Die Cut Carton Market Size and Growth

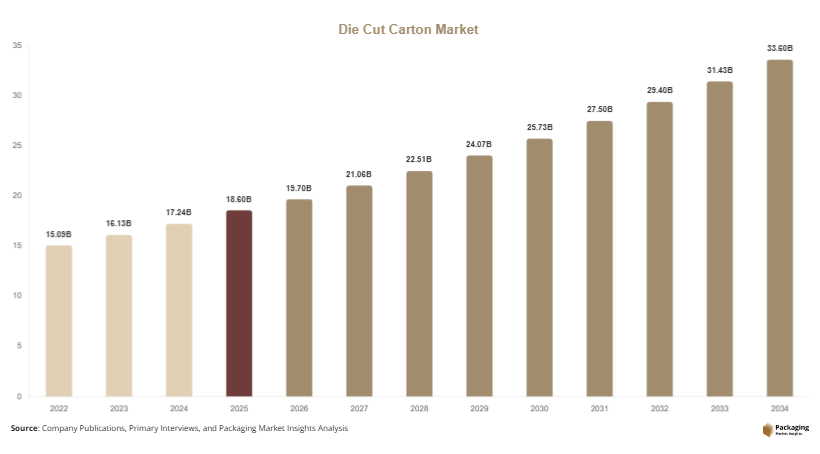

The global die cut carton market size is estimated at USD 18.6 billion in 2025 and is expected to reach USD 19.7 billion in 2026. By 2034, the market is forecast to attain approximately USD 33.8 billion, registering a CAGR of 6.9% during the forecast period (2025–2034). Growing demand for sustainable paperboard packaging, increasing product differentiation requirements among consumer brands, and the rapid expansion of e-commerce distribution networks are among the major factors supporting market growth.

The die cut carton market is witnessing consistent growth as industries increasingly demand customized, lightweight, and sustainable packaging solutions. Die cut cartons are widely used across food & beverages, pharmaceuticals, personal care, electronics, and e-commerce sectors due to their flexibility in design, structural strength, and branding capabilities. These cartons are manufactured using precision cutting processes that allow customized shapes, windows, inserts, and foldable structures, making them suitable for both protective and retail packaging applications.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.3%.

- Straight tuck end cartons led the type segment with a 34.7% share.

- Paperboard cartons dominated the material segment with a 58.5% share.

- Food & beverage applications led the end-use segment with a 41.8% share.

- The US remained the dominant country with a market size of USD 3.1 billion in 2025 and USD 3.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable and Recyclable Carton Packaging

Sustainability continues to reshape the die cut carton market as brand owners seek alternatives to plastic packaging. Manufacturers are increasingly utilizing recycled paperboard, biodegradable coatings, and renewable raw materials to produce environmentally responsible die cut cartons. Food companies, cosmetics brands, and pharmaceutical manufacturers are adopting recyclable cartons to comply with environmental regulations and meet consumer expectations. For example, several multinational food brands have replaced plastic trays with die cut carton alternatives featuring fiber-based structures. This trend is expected to accelerate as retailers implement sustainable packaging standards. Future developments will likely focus on compostable coatings, reduced material usage, and higher recycled content, further strengthening the position of die cut cartons across multiple industries.

Increasing Integration of Digital Printing and Smart Packaging Features

Digital printing technologies are becoming increasingly important in the die cut carton industry. Brands are seeking personalized packaging designs, shorter production runs, and enhanced visual appeal. Modern die cut cartons can incorporate QR codes, authentication labels, and interactive marketing features that improve consumer engagement. For instance, beverage and cosmetic companies are using digitally printed cartons for promotional campaigns and limited-edition product launches. The ability to customize packaging without significant tooling costs provides a competitive advantage. Going forward, integration of smart packaging elements such as traceability codes and consumer interaction platforms is expected to create new opportunities for packaging manufacturers and brand owners alike.

Market Drivers

Expansion of E-Commerce and Retail Packaging Demand

The rapid growth of e-commerce is a major driver of the die cut carton market. Online retailers require durable, lightweight, and customizable packaging solutions that protect products during transportation while enhancing customer experience. Die cut cartons provide excellent structural integrity and branding opportunities, making them ideal for shipping and retail display applications. As online shopping continues to expand globally, demand for customized packaging formats is increasing. For example, consumer electronics and personal care brands frequently utilize die cut cartons with inserts and compartments to improve product protection. This growth in e-commerce directly contributes to higher demand for die cut packaging solutions across multiple product categories.

Rising Demand for Product Differentiation and Premium Packaging

Brands increasingly rely on packaging as a marketing tool to distinguish products in competitive retail environments. Die cut cartons allow unique shapes, windows, embossing, and custom graphics that enhance product presentation and consumer appeal. Luxury food products, cosmetics, and healthcare products often utilize premium carton packaging to strengthen brand identity. For example, premium chocolate manufacturers frequently use custom die cut cartons to create distinctive shelf presence. As competition intensifies across consumer goods industries, the need for innovative packaging formats continues to increase, supporting long-term market growth and encouraging investment in advanced carton manufacturing technologies.

Market Restraint

Volatility in Raw Material Prices and Supply Chain Challenges

A major restraint affecting the die cut carton market is the fluctuation in paperboard and pulp prices. Raw material costs can vary significantly due to supply-demand imbalances, energy costs, transportation expenses, and forestry regulations. These fluctuations directly impact carton manufacturers' profit margins and pricing strategies. For example, disruptions in global pulp supply chains have periodically increased production costs for packaging converters. Small and medium-sized manufacturers are particularly vulnerable to price volatility because they often have limited purchasing power. Additionally, transportation disruptions and labor shortages can delay production schedules and increase operational expenses. Although demand remains strong, ongoing supply chain uncertainties continue to present challenges for market participants.

Market Opportunities

Expansion of Pharmaceutical and Healthcare Packaging Applications

The pharmaceutical industry presents significant growth opportunities for die cut carton manufacturers. Increasing production of prescription drugs, over-the-counter medicines, and healthcare products is driving demand for secure, tamper-evident, and information-rich packaging solutions. Die cut cartons offer excellent printability for regulatory labeling requirements while providing structural protection during transportation. Pharmaceutical companies increasingly require customized cartons for specialty medicines and medical devices. Future growth opportunities are expected to emerge from biologics, nutraceuticals, and healthcare e-commerce channels, where packaging quality and traceability play critical roles in product safety and compliance.

Growth in Emerging Markets and Sustainable Consumer Goods Packaging

Emerging economies across Asia Pacific, Latin America, and Africa represent substantial opportunities for the die cut carton market. Rising urbanization, increasing disposable incomes, and expanding retail infrastructure are boosting demand for packaged consumer goods. Manufacturers are introducing sustainable packaging solutions to align with evolving environmental regulations and consumer preferences. For example, food producers in India and Southeast Asia are increasingly adopting paper-based die cut cartons to reduce plastic consumption. Future investments in packaging automation, recycling infrastructure, and local manufacturing facilities are expected to support long-term market expansion across developing regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.7 Billion |

| Market Size in 2034 | USD 33.8 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Straight tuck end cartons dominated the market in 2024, accounting for approximately 34.7% of total revenue share. Their widespread adoption is attributed to their versatility, cost efficiency, and suitability for a wide range of products including cosmetics, pharmaceuticals, food items, and consumer electronics. These cartons offer easy assembly, strong structural performance, and excellent printability, making them a preferred choice among manufacturers and brand owners. Many consumer packaged goods companies utilize straight tuck end cartons because they can be efficiently produced in large volumes while maintaining attractive shelf presentation. The segment also benefits from compatibility with automated packaging lines and flexible design options. Continued demand from retail packaging applications is expected to support the segment's dominant position throughout the forecast period.

Custom display cartons are projected to be the fastest-growing type segment, expanding at a CAGR of 7.8% through 2034. Growth is driven by increasing demand for point-of-sale marketing solutions and enhanced retail visibility. Brands are utilizing display-ready cartons to improve product presentation and attract consumer attention in competitive retail environments. Packaging innovations such as digitally printed graphics, interactive features, and sustainable materials are further supporting adoption. Future demand is expected to increase as retailers seek packaging formats that combine product protection with merchandising functionality.

By Material

Paperboard cartons dominated the material segment in 2024 with approximately 58.5% market share. The segment's leadership is supported by excellent printability, recyclability, lightweight properties, and cost efficiency. Paperboard is widely used across food packaging, healthcare products, cosmetics, and consumer goods applications. Manufacturers favor paperboard because it offers strong branding opportunities while supporting sustainability objectives. For example, many packaged food companies utilize paperboard die cut cartons to replace plastic packaging formats and comply with environmental regulations. Strong availability of raw materials and established recycling systems continue to reinforce the segment's dominant position.

Recycled fiberboard cartons are expected to witness the fastest growth, registering a CAGR of 7.6% during the forecast period. Growing sustainability initiatives and increasing consumer awareness regarding environmental issues are driving adoption. Brands are actively seeking packaging materials with lower carbon footprints and higher recycled content. Packaging converters are investing in advanced processing technologies to improve the quality and performance of recycled fiberboard materials. Future growth is expected to be supported by stricter environmental regulations and expanding circular economy programs.

By End-Use

Food & beverage applications represented the largest end-use segment in 2024, accounting for approximately 41.8% of total market share. Rising demand for packaged foods, ready-to-eat meals, confectionery products, and beverage multipacks continues to drive carton consumption. Die cut cartons provide excellent product protection, branding opportunities, and sustainability benefits. Food manufacturers increasingly utilize customized cartons to differentiate products and improve consumer appeal. Growing retail penetration and changing consumer lifestyles are expected to support continued segment dominance throughout the forecast period.

Pharmaceutical packaging is anticipated to be the fastest-growing end-use segment, expanding at a CAGR of 7.5% through 2034. Increasing healthcare expenditure, pharmaceutical production, and regulatory labeling requirements are driving demand for customized carton packaging. Die cut cartons offer tamper-evident features, product protection, and detailed information display capabilities. Pharmaceutical companies are increasingly adopting advanced packaging solutions that support traceability and compliance requirements. Continued growth in specialty medicines and healthcare distribution channels is expected to create significant opportunities for carton manufacturers.

Die Cut Carton Market Segmentations

By Type

- Straight Tuck End Cartons

- Reverse Tuck End Cartons

- Auto-Lock Bottom Cartons

- Custom Display Cartons

By Material

- Paperboard

- Corrugated Board

- Recycled Fiberboard

By End-User

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Consumer Electronics

- Industrial Products

Regional Analysis

North America

North America accounted for approximately 27.8% of the global die cut carton market share in 2025 and is expected to grow at a CAGR of 6.4% through 2034. The region benefits from strong packaging demand across food, healthcare, cosmetics, and e-commerce industries. Increasing adoption of recyclable packaging materials and growing investment in automated carton manufacturing technologies are supporting market growth. Consumer preference for sustainable packaging continues to influence purchasing decisions, encouraging brand owners to shift toward paper-based packaging solutions. In addition, retail chains and online platforms are seeking customized packaging designs that improve product presentation and transportation efficiency.

The United States dominates the regional market due to its large consumer goods and e-commerce sectors. A unique growth driver is the rapid expansion of subscription-based retail packaging. Companies delivering cosmetics, meal kits, and specialty consumer products increasingly utilize customized die cut cartons to enhance customer experience. For example, several direct-to-consumer brands use premium printed cartons with personalized designs and protective inserts. This trend continues to increase demand for advanced carton packaging solutions throughout the country.

Europe

Europe represented approximately 24.5% of global market share in 2025 and is projected to grow at a CAGR of 6.6% during the forecast period. The region benefits from strict environmental regulations promoting recyclable and renewable packaging materials. Packaging manufacturers are increasingly utilizing certified paperboard and sustainable production processes to meet regulatory requirements. Growing demand for premium food products and healthcare packaging is also contributing to market growth. Furthermore, strong recycling infrastructure supports widespread adoption of paper-based carton packaging solutions across multiple industries.

Germany remains the leading country within Europe. A unique growth factor is the country's advanced manufacturing and packaging automation sector. German packaging companies are investing heavily in high-speed die-cutting and digital printing equipment to improve production efficiency and customization capabilities. For example, pharmaceutical packaging suppliers in Germany increasingly utilize advanced carton technologies to meet stringent regulatory requirements. These investments continue to strengthen the country's position within the regional market.

Asia Pacific

Asia Pacific dominated the die cut carton market with a 39.2% share in 2025 and is forecast to register a CAGR of 7.5% through 2034. Rapid industrialization, expanding retail networks, and increasing demand for packaged consumer goods are key growth drivers. The region benefits from large-scale manufacturing activities and rising consumption of food, beverages, personal care products, and pharmaceuticals. E-commerce expansion across China, India, and Southeast Asia is generating significant demand for customized packaging solutions. In addition, investments in sustainable packaging technologies are supporting long-term market development.

China is the dominant country in Asia Pacific. A unique growth driver is the rapid growth of domestic consumer brands seeking differentiated packaging solutions. Chinese food, cosmetics, and electronics manufacturers increasingly utilize customized die cut cartons to enhance product visibility and brand recognition. For example, premium tea and skincare brands are adopting innovative carton packaging designs to strengthen retail appeal. This trend continues to stimulate demand for advanced carton manufacturing technologies.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.1% of global market share in 2025 and is expected to grow at a CAGR of 6.5%. The region is experiencing increasing demand for packaged foods, healthcare products, and consumer goods. Urbanization, population growth, and expansion of modern retail channels are supporting market development. Packaging manufacturers are gradually increasing investments in local production facilities to serve growing regional demand. Sustainable packaging initiatives are also gaining attention among governments and multinational consumer goods companies operating in the region.

The United Arab Emirates is the dominant country within the region. A unique growth factor is the expansion of luxury retail and premium consumer goods sectors. High-end cosmetics, confectionery, and specialty products increasingly utilize customized die cut cartons to enhance product presentation. For example, luxury gifting products frequently feature premium carton packaging with decorative finishes. This trend continues to support demand for sophisticated packaging solutions throughout the country.

Latin America

Latin America held approximately 4.4% of the global market in 2025 and is projected to grow at the fastest CAGR of 7.3% during the forecast period. Rising consumption of packaged food products, growing retail modernization, and increasing demand for sustainable packaging are driving regional growth. Brand owners are investing in customized packaging solutions to improve product differentiation and attract consumers. Additionally, increasing foreign investment in food processing and consumer goods manufacturing is creating new opportunities for carton suppliers.

Brazil remains the dominant country within Latin America. A unique growth driver is the expansion of processed food exports. Food manufacturers increasingly require high-quality die cut cartons for both domestic sales and international shipments. For example, packaged coffee and confectionery producers are utilizing customized cartons to improve brand visibility in export markets. Growing packaging demand and improving manufacturing capabilities continue to support regional market growth.

Competitive Landscape

The die cut carton market is moderately fragmented, with leading manufacturers competing through product innovation, sustainability initiatives, geographic expansion, and printing technology advancements. WestRock Company remains a leading player due to its extensive packaging portfolio, integrated paperboard operations, and strong presence across food, healthcare, and consumer goods packaging markets.

Other major companies include Smurfit Westrock plc, Graphic Packaging International, International Paper Company, and DS Smith Plc. These companies continue to invest in recyclable materials, digital printing capabilities, and automated manufacturing technologies. Strategic acquisitions and partnerships remain common approaches for expanding production capacity and strengthening market reach.

Recent developments include investments in fiber-based packaging solutions, advanced die-cutting technologies, and lightweight carton structures. Companies are also focusing on customized packaging designs that improve sustainability performance while meeting evolving consumer and regulatory requirements.

Key Players List

- WestRock Company

- Smurfit Westrock plc

- Graphic Packaging International

- International Paper Company

- DS Smith Plc

- Mondi Group

- Stora Enso Oyj

- Sonoco Products Company

- Packaging Corporation of America

- Mayr-Melnhof Karton AG

- Rengo Co., Ltd.

- Oji Holdings Corporation

- UFP Technologies Inc.

- Georgia-Pacific LLC

- Pratt Industries Inc.