Flexible Intermediate Bulk Container Market Size and Growth

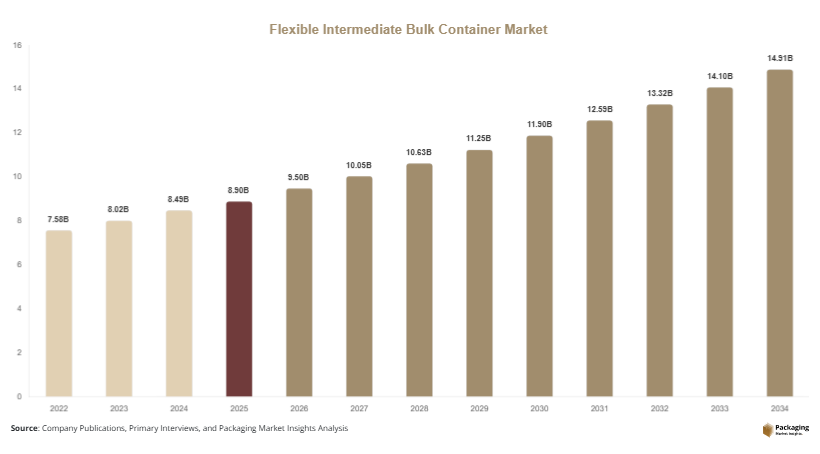

The global flexible intermediate bulk container market size was valued at USD 8.9 billion in 2025 and is projected to reach USD 9.5 billion in 2026. By 2034, the market is expected to attain approximately USD 15.8 billion, registering a CAGR of 5.8% during the forecast period (2025–2034). The flexible intermediate bulk container market is experiencing consistent growth due to increasing demand for cost-effective bulk packaging and transportation solutions across industries such as chemicals, food and beverages, pharmaceuticals, agriculture, mining, and construction. Flexible Intermediate Bulk Containers (FIBCs), commonly referred to as bulk bags or jumbo bags, are widely used for storing and transporting dry, flowable products. Their lightweight design, high load-bearing capacity, reusability, and ease of handling make them a preferred alternative to rigid bulk packaging formats.

Several factors are contributing to market growth. First, increasing international trade activities and expanding industrial production are driving demand for efficient bulk transportation solutions. Second, the growing agricultural sector requires reliable packaging for grains, seeds, fertilizers, and animal feed, creating substantial opportunities for FIBC manufacturers. Third, rising demand from the chemical industry for safe and compliant packaging solutions is supporting market expansion. Furthermore, the growing focus on sustainable and reusable packaging is encouraging industries to adopt FIBCs due to their lower environmental impact compared to many traditional bulk packaging formats.

Key Market Insights

- Asia Pacific dominated the market with a 41.2% share in 2025, while .

- America is projected to grow at the fastest CAGR of 6.6%.

- Type C conductive FIBCs led the type segment with a 31.7% share.

- Polypropylene-based containers dominated the material segment with a 78.9% share.

- Chemicals applications led the end-use segment with 35.8% share, while pharmaceutical applications are expected to grow at a CAGR of 7.2%.

- The US remained the dominant country with a market size of USD 1.8 billion in 2025 and USD 1.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Reusable Bulk Packaging Solutions

Sustainability has become a major trend within the flexible intermediate bulk container market. Industrial companies are increasingly seeking reusable packaging solutions that reduce waste generation and lower transportation costs. FIBCs can often be reused multiple times depending on their design specifications, making them attractive for manufacturers focused on environmental goals. For example, food processing and agricultural companies are implementing closed-loop logistics systems that allow bulk bags to be collected, inspected, and reused. This trend is expected to accelerate as environmental regulations become stricter across major economies. Future developments in recyclable woven polypropylene materials and circular packaging programs will further strengthen the role of sustainable FIBCs in global supply chains.

Growth of Specialized FIBCs for Hazardous and Sensitive Materials

Manufacturers are increasingly developing specialized FIBCs designed for handling hazardous chemicals, pharmaceutical ingredients, and combustible powders. Anti-static, conductive, and food-grade bulk containers are gaining traction due to rising safety requirements across industries. For instance, chemical manufacturers increasingly utilize Type C and Type D FIBCs to prevent electrostatic discharge during transportation. Pharmaceutical companies are also adopting high-purity bulk bags designed to minimize contamination risks. The future impact of this trend will be significant as industrial safety regulations continue evolving. Increased investment in advanced materials, traceability systems, and compliance-focused packaging solutions is expected to create new growth opportunities for manufacturers.

Market Drivers

Expanding Global Chemical Manufacturing Industry

The rapid growth of the chemical industry remains a major driver of the flexible intermediate bulk container market. Chemicals often require secure bulk packaging solutions that support safe transportation and storage. FIBCs offer high load capacity, chemical resistance, and compatibility with automated handling systems. As chemical production expands across Asia Pacific, North America, and the Middle East, demand for industrial bulk packaging continues to rise. For example, fertilizer and petrochemical manufacturers increasingly rely on FIBCs to improve logistics efficiency and reduce packaging costs. The expansion of chemical exports and industrial production capacities is expected to sustain strong market demand over the coming years.

Increasing Demand from Agriculture and Food Processing Sectors

Agriculture and food processing industries represent another significant growth driver. Bulk bags are extensively used for grains, sugar, flour, seeds, animal feed, and agricultural inputs. Their lightweight design and cost efficiency make them suitable for large-volume transportation. As global food production continues to increase to meet population growth, demand for bulk packaging solutions is rising accordingly. For example, grain exporters utilize food-grade FIBCs to improve handling efficiency and reduce product losses during transportation. Continued investments in agricultural infrastructure and food supply chains are expected to support long-term market growth.

Market Restraint

Volatility in Polypropylene Prices and Regulatory Compliance Challenges

A key restraint affecting the flexible intermediate bulk container market is the volatility of polypropylene prices, which directly impacts manufacturing costs. Polypropylene remains the primary raw material used in FIBC production, making manufacturers vulnerable to fluctuations in petrochemical markets. Sudden increases in raw material costs can reduce profit margins and create pricing challenges for suppliers. Additionally, compliance with industry-specific regulations related to food safety, pharmaceutical packaging, and hazardous materials handling can increase production complexity. For example, manufacturers serving pharmaceutical clients must adhere to strict quality and contamination control standards. These factors can limit profitability and increase operational costs, particularly for smaller producers competing in highly price-sensitive markets.

Market Opportunities

Growth of Pharmaceutical Bulk Packaging Applications

The pharmaceutical industry presents substantial opportunities for FIBC manufacturers. Increasing production of active pharmaceutical ingredients and bulk pharmaceutical intermediates is creating demand for contamination-resistant bulk packaging solutions. Specialized pharmaceutical-grade FIBCs help maintain product integrity throughout transportation and storage processes. For example, pharmaceutical manufacturers increasingly require bulk bags with enhanced hygiene controls and traceability features. Future growth in pharmaceutical manufacturing, particularly in Asia Pacific and Europe, is expected to create new opportunities for advanced FIBC solutions.

Expansion of Emerging Market Logistics Infrastructure

Rapid infrastructure development across emerging economies offers significant growth potential for the flexible intermediate bulk container market. Investments in ports, warehouses, transportation networks, and industrial parks are improving bulk goods movement across regions. Countries in Southeast Asia, Latin America, and Africa are expanding logistics capabilities to support manufacturing and export activities. FIBCs play an important role in these supply chains by providing efficient packaging for bulk commodities. Continued industrialization and trade growth are expected to generate strong demand for bulk packaging solutions throughout the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.9 Billion |

| Market Size in 2026 | USD 9.5 Billion |

| Market Size in 2034 | USD 15.8 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Type C conductive FIBCs dominated the market in 2024, accounting for approximately 31.7% of total revenue. These containers are widely used for transporting flammable powders and hazardous chemicals where electrostatic discharge presents safety risks. Industries such as chemicals, petrochemicals, and specialty materials rely heavily on conductive FIBCs to meet stringent safety standards. Their ability to dissipate static electricity through grounding systems makes them suitable for demanding industrial environments. The growing emphasis on workplace safety and regulatory compliance continues to support segment dominance. Major chemical manufacturers increasingly specify Type C FIBCs as part of their packaging requirements, contributing to sustained demand across industrial applications.

Type D anti-static FIBCs are expected to be the fastest-growing subsegment, registering a CAGR of 6.8% during the forecast period. Unlike conductive bulk bags, Type D FIBCs do not require grounding while still providing protection against electrostatic hazards. This convenience enhances operational efficiency and reduces handling complexity. Growing demand from pharmaceutical, food processing, and specialty chemical industries is supporting adoption. Manufacturers continue to improve fabric technologies to enhance safety performance and durability. Future demand is expected to increase as industrial users seek packaging solutions that combine safety, convenience, and compliance.

By Material

Polypropylene-based FIBCs held the largest market share in 2024, accounting for approximately 78.9% of total revenue. Polypropylene offers high tensile strength, durability, flexibility, and cost efficiency, making it the preferred material for bulk bag manufacturing. The material performs well across a wide range of industrial applications including chemicals, agriculture, food processing, and construction materials. For example, woven polypropylene bulk bags are extensively used for transporting fertilizers, grains, minerals, and powdered chemicals. Continuous improvements in woven fabric technology further strengthen the dominance of polypropylene within the market.

Recyclable composite materials are projected to be the fastest-growing material segment, expanding at a CAGR of 6.5% through 2034. Sustainability objectives are encouraging manufacturers to explore alternative material structures that improve recyclability while maintaining performance standards. Innovations in composite fabrics and recycled content integration are supporting segment growth. Industrial companies increasingly seek packaging solutions aligned with environmental goals and corporate sustainability commitments. Future advancements in material science are expected to enhance durability and recyclability, creating additional growth opportunities.

By End-Use

The chemicals segment dominated the market in 2024 with approximately 35.8% share of total revenue. Chemical manufacturers require reliable bulk packaging solutions capable of handling powders, granules, and specialty materials safely. FIBCs provide cost-effective transportation while meeting industry safety standards. Applications include fertilizers, polymers, petrochemicals, pigments, and industrial additives. Growing global chemical production and international trade continue to support segment dominance. Packaging suppliers increasingly offer customized solutions designed to meet specific handling and storage requirements within chemical supply chains.

The pharmaceutical segment is expected to register the fastest CAGR of 7.2% through 2034. Increasing pharmaceutical production, stricter quality standards, and rising demand for active pharmaceutical ingredients are supporting growth. Pharmaceutical manufacturers require high-purity packaging solutions that minimize contamination risks and maintain product integrity. Advanced FIBCs featuring traceability systems, hygienic designs, and enhanced barrier properties are gaining traction. Future growth is expected to be supported by expanding pharmaceutical manufacturing capacities across Asia Pacific, Europe, and North America.

Flexible Intermediate Bulk Container Market Segmentations

By Type

- Type A FIBCs

- Type B FIBCs

- Type C Conductive FIBCs

- Type D Anti-Static FIBCs

By Material

- Polypropylene

- Composite Materials

- Recycled Polypropylene

- Specialty Fabrics

By End-User

- Chemicals

- Agriculture

- Food & Beverage

- Pharmaceuticals

- Construction & Mining

Regional Analysis

North America

North America accounted for approximately 24.7% of the global flexible intermediate bulk container market share in 2025 and is expected to register a CAGR of 5.2% through 2034. The region benefits from strong industrial activity, advanced logistics infrastructure, and significant demand from chemical, food, and agricultural sectors. Growing emphasis on supply chain efficiency and sustainability is encouraging businesses to adopt reusable bulk packaging solutions. Manufacturers are increasingly investing in high-performance FIBCs that comply with stringent safety and regulatory standards. The presence of established industrial packaging suppliers further supports market development across the region.

The United States dominates the North American market. A unique growth driver is the expansion of domestic chemical production supported by abundant raw material availability. Chemical manufacturers continue to invest in export-oriented operations, increasing demand for safe bulk transportation solutions. A notable industry trend involves growing adoption of anti-static FIBCs for hazardous material handling. The country's advanced logistics network and industrial automation initiatives are expected to support long-term market growth.

Europe

Europe represented approximately 22.1% of global market revenue in 2025 and is forecast to expand at a CAGR of 5.5% during the forecast period. Sustainability objectives and stringent industrial safety regulations are driving demand for high-quality FIBCs across the region. The chemical, food processing, and pharmaceutical industries remain key consumers of bulk packaging solutions. European companies are increasingly implementing reusable packaging systems to reduce waste and improve resource efficiency. Furthermore, growth in cross-border trade activities continues to support demand for efficient bulk transportation packaging.

Germany remains the dominant country within Europe. A unique growth factor is the country's strong industrial manufacturing base, particularly in chemicals and specialty materials. German companies are increasingly investing in advanced bulk handling technologies that integrate seamlessly with automated logistics systems. A growing trend involves adoption of smart tracking technologies within industrial packaging operations. These developments are expected to support continued market expansion throughout the country.

Asia Pacific

Asia Pacific dominated the market with a 41.2% share in 2025 and is expected to register a CAGR of 6.3% through 2034. Rapid industrialization, increasing exports, and strong growth in agriculture and chemical production are driving regional demand. Countries throughout the region are expanding manufacturing capacities and investing in logistics infrastructure, creating favorable conditions for bulk packaging suppliers. Rising food production and fertilizer consumption are also contributing to increased FIBC utilization. The region continues to serve as a major manufacturing hub for bulk packaging products and industrial commodities.

China is the dominant country in Asia Pacific. A unique growth driver is the country's extensive export-oriented manufacturing sector. Bulk bags are widely utilized for transporting chemicals, minerals, agricultural products, and industrial materials. An industry trend involves increasing adoption of recyclable FIBCs as manufacturers seek to align with sustainability initiatives. Continued industrial expansion and trade growth are expected to support robust market demand.

Middle East & Africa

The Middle East & Africa accounted for approximately 5.1% of market revenue in 2025 and is projected to grow at a CAGR of 5.9% through 2034. Growth is supported by increasing investments in petrochemicals, mining, and agricultural sectors. Demand for efficient bulk transportation solutions is rising as regional industries expand production and export activities. Governments are also investing in logistics infrastructure to strengthen international trade capabilities. FIBCs provide cost-effective packaging solutions for transporting bulk commodities across domestic and international markets.

Saudi Arabia dominates the regional market. A unique growth factor is the country's large-scale petrochemical industry. Bulk packaging demand continues to increase as chemical exports expand. A notable trend involves investments in industrial logistics zones designed to improve supply chain efficiency. These developments are expected to generate sustained demand for industrial packaging products, including FIBCs.

Latin America

Latin America held approximately 6.9% of the global market share in 2025 and is projected to record the fastest CAGR of 6.6% through 2034. Agricultural exports, mining activities, and industrial production are driving market growth across the region. Countries are increasingly investing in export infrastructure to support commodity shipments. Demand for durable and cost-efficient packaging solutions continues to rise among agricultural producers and mining companies. The region offers substantial growth potential due to expanding trade volumes and industrialization efforts.

Brazil remains the dominant country within Latin America. A unique growth driver is the country's strong agricultural export industry. Bulk bags are extensively used for transporting soybeans, sugar, coffee, and animal feed products. An industry trend involves increasing use of food-grade FIBCs to support agricultural exports. These developments are expected to contribute significantly to regional market growth.

Competitive Landscape

The flexible intermediate bulk container market is moderately consolidated, with leading companies focusing on product innovation, geographic expansion, and sustainability initiatives. Competition is driven by pricing, product quality, regulatory compliance, and customer-specific customization capabilities.

Berry Global Inc. is recognized as a market leader due to its extensive industrial packaging portfolio and global manufacturing footprint. The company recently expanded its sustainable industrial packaging solutions by introducing recyclable bulk bag materials designed to reduce environmental impact while maintaining performance standards.

Other major players include Greif Inc., LC Packaging International BV, Conitex Sonoco, and BAG Corp. These companies continue to invest in advanced material technologies, anti-static packaging solutions, and enhanced logistics support services. Strategic partnerships with chemical, food, and pharmaceutical manufacturers remain common growth strategies. The competitive landscape is expected to evolve further as sustainability and industrial safety requirements continue to shape purchasing decisions.

Key Players List

- Berry Global Inc.

- Greif Inc.

- LC Packaging International BV

- Conitex Sonoco

- BAG Corp

- Global-Pak Inc.

- Rishi FIBC Solutions Pvt. Ltd.

- Intertape Polymer Group

- Emmbi Industries Ltd.

- Halsted Corporation

- Jumbo Bag Ltd.

- Taihua Group

- Langston Companies Inc.

- United Bags Inc.

- Plastene India Limited

- Bulk Lift International LLC

- AmeriGlobe LLC

- Virgo Polymer India Ltd.