Shrink Label Films Market Size and Growth

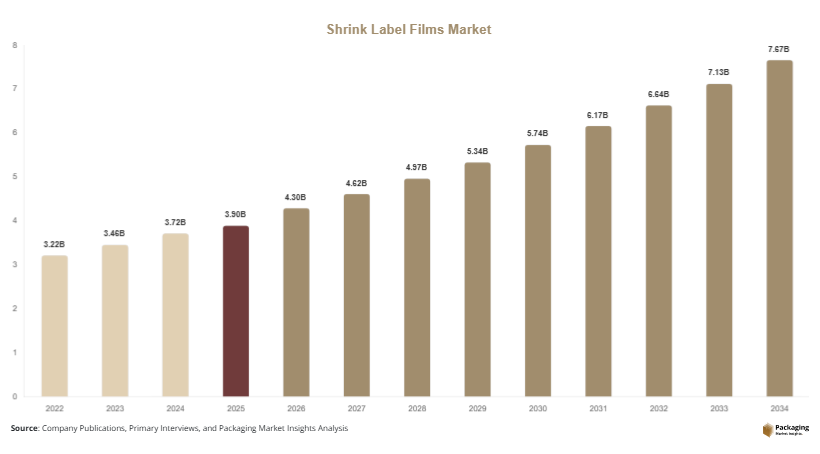

In 2025, the global shrink label films market size is estimated at USD 3.9 billion, and it is projected to reach USD 4.3 billion in 2026. By 2034, the market is expected to attain approximately USD 7.8 billion, registering a CAGR of 7.5% during 2025–2034. This growth reflects the increasing adoption of shrink sleeve labeling technologies in both developed and emerging economies. The shrink label films market is witnessing steady expansion due to increasing demand for premium packaging aesthetics, brand differentiation, and high-performance labeling solutions across beverage, personal care, household products, and pharmaceutical industries.

The market expansion is driven by several key factors. One of the primary drivers is the rising demand for visually appealing packaging, where shrink label films provide 360-degree branding coverage, enhancing shelf visibility. Another major factor is the growth of bottled beverage consumption, particularly in carbonated drinks, juices, and functional beverages, where shrink labels offer durability and resistance to moisture and abrasion. Additionally, advancements in polymer film technologies, including improved shrink performance and recyclability, are supporting broader adoption across FMCG industries.

Key Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

- Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led the segment with 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

- China remained dominant with USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Full-Body Shrink Sleeve Labeling Solutions

The adoption of full-body shrink sleeve labeling is increasing rapidly across beverage, cosmetics, and household product industries. These films provide 360-degree coverage, allowing brands to utilize the entire container surface for high-impact graphics and promotional messaging. This trend is particularly strong in carbonated soft drinks and energy beverages, where shelf competition is intense. Manufacturers are investing in advanced printing technologies such as gravure and digital printing to enhance visual appeal and support short production runs. Additionally, shrink films are being engineered with improved shrink ratios and clarity, enabling better conformity to complex container shapes. This trend is reshaping packaging design strategies across FMCG sectors.

Shift Toward Sustainable and Recyclable Shrink Film Materials

Sustainability is becoming a major trend in the shrink label films market as regulatory pressure and consumer awareness continue to rise. Manufacturers are increasingly developing recyclable PET-G and polyolefin-based shrink films that support circular economy initiatives. Brands are shifting away from PVC-based shrink films due to environmental concerns and recyclability limitations. Additionally, lightweight film structures are being introduced to reduce material consumption while maintaining performance. Companies are also investing in bio-based polymers and mono-material labeling systems to improve recycling efficiency. This transition is expected to redefine material innovation standards in shrink labeling applications globally.

Market Drivers

Expanding Beverage Industry and High Demand for Decorative Labeling

The rapid expansion of the beverage industry is a key driver of the shrink label films market. Carbonated soft drinks, bottled water, energy drinks, and functional beverages rely heavily on shrink sleeve labels to differentiate products in competitive retail environments. These labels offer superior graphics, durability, and resistance to moisture and temperature variations, making them ideal for beverage packaging. Increasing urbanization and changing consumer lifestyles are boosting packaged beverage consumption globally. Additionally, beverage manufacturers are focusing on premium packaging aesthetics to enhance brand identity, further increasing the adoption of shrink label films across global markets.

Growth in Premium Packaging and Brand Differentiation Strategies

Another major driver is the growing emphasis on premium packaging and brand differentiation across FMCG and personal care industries. Shrink label films provide full-body coverage, enabling brands to create visually appealing designs that enhance consumer engagement. Companies are increasingly using shrink sleeves for seasonal packaging, promotional campaigns, and limited-edition product launches. The flexibility of shrink films allows for high customization and compatibility with complex container shapes, making them a preferred choice for premium packaging strategies. Rising competition in retail and e-commerce channels is further accelerating the demand for high-quality labeling solutions.

Market Restraint

Recycling Challenges Associated with Multi-Layer Shrink Films

One of the major restraints in the shrink label films market is the recycling difficulty associated with multi-layer shrink film structures. Many shrink sleeves are made from materials that differ from the primary packaging container, which complicates recycling processes and reduces material recovery efficiency. In particular, PVC-based shrink films pose environmental challenges due to their limited recyclability and potential contamination in PET recycling streams. This has led to increasing regulatory scrutiny and pressure on manufacturers to transition toward mono-material and recyclable alternatives. However, the cost and performance trade-offs associated with sustainable alternatives remain a challenge for widespread adoption.

Market Opportunities

Expansion of Recyclable PET-Based Shrink Film Technologies

The development of recyclable PET-based shrink films presents a significant opportunity in the market. These films are compatible with existing PET recycling streams, improving sustainability performance and reducing environmental impact. Technological advancements are enabling improved shrink properties, clarity, and printability while maintaining recyclability. Beverage and personal care brands are increasingly adopting PET-G shrink sleeves to align with sustainability targets. As recycling infrastructure improves globally, the adoption of PET-based shrink films is expected to accelerate, opening new growth avenues for manufacturers focusing on eco-friendly packaging solutions.

Increasing Demand from E-Commerce and Customized Packaging Applications

The rapid expansion of e-commerce platforms is creating strong demand for customized and visually distinctive packaging solutions. Shrink label films are increasingly being used for branding, tamper evidence, and product differentiation in online retail packaging. Companies are leveraging digital printing technologies to produce short-run, customized shrink labels for seasonal campaigns and regional markets. This flexibility allows brands to respond quickly to consumer trends and marketing strategies. Additionally, the rise of direct-to-consumer brands is further increasing demand for high-quality shrink labeling solutions that enhance product visibility and brand identity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.9 Billion |

| Market Size in 2026 | USD 4.3 Billion |

| Market Size in 2034 | USD 7.8 Billion |

| CAGR | 7.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Material Type Segment

The Material Type segment is primarily dominated by PVC-based shrink films, which accounted for approximately 36.2% share in 2024. These films are widely used due to their high shrink performance, cost efficiency, and excellent printability. PVC shrink films are commonly used in beverage packaging, household products, and personal care items. Their ability to conform to complex container shapes makes them a preferred choice among manufacturers. However, environmental concerns are gradually shifting preferences toward alternative materials.

The fastest-growing subsegment is PET-G shrink films, projected to expand at a CAGR of 8.2%, driven by increasing demand for recyclable and environmentally friendly packaging solutions. These films offer superior clarity, recyclability, and compatibility with PET recycling streams. Beverage companies are increasingly adopting PET-G shrink sleeves to meet sustainability targets and regulatory requirements. Continuous innovation in polymer technology is enhancing shrink performance and expanding application scope.

Application Segment

The beverage packaging segment dominated applications with a 44.5% share in 2024, driven by strong consumption of bottled water, carbonated drinks, and energy beverages. Shrink label films are widely used in this segment due to their durability and high visual impact. Brands rely on shrink sleeves to differentiate products in highly competitive retail environments.

The personal care and cosmetics segment is the fastest-growing application, projected at a CAGR of 7.9%, driven by increasing demand for premium packaging and product differentiation. Shrink labels are used for shampoos, lotions, and skincare products to enhance shelf appeal and branding opportunities.

End-Use Segment

The FMCG sector dominated the end-use segment with a 49.1% share in 2024, driven by large-scale packaging requirements across food, beverage, and household products. Shrink films are extensively used for branding and product identification in retail environments.

The e-commerce sector is the fastest-growing end-use category, expanding at a CAGR of 8.1%, driven by increasing demand for customized packaging solutions. Brands are using shrink labels for tamper evidence and enhanced product presentation in online retail channels.

Shrink Label Films Market Segmentations

By Material Type

- PVC Shrink Films

- PET-G Shrink Films

- OPS (Oriented Polystyrene) Films

- Polyolefin Shrink Films

By Application

- Beverage Packaging

- Food Packaging

- Personal Care & Cosmetics

- Household Products

- Pharmaceutical Packaging

By End Use

- FMCG Industry

- E-commerce Industry

- Retail Industry

- Healthcare Industry

- Industrial Sector

Regional Analysis

North America

North America accounted for approximately 26.9% market share in 2025, with a projected CAGR of 7.2% through 2034. Growth is driven by strong demand from beverage and personal care industries, along with increasing adoption of premium packaging solutions across retail channels.

The United States dominates the regional market due to advanced packaging technologies and strong FMCG presence. A key growth factor is the rising demand for sustainable shrink films driven by corporate ESG commitments and regulatory pressure on plastic usage.

Europe

Europe held around 28.1% market share in 2025, with a CAGR of 7.4% projected through 2034. The region benefits from strict environmental regulations and high adoption of recyclable packaging materials across industries.

Germany leads the European market due to its strong manufacturing base and advanced recycling infrastructure. A key growth factor is the European Union’s focus on circular packaging systems and reduction of non-recyclable plastic waste.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025, growing at a CAGR of 8.3%. The region is driven by large-scale beverage production, rapid urbanization, and expanding FMCG consumption.

China remains the leading country due to strong manufacturing capabilities and growing packaging demand. A key growth factor is the expansion of domestic beverage industries and increasing investment in advanced packaging technologies.

Middle East & Africa

The Middle East & Africa region accounted for 4.8% market share in 2025, with a CAGR of 6.4%. Growth is supported by increasing retail expansion and gradual adoption of modern packaging solutions.

South Africa leads the region due to rising FMCG distribution networks. A key growth factor is increasing investment in packaged food and beverage industries.

Latin America

Latin America held 2.8% market share in 2025, with the fastest CAGR of 6.2%. The region is experiencing rising demand for branded packaging solutions in food and beverage sectors.

Brazil dominates the market due to strong beverage consumption and retail expansion. A key growth factor is increasing adoption of visually enhanced packaging to support brand competitiveness.

Competitive Landscape

The shrink label films market is moderately consolidated, with key players focusing on innovation, sustainability, and capacity expansion. Major companies include Amcor Plc, CCL Industries Inc., Huhtamaki Oyj, Fuji Seal International, and Klöckner Pentaplast Group. Amcor Plc remains a leading player due to its strong global presence and advanced shrink film portfolio.

Recent developments include expansion of recyclable shrink film production lines, investment in PET-based sustainable labeling solutions, and integration of digital printing technologies for customized packaging applications across global markets.

Key Players List

- Amcor Plc

- CCL Industries Inc.

- Huhtamaki Oyj

- Fuji Seal International Inc.

- Klöckner Pentaplast Group

- Berry Global Inc.

- Taghleef Industries

- Constantia Flexibles

- Coveris Holdings S.A.

- Multi-Color Corporation

- WestRock Company

- Bemis Company Inc.

- Toray Industries Inc.

- Innovia Films

- Sealed Air Corporation