Sterile Medical Packaging Market Size and Growth

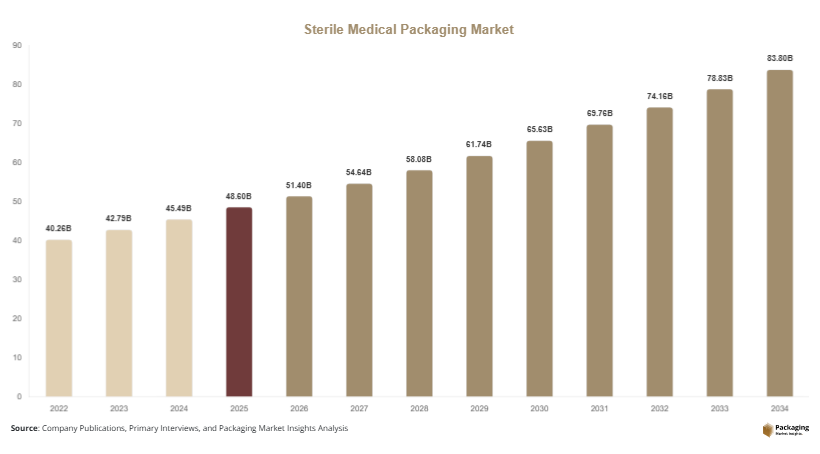

The global sterile medical packaging market size was valued at USD 48.6 billion in 2025 and is projected to reach USD 51.4 billion in 2026. By 2034, the market is forecast to reach USD 83.9 billion, registering a CAGR of 6.3% during the forecast period from 2025 to 2034. Sterile medical packaging plays a critical role in maintaining product integrity, reducing infection risks, and ensuring compliance with healthcare regulations across pharmaceutical, biotechnology, diagnostic, and medical device industries. The sterile medical packaging market is witnessing stable expansion due to increasing demand for contamination-free medical products, growth in pharmaceutical manufacturing, and rising adoption of advanced healthcare devices.

One of the major growth factors driving the market is the increasing global volume of surgical procedures and hospital admissions. The rise in chronic diseases, aging populations, and expansion of healthcare infrastructure have accelerated the consumption of sterile medical devices and pharmaceuticals, increasing demand for sterile barrier packaging systems. Healthcare providers continue to emphasize infection prevention, leading to wider adoption of sterilized trays, pouches, wraps, and blister packaging solutions.

Key Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Thermoform trays led the type segment with a 31.4% share.

- Plastic materials dominated with a 54.8% share.

- Pharmaceutical applications led the end-use segment with 42.6% share.

- The US remained the dominant country with a market size of USD 10.8 billion in 2025 and USD 11.4 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Sterile Packaging Solutions

Healthcare companies are increasingly adopting sustainable sterile medical packaging solutions to reduce environmental impact and comply with stricter waste management regulations. Hospitals and pharmaceutical manufacturers are focusing on recyclable polymers, lightweight packaging materials, and reduced plastic consumption across sterile barrier systems. Medical packaging suppliers are developing mono-material pouches and recyclable thermoformed trays that maintain sterility while lowering packaging waste. For instance, several pharmaceutical packaging manufacturers in Europe have introduced recyclable polyethylene-based sterile films for medical device applications. This trend is expected to influence procurement strategies among hospitals and healthcare providers over the next decade. Rising sustainability commitments from global healthcare companies will likely encourage investments in renewable materials, energy-efficient production technologies, and biodegradable sterile packaging formats.

Rising Use of Smart and Traceable Medical Packaging

The market is witnessing increasing integration of smart packaging technologies for product authentication, traceability, and inventory monitoring. Healthcare providers and pharmaceutical manufacturers are using QR codes, RFID tags, temperature indicators, and digital tracking systems in sterile medical packaging to improve supply chain transparency. These technologies help monitor sterilization status, storage conditions, and product authenticity during transportation. Pharmaceutical companies handling temperature-sensitive biologics and vaccines are increasingly adopting intelligent packaging systems to reduce product loss and contamination risks. For example, cold-chain packaging suppliers in North America are introducing smart labels capable of detecting temperature fluctuations during shipment. The future impact of this trend is significant as digital healthcare systems continue expanding. Smart sterile packaging is expected to support regulatory compliance, reduce counterfeiting risks, and improve operational efficiency across healthcare supply chains.

Market Drivers

Increasing Demand for Sterile Pharmaceutical Packaging

The rising production of injectable drugs, vaccines, biologics, and specialty medicines is driving the demand for sterile pharmaceutical packaging solutions worldwide. Pharmaceutical manufacturers require high-barrier packaging systems that preserve product sterility and extend shelf life. Growth in chronic diseases and immunization programs has significantly increased global pharmaceutical production volumes. As a result, sterile blister packs, vials, pouches, and trays are witnessing strong demand across developed and emerging economies. For example, expanding vaccine production facilities in India and the United States have increased demand for sterilized medical-grade packaging materials. The cause-and-effect relationship is clear as higher pharmaceutical manufacturing directly raises the need for reliable sterile packaging solutions capable of preventing contamination during transportation and storage.

Expansion of Healthcare Infrastructure and Surgical Procedures

Rapid expansion of healthcare infrastructure and rising surgical procedures are significantly contributing to market growth. Hospitals, ambulatory surgical centers, and diagnostic laboratories require sterile packaging for medical instruments, surgical kits, catheters, and disposable devices. Aging populations and increasing incidence of chronic illnesses have accelerated hospital admissions globally. Countries such as China, Brazil, and Saudi Arabia are investing heavily in healthcare infrastructure development, creating new opportunities for sterile packaging suppliers. In addition, minimally invasive surgeries and advanced medical procedures require specialized sterile packaging solutions with improved durability and sealing performance. Medical device manufacturers are therefore increasing investments in sterile barrier packaging systems to meet growing demand from hospitals and outpatient facilities.

Market Restraint

High Costs Associated with Sterile Packaging Compliance and Validation

One of the primary restraints affecting the sterile medical packaging market is the high cost associated with regulatory compliance, sterilization validation, and quality assurance processes. Sterile medical packaging materials must comply with stringent international standards related to contamination control, material compatibility, and patient safety. Manufacturers are required to conduct extensive testing for seal integrity, microbial barrier performance, sterilization compatibility, and transportation durability. These procedures significantly increase production costs, especially for small and medium-sized packaging companies.

In addition, fluctuations in raw material prices for medical-grade plastics, films, and specialty coatings are affecting profitability across the industry. The transition toward sustainable and recyclable materials further adds complexity and investment requirements for manufacturers. For example, healthcare packaging suppliers adopting recyclable sterile films often face higher development costs due to material performance limitations during sterilization processes. Smaller healthcare providers and local pharmaceutical companies in developing economies may struggle to adopt advanced sterile packaging solutions because of budget constraints. This cost pressure can slow market penetration in price-sensitive regions and limit adoption of innovative packaging technologies.

Market Opportunities

Growth of Home Healthcare and Self-Administration Devices

The rapid growth of home healthcare services and self-administered medical devices presents strong opportunities for sterile medical packaging manufacturers. Patients increasingly prefer home-based treatment solutions such as insulin pens, injectable therapies, wound care products, and portable diagnostic devices. These products require compact, lightweight, and highly sterile packaging formats to ensure patient safety and ease of use. Packaging manufacturers are developing user-friendly sterile pouches, peelable films, and tamper-evident containers designed specifically for home healthcare applications.

The future scope for this opportunity is substantial as aging populations and healthcare cost reduction strategies continue encouraging home treatment adoption. For example, demand for sterile packaging for home dialysis kits and wearable drug delivery devices has increased significantly in North America and Europe. Packaging suppliers that focus on ergonomic designs and simplified opening mechanisms are expected to gain competitive advantages in the coming years.

Rising Demand for Sustainable Medical Packaging Materials

Sustainability initiatives across healthcare industries are creating new opportunities for environmentally responsible sterile medical packaging solutions. Governments and healthcare organizations are implementing waste reduction targets and encouraging adoption of recyclable materials. Packaging manufacturers are investing in recyclable polymer films, paper-based sterile barriers, and bio-based materials that meet sterility requirements while reducing environmental impact.

This opportunity is expected to expand rapidly as pharmaceutical companies incorporate sustainability targets into procurement strategies. For instance, medical packaging suppliers in Europe are introducing fiber-based sterile packaging structures with lower carbon footprints. The growing adoption of circular economy practices and green healthcare initiatives will likely support long-term demand for sustainable sterile packaging technologies. Emerging economies are also beginning to adopt eco-friendly healthcare packaging standards, further increasing growth potential across the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.6 Billion |

| Market Size in 2026 | USD 51.4 Billion |

| Market Size in 2034 | USD 83.9 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Thermoform trays dominated the sterile medical packaging market in 2024, accounting for approximately 31.4% of the total market share. These packaging formats are widely used for surgical instruments, implantable devices, catheters, and diagnostic products because they provide superior product protection, structural rigidity, and sterilization compatibility. Thermoform trays are commonly manufactured using medical-grade polyethylene terephthalate glycol (PETG), high-density polyethylene (HDPE), and polypropylene materials that can withstand ethylene oxide and gamma sterilization processes. Their dominance is also supported by the increasing demand for customized packaging configurations for complex medical devices. Major healthcare manufacturers prefer thermoform trays because they reduce contamination risks during transportation and storage. For example, orthopedic implant manufacturers in the United States and Germany increasingly use multi-compartment thermoform packaging systems for enhanced product organization and sterilization performance. In addition, the rise of minimally invasive surgical devices and disposable healthcare instruments continues supporting demand for sterile tray packaging across hospitals and ambulatory surgical centers.

Sterile pouches are projected to witness the fastest CAGR of 7.3% during the forecast period. Growth is primarily driven by rising demand for lightweight, flexible, and cost-efficient sterile packaging solutions across healthcare applications. Sterile pouches are extensively used for single-use surgical tools, wound care products, syringes, and home healthcare consumables. Their popularity is increasing because of ease of handling, reduced storage requirements, and compatibility with multiple sterilization techniques. Manufacturers are introducing high-barrier peelable pouches with enhanced puncture resistance and improved sealing performance. Demand for sterile pouches is also growing in emerging economies due to expanding healthcare infrastructure and increasing use of disposable medical products. Sustainability trends are encouraging the development of recyclable pouch materials and mono-material sterile barrier systems. Future market growth is expected to benefit from rising home healthcare adoption, increasing pharmaceutical exports, and growth in e-commerce distribution of medical supplies requiring compact sterile packaging formats.

By Material

Plastic materials held the largest share of the sterile medical packaging market in 2024, contributing nearly 54.8% of overall revenue. Plastic remains the preferred material because of its excellent barrier properties, durability, flexibility, and compatibility with sterilization methods such as gamma radiation and ethylene oxide treatment. Polyethylene, polypropylene, PET, and PVC are widely used in sterile packaging for pharmaceutical products, surgical kits, medical trays, and blister packaging systems. The dominance of plastic materials is also linked to their cost efficiency and ability to maintain product integrity during transportation. Healthcare packaging manufacturers favor plastics because they can be molded into customized packaging structures with high seal strength and contamination resistance. For instance, prefilled syringe packaging and IV therapy packaging systems heavily rely on medical-grade plastics to ensure patient safety and product stability. Growth in biologics manufacturing and vaccine distribution has further strengthened demand for advanced plastic-based sterile packaging materials worldwide.

Paper and paperboard materials are expected to record the fastest CAGR of 6.8% over the forecast period due to increasing sustainability initiatives across the healthcare industry. Hospitals, pharmaceutical companies, and packaging manufacturers are actively seeking eco-friendly alternatives to reduce medical waste and carbon emissions. Sterile paper-based wraps, pouches, and medical-grade kraft paper products are gaining popularity because they offer recyclability and lower environmental impact. Innovations in coated paper materials with enhanced microbial barrier performance are expanding their application range across surgical instrument packaging and sterile medical supplies. European healthcare systems are particularly encouraging adoption of recyclable paper-based sterile packaging solutions through stricter environmental regulations. Manufacturers are also developing hybrid paper-polymer structures that balance sustainability with high sterilization compatibility. Future growth in this segment is expected to benefit from rising government pressure on healthcare waste reduction and increasing investments in renewable packaging technologies across pharmaceutical and medical device industries.

By End-Use

Pharmaceutical manufacturing emerged as the dominant end-use segment in 2024, accounting for approximately 42.6% of the global sterile medical packaging market share. The segment’s dominance is driven by the increasing production of injectable drugs, vaccines, biologics, and specialty medicines requiring contamination-free packaging environments. Pharmaceutical companies depend on sterile packaging solutions such as blister packs, vials, pouches, ampoules, and sterile films to maintain product stability and regulatory compliance. Rising prevalence of chronic diseases and expansion of immunization programs have significantly increased demand for sterile pharmaceutical packaging worldwide. Large pharmaceutical producers in the United States, India, and China continue investing in automated sterile packaging facilities to improve production efficiency and minimize contamination risks. Growth in contract pharmaceutical manufacturing organizations is also supporting higher packaging consumption. In addition, stringent healthcare regulations related to patient safety and product integrity continue encouraging pharmaceutical companies to adopt advanced sterile barrier packaging technologies.

Home healthcare applications are projected to grow at the fastest CAGR of 7.5% during the forecast period. Increasing preference for at-home treatment, remote patient monitoring, and self-administered therapies is driving demand for compact and user-friendly sterile packaging solutions. Medical products such as insulin delivery systems, diagnostic kits, wound care products, and disposable injection devices require reliable sterile packaging to ensure safe patient use. Healthcare providers are increasingly focusing on reducing hospital admissions and treatment costs, encouraging broader adoption of home healthcare solutions. Packaging manufacturers are responding by developing lightweight sterile pouches, easy-open blister packs, and tamper-evident packaging systems designed specifically for consumer convenience. Demand for portable and single-use sterile medical products is particularly strong in North America, Europe, and parts of Asia Pacific. Future growth opportunities in this segment are expected to emerge from aging populations, rising chronic disease management programs, and expanding digital healthcare ecosystems worldwide.

Sterile Medical Packaging Market Segmentations

By Type

- Thermoform Trays

- Sterile Bottles & Containers

- Pouches & Bags

- Blister & Clamshell Packaging

- Wraps & Lids

By Material

- Plastic

- Paper & Paperboard

- Aluminum Foil

- Tyvek

- Glass

By End-User

- Pharmaceutical Companies

- Medical Device Manufacturers

- Hospitals & Clinics

- Diagnostic Laboratories

- Contract Manufacturing Organizations

Regional Analysis

North America

North America accounted for 28.7% of the global sterile medical packaging market share in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. The region benefits from advanced healthcare infrastructure, high pharmaceutical spending, and strong regulatory standards for sterile packaging. Demand for biologics, injectable drugs, and minimally invasive surgical devices continues supporting packaging consumption across the United States and Canada. In addition, rising adoption of home healthcare solutions and increasing healthcare expenditure are strengthening market growth. Packaging manufacturers in the region are investing in sustainable medical packaging technologies and smart traceability solutions to improve operational efficiency and regulatory compliance.

The United States dominates the regional market due to its large pharmaceutical manufacturing industry and expanding medical device sector. Growth is supported by rising surgical procedure volumes and increasing biologics production. Several healthcare packaging suppliers are expanding sterile packaging production facilities across the country to meet growing demand for sterile pouches, thermoform trays, and prefillable systems. The country is also witnessing rising adoption of RFID-enabled sterile packaging for healthcare inventory management. Investments in vaccine manufacturing and temperature-sensitive biologic packaging are expected to create additional opportunities throughout the forecast period.

Europe

Europe represented 24.8% of the sterile medical packaging market in 2025 and is expected to register a CAGR of 5.8% through 2034. Strict healthcare safety regulations and strong environmental policies are influencing packaging innovation across the region. Pharmaceutical and biotechnology companies are increasingly adopting recyclable sterile packaging materials to comply with sustainability goals. Demand for advanced sterile barrier systems remains high across Germany, France, Italy, and the United Kingdom. In addition, the growing elderly population and expansion of healthcare services continue driving consumption of sterile medical products and packaging solutions.

Germany leads the European market due to its strong pharmaceutical manufacturing base and advanced medical technology industry. The country has witnessed growing demand for sterile packaging in injectable drug delivery systems and surgical device packaging. German packaging companies are investing in recyclable medical-grade materials and automated packaging technologies to improve efficiency and sustainability. Expansion of biologics manufacturing and growing exports of medical devices are also contributing to regional market growth. The increasing use of paper-based sterile wraps in hospitals reflects changing healthcare procurement strategies across Europe.

Asia Pacific

Asia Pacific held the largest market share of 39.1% in 2025 and is forecast to grow at a CAGR of 7.2% during the forecast period. Rapid expansion of healthcare infrastructure, pharmaceutical manufacturing growth, and increasing healthcare spending are major factors supporting regional demand. Countries including China, India, Japan, and South Korea are experiencing rising consumption of sterile medical products due to population growth and improved healthcare access. The region is also benefiting from increasing foreign investments in pharmaceutical production and contract manufacturing services. Growing awareness regarding infection prevention is accelerating adoption of advanced sterile packaging systems.

China remains the dominant country in the region due to its extensive pharmaceutical manufacturing industry and expanding hospital infrastructure. The country has become a major global supplier of medical consumables and sterile healthcare products. Chinese packaging manufacturers are increasing investments in high-barrier sterile films and automated packaging systems to support export demand. The rise of domestic biologics manufacturing and vaccine production facilities is also contributing to increased packaging consumption. In India, rapid growth in contract pharmaceutical manufacturing is creating additional opportunities for sterile packaging suppliers focused on cost-effective and sustainable solutions.

Middle East & Africa

The Middle East & Africa accounted for 4.9% of the market share in 2025 and is expected to grow at a CAGR of 6.1% through 2034. Healthcare modernization initiatives and increasing pharmaceutical imports are supporting regional demand for sterile medical packaging. Governments in Gulf Cooperation Council countries are investing heavily in healthcare infrastructure development, including hospitals, medical laboratories, and pharmaceutical manufacturing facilities. Demand for sterile packaging solutions is increasing due to rising healthcare awareness and expanding access to medical services. In addition, medical tourism growth in countries such as the United Arab Emirates and Saudi Arabia is supporting higher consumption of sterile healthcare products.

Saudi Arabia dominates the regional market due to its large-scale healthcare investments and expanding pharmaceutical sector. The country is increasing domestic pharmaceutical production to reduce dependence on imports, which is boosting demand for sterile packaging solutions. Growth in hospital construction projects and rising surgical procedures are contributing to packaging demand across the healthcare system. Healthcare providers are also focusing on infection control measures, encouraging adoption of high-quality sterile barrier packaging materials. Increasing investment in cold-chain logistics and biologic drug storage infrastructure is expected to support future market growth.

Latin America

Latin America represented 2.5% of the global sterile medical packaging market in 2025 and is projected to grow at the fastest CAGR of 7.1% during the forecast period. Rising healthcare expenditure, increasing pharmaceutical production, and improving healthcare access are supporting regional market expansion. Countries including Brazil, Mexico, and Argentina are witnessing increased demand for sterile medical products due to growing chronic disease prevalence and expanding healthcare coverage programs. The rise of local pharmaceutical manufacturing and generic drug production is also contributing to packaging demand across the region.

Brazil leads the Latin American market due to its growing pharmaceutical industry and large healthcare consumer base. The country is witnessing increasing demand for sterile packaging solutions used in injectable drugs, surgical instruments, and diagnostic kits. Expansion of local medical device manufacturing and rising imports of advanced healthcare products are supporting packaging consumption. In addition, healthcare providers are focusing on improved sterilization standards and contamination prevention measures. Packaging companies operating in Brazil are introducing cost-efficient sterile packaging materials designed for emerging healthcare markets, creating favorable long-term growth opportunities.

Competitive Landscape

The sterile medical packaging market is moderately consolidated, with leading companies focusing on product innovation, sustainable material development, and strategic partnerships to strengthen their global market presence. Major players are investing heavily in advanced barrier technologies, recyclable sterile packaging materials, and automation systems to improve operational efficiency and comply with evolving healthcare regulations. Competition is increasing due to rising demand for pharmaceutical and medical device packaging solutions across developed and emerging markets.

Amcor plc remains one of the leading companies in the market due to its broad healthcare packaging portfolio, strong global manufacturing network, and continuous investment in sustainable medical-grade packaging materials. The company has focused on developing recyclable sterile packaging systems and high-barrier flexible films designed for pharmaceutical and medical device applications.

Berry Global Group, Inc. continues expanding its healthcare packaging division through acquisitions and product innovation strategies. The company has introduced lightweight sterile packaging solutions that reduce material consumption while maintaining sterilization performance. DuPont is strengthening its position through the expansion of Tyvek sterile packaging solutions widely used for medical devices and pharmaceutical products. West Pharmaceutical Services, Inc. is focusing on advanced containment and injectable packaging technologies to support biologics manufacturing growth.

Nelipak Corporation and Sonoco Products Company are increasing investments in thermoformed sterile trays and sustainable packaging systems to address rising demand from surgical device manufacturers. Companies are also collaborating with pharmaceutical manufacturers and healthcare providers to improve packaging customization, traceability, and contamination prevention capabilities.

Key Players List

- Amcor plc

- Berry Global Group, Inc.

- DuPont de Nemours, Inc.

- West Pharmaceutical Services, Inc.

- Sonoco Products Company

- Nelipak Corporation

- Wipak Group

- SteriPack Group

- TekniPlex Healthcare

- Sealed Air Corporation

- Oliver Healthcare Packaging

- Becton, Dickinson and Company

- Gerresheimer AG

- Mondi plc

- AptarGroup, Inc.