Textile Packaging Market Size and Growth

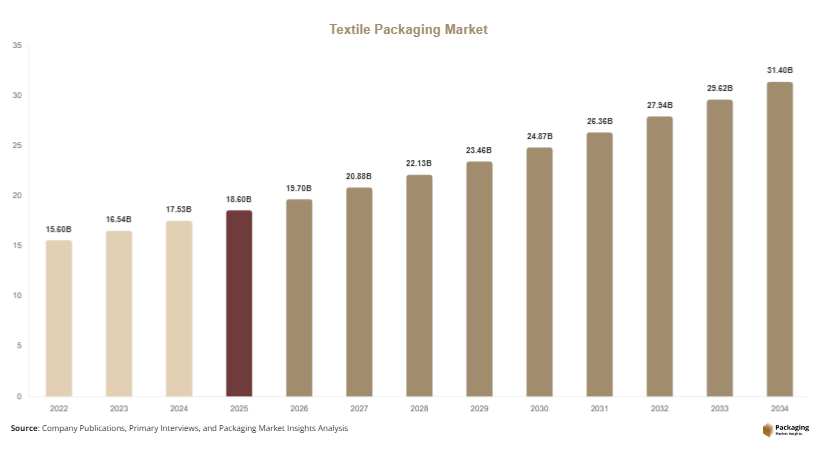

The global textile packaging market was valued at USD 18.6 billion in 2025 and is projected to reach USD 19.7 billion in 2026. The market is expected to attain USD 31.5 billion by 2034, registering a CAGR of 6.0% during the forecast period from 2025 to 2034. Growth is supported by expanding global textile production, rising online apparel sales, and increasing adoption of sustainable packaging solutions.

The textile packaging market is witnessing steady growth as textile manufacturers, apparel brands, retailers, and e-commerce platforms increasingly prioritize product protection, sustainability, and brand presentation. Textile packaging encompasses a broad range of solutions including poly bags, cartons, boxes, pouches, labels, hangers, protective wraps, and reusable packaging formats designed for garments, fabrics, home textiles, technical textiles, and fashion accessories. Packaging plays a critical role in preventing contamination, moisture exposure, wrinkles, and transportation damage while enhancing product appeal throughout the supply chain.

Key Market Highlights

- Asia Pacific dominated the market with a 41.3% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.8%.

- Poly bags led the type segment with a 38.7% share.

- Plastic packaging dominated the material segment with a 48.9% share.

- Apparel packaging applications led the market with a 46.8% share.

- The US remained the dominant country with a market size of USD 2.7 billion in 2025 and USD 2.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Recyclable Textile Packaging

Sustainability has emerged as a major trend in the textile packaging market as fashion brands face increasing pressure to reduce packaging waste and improve environmental performance. Manufacturers are replacing conventional plastic packaging with recyclable paper-based mailers, compostable bags, and reusable packaging solutions. Several apparel brands have committed to reducing single-use plastics throughout their supply chains. For example, global fashion retailers are increasingly shipping garments in recycled-content packaging and biodegradable protective covers. This trend is expected to accelerate as governments introduce stricter regulations on packaging waste and consumers actively seek environmentally responsible brands. Future investments in renewable materials and circular packaging systems are likely to support long-term market growth.

Growth of Smart Packaging and Product Traceability

The adoption of smart packaging technologies is transforming textile packaging operations. RFID tags, QR codes, digital labels, and connected packaging systems are helping brands improve supply chain visibility and product authentication. Apparel manufacturers increasingly use smart labels to track inventory and provide customers with detailed product information. For example, premium fashion brands are implementing QR-enabled packaging that allows consumers to verify authenticity and access sustainability information. Looking ahead, digital packaging technologies are expected to support stronger brand engagement, improved inventory management, and enhanced anti-counterfeiting measures across global textile markets.

Market Drivers

Expansion of Global E-Commerce Apparel Sales

The rapid growth of online fashion retail is a significant driver for the textile packaging market. Consumers increasingly purchase apparel, footwear, and fashion accessories through digital channels, creating substantial demand for protective and lightweight packaging solutions. Packaging is essential for ensuring product quality during shipping and handling. For example, major online apparel retailers use durable mailers and protective packaging systems to reduce product returns and damage rates. As cross-border e-commerce continues to expand and fashion brands strengthen direct-to-consumer business models, packaging demand is expected to increase significantly throughout the forecast period.

Increasing International Trade in Textiles and Garments

Globalization of textile manufacturing and apparel supply chains is supporting packaging demand worldwide. Garments and textile products are frequently transported across multiple countries before reaching consumers, requiring effective packaging solutions that maintain quality and appearance. Protective packaging helps minimize damage caused by moisture, dust, and handling. For example, apparel exporters in Asia rely heavily on protective garment packaging to meet quality requirements in North American and European markets. Continued growth in textile exports and international sourcing activities is expected to support market expansion.

Market Restraint

Volatility in Raw Material Costs and Environmental Compliance Challenges

One of the primary restraints affecting the textile packaging market is the volatility of raw material prices, particularly for plastics, paperboard, and specialty packaging materials. Packaging manufacturers face fluctuating production costs due to changes in energy prices, supply chain disruptions, and global trade conditions. These cost increases can directly impact profit margins and create pricing challenges for textile brands.

Environmental regulations present an additional challenge. Many regions are implementing stricter requirements regarding plastic usage, recyclability, and packaging waste management. Compliance often requires investments in new materials, equipment, and production processes. For example, apparel brands transitioning from conventional poly bags to sustainable alternatives may face higher packaging costs and operational adjustments. While sustainable packaging adoption continues to increase, balancing environmental objectives with cost efficiency remains a significant challenge for industry participants.

Market Opportunities

Development of Reusable Packaging Solutions

Reusable packaging represents a major opportunity for market participants. Fashion retailers and e-commerce companies are increasingly exploring packaging systems that can be returned, reused, or repurposed multiple times. Reusable textile packaging helps reduce waste generation and supports circular economy objectives. For example, several apparel subscription services have introduced reusable shipping bags designed for multiple delivery cycles. Future growth opportunities are expected to emerge as sustainability targets become more ambitious and consumers show greater acceptance of reusable packaging models.

Premium Packaging for Luxury and Designer Brands

The expansion of luxury fashion and designer apparel segments presents significant opportunities for premium textile packaging solutions. High-end brands increasingly invest in rigid boxes, customized inserts, decorative wrapping, and branded packaging experiences. These packaging formats enhance product presentation and reinforce brand value. For example, luxury fashion houses frequently use premium packaging materials that complement product exclusivity. As premium fashion consumption rises globally, packaging suppliers are expected to benefit from increasing demand for customized and aesthetically sophisticated packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.7 Billion |

| Market Size in 2034 | USD 31.5 Billion |

| CAGR | 6.0% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Poly bags dominated the textile packaging market in 2024, accounting for approximately 38.7% of total revenue. These packaging solutions remain widely used due to their affordability, flexibility, lightweight characteristics, and protective capabilities. Poly bags are commonly utilized for packaging garments, fabrics, home textiles, and accessories during transportation and storage. They help prevent moisture exposure, dust accumulation, and product contamination while supporting efficient logistics operations. Industry examples include apparel exporters that package garments individually in protective poly bags before shipment to retailers. The segment also benefits from widespread compatibility with automated packaging systems and global textile supply chains. Continuous improvements in recyclable poly bag materials further support segment leadership.

Reusable textile packaging is projected to be the fastest-growing subsegment, expanding at a CAGR of 7.4% through 2034. Growth is driven by increasing sustainability commitments among fashion brands and e-commerce companies. Reusable packaging solutions help reduce waste generation and improve environmental performance while supporting circular economy initiatives. Packaging manufacturers are introducing durable mailers, reusable garment bags, and returnable packaging systems designed for multiple usage cycles. Future demand is expected to increase as brands pursue packaging reduction targets and consumers demonstrate stronger interest in sustainable purchasing practices.

By Material

Plastic packaging held the largest market share of approximately 48.9% in 2024. Plastic materials remain widely used because of their strength, moisture resistance, transparency, and cost efficiency. Applications include garment bags, shrink wraps, mailers, and protective packaging formats. Textile manufacturers and retailers continue utilizing plastic packaging due to its ability to maintain product quality throughout transportation and storage processes. Industry examples include export-oriented garment manufacturers that rely on plastic packaging to protect products from environmental exposure during international shipping. Advances in recyclable plastics and recycled-content materials are helping improve sustainability performance within the segment.

Paper-based packaging is anticipated to be the fastest-growing material segment, registering a CAGR of 7.1% during the forecast period. Growth is supported by increasing regulatory pressure to reduce plastic waste and rising consumer demand for sustainable packaging alternatives. Packaging companies are developing paper mailers, kraft boxes, and recyclable wrapping materials tailored to textile applications. Future opportunities are expected to emerge from innovations that enhance durability and moisture resistance. As apparel brands continue transitioning toward environmentally responsible packaging, adoption of paper-based materials is likely to accelerate significantly.

By End-Use

Apparel packaging accounted for the largest market share of approximately 46.8% in 2024. The segment benefits from the large volume of garments produced and distributed worldwide each year. Packaging solutions are essential for protecting apparel products from wrinkles, dust, moisture, and handling damage. Industry examples include fashion retailers utilizing branded packaging to improve customer experience and strengthen brand recognition. Growth in online apparel sales further supports demand for protective packaging solutions. Consistent global demand for clothing products ensures continued leadership of the apparel packaging segment within the overall market.

Luxury fashion packaging is expected to register the fastest CAGR of 7.6% through 2034. Growth is fueled by increasing consumer spending on premium apparel, designer accessories, and luxury fashion products. High-end brands continue investing in sophisticated packaging formats that emphasize exclusivity and customer experience. Packaging innovations include rigid boxes, magnetic closures, decorative finishes, and sustainable premium materials. Future demand is expected to benefit from luxury market expansion, digital luxury retail growth, and rising consumer expectations regarding product presentation. These factors collectively support strong growth prospects for luxury fashion packaging.

Textile Packaging Market Segmentations

By Type

- Poly Bags

- Boxes & Cartons

- Pouches

- Hanger Packaging

- Reusable Textile Packaging

By Material

- Plastic

- Paper & Paperboard

- Fabric-Based Packaging

- Biodegradable Materials

- Composite Materials

By End-User

- Apparel Packaging

- Home Textile Packaging

- Technical Textile Packaging

- Fashion Accessories Packaging

- Luxury Fashion Packaging

Regional Analysis

North America

North America accounted for approximately 24.6% of the global textile packaging market share in 2025 and is projected to expand at a CAGR of 5.5% through 2034. The region benefits from strong apparel consumption, advanced e-commerce infrastructure, and increasing demand for sustainable packaging solutions. Retailers continue investing in packaging innovations that improve shipping efficiency and reduce environmental impact. The growth of direct-to-consumer fashion brands is also creating demand for customized packaging formats. Increasing consumer awareness regarding sustainable packaging practices further supports market development across the region.

The United States dominates the North American market. A unique growth driver is the rapid expansion of online fashion subscription services and direct-to-consumer apparel platforms. These business models rely heavily on efficient packaging systems capable of enhancing customer experience while protecting products. Many apparel brands are also implementing recyclable mailers and reusable packaging programs, creating additional opportunities for packaging suppliers.

Europe

Europe represented approximately 22.8% of the global market in 2025 and is forecast to grow at a CAGR of 5.8% through 2034. The region benefits from strong sustainability regulations, advanced packaging technologies, and a well-established fashion industry. Packaging manufacturers are increasingly developing recyclable and renewable packaging materials to comply with circular economy objectives. Demand for sustainable textile packaging continues to rise among apparel brands seeking to reduce environmental impact and strengthen corporate sustainability commitments.

Germany remains the dominant country within Europe. A unique growth driver is the increasing demand for eco-certified apparel and sustainable fashion products. Retailers are adopting recyclable packaging materials and minimizing excess packaging to align with consumer expectations. Several leading European apparel brands have introduced packaging reduction initiatives, encouraging innovation throughout the textile packaging value chain.

Asia Pacific

Asia Pacific dominated the textile packaging market with a 41.3% share in 2025 and is expected to register a CAGR of 6.4% through 2034. The region serves as a major global hub for textile manufacturing, garment production, and apparel exports. Rising disposable incomes, growing fashion consumption, and expanding retail infrastructure are supporting packaging demand. Packaging suppliers continue investing in production capacity and innovative materials to meet the needs of textile manufacturers operating throughout the region.

China remains the dominant country in Asia Pacific. A unique growth driver is the country's extensive apparel export industry. Chinese manufacturers ship large volumes of garments and textile products worldwide, creating substantial demand for protective packaging solutions. Increasing adoption of automation and digital supply chain technologies is also driving demand for smart packaging systems within the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.7% of market revenue in 2025 and is projected to grow at a CAGR of 6.0% through 2034. Growth is supported by expanding retail infrastructure, rising fashion consumption, and increasing textile imports. The region is witnessing gradual adoption of premium packaging solutions as international apparel brands strengthen market presence. Packaging manufacturers are focusing on cost-effective and durable solutions suited to regional logistics conditions.

United Arab Emirates remains the dominant country in the region. A unique growth driver is the rapid expansion of luxury retail and premium fashion outlets. High-end brands emphasize premium packaging experiences that align with customer expectations. This trend is creating opportunities for suppliers specializing in decorative and customized textile packaging solutions.

Latin America

Latin America represented approximately 6.6% of the global textile packaging market in 2025 and is expected to grow at the fastest CAGR of 6.8% through 2034. Growing urbanization, expanding apparel manufacturing activities, and increasing e-commerce adoption are supporting regional market growth. Retail modernization and rising consumer spending on fashion products continue to create demand for innovative packaging solutions. Packaging suppliers are also introducing sustainable alternatives to address changing environmental priorities.

Brazil remains the dominant country in Latin America. A unique growth driver is the expansion of domestic fashion brands and regional textile production. Manufacturers increasingly require protective packaging capable of supporting nationwide distribution and export activities. The adoption of customized packaging solutions among apparel companies is expected to strengthen future market opportunities.

Competitive Landscape

The textile packaging market is moderately fragmented, with manufacturers competing through sustainability initiatives, product innovation, customization capabilities, and geographic expansion strategies. Market participants are increasingly focusing on recyclable materials, reusable packaging formats, and digital printing technologies to strengthen competitive positions.

Amcor plc remains one of the leading participants in the market due to its extensive packaging portfolio, global manufacturing network, and strong focus on sustainable packaging innovation. The company recently expanded its recyclable flexible packaging offerings for apparel and textile applications, supporting customer sustainability goals.

Other major players include Mondi Group, DS Smith Plc, Berry Global Group, Inc., and Sonoco Products Company. These companies continue investing in lightweight materials, digital packaging solutions, and advanced printing technologies. Strategic partnerships with apparel brands and e-commerce retailers are becoming increasingly important as demand for customized packaging continues to grow.

Industry participants are also exploring smart packaging technologies, RFID integration, and reusable packaging systems to enhance product functionality and supply chain efficiency. Competition is expected to intensify as sustainability and e-commerce trends continue shaping the future of textile packaging.

Key Players List

- Amcor plc

- Mondi Group

- DS Smith Plc

- Berry Global Group, Inc.

- Sonoco Products Company

- Smurfit Westrock

- International Paper Company

- Huhtamaki Oyj

- Sealed Air Corporation

- Coveris Holdings S.A.

- Stora Enso Oyj

- Graphic Packaging International LLC

- ProAmpac LLC

- UFlex Limited

- Constantia Flexibles Group GmbH

- WestRock Company

- Novolex Holdings LLC