Flexible Lid Stock Packaging Market Size and Growth

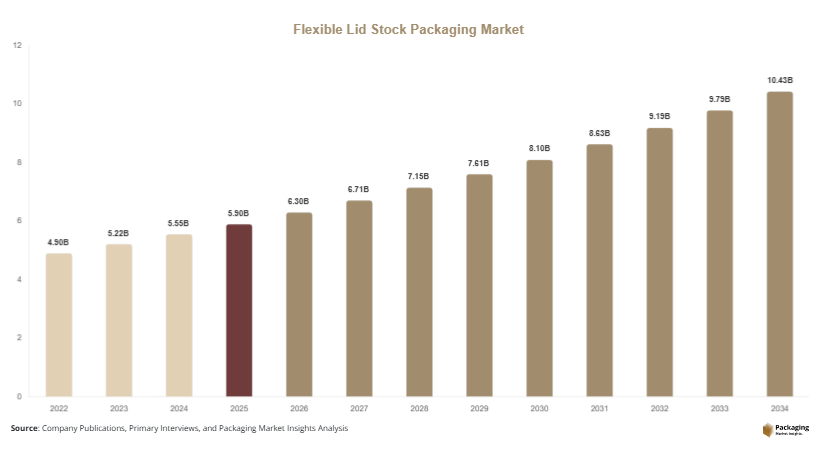

The global flexible lid stock packaging market size was valued at USD 5.9 billion in 2025 and is projected to reach USD 6.3 billion in 2026. The market is expected to reach approximately USD 10.4 billion by 2034, registering a CAGR of 6.5% during the forecast period (2025–2034). The flexible lid stock packaging market is witnessing sustained growth due to increasing demand for convenient, lightweight, and high-performance packaging solutions across food, beverage, pharmaceutical, and personal care industries. Flexible lid stock packaging is widely used for sealing trays, cups, containers, and thermoformed packages, providing product protection, extended shelf life, and enhanced consumer convenience. Manufacturers are increasingly adopting advanced lid stock materials that offer peelability, resealability, barrier protection, and compatibility with high-speed packaging equipment.

Several factors are driving market expansion. First, rising consumption of packaged and ready-to-eat foods is creating significant demand for flexible lidding solutions that maintain freshness and product quality. Second, the growth of pharmaceutical packaging applications requiring secure sealing and contamination protection is supporting adoption across healthcare sectors. Third, increasing consumer preference for convenience packaging formats, including single-serve meals, dairy products, and beverage containers, is encouraging manufacturers to invest in innovative lid stock technologies.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.2%.

- Peelable lid stock led the type segment with a 41.8% share.

- Plastic-based materials dominated with a 63.7% share.

- Food & beverage applications led the segment with 67.4% share.

- The US remained the dominant country with a market size of USD 1.3 billion in 2025 and USD 1.4 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Recyclable and Mono-Material Lid Stock Solutions

Packaging manufacturers are increasingly developing recyclable lid stock structures to meet sustainability goals and evolving regulatory requirements. Traditional multilayer materials often create recycling challenges, encouraging companies to introduce mono-material polyethylene and polypropylene-based solutions. These products provide adequate barrier performance while supporting circular economy initiatives. Food brands are increasingly adopting recyclable lid stock for dairy products, fresh foods, and ready meals. For example, several European packaging converters have launched recyclable lidding films compatible with existing tray systems. The future impact of this trend will include improved recycling rates, greater regulatory compliance, and increased investment in sustainable packaging technologies throughout the value chain.

Growth of High-Barrier Packaging for Fresh and Processed Foods

Demand for high-barrier lid stock packaging is increasing as food manufacturers focus on shelf-life extension and food waste reduction. Flexible lid stock materials with enhanced oxygen and moisture barriers help maintain product quality during storage and transportation. Meat, seafood, dairy, and ready-meal producers are increasingly utilizing advanced barrier structures. For example, modified atmosphere packaging systems commonly incorporate specialized lid stock films to preserve freshness. As global food distribution networks expand and consumer demand for convenient packaged foods rises, high-barrier flexible lid stock packaging is expected to become an increasingly important component of food preservation strategies.

Market Drivers

Expansion of Packaged Food and Convenience Food Consumption

Growing urbanization and changing consumer lifestyles are increasing demand for packaged foods that offer convenience, portability, and extended shelf life. Flexible lid stock packaging supports these requirements by providing effective sealing and product protection. Ready-to-eat meals, yogurt cups, fresh produce trays, and snack packaging frequently utilize flexible lidding materials. As consumers continue to seek time-saving food solutions, manufacturers are expanding production capacities and launching new packaging formats. The direct relationship between packaged food consumption and lid stock demand remains one of the strongest growth drivers supporting market expansion globally.

Increasing Pharmaceutical Packaging Requirements

The pharmaceutical sector is becoming a significant consumer of flexible lid stock packaging due to strict product protection and hygiene requirements. Medical devices, diagnostic kits, and pharmaceutical products often require secure sealing systems that prevent contamination and maintain product integrity. Flexible lid stock materials offer strong sealing performance while enabling convenient opening features. For example, healthcare packaging companies increasingly use peelable lidding solutions for sterile medical packaging applications. Growing healthcare expenditures and expanding pharmaceutical production capacities across emerging economies are expected to further drive demand for advanced lid stock packaging solutions.

Market Restraint

Volatility in Raw Material Prices

Fluctuations in the prices of polymers, aluminum, adhesives, and specialty coatings present a major challenge for the flexible lid stock packaging market. Raw material costs are influenced by crude oil prices, supply chain disruptions, trade policies, and regional economic conditions. Packaging manufacturers often face difficulties maintaining profit margins when input costs rise unexpectedly.

The impact is particularly significant for small and medium-sized converters with limited pricing flexibility. For example, periods of rising resin costs can increase production expenses for polyethylene and polypropylene lid stock materials. Additionally, price instability may delay investments in new packaging technologies or sustainable product development. Although manufacturers attempt to mitigate risks through long-term supplier agreements and material optimization strategies, ongoing raw material volatility remains a constraint that could influence market growth and profitability throughout the forecast period.

Market Opportunities

Expansion of Sustainable Packaging Solutions

Sustainability remains a major growth opportunity for flexible lid stock manufacturers. Consumer demand for environmentally responsible packaging is encouraging investment in recyclable, compostable, and bio-based materials. Food and beverage companies are actively seeking packaging formats that reduce environmental impact without compromising performance. Flexible lid stock producers are developing innovative structures that support recycling streams while maintaining sealing strength and barrier properties. Future opportunities are expected to emerge from government regulations promoting sustainable packaging and increasing corporate commitments to environmental responsibility.

Growing Demand in Emerging Economies

Rapid urbanization, rising disposable incomes, and expanding retail sectors are creating significant opportunities across emerging economies. Countries in Asia Pacific, Latin America, and the Middle East are witnessing strong growth in packaged food consumption and healthcare investments. Flexible lid stock packaging suppliers can benefit from increasing demand for dairy products, convenience foods, pharmaceuticals, and personal care products. As food processing industries continue to modernize and retail infrastructure expands, the market is expected to experience substantial growth opportunities in these developing regions over the next decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.9 Billion |

| Market Size in 2026 | USD 6.3 Billion |

| Market Size in 2034 | USD 10.4 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Peelable lid stock dominated the market in 2024, accounting for approximately 41.8% of total revenue. This segment maintains leadership due to its widespread use across dairy products, ready meals, pharmaceuticals, and fresh food packaging applications. Consumers prefer peelable packaging because it provides easy opening while maintaining package integrity during transportation and storage. Food manufacturers value peelable lid stock for its compatibility with automated filling and sealing operations. Increasing demand for convenience packaging formats continues to strengthen segment growth. The ability to combine strong sealing performance with user-friendly functionality remains a major factor supporting market dominance.

Resealable lid stock is expected to be the fastest-growing subsegment, expanding at a CAGR of 7.5% during the forecast period. Growth is driven by increasing consumer demand for packaging that preserves freshness after opening. Products such as snacks, dairy items, and ready-to-eat foods increasingly utilize resealable solutions. Packaging innovations are improving reseal performance while reducing material usage. As food waste reduction becomes a greater priority for consumers and manufacturers, resealable lid stock is expected to gain significant market traction.

By Material

Plastic-based materials held the largest market share in 2024, representing approximately 63.7% of total revenue. Polyethylene, polypropylene, and polyester-based lid stock materials continue to dominate due to their strong sealing properties, durability, flexibility, and barrier performance. Food processors and pharmaceutical manufacturers rely on plastic-based lid stock because of its compatibility with diverse packaging systems. Additionally, advancements in recyclable plastic structures are helping maintain demand despite sustainability concerns. The segment continues to benefit from established manufacturing infrastructure and cost-effective production processes.

Paper-based materials are projected to register the fastest CAGR of 7.1% through 2034. Rising environmental awareness and regulatory pressure are encouraging adoption of renewable packaging materials. Packaging companies are developing paper-based lid stock products with enhanced barrier coatings and sealing capabilities. Food service applications and sustainable retail packaging formats are creating new opportunities for paper-based solutions. As sustainability goals become more important throughout the packaging value chain, demand for paper-based materials is expected to accelerate significantly.

By End-Use

Food & beverage emerged as the dominant end-use segment in 2024 with a market share of approximately 67.4%. Flexible lid stock packaging is extensively used for dairy products, fresh foods, beverages, frozen meals, and convenience foods. The segment benefits from growing consumer demand for packaged products that offer convenience, freshness, and safety. Manufacturers increasingly utilize advanced barrier films and easy-open features to enhance consumer experience. Continuous innovation in food packaging formats further supports the dominance of this segment.

Pharmaceutical packaging represents the fastest-growing end-use segment and is projected to expand at a CAGR of 7.3% during the forecast period. Growth is driven by increasing healthcare expenditures, expanding pharmaceutical production, and rising demand for sterile packaging solutions. Flexible lid stock materials are widely used in medical device packaging, diagnostic kits, and healthcare products requiring contamination protection. Ongoing investments in healthcare infrastructure and pharmaceutical manufacturing capacity are expected to support robust long-term growth for this segment.

Flexible Lid Stock Packaging Market Segmentations

By Type

- Peelable Lids

- Resealable Lids

- Barrier Lids

- Anti-Fog Lids

- Easy-Open Lids

By Material

- Plastic Films

- Aluminum Foil

- Paper-Based Materials

- Multi-Layer Laminates

By End-User

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Household Products

- Industrial Products

Regional Analysis

North America

North America accounted for approximately 26.4% of the flexible lid stock packaging market share in 2025 and is expected to expand at a CAGR of 6.1% through 2034. The region benefits from a mature packaged food industry, strong healthcare infrastructure, and widespread adoption of advanced packaging technologies. Demand is particularly strong for high-barrier and recyclable lid stock products used in dairy, fresh food, and pharmaceutical applications. Food manufacturers increasingly prioritize shelf-life extension and convenience packaging formats, supporting market growth. Investments in sustainable packaging innovations and consumer preference for packaged food products continue to create favorable conditions for long-term expansion.

The United States dominates the regional market. A unique growth driver is the rapid adoption of convenience meal solutions and meal-kit delivery services. These products require reliable sealing technologies to maintain freshness and ensure product safety during transportation. Packaging companies are responding by developing advanced peelable and resealable lid stock materials. Additionally, growing demand for healthcare packaging and pharmaceutical products further strengthens the country's position as the leading contributor to regional market revenue.

Europe

Europe represented approximately 24.6% of market share in 2025 and is projected to register a CAGR of 5.8% during the forecast period. The region benefits from stringent packaging regulations, strong food processing industries, and increasing demand for recyclable packaging materials. European consumers increasingly prefer sustainable packaging options, encouraging manufacturers to introduce mono-material and recyclable lid stock solutions. Growth is also supported by rising demand for fresh and chilled food products requiring advanced sealing technologies.

Germany remains the dominant country within Europe. A unique growth factor is the country's focus on circular economy initiatives and packaging sustainability. German packaging manufacturers are investing heavily in recyclable film technologies and advanced barrier materials. For example, several food producers are transitioning toward recyclable lidding structures compatible with existing recycling systems. This trend is expected to strengthen market demand while supporting environmental objectives and regulatory compliance.

Asia Pacific

Asia Pacific held the largest share of the flexible lid stock packaging market at 39.2% in 2025 and is expected to grow at a CAGR of 7.0% through 2034. Rapid urbanization, expanding middle-class populations, and increasing consumption of packaged foods are driving regional demand. The growth of food processing industries in China, India, Japan, and Southeast Asia continues to create significant opportunities for packaging manufacturers. Rising investments in pharmaceutical production and organized retail networks are also contributing to market expansion.

China dominates the Asia Pacific market. A unique growth driver is the country's extensive packaged food manufacturing sector. Food producers increasingly adopt advanced lid stock packaging to enhance product protection and shelf-life performance. Additionally, the expansion of e-commerce grocery services and ready-meal consumption is increasing demand for convenient packaging formats. These factors continue to position China as a major growth engine for the regional market.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.8% of global market share in 2025 and is forecast to grow at a CAGR of 6.4%. Increasing investments in food processing facilities, healthcare infrastructure, and retail development are supporting demand for flexible lid stock packaging. The region's growing population and rising consumption of packaged foods are encouraging packaging manufacturers to expand operations. Demand for hygienic packaging solutions is also increasing across pharmaceutical and personal care sectors.

Saudi Arabia is the dominant market within the region. A unique growth driver is the country's ongoing investment in domestic food manufacturing and packaging industries. Government initiatives aimed at improving food security are encouraging local production of packaged food products. As manufacturers expand processing capabilities, demand for advanced lid stock packaging materials continues to increase, supporting regional market growth.

Latin America

Latin America captured approximately 5.0% of market share in 2025 and is projected to record the fastest CAGR of 7.2% during the forecast period. Rising urbanization, growing retail chains, and increasing consumption of packaged foods are contributing to market expansion. Food exporters are adopting advanced packaging solutions to improve product quality and shelf life during transportation. Demand for flexible packaging formats is also increasing among regional consumers seeking convenience and affordability.

Brazil remains the leading country in Latin America. A unique growth factor is the country's strong dairy and processed food industries. Manufacturers increasingly utilize flexible lid stock packaging for yogurt, cheese, and ready-to-eat meal applications. Furthermore, investments in modern packaging technologies and expanding food exports are expected to create additional growth opportunities for packaging suppliers operating within the region.

Competitive Landscape

The flexible lid stock packaging market is moderately competitive, with global and regional players focusing on product innovation, sustainability initiatives, strategic partnerships, and capacity expansion. Companies are investing in recyclable materials, advanced barrier technologies, and digital printing solutions to meet evolving customer requirements.

Amcor plc is recognized as a leading market participant due to its extensive product portfolio, global manufacturing presence, and strong focus on sustainable packaging innovation. The company recently expanded its recyclable flexible packaging offerings to address increasing customer demand for environmentally responsible packaging solutions.

Other major companies such as Berry Global Inc., Constantia Flexibles, Mondi Group, and Coveris Holdings S.A. continue to strengthen their market positions through acquisitions, research and development activities, and regional expansion strategies. Competitive differentiation increasingly depends on sustainability performance, sealing technology advancements, and customized packaging solutions tailored to specific end-use industries.

Key Players List

- Amcor plc

- Berry Global Inc.

- Constantia Flexibles Group GmbH

- Mondi Group

- Coveris Holdings S.A.

- Winpak Ltd.

- Sealed Air Corporation

- Huhtamaki Oyj

- ProAmpac LLC

- Sonoco Products Company

- UFlex Ltd.

- Clondalkin Group

- Transcontinental Inc.

- Schur Flexibles Group

- Glenroy Inc.

- FlexPak Services LLC

- Printpack Inc.