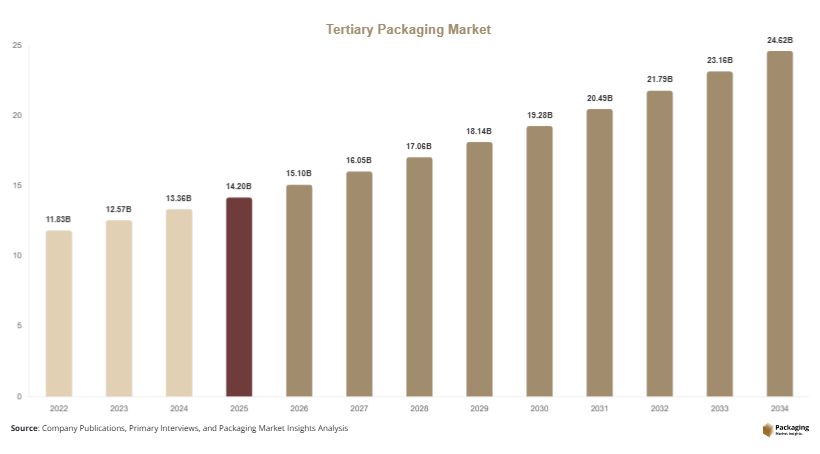

The global tertiary packaging market size is estimated at USD 14.2 billion in 2025, rising to USD 15.1 billion in 2026. By 2034, the market is projected to reach approximately USD 24.8 billion, registering a CAGR of 6.3% during 2025–2034. Growth is strongly supported by increasing demand for bulk handling efficiency, logistics optimization, and protection of goods during long-distance transportation. The tertiary packaging market is experiencing steady expansion as global supply chains become more complex and trade volumes increase across manufacturing, retail, and e-commerce ecosystems.

One of the most significant growth factors is the rapid expansion of global trade networks. As industries such as automotive, electronics, FMCG, and pharmaceuticals expand internationally, the need for standardized bulk packaging solutions such as corrugated boxes, pallets, stretch films, and reusable containers has increased. These solutions help streamline logistics operations and reduce product damage during multi-stage transportation.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Corrugated boxes led the type segment with a 30.1% share.

- Paper-based packaging dominated with a 52.3% share.

- Retail & e-commerce logistics led the segment with 44.2% share.

- The US remained the dominant country with a market size of USD 4.8 billion in 2025 and USD 5.1 billion in 20

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Reusable and Returnable Packaging Systems

A major trend shaping the tertiary packaging market is the increasing adoption of reusable and returnable packaging systems. Industries such as automotive, electronics, and large-scale retail are transitioning from single-use corrugated boxes and wooden pallets to durable plastic crates, foldable containers, and modular packaging systems. These reusable systems are designed for multiple cycles of use, significantly reducing packaging waste and operational costs. For example, automotive manufacturers in Germany and Japan use standardized reusable containers to transport components between suppliers and assembly plants. This reduces dependency on disposable packaging and enhances logistics efficiency. Over time, this trend is expected to strengthen as companies move toward circular supply chain models.

Integration of Smart Logistics and Digital Tracking Technologies

Another key trend is the integration of digital technologies such as RFID tagging, IoT sensors, and AI-based logistics platforms into tertiary packaging systems. These technologies allow real-time tracking of bulk shipments, improving visibility and reducing losses during transportation. Warehouses are increasingly adopting automated palletizing systems that can identify, sort, and route packages without manual intervention. For instance, large e-commerce fulfillment centers use smart pallets equipped with tracking chips to manage thousands of shipments daily. This trend is improving operational efficiency and enabling predictive logistics planning, which is expected to transform global supply chain operations.

Market Drivers

Expansion of Global E-commerce and Retail Logistics

The rapid growth of e-commerce platforms is a key driver of the tertiary packaging market. Online retail requires efficient bulk packaging systems to consolidate large volumes of individual orders into transport-ready shipments. Tertiary packaging solutions such as corrugated boxes, stretch wraps, and pallets ensure safe handling during long-distance and last-mile delivery. For example, global e-commerce companies operate highly automated distribution centers where tertiary packaging plays a crucial role in sorting and consolidating goods. As consumer demand for fast delivery continues to increase, the need for efficient packaging systems will grow significantly.

Industrial Manufacturing and Export Growth

The expansion of industrial manufacturing and global export activities is another important driver. Industries such as automotive, electronics, and consumer goods rely heavily on tertiary packaging for transporting finished goods and components across international markets. These industries require robust packaging solutions that can withstand multiple handling points and long transit durations. For instance, electronics manufacturers in China and South Korea use reinforced corrugated packaging and palletized shipping systems to ensure product safety during export. Increasing globalization of supply chains continues to drive demand for tertiary packaging solutions.

Market Restraint

Volatility in Raw Material Prices and Supply Chain Disruptions

A key restraint affecting the tertiary packaging market is the volatility in raw material prices, particularly for paper, wood, and plastic. These materials form the backbone of packaging products such as corrugated boxes and pallets. Price fluctuations caused by supply chain disruptions, energy costs, and environmental regulations directly impact production costs. For example, during periods of global supply chain instability, the price of recycled paper fiber can increase significantly, affecting corrugated packaging manufacturers. This creates cost unpredictability for both manufacturers and end users. Additionally, dependency on natural resources exposes the industry to regulatory constraints and sustainability pressures, limiting long-term pricing stability.

Market Opportunities

Rising Demand for Sustainable Packaging Solutions

Sustainability is creating strong growth opportunities in the tertiary packaging market. Companies are increasingly adopting recyclable, biodegradable, and lightweight materials to meet environmental regulations and corporate sustainability goals. Paper-based pallets, recycled corrugated boards, and bio-composite packaging materials are gaining traction across industries. For example, FMCG companies are shifting toward fully recyclable bulk packaging systems to reduce environmental impact. Governments across Europe and North America are also enforcing stricter packaging waste regulations, encouraging adoption of sustainable alternatives. This shift is expected to create long-term opportunities for innovation in eco-friendly packaging technologies.

Growth of Smart Warehousing and Automated Logistics Systems

The development of smart warehouses and automated logistics systems is another major opportunity. The integration of robotics, AI, and IoT in supply chain operations is increasing demand for intelligent packaging solutions. Tertiary packaging systems are being designed to work seamlessly with automated storage and retrieval systems (AS/RS). For instance, automated distribution centers use sensor-enabled pallets to track inventory movement in real time. This improves efficiency, reduces labor costs, and minimizes errors. As digital transformation accelerates across logistics industries, demand for smart-compatible packaging systems is expected to grow significantly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.2 Billion |

| Market Size in 2026 | USD 15.1 Billion |

| Market Size in 2034 | USD 24.8 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Corrugated boxes dominated the tertiary packaging market in 2024 with a 32.5% share due to their cost-effectiveness, recyclability, and versatility across industries. They are widely used in retail, FMCG, and e-commerce logistics for bulk shipment consolidation. Their lightweight structure combined with high stacking strength makes them ideal for warehouse storage and long-distance transportation. For example, global e-commerce companies rely heavily on corrugated cartons to consolidate multiple secondary packages into single shipments, improving logistics efficiency.

Reusable plastic containers are the fastest-growing subsegment with a CAGR of 6.6%. Their durability and long lifecycle make them ideal for automotive and industrial logistics. Companies are increasingly adopting closed-loop systems where containers are returned, cleaned, and reused multiple times. This reduces long-term packaging costs and supports sustainability goals. The adoption of automated return logistics systems is expected to further accelerate this segment.

By Material

Paper-based materials dominated the market in 2024 with a 51.8% share due to their widespread use in corrugated packaging systems. Their recyclability and cost efficiency make them the preferred choice for retail and e-commerce sectors. Paper-based packaging is also supported by regulatory policies promoting sustainable packaging practices.

Hybrid materials are the fastest-growing segment with a CAGR of 5.8%. These materials combine paper, plastic, and reinforced fibers to enhance strength and durability. They are increasingly used in high-value industrial shipments requiring enhanced protection during transit. The growing demand for lightweight yet strong packaging solutions is expected to drive this segment further.

By End-Use

Retail & e-commerce dominated the market in 2024 with a 45.3% share due to rising online shopping activity and warehouse consolidation needs. Tertiary packaging plays a critical role in aggregating individual orders into bulk shipments for efficient distribution. Large fulfillment centers rely heavily on palletized systems and corrugated packaging for daily operations.

Industrial manufacturing is the fastest-growing segment with a CAGR of 6.2%, driven by global supply chain expansion. Automotive and electronics industries require robust packaging systems for transporting components across international markets. Increasing automation in manufacturing logistics is further boosting demand for advanced tertiary packaging solutions.

Tertiary Packaging Market Segmentations

By Type

- Corrugated Boxes

- Wooden Pallets

- Plastic Containers

- Shrink Wraps

By Material

- Paper-Based Packaging

- Plastic Packaging

- Wood-Based Packaging

- Hybrid Materials

By End-Use

- Retail & E-commerce

- Industrial Manufacturing

- Food & Beverage Logistics

- Pharmaceuticals

By Region

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Regional Analysis

North America

North America accounted for approximately 28.6% of the tertiary packaging market in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. The region benefits from highly developed logistics infrastructure, strong retail networks, and rapid adoption of warehouse automation technologies. Growth is further supported by the expansion of e-commerce giants and increasing demand for efficient bulk shipment consolidation across industries such as FMCG, automotive, and pharmaceuticals.

The United States dominates the regional market due to its advanced distribution systems and strong consumption base. A key growth driver is the widespread adoption of omnichannel retailing, where companies integrate physical stores with online platforms. This has increased the need for standardized tertiary packaging systems that can efficiently support both retail and direct-to-consumer logistics operations. For example, large retail chains in the U.S. use automated pallet systems to manage high-volume distribution across national networks.

Europe

Europe held a 24.1% share in 2025 and is expected to grow at a CAGR of 5.6%. The region places strong emphasis on sustainability and circular economy initiatives, which significantly influence packaging trends. Demand for reusable pallets, recyclable corrugated boxes, and eco-friendly bulk packaging solutions is increasing across industries.

Germany leads the European market due to its strong industrial manufacturing base. A key growth factor is the automotive sector’s reliance on returnable packaging systems for cross-border component transport. For example, automotive suppliers in Germany and France use standardized reusable containers to optimize supply chain efficiency and reduce packaging waste across production networks.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is expected to grow at a CAGR of 6.8%. Rapid industrialization, export-driven economies, and expanding e-commerce platforms are major growth drivers. The region also benefits from large-scale manufacturing hubs and increasing investments in logistics infrastructure.

China is the leading country, supported by its massive export-oriented manufacturing sector. A key driver is the expansion of cross-border e-commerce logistics networks. For instance, Chinese fulfillment centers use advanced palletizing systems and automated packaging lines to manage international shipments efficiently, boosting demand for tertiary packaging solutions.

Middle East & Africa

The region accounted for 5.2% of the market in 2025 and is projected to grow at a CAGR of 6.0%. Growth is driven by increasing trade activities, infrastructure development, and rising demand for imported goods.

The UAE leads the region due to its strategic position as a global logistics hub. A key growth driver is re-export trade activity, where goods are imported, repackaged, and exported to other regions. This requires efficient bulk packaging systems to maintain product integrity during transit.

Latin America

Latin America held a 4.7% share in 2025 and is expected to grow at the fastest CAGR of 6.9%. Growth is driven by rising industrial production, agricultural exports, and expanding retail infrastructure.

Brazil dominates the region due to its strong agro-export economy. A key driver is increasing demand for palletized agricultural shipments, particularly for coffee, soybeans, and meat exports, requiring durable tertiary packaging systems for long-distance transport.

Competitive Landscape

The tertiary packaging market is moderately consolidated with major players focusing on sustainability, automation, and material innovation. International Paper Company is a leading player due to its strong global corrugated packaging network and sustainable product offerings. The company continues to expand its recycled fiber-based packaging solutions to meet growing environmental regulations.

Other key players include WestRock, Smurfit Kappa, DS Smith, and Mondi Group. These companies are investing in automation technologies, lightweight materials, and circular economy packaging models. Strategic mergers, acquisitions, and partnerships are also common strategies to expand geographic presence and strengthen supply chain capabilities.

Key Players List

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- Packaging Corporation of America

- Georgia-Pacific LLC

- Rengo Co. Ltd.

- Oji Holdings Corporation

- Sonoco Products Company

- Menasha Corporation

- UFP Industries

- Nefab Group

- Cabka Group

- Schoeller Allibert