Lightweight Shopping Bags Market Size and Growth

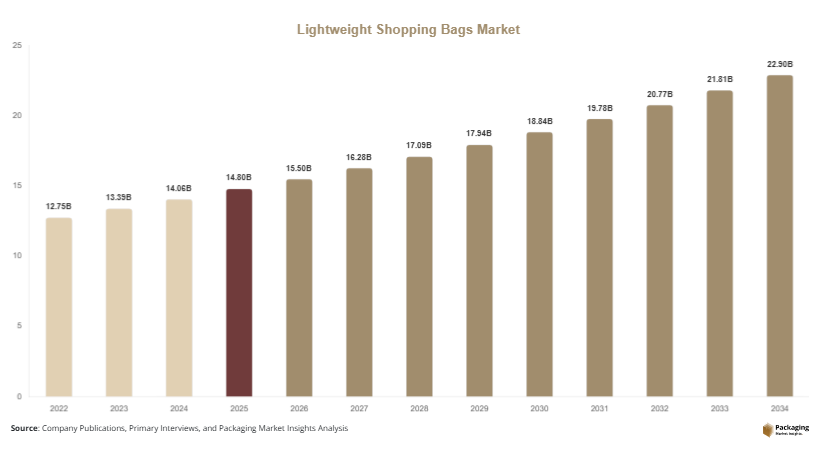

The global lightweight shopping bags market was valued at USD 14.8 billion in 2025 and is projected to reach USD 22.9 billion by 2034, expanding at a CAGR of 5.0% during the forecast period from 2025 to 2034. The market reached an estimated value of USD 15.5 billion in 2026 due to increasing retail activities, growing consumer preference for convenient packaging solutions, and rising adoption of reusable and recyclable shopping bags across supermarkets, grocery chains, fashion stores, and e-commerce delivery platforms. Lightweight shopping bags are widely used because they reduce material consumption, lower transportation costs, and improve handling efficiency for retailers and consumers.

The market is witnessing steady growth as governments and retail companies encourage sustainable alternatives to conventional heavy plastic bags. Many countries are introducing restrictions on single-use plastics, encouraging manufacturers to develop biodegradable, paper-based, woven polypropylene, and reusable lightweight bag solutions. Rapid urbanization and the expansion of organized retail networks are further increasing demand for cost-efficient shopping bags with improved durability and branding capabilities. In addition, the growing influence of environmentally conscious consumers is driving investments in recyclable materials and compostable bag technologies.

Key Highlights

- Asia Pacific dominated the market with a 38.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Plastic lightweight bags led the type segment with a 42.6% share.

- Polyethylene material dominated the market with a 47.8% share.

- Grocery & supermarket applications led the segment with 45.3% share.

- The US remained the dominant country with a market size of USD 2.8 billion in 2025 and USD 2.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Reusable and Recyclable Shopping Bags

Retailers and packaging manufacturers are increasingly focusing on reusable and recyclable lightweight shopping bags as sustainability regulations continue to strengthen worldwide. Governments across Europe, North America, and parts of Asia are imposing taxes and bans on conventional single-use plastic bags, encouraging consumers to switch toward reusable alternatives. Lightweight woven polypropylene bags, recyclable polyethylene bags, and reinforced paper bags are gaining popularity across supermarkets and retail chains. Large retailers are launching branded reusable bag programs to reduce waste generation while improving customer loyalty. For example, grocery chains are increasingly offering recycled-content shopping bags with enhanced durability and lower material thickness. This trend is expected to create long-term demand for eco-friendly bag manufacturing technologies and recycled packaging materials.

Expansion of Lightweight Packaging in E-Commerce Retail

The rapid expansion of e-commerce and quick-commerce delivery services is significantly influencing the lightweight shopping bags market. Online retailers are adopting lightweight flexible packaging solutions to reduce shipping costs and improve handling efficiency during delivery operations. Lightweight shopping bags with enhanced tear resistance and moisture protection are increasingly used for grocery delivery, apparel packaging, and convenience retail distribution. Retailers are integrating printed branding and digital tracking features into shopping bags to improve customer engagement and supply chain visibility. The growth of urban home delivery services in countries such as India, Brazil, and Indonesia is further increasing demand for lightweight packaging formats. Future developments in high-strength recyclable polymers and biodegradable films are expected to support innovation in e-commerce packaging applications.

Market Drivers

Rising Government Restrictions on Conventional Plastic Bags

Government regulations aimed at reducing plastic waste are strongly supporting the growth of the lightweight shopping bags market. Many countries are introducing restrictions on thick plastic packaging and promoting recyclable or biodegradable bag alternatives. Retailers are increasingly replacing traditional plastic bags with lightweight recyclable and reusable formats to comply with environmental regulations. Countries across Europe and Asia are implementing plastic reduction targets that encourage adoption of low-weight sustainable shopping bags. For example, several supermarket chains are transitioning toward thinner recyclable polyethylene bags and compostable materials to meet sustainability commitments. These regulations are encouraging packaging manufacturers to invest in recycled-content materials, biodegradable resins, and low-weight flexible packaging technologies.

Growth of Organized Retail and Supermarket Chains

The expansion of supermarkets, convenience stores, and organized retail chains is driving strong demand for lightweight shopping bags globally. Urban consumers increasingly prefer packaged grocery shopping and modern retail environments, increasing the requirement for cost-efficient and easy-to-carry packaging solutions. Lightweight shopping bags reduce transportation and storage expenses while offering convenient handling for consumers. Retailers are also adopting customized shopping bags with printed branding and promotional messaging to strengthen customer visibility. Emerging economies including India, Vietnam, Indonesia, and Mexico are witnessing rapid retail infrastructure development, contributing to increased consumption of lightweight bags. The growing penetration of discount retail stores and hypermarkets is expected to sustain long-term market demand.

Market Restraint

Volatility in Raw Material Prices and Environmental Concerns

Fluctuating raw material prices remain a major restraint for the lightweight shopping bags market. Polyethylene, polypropylene, recycled paper, and biodegradable polymers are subject to price volatility influenced by crude oil prices, supply chain disruptions, and recycling infrastructure limitations. Rising costs of biodegradable resins and recycled raw materials can increase manufacturing expenses for bag producers, limiting profitability. Environmental concerns regarding plastic waste generation also continue to affect market growth in certain regions. Although lightweight plastic bags reduce material consumption, improper disposal and limited recycling infrastructure create sustainability challenges. Several municipalities are introducing strict regulations against plastic packaging, forcing manufacturers to redesign production processes and invest in alternative materials. Smaller manufacturers may face operational difficulties due to higher compliance and sustainability investment costs.

Market Opportunities

Increasing Demand for Biodegradable Shopping Bags

The growing adoption of biodegradable shopping bags presents significant opportunities for packaging manufacturers. Consumers are increasingly seeking sustainable packaging alternatives that minimize environmental impact while maintaining convenience and durability. Biodegradable lightweight shopping bags made from starch blends, polylactic acid, and bio-based polymers are gaining traction in food retail, supermarkets, and specialty stores. Governments are supporting bio-based packaging adoption through sustainability incentives and plastic reduction initiatives. Retailers are also introducing compostable bag programs to improve environmental branding and meet corporate sustainability targets. Future advancements in bio-based resin technology and industrial composting infrastructure are expected to strengthen long-term market growth opportunities.

Expansion of Printed and Smart Shopping Bags

The integration of branding technologies and smart packaging concepts into lightweight shopping bags is creating new revenue opportunities for manufacturers. Retailers are increasingly using printed shopping bags as low-cost marketing tools to improve customer engagement and enhance brand visibility. QR codes, promotional printing, and digital tracking elements are becoming common in reusable and recyclable shopping bags. Fashion retailers and premium grocery chains are adopting customized lightweight bags to strengthen customer experience and improve product differentiation. Growth in digital printing technologies is enabling cost-efficient short-run production of customized packaging solutions. Future demand for interactive retail packaging and sustainable branding initiatives is expected to support innovation in smart shopping bag manufacturing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.8 Billion |

| Market Size in 2026 | USD 15.5 Billion |

| Market Size in 2034 | USD 22.9 Billion |

| CAGR | 5.0% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

T-shirt bags dominated the lightweight shopping bags market in 2024, accounting for approximately 38.6% of the global market share. Their dominance is primarily linked to widespread adoption across supermarkets, grocery stores, convenience outlets, and fresh produce retailers. These bags offer low manufacturing costs, easy storage, high carrying capacity, and compatibility with automated dispensing systems, making them a practical choice for high-volume retail environments. In developing economies across Asia Pacific and Africa, small retail shops continue to rely heavily on lightweight T-shirt bags because of affordability and operational convenience. Major food retailers and discount chains also prefer this format due to rapid checkout efficiency and reduced packaging expenses. Manufacturers are increasingly incorporating recycled polyethylene and downgauged resin technologies into T-shirt bags to meet sustainability goals while maintaining durability. Retailers are also introducing printed branding and QR-enabled promotional messaging on lightweight T-shirt bags to improve customer engagement. The segment continues to maintain strong market demand despite regulatory pressures, particularly in regions where cost-sensitive retail operations dominate the consumer goods landscape.

Reusable lightweight shopping bags are projected to register the fastest CAGR of 7.4% during the forecast period. Rising environmental awareness, government restrictions on single-use plastics, and increasing consumer preference for sustainable shopping solutions are accelerating adoption of reusable lightweight bags across global retail chains. These bags are manufactured using woven polypropylene, recycled PET, biodegradable polymers, and lightweight fabric blends that provide durability without increasing transportation costs. Retailers across Europe and North America are actively promoting reusable bag loyalty programs to reduce disposable packaging waste and improve brand sustainability positioning. Fashion retailers and premium grocery brands are also investing in aesthetically designed lightweight reusable bags to strengthen customer retention strategies. Advancements in foldable compact bag designs, washable materials, and enhanced printing technologies are further supporting segment expansion. E-commerce grocery delivery services are increasingly utilizing reusable lightweight bags to align with sustainability commitments and reduce secondary packaging waste. As regulatory frameworks become stricter globally, reusable lightweight bags are expected to become a core component of circular retail packaging systems over the next decade.

By Material

Polyethylene dominated the material segment in 2024 with a market share of nearly 46.8%. The material continues to lead due to its lightweight structure, moisture resistance, flexibility, and cost-effectiveness across retail packaging applications. High-density polyethylene and low-density polyethylene are extensively used in grocery bags, convenience store bags, and promotional shopping bags because they provide strong load-bearing capability with minimal material usage. Polyethylene bags also support high-speed production processes, making them suitable for large-scale retail operations. In emerging economies, polyethylene remains widely preferred because of low raw material costs and established manufacturing infrastructure. Packaging manufacturers are increasingly introducing recycled-content polyethylene bags to comply with evolving environmental regulations while maintaining performance standards. Advanced downgauging technologies are also helping manufacturers reduce resin consumption without compromising strength. Major retailers continue to adopt recyclable polyethylene bags integrated with post-consumer recycled materials to improve sustainability metrics. Despite regulatory challenges related to conventional plastics, polyethylene maintains strong market relevance due to affordability, versatility, and continuous innovation in recyclable flexible packaging technologies.

Biodegradable and compostable materials are expected to witness the fastest CAGR of 8.1% through 2034. Increasing government bans on traditional plastic shopping bags and growing consumer preference for environmentally responsible packaging are driving substantial investment in compostable materials such as PLA, starch blends, PBAT, and bio-based polymers. Retailers across Europe, Canada, and parts of Asia Pacific are rapidly transitioning toward biodegradable shopping bags to comply with sustainability regulations and corporate ESG targets. Food retailers and organic grocery chains are particularly active in adopting compostable lightweight shopping bags to strengthen eco-friendly brand positioning. Innovations in bio-based resin formulations are improving tensile strength, moisture resistance, and shelf stability, enabling broader commercial adoption. Manufacturers are also focusing on industrial composting compatibility and certification standards to improve product acceptance among retailers and consumers. As circular economy policies continue to expand globally, biodegradable materials are expected to gain significant market penetration in urban retail and foodservice sectors over the forecast period.

By End-Use

Retail and grocery applications dominated the lightweight shopping bags market in 2024, accounting for approximately 52.4% of total market share. The segment’s leadership is driven by growing global retail activity, expansion of supermarket chains, and increasing consumer demand for convenient carry solutions. Grocery retailers require lightweight bags that are economical, easy to distribute, and capable of carrying diverse products efficiently. Urbanization and rising consumer spending in emerging markets continue to support demand for affordable retail packaging formats. Hypermarkets, convenience stores, discount chains, and wholesale retailers extensively utilize lightweight shopping bags for checkout operations and promotional campaigns. Many retailers are now integrating recycled materials and sustainability labeling into shopping bags to improve environmental performance and strengthen regulatory compliance. Digital printing technologies are also enabling customized branding and seasonal marketing campaigns on lightweight retail bags. In regions such as Asia Pacific and Latin America, expanding organized retail infrastructure continues to create substantial demand for low-cost and high-volume shopping bag solutions across food and consumer goods sectors.

E-commerce and food delivery applications are anticipated to record the fastest CAGR of 7.8% during the forecast period. Rapid growth in online grocery platforms, quick-commerce services, and home delivery operations is creating strong demand for lightweight yet durable shopping bags capable of supporting efficient logistics. Food delivery companies increasingly require lightweight bags that reduce transportation costs while ensuring product safety and convenience. Retailers are also investing in recyclable and reusable bag formats to improve sustainability within last-mile delivery networks. In urban markets, lightweight bags with reinforced handles, thermal protection features, and tamper-evident sealing systems are becoming increasingly common. The expansion of app-based grocery delivery services across Asia Pacific, North America, and Europe is further accelerating segment growth. Manufacturers are introducing innovative lightweight delivery bags with moisture resistance, high print quality, and reusable functionality to support evolving e-commerce packaging requirements. As digital retail ecosystems continue expanding globally, demand for lightweight shopping bags in delivery and fulfillment operations is expected to increase substantially over the next decade.

Lightweight Shopping Bags Market Segmentations

By Type

- T-Shirt Bags

- Die-Cut Handle Bags

- Drawstring Bags

- Wicketed Bags

- Reusable Lightweight Shopping Bags

By Material

- Polyethylene

- Polypropylene

- Biodegradable & Compostable Materials

- Recycled Plastic Materials

- Paper-Based Lightweight Materials

By End-User

- Retail & Grocery

- Foodservice & Takeaway

- E-Commerce & Delivery

- Apparel & Fashion Retail

- Household & General Merchandise

Regional Analysis

North America

North America accounted for 24.7% of the global lightweight shopping bags market share in 2025 and is projected to expand at a CAGR of 4.8% during the forecast period. The region is witnessing increasing demand for recyclable and reusable shopping bags due to rising environmental awareness and government restrictions on conventional plastic packaging. Supermarkets, convenience stores, and retail chains are increasingly adopting lightweight bags made from recyclable polyethylene and paper-based materials. The growth of grocery delivery services and e-commerce retail platforms is also supporting market expansion. Retailers across the United States and Canada are investing in reusable packaging initiatives to improve sustainability compliance and reduce operational packaging costs.

The United States remained the dominant country in North America due to strong organized retail infrastructure and high packaged product consumption. One major growth driver is the increasing adoption of reusable shopping bag programs across grocery and supermarket chains. Several retailers are replacing conventional plastic bags with recycled-content alternatives and low-weight reusable formats. Growth in online grocery delivery and quick-commerce retail services is further increasing demand for lightweight packaging solutions. Rising investments in recycling infrastructure and sustainable packaging innovation are expected to support continued regional market growth.

Europe

Europe represented 22.1% of the global lightweight shopping bags market in 2025 and is anticipated to grow at a CAGR of 5.1% through 2034. The region continues to witness strong demand for biodegradable and paper-based shopping bags due to strict sustainability regulations and consumer preference for eco-friendly packaging. European retailers are rapidly transitioning toward reusable bag programs and recyclable packaging materials. Countries including Germany, France, and Italy are implementing aggressive plastic reduction policies that encourage lightweight sustainable packaging adoption. Retailers are increasingly focusing on compostable and recycled shopping bag materials to improve environmental compliance and reduce landfill waste.

Germany dominated the European market due to its advanced recycling infrastructure and strong retail sector. A key growth factor is the increasing use of reusable shopping bags integrated with sustainable branding initiatives. Retail chains are promoting multi-use shopping bags to reduce packaging waste and improve environmental awareness among consumers. Germany is also investing in recycled polymer processing technologies to strengthen circular packaging systems. Rising demand for sustainable grocery packaging and eco-friendly retail solutions is expected to support regional market expansion during the forecast period.

Asia Pacific

Asia Pacific dominated the lightweight shopping bags market with a 38.9% share in 2025 and is projected to register a CAGR of 5.8% during the forecast period. Rapid urbanization, rising retail infrastructure development, and increasing packaged product consumption are supporting strong market growth across the region. Countries including China, India, Japan, and Indonesia are witnessing increasing demand for lightweight shopping bags across supermarkets, convenience stores, and e-commerce platforms. Manufacturers are expanding production capacity for recyclable and biodegradable bags to address sustainability concerns and regulatory changes. Growth in quick-commerce grocery delivery services is also supporting market expansion.

China emerged as the dominant country in Asia Pacific due to large-scale retail activity and extensive packaging manufacturing capabilities. One major growth driver is the rapid expansion of organized retail chains and food delivery platforms. Chinese retailers are increasingly adopting lightweight recyclable bags to comply with government sustainability targets and reduce packaging costs. India is also witnessing strong growth in reusable bag demand due to increasing plastic restrictions and rising environmental awareness. The region continues to benefit from low manufacturing costs and strong demand for affordable retail packaging solutions.

Middle East & Africa

The Middle East & Africa accounted for 5.4% of the global lightweight shopping bags market share in 2025 and is expected to expand at a CAGR of 4.6% during the forecast period. Increasing urban retail development and rising packaged product demand are contributing to regional market growth. Supermarkets and convenience retail chains are increasingly adopting lightweight shopping bags to improve packaging efficiency and reduce operational costs. Several Gulf countries are implementing sustainability initiatives aimed at reducing plastic waste generation and encouraging reusable packaging adoption. Growing tourism and retail expansion are also supporting packaging demand across the region.

Saudi Arabia remained the dominant country in the Middle East & Africa market due to rising supermarket penetration and growing retail modernization. A major growth driver is the increasing implementation of plastic reduction initiatives across urban retail networks. Retailers are introducing reusable and recyclable shopping bag programs to improve sustainability compliance. The expansion of convenience retail and food delivery services is also contributing to increased demand for lightweight packaging products. Continued investments in sustainable packaging infrastructure are expected to create long-term market opportunities across the region.

Latin America

Latin America held 8.9% of the global lightweight shopping bags market in 2025 and is projected to grow at the fastest CAGR of 6.4% during the forecast period. The region is benefiting from increasing supermarket penetration, expanding urban populations, and rising demand for affordable retail packaging solutions. Countries including Brazil, Mexico, and Argentina are witnessing growth in organized retail networks and packaged food consumption. Retailers are increasingly adopting lightweight recyclable bags to reduce packaging expenses and improve operational efficiency. The expansion of food delivery and e-commerce sectors is also strengthening regional demand.

Brazil dominated the Latin American market due to rapid retail sector growth and increasing consumer awareness regarding sustainable packaging. One unique growth driver is the growing adoption of biodegradable shopping bags in supermarkets and food retail chains. Retailers are introducing reusable packaging programs supported by local sustainability campaigns. Mexico is also witnessing rising demand for lightweight paper-based shopping bags due to evolving packaging regulations. Continued investment in retail infrastructure and recycling programs is expected to support future market expansion across Latin America.

Competitive Landscape

The lightweight shopping bags market is moderately fragmented, with global and regional manufacturers competing through sustainability innovation, material optimization, and large-scale retail partnerships. Leading companies are focusing on recyclable materials, biodegradable polymers, downgauged plastic technologies, and reusable packaging formats to align with evolving regulatory requirements and consumer preferences. Strategic investments in automated production systems and advanced printing technologies are also helping companies improve operational efficiency and product customization capabilities.

Novolex Holdings remains one of the leading players in the market due to its extensive product portfolio, strong distribution network, and aggressive expansion into sustainable retail packaging solutions. The company has increased investments in recycled-content shopping bags and circular economy initiatives to strengthen its position across North America and Europe. Berry Global is another major participant focusing on lightweight recyclable polyethylene solutions and downgauging technologies to reduce raw material consumption. International Plastics Inc. and Inteplast Group continue to expand production capacities to meet rising retail and e-commerce demand across emerging economies.

Companies are increasingly forming partnerships with supermarkets, retail chains, and foodservice operators to develop customized sustainable bag solutions. Several manufacturers are also introducing compostable and reusable shopping bag portfolios in response to tightening environmental regulations globally. Technological advancements in high-strength lightweight films, bio-based materials, and digital printing capabilities are expected to intensify competitive differentiation during the forecast period.

Key Players List

- Novolex Holdings, LLC

- Berry Global Group, Inc.

- Inteplast Group Corporation

- International Plastics Inc.

- Mondi plc

- Smurfit Westrock plc

- BioBag International AS

- Coveris Holdings S.A.

- Ampac Holdings, LLC

- Elif Holding A.Ş.

- Reynolds Consumer Products Inc.

- Polybags Limited

- Thantawan Industry Public Company Limited

- Command Packaging LLC

- Rutan Poly Industries, Inc.

- Dagoplast AS

- Shabra Group

- Sahachit Watana Plastic Industry Co., Ltd.

- Symphony Polymers Pvt. Ltd.

- Eco-Products, Inc.