Bulk Liquid Transport Packaging Market Size and Growth

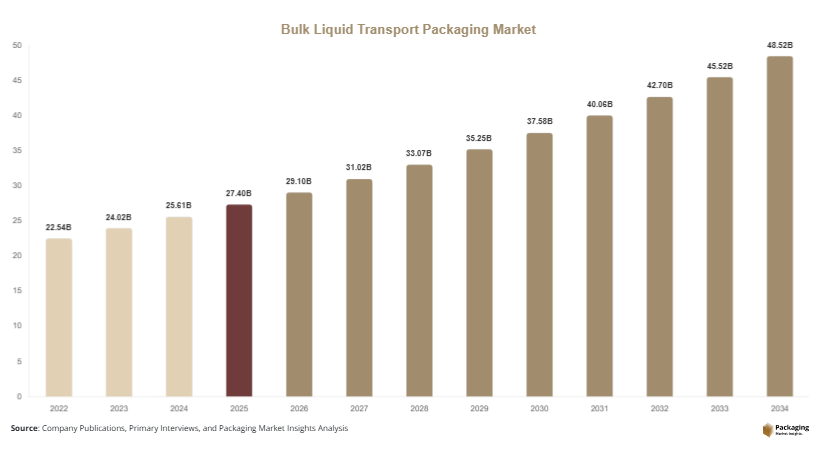

The bulk liquid transport packaging market size was valued at approximately USD 27.4 billion in 2025 and is projected to reach USD 29.1 billion in 2026. Over the forecast period, the market is expected to grow to nearly USD 48.6 billion by 2034, expanding at a CAGR of 6.6% from 2025 to 2034. This growth is supported by rising global trade activities and the need for efficient logistics solutions that ensure product integrity during transportation. The global bulk liquid transport packaging market is witnessing steady expansion due to increasing demand for safe, cost-efficient, and sustainable transportation of liquid goods across industries such as chemicals, food & beverages, pharmaceuticals, and oil & lubricants.

One of the primary growth factors is the increasing international trade of liquid commodities, including edible oils, chemicals, and industrial liquids. Bulk liquid transport packaging solutions such as flexitanks, intermediate bulk containers (IBCs), and drums provide cost-effective and reliable transportation options, enabling businesses to reduce shipping costs and improve operational efficiency. Another important factor is the growing emphasis on sustainability, which is encouraging the adoption of reusable and recyclable packaging materials. Companies are shifting toward eco-friendly packaging solutions to comply with environmental regulations and reduce carbon footprints.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.4%.

- Flexitanks led the type segment with a 34.7% share, while intermediate bulk containers are expected to grow at a CAGR of 7.1%.

- Plastic-based packaging dominated with a 56.8% share, while composite materials are forecasted to grow at a CAGR of 6.9%.

- Chemical applications led the segment with 41.3% share, while food & beverage is expected to grow at a CAGR of 7.3%.

- China remained the dominant country with a market size of USD 6.8 billion in 2025 and USD 7.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Reusable Packaging Solutions

The bulk liquid transport packaging market is witnessing a shift toward sustainable and reusable packaging solutions as companies aim to reduce environmental impact and comply with stringent regulations. Flexitanks and IBCs are increasingly being designed for multiple uses, reducing waste generation and lowering overall packaging costs. Manufacturers are focusing on developing recyclable materials and improving product life cycles to align with global sustainability goals. Additionally, the use of biodegradable liners and eco-friendly coatings is gaining traction. This trend is particularly strong in developed markets, where regulatory pressure and consumer awareness are high, driving the adoption of environmentally responsible packaging solutions.

Rising Demand for Efficient Logistics and Cost Optimization

The growing focus on logistics efficiency and cost reduction is significantly influencing market trends. Bulk liquid transport packaging solutions offer advantages such as higher payload capacity, reduced packaging waste, and lower transportation costs compared to traditional methods. Flexitanks, for example, allow for the transportation of larger volumes of liquid within standard shipping containers, optimizing space utilization. Companies are increasingly adopting these solutions to improve supply chain efficiency and reduce operational expenses. This trend is further supported by the expansion of global trade networks and the need for reliable transportation solutions that ensure product quality and safety.

Market Drivers

Growth in Global Trade of Liquid Commodities

The expansion of global trade in liquid commodities is a major factor driving the bulk liquid transport packaging market. Products such as edible oils, chemicals, and beverages are being transported across long distances, requiring efficient and secure packaging solutions. Bulk liquid packaging systems enable cost-effective transportation by maximizing container capacity and reducing the need for additional packaging materials. As international trade continues to grow, the demand for reliable and scalable packaging solutions is expected to increase, supporting market expansion.

Expansion of Food and Beverage Industry

The rapid growth of the food and beverage industry is another key driver for the market. Increasing consumption of liquid food products such as juices, dairy products, and edible oils is driving demand for hygienic and efficient transport packaging. Bulk liquid packaging solutions help maintain product quality and prevent contamination during transit. Additionally, the rise of processed and packaged food products is further boosting demand. Emerging economies, in particular, are witnessing significant growth in this sector, creating opportunities for packaging manufacturers to expand their offerings.

Market Restraint

Regulatory and Safety Compliance Challenges

The bulk liquid transport packaging market faces challenges related to regulatory compliance and safety standards. Different regions have varying regulations regarding the transportation of liquid goods, particularly hazardous chemicals and pharmaceutical products. Compliance with these regulations requires manufacturers to invest in testing, certification, and quality control processes, increasing operational costs. Additionally, failure to meet safety standards can result in product contamination, environmental damage, and financial losses. For example, leakage or spillage during transportation can lead to significant environmental hazards and legal liabilities. These challenges can hinder market growth, especially for smaller companies with limited resources.

Market Opportunities

Increasing Demand from Emerging Economies

Emerging economies present significant growth opportunities for the bulk liquid transport packaging market. Rapid industrialization and urbanization are driving demand for liquid products such as chemicals, fuels, and food items. Governments in these regions are investing in infrastructure development, including transportation and logistics networks, which supports the adoption of bulk liquid packaging solutions. Additionally, the growing middle-class population is increasing consumption of packaged food and beverages, further boosting demand. Companies that expand their presence in these markets can benefit from rising demand and favorable economic conditions.

Technological Advancements in Packaging Materials

Advancements in packaging materials and design are creating new opportunities for market growth. Innovations such as multi-layer films, high-strength polymers, and smart packaging technologies are enhancing the performance and reliability of bulk liquid transport packaging. These advancements improve durability, reduce contamination risks, and extend product shelf life. Additionally, the development of lightweight materials is helping reduce transportation costs and environmental impact. As manufacturers continue to invest in research and development, the adoption of advanced packaging solutions is expected to increase, driving market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 27.4 Billion |

| Market Size in 2026 | USD 29.1 Billion |

| Market Size in 2034 | USD 48.6 Billion |

| CAGR | 6.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexitanks accounted for the largest share of the market in 2024, contributing approximately 34.7% of total revenue. This dominance is attributed to their cost efficiency and ability to transport large volumes of liquid within standard shipping containers. Flexitanks are widely used for transporting non-hazardous liquids such as edible oils, wine, and industrial liquids. Their lightweight design and ease of installation make them a preferred choice for many industries. Additionally, advancements in flexitank technology, such as multi-layer construction and improved barrier properties, are enhancing their performance and reliability.

Intermediate bulk containers (IBCs) are expected to grow at the fastest CAGR of 7.1% during the forecast period. This growth is driven by their versatility and reusability, making them suitable for a wide range of applications. IBCs are commonly used for transporting hazardous and non-hazardous liquids, offering durability and ease of handling. The increasing focus on sustainability and cost efficiency is driving the adoption of reusable packaging solutions such as IBCs. Additionally, advancements in material design are improving their strength and longevity, supporting segment growth.

By Material

Plastic-based packaging dominated the market in 2024 with a share of approximately 56.8%. This dominance is due to the material’s durability, flexibility, and cost-effectiveness. Plastic packaging solutions such as flexitanks and IBCs provide excellent resistance to corrosion and contamination, making them suitable for transporting a wide range of liquids. The widespread availability of plastic materials and their adaptability to different packaging designs further contribute to their strong market position.

Composite materials are expected to grow at a CAGR of 6.9% during the forecast period. These materials combine the benefits of different components, offering enhanced strength and performance. Composite packaging solutions are increasingly being used for transporting hazardous liquids, as they provide better protection and durability. The growing demand for high-performance packaging solutions is driving the adoption of composite materials. Additionally, advancements in material technology are improving their recyclability, supporting sustainable packaging initiatives.

By Application

The chemical segment accounted for the largest share of the market in 2024, contributing approximately 41.3% of total revenue. This dominance is driven by the extensive use of bulk liquid packaging for transporting chemicals across industries. Packaging solutions such as IBCs and drums provide safe and efficient transportation, reducing the risk of leakage and contamination. The growth of the chemical industry, particularly in emerging economies, is further supporting demand for bulk liquid packaging solutions.

The food and beverage segment is expected to grow at the fastest CAGR of 7.3% during the forecast period. This growth is driven by increasing consumption of liquid food products and the need for hygienic transportation solutions. Bulk liquid packaging solutions help maintain product quality and extend shelf life, making them suitable for food and beverage applications. The expansion of the global food industry and rising demand for packaged food products are expected to drive growth in this segment.

Bulk Liquid Transport Packaging Market Segmentations

By Product Type

- Flexitanks

- Intermediate Bulk Containers (IBCs)

- Drums

By Application

- Chemicals

- Food & Beverage

- Pharmaceuticals

- Oil & Lubricants

By Material

- Plastic

- Metal

- Composite

Regional Analysis

North America

North America accounted for approximately 22.5% of the bulk liquid transport packaging market in 2025 and is expected to grow at a CAGR of 5.9% through 2034. The region benefits from a well-established logistics infrastructure and high demand for efficient packaging solutions. Industries such as chemicals, food and beverages, and pharmaceuticals are major contributors to market growth. Additionally, increasing focus on sustainability is encouraging the adoption of reusable packaging solutions.

The United States dominates the regional market due to its strong industrial base and advanced supply chain systems. A unique growth factor is the increasing adoption of eco-friendly packaging solutions driven by regulatory requirements and corporate sustainability initiatives. This trend is expected to continue supporting market expansion in the region.

Europe

Europe held a market share of around 19.8% in 2025 and is projected to grow at a CAGR of 5.7% during the forecast period. The region’s growth is driven by stringent environmental regulations and the adoption of sustainable packaging solutions. Industries such as food and beverages and chemicals are key contributors to demand.

Germany leads the European market, supported by its strong manufacturing sector and advanced logistics infrastructure. A unique growth factor is the increasing focus on circular economy practices, which encourages the use of reusable and recyclable packaging materials. This trend is driving innovation and adoption of advanced packaging solutions.

Asia Pacific

Asia Pacific dominated the market with a 38.2% share in 2025 and is expected to grow at a CAGR of 7.2% through 2034. The region’s growth is driven by rapid industrialization, increasing trade activities, and expanding food and beverage industry. Countries such as China and India are major contributors to market growth.

China is the dominant country in the region, supported by its large manufacturing base and growing export activities. A unique growth factor is the expansion of industrial production, which increases demand for efficient bulk liquid transport packaging solutions. This trend is expected to strengthen the region’s market position.

Middle East & Africa

The Middle East & Africa region accounted for approximately 8.1% of the market in 2025 and is projected to grow at a CAGR of 6.3% over the forecast period. The region is witnessing increased adoption of bulk liquid packaging solutions due to growing industrial and trade activities.

Saudi Arabia is a key market in this region, driven by its strong oil and chemical industries. A unique growth factor is the increasing export of petrochemical products, which requires reliable and efficient packaging solutions for transportation. This trend is supporting market growth in the region.

Latin America

Latin America held a market share of 10.4% in 2025 and is expected to grow at the fastest CAGR of 7.4% during the forecast period. The region is experiencing growth in industries such as food and beverages and chemicals, driving demand for bulk liquid packaging solutions.

Brazil dominates the regional market due to its expanding industrial base and increasing trade activities. A unique growth factor is the growth of agricultural exports, which require efficient packaging for liquid products such as edible oils and beverages. This trend is expected to drive market expansion in the region.

Competitive Landscape

The bulk liquid transport packaging market is moderately fragmented, with several global and regional players competing based on product innovation, pricing strategies, and distribution networks. Companies are focusing on developing sustainable and cost-effective packaging solutions to meet evolving customer demands. Strategic partnerships and acquisitions are also common as companies aim to expand their market presence and enhance their product portfolios.

Greif, Inc. is a leading player in the market, known for its extensive range of industrial packaging solutions. The company has recently introduced sustainable packaging products aimed at reducing environmental impact. Other major players are also investing in research and development to improve product performance and meet regulatory requirements, contributing to the overall growth of the market.

Key Players List

- Greif, Inc.

- Berry Global Inc.

- Mauser Packaging Solutions

- SCHÜTZ GmbH & Co. KGaA

- Hoover Ferguson Group, Inc.

- Bulk Liquid Solutions Pvt. Ltd.

- Qingdao LAF Packaging Co., Ltd.

- SIA Flexitanks

- Trans Ocean Bulk Logistics Ltd.

- Environmental Packaging Technologies, Inc.

- TPS Rental Systems Ltd.

- Qingdao BLT Packing Industrial Co., Ltd.

- Trust Flexitanks

- KriCon Group BV

- Rishi FIBC Solutions Pvt. Ltd.