Packaging Services Market Size and Growth

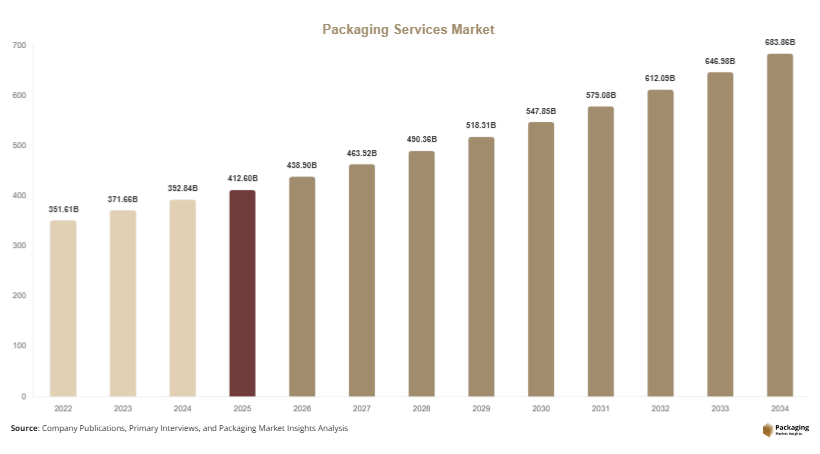

The global packaging services market size is estimated at USD 412.6 billion in 2025 and is projected to reach USD 438.9 billion in 2026. By 2034, the market is forecast to reach USD 702.4 billion, registering a CAGR of 5.7% during 2025–2034. Market growth is being driven by rising e-commerce fulfillment demand, expanding pharmaceutical packaging outsourcing, and increasing complexity in customized consumer goods packaging requirements. The packaging services market is experiencing steady expansion as businesses increasingly outsource packaging design, contract packing, labeling, kitting, repacking, warehousing, and fulfillment operations to specialized service providers.

One major growth factor is the rapid expansion of omnichannel retail, where brands require flexible packaging operations that can support direct-to-consumer shipping, retail-ready packaging, and promotional bundling simultaneously. A second growth factor is the pharmaceutical and healthcare sector’s increasing reliance on outsourced packaging services for serialization, blister packaging, tamper-evident packaging, and regulatory labeling. A third key factor is the rising demand for sustainable packaging conversion services, where companies seek providers capable of integrating recyclable materials, lightweight formats, and environmentally aligned packaging systems without disrupting supply chain efficiency.

Key Highlights:

- Asia Pacific dominated the market with a 36.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Contract packaging led the type segment with a 33.6% share.

- Plastic-based packaging materials dominated with a 46.8% share.

- Food and beverage applications led the end-use segment with 29.4% share.

- The US remained the dominant country with a market size of USD 74.8 billion in 2025 and USD 79.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Automation in Contract Packaging Operations

Automation is becoming central to service efficiency across the packaging services market. Providers are increasingly adopting robotic packing cells, automated sorting systems, digital print-on-demand labeling, and AI-based inspection platforms to improve throughput and reduce packaging errors. For example, large fulfillment centers now use robotic carton assembly and automated dimensioning systems to optimize packaging size and shipping efficiency. Over time, automation is expected to reduce operational cost per unit while improving scalability for seasonal demand spikes.

Sustainable Packaging Conversion Services

Sustainability is reshaping outsourced packaging models. Brands increasingly seek packaging partners that can source recyclable substrates, reduce secondary packaging waste, and redesign pack formats for material efficiency. Food delivery companies, subscription box brands, and consumer goods manufacturers are increasingly outsourcing sustainable pack conversion projects. This trend is likely to create long-term demand for packaging service providers that combine operational execution with sustainable packaging engineering expertise.

Market Drivers

Expansion of E-Commerce Fulfillment Networks

The continued expansion of e-commerce is directly increasing demand in the packaging services market. Online retail requires customized packaging, protective packing, returns packaging, promotional inserts, and rapid order fulfillment at scale. As order volume rises, brands increasingly outsource packaging execution to specialized providers. For example, cosmetics brands often rely on contract packers for gift sets, influencer kits, and subscription box assembly. This outsourcing model improves flexibility and lowers fixed infrastructure costs.

Rising Pharmaceutical Packaging Outsourcing

Healthcare companies are increasingly outsourcing packaging services due to strict compliance requirements and growing product complexity. Pharmaceutical packaging services include serialization, blister packs, labeling, cold-chain preparation, tamper-evident sealing, and regulatory packaging adaptation. Contract packaging specialists offer validated packaging lines that help pharmaceutical firms maintain compliance while accelerating time-to-market. This trend is expected to remain a major growth driver through the forecast period.

Market Restraint

Margin Pressure from Input Cost Volatility

One restraint affecting the packaging services market is cost volatility in packaging substrates, adhesives, labels, corrugated materials, and logistics operations. Service providers often operate on contract pricing models, making sudden increases in raw material or transportation costs difficult to fully pass on to customers. For example, fluctuations in corrugated board pricing can significantly affect fulfillment packaging margins during peak shipping seasons. This creates profitability pressure, especially for mid-sized packaging service operators competing on price-sensitive contracts.

Market Opportunities

Growth in Value-Added Customized Packaging

Customized packaging services represent a major opportunity in the packaging services market. Brands increasingly demand promotional bundling, gift packaging, regional labeling customization, and premium pack finishing to differentiate customer experience. Luxury beauty, premium beverages, and direct-to-consumer wellness brands are actively outsourcing these specialized packaging requirements. Future demand is expected to rise as personalization becomes a stronger commercial strategy.

Expansion in Emerging Consumer Markets

Emerging economies offer strong long-term growth opportunities for outsourced packaging services. Rising retail penetration, growing healthcare demand, and rapid logistics modernization are increasing packaging complexity in countries such as India, Brazil, Indonesia, and Vietnam. Service providers expanding regional packaging hubs can benefit from local manufacturing growth, increasing export packaging demand, and broader adoption of organized retail packaging systems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 412.6 Billion |

| Market Size in 2026 | USD 438.9 Billion |

| Market Size in 2034 | USD 702.4 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Contract packaging dominated the market in 2024 with 33.6% share. This segment leads due to broad service scope including filling, sealing, labeling, assembly, and retail-ready packaging. Food manufacturers, cosmetics brands, and pharmaceutical companies increasingly outsource packaging execution to reduce capital investment and improve scalability. Contract packaging also allows seasonal capacity flexibility, making it operationally attractive for fast-moving consumer brands.

Fulfillment and kitting services are expected to grow at the fastest CAGR of 6.8% through 2034. Growth is driven by subscription commerce, promotional bundling, and omnichannel retail packaging requirements. Service providers are investing in automation, modular assembly systems, and digital inventory management to support rising demand for customized order assembly and direct-to-consumer shipping solutions.

By Material

Plastic-based packaging materials accounted for 46.8% share in 2024, supported by durability, lightweight structure, and compatibility with automated packaging lines. Flexible films, rigid plastic containers, shrink wraps, and protective inserts remain widely used across food, healthcare, and electronics packaging services. Their versatility continues to support dominance despite sustainability pressure.

Paper-based sustainable materials are projected to grow at a CAGR of 6.7%. Corrugated packaging, molded fiber inserts, paper wraps, and recyclable cartons are gaining traction as brands reduce plastic dependency. Packaging service providers are expanding paper conversion capabilities and lightweight structural packaging solutions to meet evolving sustainability targets.

By End-Use

Food and beverage led the market with 29.4% share in 2024. Demand is supported by repacking, labeling, promotional bundling, meal kit assembly, and shelf-ready packaging services. Brands increasingly outsource seasonal promotional packaging and regional labeling adaptation. Beverage multipacks, snack bundles, and ready-to-ship food packaging contribute significantly to service volume.

Healthcare packaging is forecast to grow at the fastest CAGR of 6.9%. Rising pharmaceutical output, regulatory labeling requirements, serialization demand, and medical device packaging complexity are driving expansion. Future growth will include cold-chain packaging preparation, tamper-evident assembly, and advanced compliance packaging services designed for regulated healthcare supply chains.

Packaging Services Market Segmentations

By Type

- Contract Packaging

- Fulfillment Services

- Kitting and Assembly

- Labeling and Repackaging

- Warehousing and Distribution Packaging

By Material

- Plastic-Based Materials

- Paper and Paperboard

- Flexible Films

- Glass Packaging Components

- Metal Packaging Components

By End-User

- Food and Beverage

- Healthcare

- Personal Care

- Industrial Goods

- Consumer Electronics

Regional Analysis

North America

North America accounted for 27.4% of the global packaging services market share in 2025 and is projected to grow at a CAGR of 5.0% through 2034. Growth is supported by mature e-commerce infrastructure, strong contract packaging demand, and pharmaceutical outsourcing expansion. Consumer packaged goods companies increasingly outsource seasonal packaging, promotional kitting, and fulfillment packaging to improve operational flexibility.

The United States dominates the regional market. A unique growth driver is subscription commerce packaging, where recurring monthly shipment models require highly customized assembly, branded inserts, and personalized pack formats. This recurring service model is generating steady outsourced packaging demand across beauty, wellness, snacks, and specialty retail sectors.

Europe

Europe held 23.1% market share in 2025 and is expected to expand at a CAGR of 5.1%. Market demand is driven by sustainable packaging regulations, premium retail packaging needs, and pharmaceutical contract packing growth. Brands increasingly partner with service providers that can manage recyclable packaging conversion and regional regulatory packaging adaptation.

Germany leads the European market. A unique growth factor is industrial export packaging services, where machinery, automotive parts, and precision equipment require customized protective packaging, compliance documentation insertion, and logistics-ready packaging systems for cross-border shipments.

Asia Pacific

Asia Pacific led the market with 36.9% share in 2025 and is forecast to grow at a CAGR of 6.0%. Expansion is supported by manufacturing growth, export packaging demand, rising middle-class consumption, and large-scale retail logistics development. Contract packaging providers are increasingly serving food brands, electronics exporters, and healthcare manufacturers across regional markets.

China remains dominant in Asia Pacific. A unique driver is contract packaging for export manufacturing, where global brands rely on specialized packaging partners for labeling localization, bundled packaging, retail-ready conversion, and protective transit packaging for international shipments.

Middle East & Africa

The Middle East & Africa represented 5.1% of market share in 2025 and is projected to grow at a CAGR of 5.8%. Growth is driven by food imports, healthcare logistics expansion, and increasing organized retail packaging demand. Packaging outsourcing is rising as brands seek scalable operational partners without investing heavily in in-house packaging infrastructure.

The United Arab Emirates leads the region. A unique growth factor is re-export packaging and relabeling services, where imported products are repackaged, relabeled, and customized for regional markets before redistribution across Gulf and African trade corridors.

Latin America

Latin America accounted for 7.5% share in 2025 and is projected to record the fastest CAGR of 6.4%. Rising retail formalization, pharmaceutical expansion, and packaged food consumption are strengthening outsourced packaging demand. Regional brands increasingly rely on third-party providers for packaging flexibility and cost control.

Brazil dominates the market in Latin America. A unique growth driver is agricultural export packaging services, where specialty food, processed goods, and packaged agricultural products require labeling, compliance packing, and logistics-ready export packaging for international trade.

Competitive Landscape

The packaging services market is moderately consolidated, with major providers competing through geographic scale, automation investment, industry specialization, and sustainable packaging capabilities. WestRock Company remains a leading participant due to its broad packaging service network, integrated packaging solutions, and strong relationships across food, healthcare, and industrial markets. The company recently expanded automated fulfillment packaging operations to support rising omnichannel retail demand.

Other notable companies include DS Smith plc, Sonoco Products Company, Amcor plc, and Sealed Air Corporation. These firms are investing in smart packaging integration, recyclable material processing, automated packing systems, and regional service expansion. Competitive differentiation increasingly depends on operational speed, customization flexibility, and sustainable packaging execution.

Key Players List

- WestRock Company

- DS Smith plc

- Sonoco Products Company

- Amcor plc

- Sealed Air Corporation

- Smurfit Kappa Group

- FedEx Supply Chain

- GXO Logistics

- DHL Supply Chain

- Nefab Group

- Veritiv Corporation

- Menasha Packaging

- Berlin Packaging

- UFP Packaging

- Sharp Packaging Services