Vials Packaging Market Size and Growth

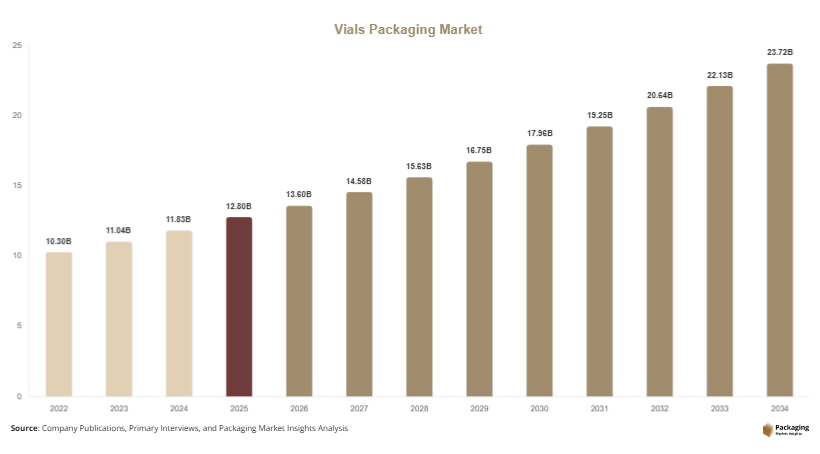

The global vials packaging market size is estimated at USD 12.8 billion in 2025 and is projected to reach USD 13.6 billion in 2026. By 2034, the market is forecast to attain approximately USD 23.7 billion, registering a CAGR of 7.2% during the forecast period (2025–2034). Growth is primarily supported by increasing demand for injectable therapies, expanding vaccine manufacturing capacity, and the rising prevalence of chronic diseases requiring biologic treatments.

The vials packaging market is experiencing steady expansion due to rising pharmaceutical production, increasing biologics manufacturing, and growing demand for secure packaging solutions for injectable drugs and diagnostic products. Vials are essential primary packaging components used to store vaccines, biologics, injectable medicines, laboratory reagents, and specialty healthcare products. The market continues to evolve with advancements in sterile packaging technologies, regulatory compliance requirements, and increasing investments in healthcare infrastructure worldwide.

Key Highlights

- Asia Pacific dominated the market with a 36.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.7%.

- Sterile vials led the type segment with a 44.5% share.

- Glass vials dominated the material segment with a 71.4% share.

- Pharmaceutical applications led the end-use segment with a 67.9% share.

- The US remained the dominant country with a market size of USD 2.6 billion in 2025 and USD 2.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Ready-to-Use Sterile Vials

The pharmaceutical industry is increasingly adopting ready-to-use sterile vials to improve operational efficiency and reduce contamination risks during manufacturing. These vials arrive pre-sterilized and prepared for filling operations, eliminating several processing steps within pharmaceutical facilities. As a result, manufacturers can reduce production time, lower operational costs, and improve compliance with regulatory standards. For example, vaccine manufacturers increasingly utilize ready-to-use vial systems to accelerate production schedules and maintain sterility requirements. The trend is expected to expand further as biologics production grows globally. Future developments may include enhanced sterile barrier technologies, automated filling compatibility, and advanced surface treatments designed to improve drug stability and manufacturing efficiency.

Growing Utilization of Advanced Polymer-Based Vials

Advanced polymer vial technologies are gaining attention as alternatives to traditional glass packaging. Materials such as cyclic olefin polymer (COP) and cyclic olefin copolymer (COC) offer excellent chemical resistance, reduced breakage risk, and improved dimensional consistency. Pharmaceutical companies are increasingly exploring polymer vials for sensitive biologics and specialty injectable products. For example, several biotechnology firms have adopted polymer vial systems for high-value therapies that require enhanced protection against particulate contamination. As manufacturing technologies improve, polymer-based packaging is expected to become more widely adopted across pharmaceutical and biotechnology sectors. Future growth will likely be supported by material innovations that enhance barrier properties and regulatory acceptance.

Market Drivers

Rising Demand for Injectable Drugs and Biologics

The increasing use of injectable medications is a major driver of the vials packaging market. Biologic therapies, vaccines, monoclonal antibodies, and specialty pharmaceutical products often require sterile vial packaging to maintain safety and efficacy. As chronic diseases become more prevalent, healthcare providers are increasingly relying on injectable treatments to manage complex medical conditions. This trend directly increases demand for pharmaceutical-grade vial packaging. For example, oncology therapies and autoimmune disease treatments frequently require sterile glass vials due to their stability and compatibility requirements. As pharmaceutical pipelines continue to expand, manufacturers are expected to increase production capacity, further driving demand for vial packaging solutions.

Expansion of Global Vaccine Manufacturing Capacity

Governments and healthcare organizations are investing heavily in vaccine manufacturing infrastructure to strengthen public health preparedness. Vaccine production requires large volumes of sterile vials capable of maintaining product quality throughout storage and distribution. Pharmaceutical companies continue to expand production facilities and establish regional manufacturing hubs to improve supply chain resilience. For instance, vaccine manufacturers in North America, Europe, and Asia are increasing investments in packaging systems designed for large-scale immunization programs. This expansion of vaccine manufacturing capacity directly supports growth in the vial packaging industry and creates long-term demand for specialized pharmaceutical packaging products.

Market Restraint

Stringent Regulatory Requirements and Manufacturing Complexity

One of the major restraints affecting the vials packaging market is the strict regulatory framework governing pharmaceutical packaging. Vials must meet rigorous standards related to sterility, material compatibility, dimensional accuracy, and product safety. Compliance requires significant investments in quality assurance systems, validation processes, and specialized manufacturing equipment. For example, pharmaceutical-grade glass vial production requires extensive testing to ensure resistance to chemical interactions and particulate contamination. Failure to meet regulatory requirements can result in costly recalls, production delays, and reputational damage. Small manufacturers may face challenges in maintaining compliance due to limited financial resources. These regulatory complexities can increase production costs and create barriers to market entry despite strong demand growth.

Market Opportunities

Growth of Biopharmaceutical Manufacturing Facilities

The expansion of biopharmaceutical manufacturing facilities presents significant opportunities for vial packaging suppliers. Increasing investments in biologics, biosimilars, gene therapies, and cell-based treatments are creating demand for specialized packaging solutions. These therapies often require highly controlled storage conditions and advanced packaging materials to maintain stability. Pharmaceutical manufacturers are establishing new production facilities across North America, Europe, and Asia to support growing demand. Vial packaging suppliers can capitalize on this trend by developing products specifically designed for sensitive biologic formulations. Future opportunities may include customized vial systems, advanced coatings, and integrated traceability features.

Emerging Demand for Smart Pharmaceutical Packaging

Smart packaging technologies are creating new opportunities within the vial packaging industry. Pharmaceutical companies increasingly seek packaging solutions that improve product traceability, anti-counterfeiting protection, and supply chain visibility. Technologies such as RFID tags, QR codes, and temperature-monitoring indicators are being incorporated into vial packaging systems. For example, specialty biologics manufacturers are implementing digital tracking solutions to monitor product conditions during transportation. As healthcare supply chains become more complex, demand for intelligent packaging systems is expected to increase. This trend offers substantial growth opportunities for manufacturers capable of integrating digital technologies into pharmaceutical packaging products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.8 Billion |

| Market Size in 2026 | USD 13.6 Billion |

| Market Size in 2034 | USD 23.7 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Sterile vials dominated the market in 2024, accounting for approximately 44.5% of total revenue share. Their leadership position is supported by widespread use across pharmaceutical manufacturing, vaccine production, and injectable drug packaging applications. Sterile vials help reduce contamination risks and comply with stringent pharmaceutical regulations. Manufacturers increasingly prefer sterile vial formats because they improve operational efficiency and reduce processing requirements. For example, vaccine producers and contract manufacturing organizations rely heavily on sterile vial systems to accelerate production timelines while maintaining product safety. The segment also benefits from rising demand for biologics and injectable therapies that require highly controlled packaging environments. Continued expansion of pharmaceutical manufacturing capacity is expected to support the dominance of sterile vials throughout the forecast period.

Ready-to-use vials are projected to be the fastest-growing segment, registering a CAGR of 8.2% through 2034. Growth is driven by increasing adoption of automated filling systems and demand for operational efficiency. These vials reduce sterilization and preparation requirements, enabling pharmaceutical companies to streamline manufacturing processes. Packaging suppliers are introducing advanced ready-to-use formats with improved sterility assurance and compatibility with high-speed production lines. Future demand is expected to increase as biologics production expands and pharmaceutical companies seek solutions that minimize contamination risks while improving production flexibility.

By Material

Glass vials dominated the material segment in 2024, capturing approximately 71.4% market share. Glass remains the preferred packaging material due to its chemical stability, transparency, and compatibility with a wide range of pharmaceutical formulations. Pharmaceutical companies rely on borosilicate glass vials for vaccines, biologics, and injectable drugs because of their proven performance and regulatory acceptance. For example, most global vaccine distribution programs utilize glass vials due to their reliability and ability to preserve product quality. The segment continues to benefit from established manufacturing infrastructure and widespread regulatory approval across global healthcare markets.

Cyclic olefin polymer (COP) vials are expected to grow at the fastest CAGR of 8.5% during the forecast period. These materials offer advantages such as lower breakage risk, improved dimensional consistency, and reduced particulate contamination. Biotechnology companies increasingly utilize polymer vials for sensitive therapies requiring specialized packaging conditions. Ongoing material innovations are enhancing barrier properties and regulatory acceptance. Future growth is expected to be driven by increasing biologics production and growing demand for advanced packaging solutions that improve product safety and handling efficiency.

By End-Use

Pharmaceutical applications dominated the market in 2024 with approximately 67.9% of total market share. Rising production of vaccines, injectable medicines, and specialty pharmaceuticals continues to support strong demand for vial packaging. Pharmaceutical manufacturers require packaging solutions that ensure sterility, regulatory compliance, and product stability throughout the supply chain. For example, hospitals and healthcare providers rely on vial-packaged injectable medicines for a wide range of therapeutic applications. The segment's leadership position is reinforced by increasing healthcare expenditure and growing pharmaceutical manufacturing activities worldwide.

Biotechnology applications are projected to be the fastest-growing segment, expanding at a CAGR of 8.0% through 2034. Growth is supported by rising investments in biologics, cell therapies, gene therapies, and biosimilars. Biotechnology products often require specialized packaging solutions capable of maintaining product integrity under highly controlled conditions. Packaging manufacturers are developing innovative vial designs and advanced materials tailored to biotechnology applications. Continued growth in research and development activities is expected to create substantial opportunities for vial packaging suppliers throughout the forecast period.

Vials Packaging Market Segmentations

By Type

- Sterile Vials

- Ready-to-Use Vials

- Standard Vials

- Specialty Vials

By Material

- Glass Vials

- Plastic Vials

- Cyclic Olefin Polymer (COP) Vials

By End-User

- Pharmaceuticals

- Biotechnology

- Diagnostics

- Research Laboratories

Regional Analysis

North America

North America accounted for approximately 30.1% of the global vials packaging market share in 2025 and is expected to expand at a CAGR of 6.8% through 2034. The region benefits from a strong pharmaceutical manufacturing base, advanced healthcare infrastructure, and significant investments in biotechnology research. Demand for sterile vial packaging remains high due to increasing production of biologics, vaccines, and specialty pharmaceuticals. The presence of major pharmaceutical companies and contract manufacturing organizations further supports market growth. In addition, regulatory emphasis on drug safety and packaging quality continues to drive investments in advanced vial manufacturing technologies.

The United States dominates the North American market. A unique growth driver is the country's leadership in biologics and specialty drug development. Pharmaceutical companies continue to expand production capacity for injectable therapies, creating sustained demand for high-performance vial packaging. For example, multiple biologics manufacturing facilities have increased adoption of ready-to-use sterile vials to improve production efficiency. The combination of innovation, strong healthcare spending, and pharmaceutical research activity continues to strengthen the U.S. position in the market.

Europe

Europe represented approximately 25.4% of the global market share in 2025 and is projected to grow at a CAGR of 6.9% during the forecast period. The region benefits from established pharmaceutical manufacturing clusters, strong regulatory frameworks, and increasing demand for injectable therapies. Investments in biologics production and vaccine development continue to support market growth. Pharmaceutical companies across Europe are increasingly adopting advanced packaging technologies to meet evolving regulatory standards and improve product safety. In addition, growing exports of pharmaceutical products are driving demand for reliable vial packaging solutions.

Germany remains the dominant country within Europe. A unique growth factor is the country's advanced pharmaceutical engineering and production capabilities. German manufacturers are investing in automated vial production technologies that improve precision and scalability. For example, several pharmaceutical packaging facilities have implemented advanced inspection systems to ensure product quality and regulatory compliance. These developments continue to support Germany's leadership position within the regional market.

Asia Pacific

Asia Pacific dominated the global vials packaging market with a 36.8% share in 2025 and is forecast to register a CAGR of 7.8% through 2034. Rapid expansion of pharmaceutical manufacturing, increasing healthcare expenditure, and growing biotechnology investments are driving market growth. Countries across the region are strengthening domestic drug production capabilities and expanding vaccine manufacturing infrastructure. The region also benefits from rising demand for affordable healthcare solutions and increasing pharmaceutical exports. Investments in packaging modernization and sterile manufacturing technologies continue to support market development.

China is the dominant country within Asia Pacific. A unique growth driver is the rapid expansion of domestic pharmaceutical production aimed at meeting growing healthcare demand. Chinese pharmaceutical companies are increasing investments in sterile injectable medicines and biologic therapies, creating strong demand for vial packaging products. For example, vaccine and biosimilar manufacturers are expanding production facilities that require large-scale vial procurement. These developments continue to support robust market growth throughout the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.8% of global market share in 2025 and is expected to grow at a CAGR of 6.7% through 2034. Increasing healthcare investments, expanding pharmaceutical imports, and government initiatives aimed at improving healthcare access are supporting market growth. Demand for injectable medications and vaccines continues to increase across the region. Pharmaceutical distributors and healthcare providers are seeking reliable packaging solutions that ensure product integrity during storage and transportation. Local manufacturing initiatives are also contributing to gradual market expansion.

The Saudi Arabia market leads the region. A unique growth factor is the country's investment in pharmaceutical localization programs designed to reduce dependence on imports. Pharmaceutical manufacturers are establishing domestic production facilities that require high-quality vial packaging solutions. For example, government-supported healthcare projects are increasing demand for injectable medicines and related packaging products. These initiatives continue to strengthen market opportunities within the country.

Latin America

Latin America held approximately 3.9% of the global market share in 2025 and is projected to register the fastest CAGR of 7.7% during the forecast period. The region is benefiting from rising pharmaceutical production, increasing healthcare expenditure, and improving access to advanced medical treatments. Demand for injectable therapies and vaccines continues to grow across key markets. Pharmaceutical manufacturers are investing in local production facilities to improve supply chain efficiency and reduce import dependency. These developments are creating new opportunities for vial packaging suppliers.

Brazil remains the dominant country in Latin America. A unique growth driver is the expansion of public healthcare programs focused on vaccine accessibility and chronic disease treatment. Pharmaceutical manufacturers are increasing production of injectable products to support national healthcare initiatives. For example, vaccine distribution programs have significantly increased demand for sterile vial packaging. Continued investments in healthcare infrastructure and pharmaceutical manufacturing are expected to support long-term market growth.

Competitive Landscape

The vials packaging market is moderately consolidated, with major manufacturers focusing on pharmaceutical-grade quality, production scalability, material innovation, and regulatory compliance. SCHOTT AG remains the leading market participant due to its extensive portfolio of pharmaceutical glass packaging products and strong global manufacturing network. The company recently expanded pharmaceutical vial production capacity to support growing demand for biologics and injectable medicines.

Other major market participants include Gerresheimer AG, SGD Pharma, Stevanato Group, and Corning Incorporated. These companies are investing in advanced glass technologies, polymer vial innovations, and ready-to-use sterile packaging solutions. Strategic collaborations with pharmaceutical manufacturers and expansion of production facilities remain key competitive strategies.

Manufacturers are also focusing on sustainability initiatives, digital traceability technologies, and enhanced quality assurance systems. Continued investment in research and development is expected to support product innovation and strengthen competitive positioning across global markets.

Key Players List

- SCHOTT AG

- Gerresheimer AG

- SGD Pharma

- Stevanato Group

- Corning Incorporated

- Nipro Corporation

- DWK Life Sciences

- West Pharmaceutical Services Inc.

- Bormioli Pharma S.p.A.

- Piramal Glass Private Limited

- Stolzle Glass Group

- APG Pharma

- Pacific Vial Manufacturing Inc.

- Adelphi Healthcare Packaging

- Shandong Pharmaceutical Glass Co., Ltd.