Health Hygiene Packaging Market Size and Growth

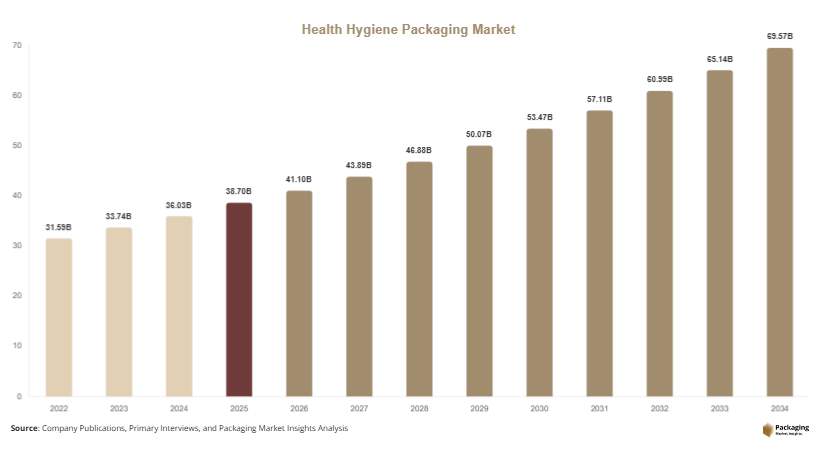

The global health hygiene packaging market size was valued at USD 38.7 billion in 2025 and is projected to reach USD 41.1 billion in 2026. The market is expected to attain approximately USD 69.8 billion by 2034, expanding at a CAGR of 6.8% during the forecast period (2025–2034). The increasing consumption of hygiene products, rising healthcare spending, and growing urban populations are contributing significantly to market expansion.

One of the primary growth factors is the rising demand for feminine hygiene and baby care products across emerging economies. Increasing disposable income and greater awareness regarding personal hygiene are encouraging product adoption and consequently driving packaging demand. Another important growth factor is the rapid expansion of healthcare facilities and medical supply chains that require secure and sterile packaging formats. Additionally, sustainability initiatives are encouraging manufacturers to develop recyclable, biodegradable, and lightweight packaging solutions without compromising product protection.

Key Market Insights

- Asia Pacific dominated the market with a 39.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.4%.

- Flexible packaging led the type segment with a 48.9% share.

- Plastic-based packaging dominated the material segment with a 56.8% share.

- Personal hygiene products led the end-use segment with a 44.7% share.

- The US remained the dominant country with a market size of USD 7.1 billion in 2025 and USD 7.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Hygiene Packaging Solutions

Sustainability has become a major trend within the health hygiene packaging market as manufacturers seek alternatives to conventional plastic packaging. Consumers, regulators, and retailers are increasingly demanding environmentally responsible packaging formats for products such as baby diapers, sanitary products, and personal care wipes. Packaging companies are introducing recyclable films, bio-based polymers, compostable pouches, and paper-based packaging structures. For example, several hygiene product manufacturers have launched diaper packaging utilizing recycled content and reduced plastic usage. The future impact of this trend is expected to be substantial as sustainability regulations become stricter and consumers prioritize environmentally conscious brands. Investments in renewable materials and circular economy initiatives will continue to influence product development strategies.

Integration of Smart and Antimicrobial Packaging Technologies

Another important trend is the increasing integration of smart packaging and antimicrobial technologies into hygiene packaging applications. Packaging manufacturers are developing solutions that enhance product safety, improve traceability, and provide consumers with additional information regarding product authenticity and usage. For example, antimicrobial packaging materials are increasingly being utilized for medical disposables and healthcare products to minimize contamination risks. QR-enabled packaging solutions are also gaining popularity for product tracking and consumer engagement. Looking ahead, advancements in smart sensors, digital labeling, and antimicrobial coatings are expected to expand across healthcare and hygiene applications, improving safety standards and operational efficiency throughout supply chains.

Market Drivers

Rising Demand for Personal Hygiene Products

Growing awareness regarding health, cleanliness, and personal care is significantly driving demand for hygiene products worldwide. Increased consumption of sanitary napkins, baby diapers, wet wipes, tissues, and adult incontinence products directly increases packaging requirements. Urbanization, changing lifestyles, and government awareness campaigns are encouraging greater adoption of personal hygiene products in emerging markets. For example, several countries in Asia and Africa have implemented initiatives promoting feminine hygiene awareness, resulting in higher product penetration rates. As demand for hygiene products continues to increase across various demographics, packaging manufacturers are expected to benefit from sustained market growth.

Expansion of Healthcare Infrastructure and Medical Supply Chains

The expansion of healthcare systems and medical product distribution networks is another major driver of the health hygiene packaging market. Hospitals, clinics, diagnostic centers, and pharmaceutical facilities require secure packaging for disposable medical products and hygiene-related healthcare items. Packaging solutions help maintain sterility, protect products from contamination, and ensure regulatory compliance. For instance, demand for individually wrapped medical disposables has increased significantly across developed and emerging healthcare markets. As governments continue investing in healthcare infrastructure and access to medical products improves globally, demand for advanced health hygiene packaging solutions is expected to grow steadily.

Market Restraint

Volatility in Raw Material Prices and Sustainability Compliance Costs

A major restraint affecting the health hygiene packaging market is the fluctuation in raw material prices and the increasing costs associated with sustainability compliance. Packaging manufacturers rely heavily on materials such as polyethylene, polypropylene, specialty films, paperboard, and bio-based polymers. Price volatility can significantly impact production costs and profit margins. Additionally, transitioning toward sustainable packaging solutions often requires investments in new manufacturing technologies, material testing, and regulatory compliance. For example, replacing conventional plastic packaging with biodegradable alternatives may increase production expenses. These challenges are particularly significant for small and medium-sized manufacturers operating in highly competitive markets. Although sustainable packaging demand continues to rise, cost pressures may slow adoption in certain regions and applications.

Market Opportunities

Expansion of Biodegradable and Recyclable Packaging Materials

The increasing emphasis on sustainability presents substantial opportunities for biodegradable and recyclable hygiene packaging solutions. Manufacturers are actively developing materials that reduce environmental impact while maintaining product protection and functionality. Applications include biodegradable diaper packaging, recyclable sanitary product wrappers, and paper-based personal care packaging. Consumer demand for environmentally friendly products is encouraging brands to differentiate themselves through sustainable packaging initiatives. Future developments in compostable films and advanced recycling technologies are expected to accelerate adoption across multiple product categories.

Growth of E-Commerce Distribution for Hygiene Products

The rapid growth of online retail channels presents a significant opportunity for packaging manufacturers serving the hygiene sector. Consumers increasingly purchase personal care and healthcare products through digital platforms, requiring packaging that protects products during transportation while maintaining brand visibility. E-commerce packaging solutions must provide durability, tamper evidence, and efficient logistics performance. For example, diaper and sanitary product brands are introducing optimized packaging formats designed specifically for direct-to-consumer distribution. As online shopping penetration continues to increase globally, demand for specialized health hygiene packaging solutions is expected to expand considerably.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.7 Billion |

| Market Size in 2026 | USD 41.1 Billion |

| Market Size in 2034 | USD 69.8 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible packaging dominated the market in 2024, accounting for approximately 48.9% of total revenue. The segment benefits from widespread utilization across baby diapers, sanitary products, wipes, tissues, and healthcare disposables. Flexible packaging offers excellent product protection, lightweight characteristics, lower transportation costs, and strong branding capabilities. Manufacturers increasingly utilize flexible pouches, wraps, and sachets to improve convenience and operational efficiency. For example, major diaper and feminine hygiene brands commonly employ multi-layer flexible packaging structures to maintain product integrity during storage and distribution. Continuous innovation in film technology and barrier materials continues to strengthen segment dominance.

Smart hygiene packaging is expected to be the fastest-growing segment, expanding at a CAGR of 8.1% through 2034. Growth is driven by increasing demand for traceability, safety monitoring, and consumer engagement features. Smart packaging technologies include QR codes, digital authentication systems, and antimicrobial materials. Healthcare product manufacturers are increasingly adopting these solutions to improve product tracking and reduce counterfeiting risks. Future developments in connected packaging and sensor technologies are expected to create new opportunities throughout the health hygiene packaging market.

By Material

Plastic-based packaging accounted for the largest market share in 2024, representing approximately 56.8% of total revenue. Materials such as polyethylene and polypropylene remain widely used because they provide durability, moisture resistance, flexibility, and cost efficiency. Plastic packaging is extensively utilized for diapers, sanitary napkins, wipes, and healthcare disposables. Industry examples include resealable diaper packs and moisture-resistant sanitary product packaging. Despite increasing sustainability concerns, plastic materials continue to dominate due to their performance characteristics and manufacturing scalability.

Paper-based packaging is projected to be the fastest-growing material segment, registering a CAGR of 7.6% through 2034. Growth is supported by sustainability initiatives, regulatory pressures, and changing consumer preferences. Manufacturers are increasingly replacing plastic components with paper-based alternatives where feasible. Innovations in coated paper technologies are improving moisture resistance and product protection capabilities. Future developments are expected to expand paper-based packaging applications across multiple hygiene product categories, supporting long-term market growth.

By End-Use

Personal hygiene products held the largest market share in 2024, accounting for approximately 44.7% of total market revenue. This segment includes baby diapers, feminine hygiene products, tissues, wipes, and adult incontinence products. Strong consumer demand, rising awareness, and increasing product accessibility continue to support growth. Packaging plays a critical role in maintaining hygiene standards, protecting products from contamination, and enhancing convenience. Major consumer goods manufacturers consistently invest in packaging innovation to improve product differentiation and consumer appeal.

Healthcare disposables are expected to be the fastest-growing end-use segment, expanding at a CAGR of 7.8% during the forecast period. Growth is driven by increasing healthcare expenditures, rising demand for infection prevention products, and expanding healthcare infrastructure. Applications include surgical supplies, protective equipment, diagnostic products, and medical consumables. Packaging innovations focused on sterility maintenance, tamper evidence, and traceability are supporting segment growth. Future demand is expected to remain strong as healthcare systems continue expanding globally.

Health Hygiene Packaging Market Segmentations

By Type

- Flexible Packaging

- Rigid Packaging

- Smart Hygiene Packaging

- Sterile Packaging

By Material

- Plastic-Based Packaging

- Paper-Based Packaging

- Aluminum-Based Packaging

- Bio-Based Packaging

By End-User

- Personal Hygiene Products

- Healthcare Disposables

- Medical Devices

- Pharmaceutical Hygiene Products

- Household Hygiene Products

Regional Analysis

North America

North America accounted for approximately 27.8% of the global health hygiene packaging market share in 2025 and is projected to register a CAGR of 6.2% through 2034. The region benefits from high awareness regarding personal hygiene, strong healthcare infrastructure, and substantial spending on healthcare and personal care products. Demand for premium hygiene products continues to increase, encouraging manufacturers to adopt advanced packaging technologies that enhance product protection and convenience. The presence of major packaging suppliers and healthcare product manufacturers further supports market development. Growing demand for sustainable packaging solutions is also contributing to innovation throughout the regional market.

The United States dominates the North American market. A unique growth driver is the growing demand for premium baby care and adult incontinence products. Manufacturers increasingly utilize high-performance packaging materials that improve product shelf life and consumer convenience. An industry trend involves the adoption of recyclable flexible packaging for hygiene products by leading consumer goods companies. The combination of strong consumer purchasing power and innovation-driven packaging development is expected to sustain market growth.

Europe

Europe held approximately 24.6% market share in 2025 and is forecast to expand at a CAGR of 6.4% during the forecast period. The market is supported by stringent packaging regulations, increasing sustainability initiatives, and widespread adoption of personal hygiene products. Consumers across Europe demonstrate strong preference for environmentally responsible packaging, encouraging manufacturers to develop recyclable and paper-based solutions. Growth in healthcare product consumption and aging populations are also supporting demand. The region continues to invest heavily in sustainable packaging technologies and circular economy programs.

Germany remains the dominant country within Europe. A unique growth factor is the country's leadership in sustainable packaging innovation. Hygiene product manufacturers are collaborating with packaging suppliers to reduce plastic usage and improve recyclability. An industry trend involves increasing adoption of mono-material flexible packaging structures for sanitary and personal care products. These developments are expected to support continued market expansion across the German market.

Asia Pacific

Asia Pacific dominated the global market with a 39.6% share in 2025 and is expected to grow at a CAGR of 7.3% through 2034. Rapid population growth, increasing disposable income, urbanization, and rising awareness regarding hygiene are key growth drivers. Demand for baby diapers, feminine hygiene products, and healthcare disposables continues to increase significantly throughout the region. Expanding manufacturing activities and improvements in healthcare access further support market growth. Several multinational hygiene product manufacturers are expanding production facilities within Asia Pacific to serve growing consumer demand.

China is the leading country within the region. A unique growth driver is the rapid expansion of domestic hygiene product manufacturing. Rising consumer awareness regarding health and sanitation has encouraged greater adoption of premium hygiene products. An industry trend involves increasing use of digitally printed packaging and high-barrier flexible materials to improve branding and product protection. Continued growth in healthcare spending and consumer product demand is expected to support long-term market expansion.

Middle East & Africa

The Middle East & Africa represented approximately 3.8% of global market revenue in 2025 and is projected to register a CAGR of 6.8% through 2034. Growth is supported by improving healthcare infrastructure, increasing hygiene awareness, and expanding retail networks. Government health initiatives and population growth are encouraging greater adoption of hygiene products across several countries. Packaging suppliers are increasingly introducing affordable and durable packaging formats designed for local market requirements. Demand for healthcare disposables and sanitation products is also contributing to market development.

Saudi Arabia dominates the regional market. A unique growth factor is the government's continued investment in healthcare modernization and public health programs. Demand for medical disposables, personal hygiene products, and healthcare packaging has increased substantially. An industry trend includes expansion of local manufacturing facilities aimed at reducing dependence on imports. These developments are expected to strengthen demand for health hygiene packaging solutions across the country.

Latin America

Latin America accounted for approximately 4.2% of global market share in 2025 and is projected to record the fastest CAGR of 7.4% through 2034. Rising consumer awareness regarding personal hygiene, expanding healthcare access, and growing urban populations are driving market growth. Governments and non-governmental organizations are implementing awareness campaigns focused on sanitation and hygiene practices. Increasing penetration of modern retail formats and online distribution channels is further supporting demand for packaged hygiene products.

Brazil remains the dominant country within Latin America. A unique growth driver is the increasing adoption of feminine hygiene products among underserved populations. Packaging manufacturers are introducing cost-effective and convenient packaging formats tailored to local consumer needs. An industry trend involves growing investments in sustainable packaging production capabilities to meet rising environmental expectations. These factors are expected to contribute to continued regional market expansion.

Competitive Landscape

The health hygiene packaging market is characterized by strong competition among global packaging manufacturers focused on innovation, sustainability, and product performance. Companies are investing in recyclable materials, smart packaging technologies, and production capacity expansion to strengthen their market positions.

Amcor plc is recognized as a leading participant in the market due to its extensive healthcare and personal care packaging portfolio. The company recently expanded its sustainable flexible packaging offerings for hygiene applications, supporting brand owners seeking environmentally responsible solutions.

Other major companies include Berry Global Inc., Mondi plc, Sonoco Products Company, and Sealed Air Corporation. These companies continue to develop lightweight packaging formats, recyclable material structures, and advanced barrier technologies. Strategic partnerships with healthcare and consumer goods manufacturers remain important growth strategies. Investments in digital printing, sustainable materials, and operational efficiency are expected to shape competitive dynamics throughout the forecast period.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi plc

- Sonoco Products Company

- Sealed Air Corporation

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Coveris Holdings S.A.

- ProAmpac LLC

- DS Smith plc

- WestRock Company

- International Paper Company

- Smurfit Westrock plc

- UFlex Limited

- Winpak Ltd.

- AptarGroup Inc.

- Gerresheimer AG

- Bemis Healthcare Packaging