Returnable Transport Packaging Market Size and Growth

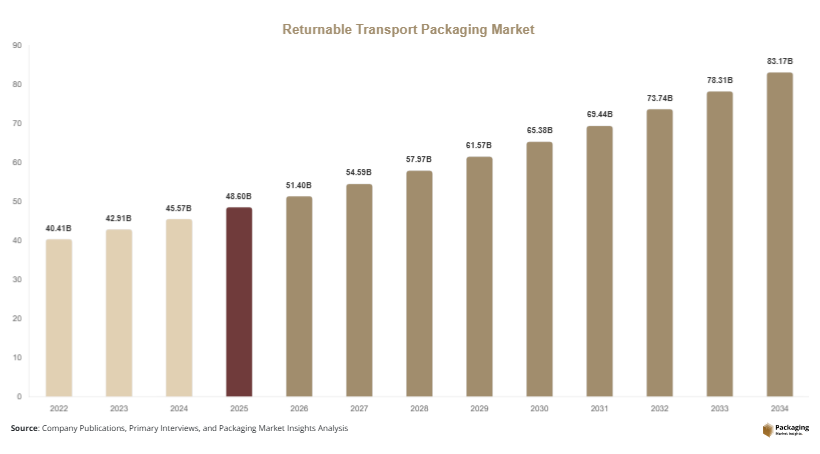

The global returnable transport packaging market size was valued at USD 48.6 billion in 2025 and is projected to reach USD 51.4 billion in 2026. By 2034, the market is expected to reach approximately USD 82.9 billion, expanding at a CAGR of 6.2% during the forecast period (2025–2034). The increasing shift toward circular economy practices and sustainable logistics operations is creating favorable conditions for long-term market expansion.

The returnable transport packaging market is experiencing steady growth as industries increasingly adopt reusable packaging systems to reduce logistics costs, improve supply chain efficiency, and meet sustainability objectives. Returnable transport packaging (RTP) includes reusable pallets, crates, containers, dunnage systems, and intermediate bulk containers that are designed for multiple shipping cycles. These solutions are widely utilized across automotive, food and beverage, retail, healthcare, industrial manufacturing, and consumer goods sectors.

Key Market Highlights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Pallets led the type segment with a 34.8% share.

- Plastic materials dominated with a 48.9% share.

- Automotive applications led the end-use segment with 30.6% share.

- The US remained the dominant country with a market size of USD 9.1 billion in 2025 and USD 9.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of Smart Tracking Technologies in RTP Systems

The integration of digital tracking technologies is becoming a defining trend in the returnable transport packaging market. Companies are increasingly deploying RFID tags, IoT sensors, and GPS-enabled monitoring systems to improve asset visibility throughout supply chains. These technologies help businesses reduce packaging loss, optimize asset utilization, and improve inventory accuracy. For example, automotive manufacturers are implementing RFID-enabled returnable containers to track components across production facilities and supplier networks. This approach reduces operational inefficiencies and enhances supply chain transparency. In the future, broader adoption of cloud-based asset management platforms is expected to further increase RTP efficiency while supporting predictive maintenance and real-time logistics optimization.

Expansion of Circular Supply Chain Models

Circular supply chain strategies are gaining momentum across manufacturing and retail industries, driving increased adoption of returnable transport packaging. Organizations are moving away from disposable packaging systems in favor of reusable alternatives that support sustainability goals and reduce waste generation. Food distributors and consumer goods companies are increasingly implementing closed-loop logistics networks using reusable pallets and containers. These systems improve resource utilization while lowering packaging procurement costs over time. Looking ahead, growing corporate commitments to carbon reduction and waste minimization are expected to accelerate the transition toward circular logistics models, creating sustained demand for RTP solutions across global markets.

Market Drivers

Rising Focus on Sustainable Logistics and Waste Reduction

Sustainability initiatives are significantly influencing demand within the returnable transport packaging market. Governments and corporations are implementing environmental policies aimed at reducing waste generation and lowering carbon emissions. Returnable packaging systems support these objectives by replacing disposable alternatives with reusable assets capable of completing numerous transport cycles. For example, beverage manufacturers increasingly use reusable crates and pallets to reduce packaging waste and improve supply chain sustainability. This cause-and-effect relationship between environmental goals and reusable packaging adoption is expected to continue driving market growth as organizations strengthen sustainability commitments and pursue circular economy strategies.

Increasing Demand from Automotive Manufacturing Supply Chains

The automotive industry remains a major driver of RTP demand due to its reliance on efficient component transportation systems. Automotive manufacturers require durable packaging solutions capable of protecting parts during repeated shipping cycles between suppliers and assembly plants. Returnable containers, racks, and pallets help reduce packaging costs while improving operational efficiency. For instance, vehicle manufacturers utilize custom-designed reusable containers for engines, transmissions, and electronic components. As global automotive production expands and electric vehicle manufacturing increases, demand for returnable transport packaging solutions is expected to strengthen across established and emerging automotive markets.

Market Restraint

High Initial Investment Requirements for Returnable Packaging Systems

A significant restraint affecting the returnable transport packaging market is the substantial upfront investment required to implement reusable packaging systems. Unlike disposable packaging, RTP solutions require expenditures on durable assets, tracking technologies, cleaning infrastructure, and reverse logistics operations. Small and medium-sized enterprises often face financial barriers when transitioning from single-use packaging to returnable systems.

The impact of this challenge can be observed in industries with fragmented supply chains where return logistics networks are less developed. For example, regional manufacturers may struggle to recover reusable containers efficiently, resulting in higher operational costs and reduced return on investment. Asset loss and damage can further increase financial risks. Although long-term cost savings frequently offset initial expenditures, the upfront capital requirements continue to limit adoption among some businesses. Future market growth will depend on improved leasing models, pooling services, and asset management solutions that reduce implementation costs and increase accessibility.

Market Opportunities

Growth of Packaging Pooling Services

Packaging pooling services present substantial opportunities for market participants. Under pooling models, companies rent reusable packaging assets rather than purchasing them outright, reducing capital expenditures and simplifying asset management. Pooling providers maintain, track, and redistribute packaging units across customer networks. For example, retailers and manufacturers increasingly utilize pooled pallets and containers to improve logistics efficiency. Future growth opportunities are expected as businesses seek flexible packaging solutions that support sustainability goals while minimizing operational complexity. Expansion of regional pooling networks will further enhance RTP accessibility across diverse industries.

Rising Adoption in Healthcare and Pharmaceutical Logistics

The healthcare sector represents an emerging opportunity for returnable transport packaging providers. Pharmaceutical manufacturers and healthcare distributors require secure, durable packaging solutions capable of protecting sensitive products during transportation. Reusable containers with temperature-control capabilities are gaining popularity for medical devices, biologics, and pharmaceutical products. Growing healthcare spending and expanding pharmaceutical supply chains are expected to increase demand for specialized RTP solutions. Future applications may include smart reusable containers equipped with environmental monitoring systems to ensure product integrity throughout distribution networks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.6 Billion |

| Market Size in 2026 | USD 51.4 Billion |

| Market Size in 2034 | USD 82.9 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Pallets dominated the market in 2024, accounting for approximately 34.8% of total market share. Pallets remain the most widely used returnable transport packaging format because of their compatibility with warehouse automation systems, forklifts, and global logistics networks. Industries including retail, automotive, food processing, and manufacturing depend heavily on reusable pallets for efficient material handling and transportation. Plastic and composite pallets are increasingly replacing traditional alternatives due to their durability and longer service life. Major logistics providers and pallet pooling operators continue expanding reusable pallet fleets to meet growing customer demand. The widespread adoption of reusable pallet systems across supply chains is expected to sustain segment leadership throughout the forecast period.

Reusable crates are anticipated to be the fastest-growing type segment, registering a CAGR of 7.4% through 2034. Growth is driven by increasing demand from food distribution, agriculture, and retail sectors where product protection and efficient handling are critical. Crates provide stackability, durability, and ease of cleaning, making them suitable for repeated use. Continued expansion of fresh produce distribution networks and grocery retail operations is expected to support long-term growth.

By Material

Plastic dominated the material segment with approximately 48.9% market share in 2024. Plastic RTP products offer durability, lightweight performance, resistance to moisture, and long operational lifespans. These characteristics make them highly suitable for pallets, crates, containers, and bulk packaging systems. Industries increasingly prefer plastic-based RTP solutions because they reduce maintenance requirements and improve transportation efficiency. Advancements in recycled plastics and sustainable manufacturing processes are further enhancing segment growth. The material's adaptability across multiple industries contributes significantly to its market leadership.

Composite materials are projected to be the fastest-growing segment, expanding at a CAGR of 7.0% during the forecast period. Composite RTP products combine strength, durability, and reduced weight, making them attractive for demanding logistics environments. Growth is being supported by increasing demand for high-performance packaging solutions in automotive and industrial applications. Future developments in sustainable composite materials are expected to create additional opportunities for market expansion.

By End-Use

Automotive accounted for approximately 30.6% of market share in 2024, making it the largest end-use segment. Automotive manufacturers rely heavily on reusable packaging systems to transport components between suppliers and assembly facilities. Returnable racks, pallets, and custom containers help protect high-value parts while reducing packaging costs. The industry's focus on lean manufacturing and supply chain efficiency further supports RTP adoption. Growth in electric vehicle production is also increasing demand for specialized reusable packaging formats designed for battery components and electronic systems.

Healthcare is expected to be the fastest-growing end-use segment, registering a CAGR of 7.5% through 2034. Rising pharmaceutical production, increasing healthcare expenditures, and expanding temperature-sensitive logistics operations are driving demand for reusable transport packaging. Advanced reusable containers equipped with monitoring technologies are becoming increasingly important for ensuring product quality and regulatory compliance. Future innovations in cold-chain RTP systems are expected to accelerate adoption across healthcare supply chains.

Returnable Transport Packaging Market Segmentations

By Type

- Pallets

- Crates

- Containers

- Dunnage Systems

- Intermediate Bulk Containers (IBCs)

By Material

- Plastic

- Metal

- Wood

- Composite Materials

- Other Materials

By End-User

- Automotive

- Food & Beverage

- Healthcare

- Consumer Goods

- Industrial Manufacturing

- Retail & E-Commerce

Regional Analysis

North America

North America accounted for approximately 27.8% of the global returnable transport packaging market share in 2025 and is expected to register a CAGR of 5.8% through 2034. The region benefits from advanced logistics infrastructure, widespread automation in warehousing operations, and strong adoption of reusable packaging systems across manufacturing sectors. Automotive, retail, and food processing industries continue investing in returnable packaging assets to reduce transportation costs and improve operational efficiency. The growth of omnichannel distribution networks is also supporting demand for durable logistics packaging solutions.

The United States dominates the regional market. A unique growth driver is the increasing adoption of pallet pooling and reusable container management programs among large retailers and manufacturers. Several major logistics providers have expanded reusable asset tracking capabilities to improve supply chain visibility. The growing integration of RFID-enabled transport packaging is further enhancing asset utilization and reducing losses, supporting long-term market growth.

Europe

Europe held approximately 25.4% of global market share in 2025 and is projected to grow at a CAGR of 6.0% during the forecast period. Strong environmental regulations and circular economy policies are encouraging businesses to replace disposable transport packaging with reusable alternatives. Industries including automotive, food processing, and industrial manufacturing remain key users of RTP solutions. The presence of well-established logistics networks and sustainability-focused supply chain initiatives continues to support regional growth. Increasing investments in packaging pooling systems are also expanding market opportunities.

Germany remains the dominant country within Europe. A unique growth driver is the country's highly integrated automotive manufacturing ecosystem, which relies extensively on reusable containers and racks for component transportation. Major automotive suppliers and vehicle manufacturers continue expanding closed-loop logistics systems to improve efficiency and reduce waste. This trend is expected to sustain strong RTP demand throughout the forecast period.

Asia Pacific

Asia Pacific dominated the market with a 38.6% share in 2025 and is forecast to expand at a CAGR of 6.8% through 2034. Rapid industrialization, manufacturing expansion, and growing export activities are supporting market development across the region. Increasing awareness of sustainable packaging practices and improvements in logistics infrastructure are encouraging RTP adoption. Countries such as China, India, Japan, and South Korea are witnessing rising demand for reusable pallets, containers, and crates across automotive, electronics, and consumer goods industries.

China leads the regional market. A unique growth driver is the expansion of industrial production clusters that require efficient inter-facility transportation systems. Manufacturers increasingly adopt reusable packaging to reduce operational costs and support sustainability initiatives. Growth in export-oriented manufacturing and e-commerce logistics is creating additional demand for durable transport packaging solutions across the country.

Middle East & Africa

The Middle East & Africa represented approximately 4.5% of global market share in 2025 and is expected to grow at a CAGR of 6.5% through 2034. Expanding industrial sectors, infrastructure development projects, and increasing regional trade activities are supporting market growth. Demand for reusable transport packaging is rising among food distributors, construction suppliers, and industrial manufacturers seeking cost-efficient logistics solutions. Investments in warehouse modernization and supply chain optimization initiatives are further contributing to market expansion.

The United Arab Emirates is the dominant country in the region. A unique growth driver is the country's role as a regional logistics hub connecting international trade routes. Distribution centers and logistics operators increasingly implement reusable packaging systems to improve operational efficiency and reduce waste. The expansion of free trade zones and warehousing facilities is expected to support future market development.

Latin America

Latin America accounted for approximately 3.7% of global market share in 2025 and is projected to register the fastest CAGR of 7.1% during the forecast period. Rising manufacturing activities, expanding agricultural exports, and growing retail distribution networks are increasing demand for reusable transport packaging solutions. Businesses are increasingly recognizing the long-term cost advantages of returnable systems compared to disposable packaging alternatives. Government initiatives supporting sustainability are also contributing to market growth.

Brazil dominates the Latin American market. A unique growth driver is the modernization of agricultural and food export supply chains that require durable reusable containers for product transportation. Agricultural cooperatives and food processors are increasingly investing in returnable packaging systems to reduce packaging costs and improve product handling efficiency. This trend is expected to create additional growth opportunities throughout the region.

Competitive Landscape

The returnable transport packaging market is characterized by the presence of global packaging manufacturers, pooling service providers, and logistics solution companies. Brambles Limited (CHEP) is widely recognized as the market leader due to its extensive pallet pooling network, global operational footprint, and advanced asset management capabilities.

Other major participants include ORBIS Corporation, Schoeller Allibert, DS Smith Plc, and IPL Plastics Inc. These companies focus on product innovation, strategic partnerships, and expansion of reusable packaging portfolios to strengthen market positions. Investments in RFID-enabled asset tracking, sustainable materials, and digital logistics platforms are becoming key competitive strategies.

Recent developments include the introduction of lightweight reusable containers, expansion of pooling services into emerging markets, and increased adoption of recycled-content RTP products. Market participants are also investing in automation-compatible packaging solutions to meet evolving warehouse and logistics requirements. As sustainability and operational efficiency become increasingly important, competition is expected to intensify across the global RTP industry.

Key Players List

- Brambles Limited (CHEP)

- ORBIS Corporation

- Schoeller Allibert

- DS Smith Plc

- IPL Plastics Inc.

- CABKA Group

- Rehrig Pacific Company

- Buckhorn Inc.

- SSI SCHAEFER Group

- Craemer Group

- Nefab Group

- Loscam International

- Myers Industries Inc.

- Georg Utz Holding AG

- Tosca Services LLC