Carrier Bags Market Size and Growth

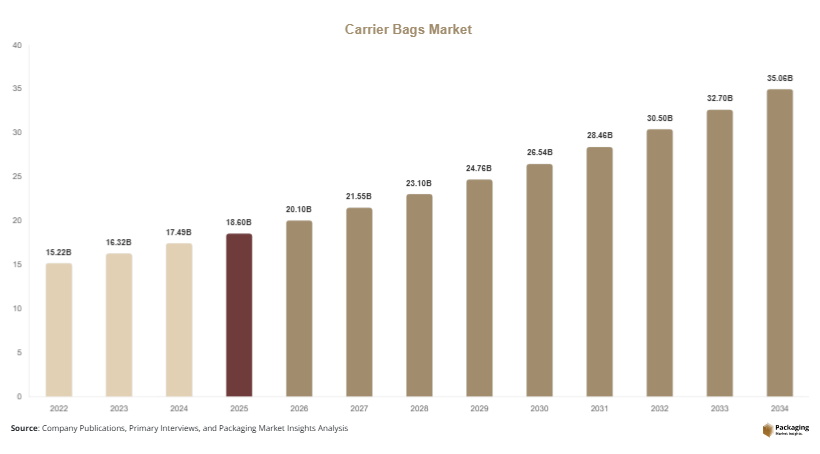

The global carrier bags market is estimated at approximately USD 18.6 billion in 2025, and it is projected to reach around USD 20.1 billion in 2026. By 2034, the market is forecasted to attain nearly USD 35.4 billion, expanding at a CAGR of 7.2% during 2025–2034. The carrier bags market has evolved into a structurally significant segment of the global packaging industry, driven by rapid expansion in retail, e-commerce, grocery distribution, and food delivery ecosystems. Carrier bags, including plastic, paper, biodegradable, and reusable variants, serve as essential packaging solutions for carrying consumer goods across organized and unorganized retail channels.

The market growth is supported by multiple structural factors. First, the rapid expansion of modern retail formats such as supermarkets, hypermarkets, and convenience stores is significantly increasing the demand for standardized and branded carrier bags. Second, the rising penetration of e-commerce and food delivery platforms is creating sustained demand for durable, lightweight, and tamper-evident packaging solutions. Third, increasing environmental awareness is pushing manufacturers to innovate in recyclable and biodegradable carrier bag materials, leading to product diversification and regulatory compliance-driven demand shifts.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 12.4 billion in 2025 and USD 13.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Biodegradable and Compostable Carrier Bags

The carrier bags market is experiencing a strong shift toward biodegradable and compostable materials as environmental regulations become stricter worldwide. Manufacturers are increasingly investing in bio-based polymers such as PLA, PHA, and starch blends to reduce environmental impact. Retailers in Europe and North America are replacing conventional plastic bags with compostable alternatives to comply with government mandates and consumer expectations. For example, supermarket chains are introducing compostable checkout bags made from corn-starch blends that degrade under industrial composting conditions. This transition is expected to significantly influence production strategies, supply chain sourcing, and material innovation. In the long term, biodegradable carrier bags are likely to become a standard offering, particularly in urban retail environments, as sustainability becomes a key purchasing criterion.

Growth of Branded and Custom Printed Carrier Bags

Another key trend shaping the carrier bags market is the rising demand for branded and customized carrier bags used as marketing tools. Retailers, restaurants, and e-commerce companies are increasingly using carrier bags as promotional assets by incorporating logos, QR codes, and personalized designs. This trend is particularly strong in fashion retail, food delivery services, and luxury goods packaging. For instance, premium retail stores are investing in high-quality paper carrier bags with matte finishes and embossed branding to enhance customer experience. The growth of digital printing technologies has made customization more cost-effective, enabling small and medium enterprises to adopt branded packaging. In the future, smart carrier bags with embedded digital tracking or interactive features may further enhance marketing value.

Market Drivers

Expansion of Organized Retail and E-commerce Platforms

The rapid expansion of organized retail and e-commerce platforms is a major driver for the carrier bags market. As supermarkets, hypermarkets, and online grocery services expand, the demand for standardized packaging solutions increases significantly. Carrier bags are essential for last-mile packaging, especially in food delivery and quick-commerce services. For example, online grocery platforms in urban Asia are heavily dependent on durable plastic and paper carrier bags to ensure safe transportation of products. The increasing frequency of online orders is directly translating into higher consumption of carrier bags, particularly in densely populated urban regions. This structural shift in consumer purchasing behavior continues to accelerate market demand globally.

Rising Demand for Sustainable Packaging Solutions

The growing emphasis on environmental sustainability is driving innovation and adoption of eco-friendly carrier bags. Governments and regulatory bodies are enforcing restrictions on single-use plastics, pushing manufacturers toward recyclable and biodegradable materials. Retailers are also adopting sustainability goals, replacing conventional bags with reusable or compostable alternatives. For example, several European supermarket chains have eliminated plastic checkout bags entirely, replacing them with paper-based alternatives. This transition is creating new growth opportunities for material manufacturers and packaging converters. Over time, sustainability-driven demand is expected to reshape the entire competitive structure of the carrier bags market.

Market Restraint

The primary restraint in the carrier bags market is the increasing regulatory pressure and fluctuating raw material costs. Strict government regulations on plastic usage, especially in developed economies, are forcing manufacturers to redesign product portfolios, which increases production complexity and cost. Additionally, raw material price volatility, particularly for petroleum-based plastics and bio-polymers, creates margin pressure for manufacturers. Small-scale producers are especially affected due to limited capacity to absorb cost fluctuations. For example, sudden increases in resin prices directly impact plastic bag manufacturing costs, leading to pricing instability in retail supply chains. Furthermore, the transition to sustainable alternatives requires significant capital investment in new machinery and material sourcing systems, which can slow market adoption in cost-sensitive regions.

Market Opportunities

Expansion of Reusable Carrier Bag Systems

Reusable carrier bag systems present a major opportunity in the evolving packaging landscape. Retailers and governments are encouraging consumers to shift toward reusable bags made from durable fabrics, woven plastics, and reinforced paper composites. These systems reduce long-term environmental impact and create recurring demand cycles for durable packaging solutions. For example, supermarket loyalty programs now encourage customers to bring reusable bags through discount incentives. Over time, reusable carrier bags are expected to become a mainstream alternative, particularly in urban retail ecosystems.

Innovation in Smart and Functional Packaging

Smart packaging integration represents another emerging opportunity in the carrier bags market. Carrier bags embedded with QR codes, RFID tags, or temperature indicators can enhance logistics tracking and consumer engagement. This is particularly relevant for food delivery and pharmaceutical distribution, where traceability is critical. For instance, food delivery companies are experimenting with QR-enabled bags that provide order tracking and promotional content. Future innovations may include recyclable smart bags with embedded sensors for freshness monitoring, opening new value-added applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 20.1 Billion |

| Market Size in 2034 | USD 35.4 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Type Segment

Plastic carrier bags dominate the type segment with a 2024 market share of approximately 52.3%, driven by low cost, durability, and widespread availability across retail channels. Plastic bags remain the preferred choice in emerging economies where affordability is a key factor. Supermarkets, local stores, and food vendors heavily rely on polyethylene-based bags for daily operations. For example, street retail in Asia and Africa continues to use lightweight plastic bags for groceries and takeaway food packaging. Despite environmental concerns, plastic remains dominant due to its functional efficiency and scalability in mass production. However, regulatory pressure is gradually reshaping this dominance, especially in developed economies where bans and taxes are reducing consumption.

The fastest-growing subsegment is biodegradable and reusable carrier bags, projected to grow at a CAGR of 8.3%. Growth is driven by environmental regulations, consumer awareness, and corporate sustainability initiatives. Paper-based and compostable bags are increasingly used in supermarkets and premium retail outlets. For example, fashion retailers are adopting reusable fabric bags as part of brand identity strategies. Future outlook suggests that hybrid materials combining strength and biodegradability will gain traction, reducing dependency on conventional plastics while maintaining performance standards.

Material Segment

Plastic materials hold the dominant position in the material segment with a 2024 share of 54.1%, primarily due to polyethylene and polypropylene usage. These materials offer flexibility, water resistance, and cost efficiency, making them ideal for large-scale retail applications. Grocery stores, convenience shops, and food delivery platforms rely heavily on plastic-based carrier bags for everyday use. Industrial-scale manufacturing in Asia ensures consistent supply and affordability, reinforcing dominance across developing regions. However, environmental concerns are pushing gradual substitution with alternative materials.

The fastest-growing material subsegment is paper-based carrier bags, with a CAGR of 7.4%. Growth is fueled by sustainability mandates and rising demand for recyclable packaging. Paper bags are widely adopted in premium retail, bakery chains, and eco-conscious supermarkets. For instance, European retail chains have fully transitioned to kraft paper bags for checkout operations. Future developments include reinforced paper composites and water-resistant coatings, expanding application potential in food delivery and retail logistics.

End-Use Segment

Food & beverage remains the dominant end-use segment with a 43.1% market share in 2024, driven by grocery shopping, takeaway services, and food delivery platforms. Carrier bags are essential for transporting packaged food, beverages, and daily essentials. Supermarkets and quick-service restaurants rely heavily on standardized carrier bag systems for customer convenience. For example, global food delivery platforms use branded carrier bags to maintain hygiene and product integrity during transit.

The fastest-growing end-use segment is healthcare, projected to grow at a CAGR of 6.9%. Growth is driven by increasing pharmaceutical distribution, home healthcare services, and medical retail expansion. Carrier bags are used for medicine packaging, diagnostic kits, and medical supply distribution. For example, pharmacies are increasingly using tamper-evident bags for prescription delivery. Future demand will be supported by regulatory compliance requirements and rising healthcare accessibility in emerging economies.

Carrier Bags Market Segmentations

By Type

- Plastic Carrier Bags

- Paper Carrier Bags

- Biodegradable Carrier Bags

- Reusable Carrier Bags

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Paper/Kraft

- Biopolymers (PLA, PHA)

- Fabric-based Materials

By End-Use

- Food & Beverage

- Retail & E-commerce

- Healthcare

- Industrial Use

- Hospitality

By Region

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Regional Analysis

North America

North America holds approximately 23.8% share of the carrier bags market in 2025, supported by strong retail infrastructure and high consumption of packaged goods. The region is projected to grow at a CAGR of 6.8% from 2025 to 2034, driven by sustainability regulations and rising adoption of eco-friendly packaging. The market is characterized by a strong shift from plastic to paper and reusable carrier bags, particularly in urban retail environments. Growth is also supported by the expansion of organized retail chains and e-commerce logistics networks.

The United States dominates the regional market, driven by large-scale supermarket chains and advanced packaging manufacturing capabilities. A key growth driver is the increasing adoption of reusable and premium branded carrier bags in retail stores. For example, major retail chains are replacing single-use plastic bags with recyclable paper alternatives featuring custom branding. Canada also contributes significantly, with provincial regulations accelerating plastic bag bans and promoting biodegradable alternatives. The regional market is further supported by innovations in sustainable materials and strong consumer awareness regarding environmental impact.

Europe

Europe accounts for around 21.5% market share in 2025, with a projected CAGR of 7.1% during the forecast period. The region has one of the strictest regulatory environments globally, significantly influencing carrier bag design and material selection. The market is heavily driven by sustainability directives, circular economy policies, and consumer preference for eco-friendly packaging.

Germany leads the European market due to its strong recycling infrastructure and advanced packaging industry. A key driver is the widespread adoption of compostable and paper-based carrier bags in retail chains. For example, supermarkets across Germany have eliminated plastic checkout bags and transitioned to certified biodegradable alternatives. The United Kingdom and France are also major contributors, with government-led initiatives reducing plastic consumption and promoting reusable bag systems. Europe’s innovation in bio-based materials continues to shape global carrier bag standards.

Asia Pacific

Asia Pacific dominates the global carrier bags market with a 37.4% share in 2025, and is expected to grow at a CAGR of 7.6% through 2034. The region benefits from large population size, rapid urbanization, and expanding retail infrastructure. High consumption of packaged goods and growing e-commerce penetration further strengthen market demand.

China remains the largest market, driven by massive retail networks and manufacturing capabilities. A key growth factor is the rapid expansion of online retail and food delivery services, which significantly increases carrier bag consumption. For instance, Chinese quick-commerce platforms rely heavily on high-volume packaging for same-day delivery services. India is also emerging rapidly due to rising disposable income and expansion of supermarket chains. Southeast Asian countries contribute through tourism-driven retail consumption and growing urban retail formats.

Middle East & Africa

The Middle East & Africa region holds approximately 9.2% share in 2025, with a CAGR of 6.4% through 2034. The market is gradually expanding due to increasing retail modernization, tourism growth, and infrastructure development. The region is witnessing a shift from traditional plastic bags toward more regulated packaging systems.

Saudi Arabia leads the regional market, supported by retail diversification initiatives under economic transformation programs. A key driver is the expansion of shopping malls and organized retail centers. For example, large retail developments in Riyadh and Dubai are increasingly adopting branded paper carrier bags. South Africa also plays a significant role due to its growing supermarket chains and packaging import demand. Environmental awareness is slowly increasing, encouraging adoption of sustainable carrier bag solutions.

Latin America

Latin America accounts for approximately 8.1% market share in 2025, and is expected to register the fastest CAGR of 7.9% during the forecast period. The region is driven by rising retail penetration, urbanization, and increasing environmental regulations. Demand for cost-effective yet sustainable packaging is growing rapidly.

Brazil dominates the market due to its large consumer base and expanding retail sector. A key growth driver is the increasing adoption of biodegradable carrier bags in urban supermarkets. For instance, Brazilian retail chains are introducing recyclable paper bags to comply with environmental policies. Mexico is also a key contributor, supported by cross-border trade and growing organized retail. The region is expected to experience strong growth in sustainable packaging adoption over the forecast period.

Competitive Landscape

The carrier bags market is moderately fragmented, with a mix of global packaging companies and regional manufacturers. Key players include Amcor plc, Berry Global Inc., Mondi Group, Novolex Holdings, and Sealed Air Corporation. Among these, Amcor plc is considered a leading market player due to its extensive product portfolio, global manufacturing footprint, and strong focus on sustainable packaging innovation.

Companies are focusing on sustainability, material innovation, and strategic partnerships with retail chains. Berry Global is expanding its recycled plastic capabilities, while Mondi Group is investing in paper-based packaging solutions. Novolex is strengthening its presence in foodservice packaging, particularly in North America. Sealed Air is focusing on advanced protective packaging and recyclable materials.

Recent strategies include mergers, acquisitions, and expansion into emerging markets. Companies are also investing in biodegradable polymer technologies and advanced printing solutions to enhance product differentiation. The competitive landscape is expected to intensify as regulatory pressure increases demand for eco-friendly carrier bag alternatives.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi Group

- Novolex Holdings

- Sealed Air Corporation

- Huhtamaki Oyj

- Coveris Holdings

- DS Smith Plc

- Sonoco Products Company

- International Paper Company

- WestRock Company

- ProAmpac LLC

- Shenzhen Yuto Packaging Technology

- Smurfit Kappa Group

- Detmold Group