FIBC Market Size and Growth

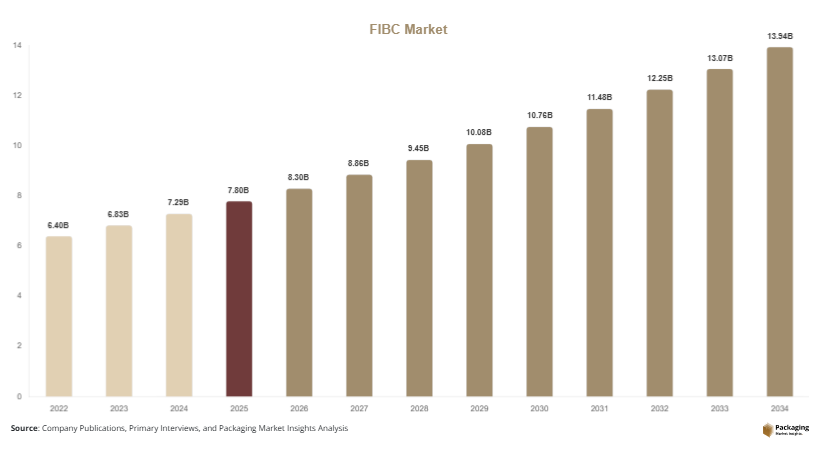

The global FIBC market size was valued at USD 7.8 billion in 2025 and is estimated to reach USD 8.3 billion in 2026. The market is forecasted to reach nearly USD 13.9 billion by 2034, registering a CAGR of 6.7% during the 2025–2034 period. The FIBC market is experiencing steady expansion due to rising demand for cost-efficient industrial bulk packaging solutions across chemicals, agriculture, food processing, pharmaceuticals, mining, and construction industries. Flexible intermediate bulk containers (FIBCs), also referred to as jumbo bags or bulk bags, are widely used for the transportation and storage of dry flowable materials because of their high load-bearing capacity, lower packaging costs, and improved logistics efficiency.

Growing industrial production and increasing international trade activities are contributing significantly to market growth. Manufacturing industries are focusing on reducing packaging waste and transportation expenses, which is increasing the adoption of reusable and recyclable FIBC solutions. The agriculture sector continues to represent a major consumer base due to rising bulk transportation requirements for grains, fertilizers, animal feed, and seeds. In addition, the expansion of chemical exports from Asian countries is increasing demand for high-strength conductive and food-grade bulk bags.

Key Market Insights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Type C conductive bags led the type segment with a 31.4% share.

- Polypropylene material dominated with a 72.6% share.

- Chemicals and fertilizers led the end-use segment with 41.8% share.

- The US remained the dominant country with a market size of USD 1.6 billion in 2025 and USD 1.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Recyclable Bulk Packaging

Sustainability has become a major trend influencing the FIBC market as manufacturers and industrial buyers focus on reducing packaging waste and improving recycling rates. End-use industries are increasingly selecting reusable polypropylene bulk bags that can support multiple shipping cycles while lowering total packaging costs. Large chemical and agricultural exporters are introducing closed-loop packaging systems where used FIBCs are collected, cleaned, and reprocessed into secondary industrial products. This trend is particularly visible in Europe and North America, where environmental regulations are encouraging businesses to reduce single-use industrial packaging.

Manufacturers are also developing lightweight woven fabrics that reduce raw material consumption without compromising tensile strength. Several packaging companies are investing in biodegradable coatings and recycled resin integration to meet sustainability targets established by multinational buyers. Over the next decade, sustainable product innovation is expected to improve procurement preference for certified recyclable FIBC products and strengthen long-term market competitiveness.

Expansion of Smart Packaging and Traceability Technologies

Digitalization in industrial supply chains is driving the integration of smart packaging technologies within the FIBC market. Companies involved in chemicals, food ingredients, and pharmaceutical distribution are increasingly using RFID tags, QR codes, and barcode tracking systems on FIBC products to improve shipment visibility and inventory management. Smart packaging enables manufacturers to monitor handling conditions, shipment locations, and stock movement in real time, reducing losses associated with inventory errors and damaged cargo.

The growing adoption of automated warehouses and industrial Internet of Things platforms is supporting this trend across developed and emerging economies. For example, food ingredient suppliers are integrating traceability systems into bulk bags to comply with stricter quality and safety regulations. Smart FIBC systems are also improving warehouse efficiency by enabling faster scanning and automated storage allocation. Future developments in digital logistics infrastructure are expected to accelerate the adoption of connected packaging systems across high-volume industrial sectors.

Market Drivers

Increasing Demand from Chemical and Agricultural Industries

The rapid growth of chemical manufacturing and agricultural trade is a major driver supporting expansion of the FIBC market. Bulk bags are widely used for transporting fertilizers, industrial powders, resins, grains, and processed agricultural products because they offer high storage efficiency and reduced transportation costs. Rising global fertilizer consumption and increasing exports of specialty chemicals from Asia are creating consistent demand for durable and contamination-resistant packaging solutions.

The chemical industry increasingly requires anti-static and conductive FIBC variants to ensure safe transportation of hazardous powders and flammable materials. Agricultural producers are also preferring FIBC solutions for handling grains and seeds due to their large carrying capacity and compatibility with mechanized loading systems. As global food demand and industrial production continue to expand, packaging suppliers are expected to witness stable order volumes from bulk commodity exporters and industrial processors.

Growth in Infrastructure and Construction Activities

Rising infrastructure investments across developing economies are significantly contributing to FIBC market growth. Construction materials such as cement, sand, minerals, and industrial additives require efficient storage and transportation systems, leading to increased demand for heavy-duty bulk packaging solutions. Governments in Asia Pacific, the Middle East, and Latin America are investing heavily in urban development, transportation projects, and industrial zones, which is supporting consumption of bulk construction materials.

FIBC bags provide logistical advantages because they reduce handling costs and simplify loading and unloading operations at construction sites. Mining companies are also adopting high-strength bulk bags for transporting ores and processed minerals across long distances. In regions experiencing rapid industrialization, packaging manufacturers are expanding production capacity to meet increasing demand from infrastructure and mining sectors. Continued public and private investment in industrial projects is expected to sustain long-term demand for bulk handling solutions.

Market Restraint

Volatility in Raw Material Prices and Recycling Challenges

Fluctuations in polypropylene prices remain a major restraint affecting the FIBC market. Polypropylene is the primary raw material used in manufacturing woven bulk bags, and its price is closely linked to crude oil market conditions. Sudden increases in oil prices or supply disruptions can significantly raise manufacturing costs for packaging producers, reducing profit margins and increasing product prices for end users. Small and medium-sized manufacturers are particularly vulnerable because they often operate with limited procurement flexibility and lower bargaining power.

In addition, recycling and disposal challenges continue to affect market expansion in regions with limited waste management infrastructure. Although reusable FIBC solutions are gaining popularity, contamination from chemicals and industrial materials can complicate recycling processes. Many developing countries lack organized collection and recycling systems for industrial plastic waste, which creates environmental concerns and regulatory pressure on manufacturers. For example, exporters handling hazardous powders often face additional cleaning and disposal costs before used bags can be recycled. These challenges may slow adoption among sustainability-focused industries and increase operational expenses for packaging suppliers.

Market Opportunities

Expansion of Pharmaceutical and Food-Grade Packaging Applications

The increasing demand for hygienic and contamination-resistant packaging solutions is creating strong opportunities for the FIBC market in pharmaceutical and food industries. Food-grade FIBC bags are being widely adopted for transporting sugar, flour, starch, dairy ingredients, and processed food additives due to their durability and cost efficiency. Pharmaceutical manufacturers are also increasing the use of cleanroom-certified bulk bags for handling active ingredients and specialty chemicals.

Stringent regulations regarding product safety and contamination control are encouraging packaging suppliers to develop advanced liner systems and sterile bulk packaging solutions. Manufacturers are investing in coated fabrics, tamper-evident closures, and moisture-resistant barriers to improve product protection during international shipments. As pharmaceutical production expands in India, China, and Europe, demand for high-performance food-grade and pharmaceutical-grade FIBC products is expected to increase substantially over the forecast period.

Rising Industrialization in Emerging Economies

Emerging economies are creating substantial growth opportunities for the FIBC market due to rapid industrialization and export expansion. Countries in Southeast Asia, Latin America, and Africa are witnessing increased investment in agriculture processing, mining, chemicals, and manufacturing sectors. These industries require efficient and economical bulk transportation solutions to support domestic distribution and international trade.

Local governments are also encouraging industrial development through infrastructure upgrades, logistics modernization, and export incentives. As industrial output increases, demand for standardized bulk packaging systems compatible with containerized shipping is expected to rise. Packaging companies are responding by establishing regional production facilities and distribution partnerships in high-growth markets. The expansion of industrial exports from countries such as Vietnam, Brazil, and South Africa is likely to create long-term opportunities for manufacturers offering cost-effective and durable FIBC solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.8 Billion |

| Market Size in 2026 | USD 8.3 Billion |

| Market Size in 2034 | USD 13.9 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Type C conductive bags accounted for the largest share of the FIBC market in 2024, representing nearly 31.4% of total revenue. These bags are widely used for transporting flammable powders and hazardous chemicals because they prevent electrostatic discharge during filling and discharge operations. Industries such as petrochemicals, specialty chemicals, and industrial powders rely heavily on conductive bulk bags to comply with safety regulations and reduce explosion risks in manufacturing facilities. Their dominance is also supported by increasing chemical exports from Asia and Europe, where workplace safety standards remain stringent. Manufacturers are continuously improving grounding systems and fabric conductivity to enhance operational reliability. The growing preference for high-performance industrial packaging among multinational chemical companies is expected to sustain demand for conductive FIBC solutions.

Ventilated FIBC bags are projected to be the fastest-growing subsegment, registering a CAGR of 7.3% during the forecast period. These bags are increasingly used in agricultural applications for products such as onions, potatoes, garlic, and firewood because they allow airflow circulation and reduce moisture accumulation. Rising global trade in fresh agricultural produce is supporting demand for ventilated packaging solutions capable of maintaining product quality during transportation and storage. Packaging manufacturers are developing reinforced ventilation panels and lightweight woven structures to improve durability and reduce handling costs. Future growth is expected to be supported by increasing food export activities and expanding cold-chain logistics infrastructure across developing economies.

By Material

Polypropylene dominated the FIBC market by material type in 2024 with a share of approximately 72.6%. The material remains highly preferred due to its strength, flexibility, moisture resistance, and cost efficiency. Polypropylene FIBC products are widely utilized in chemicals, fertilizers, food processing, and mining applications because they can withstand heavy loads while maintaining structural integrity during transportation. Manufacturers favor polypropylene because it supports high-speed weaving and customization processes, enabling large-scale production at competitive prices. The material also offers compatibility with coatings, liners, and conductive treatments used in specialized packaging applications. Rising industrial trade volumes and increasing demand for reusable packaging continue to reinforce the dominance of polypropylene-based FIBC products across global markets.

Biodegradable woven materials are expected to emerge as the fastest-growing material segment, recording a CAGR of 8.1% through 2034. Growing environmental concerns and stricter regulations on industrial plastic waste are encouraging packaging companies to develop sustainable alternatives to conventional polypropylene products. Research into biodegradable polymer blends and natural fiber composites is gaining momentum across Europe and North America. Food processing companies and environmentally conscious exporters are increasingly adopting eco-friendly packaging to strengthen sustainability commitments and improve brand positioning. Future innovations in bio-based woven fabrics, combined with government support for green manufacturing, are expected to accelerate commercialization and market adoption of biodegradable FIBC solutions.

By End-Use

Chemicals and fertilizers represented the dominant end-use segment in the FIBC market in 2024, accounting for around 41.8% of overall revenue. Bulk bags are widely used in this sector for transporting resins, industrial powders, pigments, and fertilizer products because they provide efficient handling and lower logistics costs. Chemical manufacturers prefer FIBC solutions due to their compatibility with automated filling systems and ability to safely transport hazardous materials using conductive and anti-static variants. Increasing global trade in industrial chemicals and agricultural nutrients is further supporting segment growth. Major exporters in Asia Pacific and the Middle East are expanding production capacities, leading to higher demand for durable and high-capacity packaging systems.

Pharmaceutical applications are anticipated to register the fastest CAGR of 7.5% during the forecast period. The expansion of pharmaceutical manufacturing in India, China, Europe, and North America is increasing demand for contamination-resistant and hygienic bulk packaging solutions. Pharmaceutical-grade FIBC products are designed with specialized liners, cleanroom manufacturing standards, and moisture protection features to maintain product integrity during storage and transport. Rising production of active pharmaceutical ingredients and specialty healthcare chemicals is supporting the adoption of advanced bulk packaging technologies. Future growth is likely to be driven by stricter regulatory requirements, increasing global pharmaceutical exports, and greater investment in sterile packaging innovation.

FIBC Market Segmentations

By Type

- Type A FIBC

- Type B FIBC

- Type C Conductive FIBC

- Type D Anti-Static FIBC

- Ventilated FIBC

By Material

- Polypropylene

- Polyethylene

- Biodegradable Woven Materials

- Coated Fabric Materials

By End-User

- Chemicals and Fertilizers

- Food and Beverage

- Pharmaceuticals

- Construction and Mining

- Agriculture

Regional Analysis

North America

North America accounted for approximately 22.4% of the global FIBC market share in 2025 and is projected to register a CAGR of 5.8% during the forecast period. The regional market is supported by strong demand from food processing, agriculture, chemicals, and construction industries. Increasing focus on industrial automation and warehouse efficiency is encouraging businesses to adopt standardized bulk packaging systems that integrate with automated handling equipment. Sustainability initiatives across the United States and Canada are also contributing to higher adoption of recyclable and reusable FIBC products. Growth in cross-border industrial trade under regional supply chain agreements continues to support packaging demand across manufacturing and agricultural sectors.

The United States remains the dominant country in North America due to its large chemical manufacturing and agricultural export industries. A key growth driver in the country is the rising use of food-grade bulk bags for grain exports and processed food transportation. Agricultural cooperatives and grain storage operators are increasingly replacing traditional rigid containers with lightweight FIBC solutions to reduce storage and logistics costs. In addition, growth in infrastructure rehabilitation projects is increasing demand for cement and mineral transportation packaging. Several packaging suppliers in the country are investing in digital tracking systems and customized printing solutions to improve supply chain efficiency for industrial clients.

Europe

Europe represented nearly 24.7% of the global FIBC market in 2025 and is forecasted to expand at a CAGR of 5.9% through 2034. The region benefits from advanced industrial manufacturing capabilities and strict environmental regulations promoting sustainable packaging practices. Demand for recyclable polypropylene bags and reusable industrial packaging solutions is increasing across Germany, France, Italy, and the United Kingdom. European chemical manufacturers continue to invest in high-performance conductive and anti-static FIBC solutions to comply with workplace safety standards. Rising demand for eco-friendly packaging materials from food and pharmaceutical industries is also contributing to market expansion.

Germany dominates the European market due to its strong industrial base and export-oriented manufacturing sector. One unique growth driver in the country is the increasing adoption of circular economy initiatives in industrial packaging. Packaging companies are collaborating with recycling firms to establish collection systems for used FIBC products and reduce industrial plastic waste. The German food ingredient sector is also investing in traceable packaging systems integrated with barcode and RFID technologies. Growing exports of specialty chemicals and processed food ingredients are expected to sustain long-term demand for premium-quality bulk packaging solutions across the country.

Asia Pacific

Asia Pacific held the largest share of the FIBC market at 39.1% in 2025 and is expected to register a CAGR of 7.0% during the forecast period. Rapid industrialization, rising export activity, and expansion of agricultural production are major factors supporting regional growth. Countries including China, India, Vietnam, and Indonesia are witnessing increasing demand for cost-effective bulk packaging solutions across chemicals, fertilizers, food processing, and construction industries. The growth of e-commerce-enabled industrial procurement platforms is improving product accessibility for small and medium manufacturers. Rising investments in manufacturing infrastructure and logistics modernization are further strengthening regional demand for FIBC products.

China remains the dominant country in Asia Pacific due to its extensive manufacturing and export ecosystem. A major growth driver is the country’s expanding chemical and polymer export industry, which requires high-volume bulk transportation packaging. Chinese packaging manufacturers are investing heavily in automated weaving technology and high-strength polypropylene materials to improve production efficiency and export competitiveness. India is also emerging as a significant production hub due to lower manufacturing costs and rising pharmaceutical exports. The increasing use of FIBC bags for rice, fertilizer, and mineral exports across Asian economies is expected to sustain strong regional growth throughout the forecast period.

Middle East & Africa

The Middle East & Africa accounted for around 7.8% of the global FIBC market in 2025 and is projected to grow at a CAGR of 6.1% through 2034. Industrial diversification strategies and expanding construction activity are creating steady demand for bulk packaging solutions across the region. Oil-producing economies are investing in downstream chemical manufacturing and infrastructure projects, increasing the need for durable industrial packaging systems. Rising mining activities in African countries are also supporting demand for heavy-duty FIBC bags used in mineral transportation. Improvements in logistics infrastructure and port connectivity are enhancing trade efficiency and supporting regional packaging consumption.

Saudi Arabia is the leading market within the region due to rapid growth in petrochemical and construction industries. A unique growth driver is the expansion of industrial cities and export-oriented manufacturing clusters under long-term economic diversification programs. Bulk packaging suppliers are benefiting from increasing demand for resin transportation and industrial powder handling applications. In Africa, South Africa is witnessing rising adoption of bulk bags for mining exports and agricultural processing industries. Growing investment in warehouse infrastructure and industrial storage facilities is expected to create additional opportunities for FIBC manufacturers operating across the region.

Latin America

Latin America represented approximately 6.0% of the global FIBC market in 2025 and is expected to witness the fastest CAGR of 7.1% during the forecast period. Expanding agricultural exports and mining activities are supporting strong demand for bulk packaging products across the region. Countries such as Brazil, Argentina, and Chile are major exporters of grains, fertilizers, minerals, and processed agricultural commodities, all of which require efficient transportation and storage solutions. Rising industrial trade and improving logistics infrastructure are increasing adoption of standardized bulk packaging systems among exporters and commodity producers.

Brazil dominates the regional market due to its large-scale agricultural and mining industries. One important growth driver is the increasing export volume of soybeans, sugar, and fertilizers, which require cost-effective and durable packaging for international shipments. Packaging manufacturers are establishing regional production and distribution facilities to serve agricultural cooperatives and commodity exporters more efficiently. The mining industry in Chile and Peru is also contributing to regional demand for heavy-load FIBC bags designed for mineral handling. Continued investment in export infrastructure and industrial modernization is expected to support long-term market expansion across Latin America.

Competitive Landscape

The FIBC market is moderately fragmented, with global and regional manufacturers competing through product customization, material innovation, pricing strategies, and distribution expansion. Leading companies are increasingly investing in sustainable packaging technologies and automation to improve operational efficiency and reduce manufacturing costs. Product differentiation through conductive fabrics, food-grade certifications, and smart tracking systems has become a key competitive strategy across industrial packaging markets.

Berry Global is recognized as a leading company in the market due to its broad product portfolio, global manufacturing footprint, and strong customer relationships across industrial and agricultural sectors. The company continues to focus on recyclable packaging solutions and advanced woven material technologies. Other major players are strengthening their market position through acquisitions, regional expansion, and investment in high-capacity manufacturing plants.

Several manufacturers are introducing digitally enabled packaging systems integrated with RFID tracking and traceability features to improve supply chain visibility for industrial clients. Companies are also expanding production facilities in Asia Pacific and Latin America to capitalize on rising industrial exports and lower production costs. Strategic partnerships with logistics providers and agricultural cooperatives are further supporting market penetration among bulk commodity exporters.

Key Players List

- Berry Global Inc.

- Greif Inc.

- Conitex Sonoco

- LC Packaging International BV

- Rishi FIBC Solutions

- BAG Corp

- Global-Pak Inc.

- Jumbo Bag Ltd.

- Halsted Corporation

- Intertape Polymer Group

- Emmbi Industries Limited

- Taihua Group

- United Bags Inc.

- Bulk Lift International LLC

- Plastene India Limited