Medical Flexible Packaging Market Size and Growth

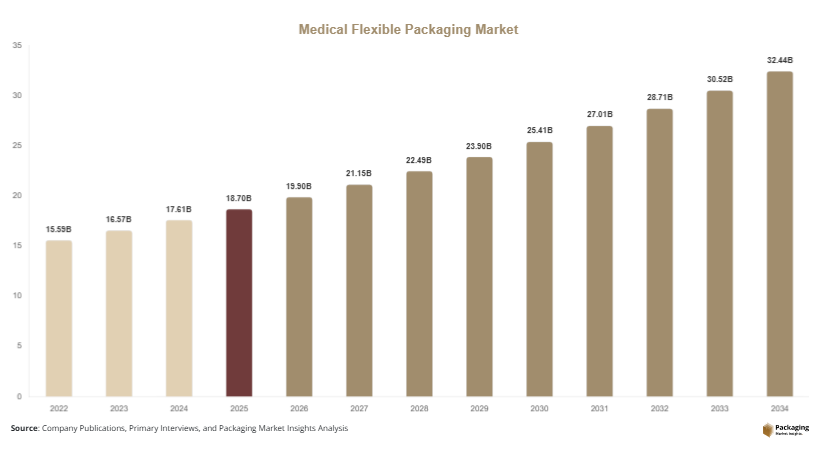

The global medical flexible packaging market size was valued at USD 18.7 billion in 2025 and is projected to reach USD 19.9 billion in 2026. By 2034, the market is forecasted to reach USD 34.6 billion, expanding at a CAGR of 6.3% during the forecast period from 2025 to 2034. Flexible packaging solutions are increasingly replacing rigid packaging formats because of their lower transportation costs, superior barrier properties, and enhanced convenience in handling and storage. The medical flexible packaging market is witnessing stable growth due to the increasing demand for sterile, lightweight, and cost-efficient healthcare packaging solutions across pharmaceutical, medical device, diagnostic, and biotechnology industries.

The growing global pharmaceutical industry remains one of the primary growth drivers for the market. Increasing production of generic drugs, biologics, vaccines, and medical consumables is accelerating the demand for high-performance flexible packaging materials such as pouches, sachets, wraps, and sterile bags. Healthcare providers are also focusing on reducing contamination risks, which supports the adoption of advanced sterile barrier packaging technologies. In addition, the rising number of surgical procedures and increasing consumption of disposable medical products are positively influencing packaging demand worldwide.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.8%.

- Pouches and bags led the type segment with a 34.7% share.

- Plastic-based flexible packaging dominated with a 58.9% share.

- Pharmaceutical applications led the segment with 46.3% share.

- The US remained the dominant country with a market size of USD 4.8 billion in 2025 and USD 5.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable Medical Packaging

Sustainability has become a major trend in the medical flexible packaging market as healthcare companies focus on reducing packaging waste and improving recyclability. Manufacturers are increasingly replacing multilayer non-recyclable structures with mono-material polyethylene and polypropylene packaging solutions that offer easier recycling processes. Pharmaceutical companies are also integrating post-consumer recycled content into secondary medical packaging applications to align with environmental regulations and sustainability goals.

For example, several packaging suppliers are developing recyclable medical pouches and sterilization wraps for hospitals and healthcare facilities. These innovations help healthcare providers reduce waste management costs while meeting sustainability targets. The future impact of this trend is expected to be significant, especially as governments implement stricter regulations regarding medical plastic waste disposal and carbon emissions reduction.

Growth of Smart and Traceable Packaging Solutions

The adoption of smart packaging technologies is increasing rapidly across the medical packaging sector. Pharmaceutical manufacturers are implementing QR codes, RFID tags, tamper-evident labels, and serialization systems to improve product tracking and prevent counterfeit medicines. Flexible packaging formats are increasingly integrated with digital authentication features that allow healthcare providers and patients to verify product authenticity.

For instance, pharmaceutical blister pouches with embedded tracking codes are being used to improve supply chain visibility and patient safety. Smart packaging also supports regulatory compliance in highly controlled pharmaceutical distribution networks. Over the coming years, the integration of IoT-enabled monitoring technologies and digital labeling systems is expected to enhance operational transparency and strengthen anti-counterfeit measures across global healthcare supply chains.

Market Drivers

Expansion of Pharmaceutical Manufacturing Activities

The continuous expansion of pharmaceutical manufacturing worldwide is a major factor driving the medical flexible packaging market. Increasing production of prescription drugs, vaccines, biologics, and over-the-counter medicines requires high-quality flexible packaging solutions capable of maintaining sterility and product integrity. Pharmaceutical manufacturers prefer flexible packaging because it reduces material usage while providing effective moisture, oxygen, and contamination barriers.

Countries such as India, China, and the United States are witnessing strong pharmaceutical production growth, leading to higher demand for pouches, sachets, strip packs, and flexible blister packaging. For example, generic drug manufacturing facilities are increasingly using multilayer flexible films to reduce packaging costs while ensuring compliance with healthcare safety standards. As pharmaceutical exports continue to rise globally, demand for durable and lightweight medical flexible packaging is expected to increase further.

Increasing Demand for Sterile Medical Packaging

The growing emphasis on infection prevention and patient safety is driving demand for sterile medical packaging solutions. Hospitals, clinics, and diagnostic laboratories require sterile packaging for surgical instruments, syringes, catheters, gloves, and medical consumables. Flexible packaging materials offer strong seal integrity, microbial resistance, and ease of sterilization, making them suitable for medical applications.

The increase in surgical procedures and healthcare-associated infection concerns has accelerated the use of sterile flexible packaging products. For instance, sterilizable pouches and medical-grade films are widely used in surgical centers and emergency healthcare facilities. The demand for single-use disposable medical products is also contributing to higher packaging consumption. This driver is expected to remain significant as healthcare systems continue focusing on hygiene and contamination control measures.

Market Restraint

Volatility in Raw Material Prices and Regulatory Compliance Costs

One of the major restraints affecting the medical flexible packaging market is the fluctuation in raw material prices combined with stringent regulatory compliance requirements. Medical flexible packaging relies heavily on polymers such as polyethylene, polypropylene, polyamide, and polyester, which are directly influenced by crude oil price volatility. Rising resin prices increase manufacturing costs and reduce profit margins for packaging companies.

In addition, medical packaging manufacturers must comply with strict regulatory standards related to sterility, safety, labeling, and material compatibility. Obtaining certifications for medical-grade packaging materials involves high testing and validation expenses. Small and medium-sized manufacturers often face operational challenges due to these compliance costs. For example, packaging companies supplying sterile pharmaceutical pouches must undergo extensive quality assurance procedures before product approval. These challenges may slow down market expansion, particularly in price-sensitive emerging economies.

Market Opportunities

Expansion of Home Healthcare and Telemedicine

The growing adoption of home healthcare services presents strong opportunities for the medical flexible packaging market. Increasing elderly populations and rising chronic disease cases are encouraging healthcare providers to deliver treatment solutions directly to patients’ homes. This trend is increasing demand for portable, lightweight, and user-friendly medical packaging formats.

Flexible packaging is widely used for home-delivered medicines, diagnostic kits, wearable medical devices, and personal healthcare products. For instance, resealable pouches and unit-dose sachets are gaining popularity in remote healthcare distribution systems. Future opportunities are expected to emerge from telemedicine growth and expanding online pharmacy services, which require secure and tamper-evident packaging for safe product delivery.

Development of High-Barrier and Advanced Functional Films

The development of high-barrier flexible films offers substantial growth opportunities for market participants. Pharmaceutical manufacturers increasingly require packaging materials capable of protecting sensitive biologics, injectables, and diagnostic products from moisture, oxygen, and UV exposure. Advanced multilayer films with enhanced barrier performance are becoming critical for extending product shelf life and maintaining efficacy.

Manufacturers are also investing in antimicrobial coatings and peelable seal technologies to improve patient convenience and packaging safety. For example, flexible packaging suppliers are introducing transparent high-barrier films for sterile device packaging applications. The future scope of this opportunity is significant as biotechnology and specialty pharmaceutical products continue to expand globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.7 Billion |

| Market Size in 2026 | USD 19.9 Billion |

| Market Size in 2034 | USD 34.6 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Pouches and bags dominated the type segment with a 34.7% market share in 2024. These packaging formats are widely used for pharmaceuticals, medical devices, surgical products, and diagnostic kits because they provide excellent flexibility, lightweight handling, and sterility protection. Hospitals and pharmaceutical manufacturers increasingly prefer pouches due to their cost efficiency and compatibility with sterilization processes such as ethylene oxide and gamma radiation. Medical pouches also support convenient storage and transportation while minimizing contamination risks. For example, pre-formed sterile pouches are extensively used for syringes, catheters, and disposable medical instruments. The growing demand for compact and portable healthcare packaging continues to strengthen the dominance of pouches and bags in the global market.

High-barrier films are projected to be the fastest-growing subsegment, expanding at a CAGR of 7.1% during the forecast period. These films offer enhanced protection against oxygen, moisture, UV radiation, and microbial contamination, making them suitable for sensitive pharmaceutical and biotechnology applications. The increasing production of biologics, vaccines, and specialty drugs is driving demand for advanced barrier packaging materials. Packaging manufacturers are developing multilayer films with improved durability and transparency to meet evolving pharmaceutical requirements. Future growth is expected to be supported by increasing investments in smart packaging technologies and temperature-sensitive healthcare product distribution systems.

By Material

Plastic-based flexible packaging accounted for the largest market share of 58.9% in 2024 due to its superior durability, flexibility, and barrier performance. Materials such as polyethylene, polypropylene, and polyester are widely used across pharmaceutical packaging applications because they provide excellent moisture resistance and seal integrity. Plastic flexible packaging is extensively utilized for IV bags, medical pouches, strip packaging, and sterilization wraps. Manufacturers prefer these materials because they reduce transportation costs and support high-speed packaging operations. For instance, pharmaceutical companies rely on multilayer plastic films to ensure long shelf life and contamination prevention for sensitive healthcare products. The growing use of disposable medical supplies continues to support strong demand for plastic-based flexible packaging.

Recyclable mono-material packaging is expected to witness the fastest growth at a CAGR of 7.4% through 2034. Increasing sustainability regulations and healthcare industry efforts to reduce plastic waste are encouraging the development of recyclable medical packaging materials. Manufacturers are introducing polyethylene-based mono-material pouches and films that offer improved recyclability without compromising sterility performance. Healthcare companies are also investing in eco-friendly packaging initiatives to reduce environmental impact and improve brand image. The future outlook for recyclable flexible packaging remains strong as sustainability becomes a key purchasing factor across pharmaceutical and healthcare industries.

By End-Use

Pharmaceutical applications dominated the end-use segment with a 46.3% share in 2024. The growing production of tablets, capsules, injectable drugs, and biologics is significantly increasing demand for flexible medical packaging solutions. Pharmaceutical manufacturers require sterile, tamper-evident, and high-barrier packaging materials to maintain product integrity and regulatory compliance. Flexible packaging formats also reduce storage space requirements and transportation costs compared to rigid packaging alternatives. For example, sachets, strip packs, and flexible blister packaging are widely used for oral solid dosage forms and unit-dose medications. Increasing pharmaceutical exports and rising generic drug production are further supporting segment dominance globally.

Diagnostic packaging is projected to register the fastest CAGR of 6.9% during the forecast period. Rising demand for diagnostic kits, rapid testing solutions, and laboratory consumables is driving growth in this segment. Flexible packaging materials are increasingly used for sample collection kits, testing strips, and sterile diagnostic components because they provide effective contamination control and lightweight portability. Healthcare providers are also expanding point-of-care testing services, which is increasing the need for compact and secure packaging formats. Future growth opportunities are expected from the expansion of personalized medicine and home diagnostic testing applications worldwide.

Medical Flexible Packaging Market Segmentations

By Type

- Bags & Pouches

- Wraps & Films

- Lids & Foils

- Sachets & Stick Packs

By Material

- Plastic

- Paper

- Aluminum Foil

- Biodegradable Materials

By End-User

- Pharmaceutical Packaging

- Medical Device Packaging

- Diagnostic Product Packaging

- Healthcare Consumables Packaging

Regional Analysis

North America

North America accounted for 28.4% of the medical flexible packaging market share in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. The region benefits from advanced healthcare infrastructure, strong pharmaceutical production capacity, and increasing adoption of sterile packaging technologies. Demand for flexible medical packaging is growing steadily across hospitals, pharmaceutical manufacturing facilities, and biotechnology companies. The United States and Canada are witnessing rising investments in healthcare logistics and cold chain packaging systems, which is accelerating flexible packaging consumption. The region also experiences strong demand for high-barrier films and tamper-evident pharmaceutical packaging solutions due to strict regulatory standards.

The United States dominates the North American market due to its large pharmaceutical manufacturing industry and growing biologics production. Increasing prescription drug consumption and expansion of specialty pharmaceutical distribution channels are driving demand for advanced medical packaging. For example, pharmaceutical companies in the U.S. are increasingly using recyclable medical pouches and lightweight sterile packaging systems to improve sustainability and reduce shipping costs. The growth of home healthcare and mail-order pharmacies is also contributing to increased demand for secure flexible packaging formats across the country.

Europe

Europe represented 24.7% of the global medical flexible packaging market in 2025 and is expected to grow at a CAGR of 5.8% through 2034. The region is characterized by strong healthcare regulations, advanced pharmaceutical research activities, and increasing investments in sustainable packaging technologies. European packaging manufacturers are focusing heavily on recyclable medical films and mono-material flexible packaging structures to comply with environmental targets. Growth in the medical device manufacturing sector is also increasing demand for sterile barrier packaging and protective flexible materials across healthcare applications.

Germany emerged as the leading country in the European market due to its strong pharmaceutical manufacturing base and advanced medical technology industry. The country is witnessing rising adoption of high-performance flexible packaging materials for diagnostic devices and sterile healthcare products. German healthcare companies are investing in automation and digital packaging systems to improve operational efficiency and traceability. Additionally, increasing exports of pharmaceutical products across Europe are supporting the growth of durable and lightweight flexible packaging solutions.

Asia Pacific

Asia Pacific dominated the medical flexible packaging market with a 39.2% share in 2025 and is forecasted to register a CAGR of 7.1% during the forecast period. Rapid healthcare infrastructure expansion, rising pharmaceutical production, and increasing population levels are driving strong market growth across the region. Countries such as China, India, Japan, and South Korea are experiencing increased demand for affordable and sterile medical packaging solutions. The region also benefits from lower manufacturing costs and growing investments in pharmaceutical exports.

China remains the dominant country in Asia Pacific due to its large pharmaceutical manufacturing sector and expanding healthcare investments. Rising production of generic medicines and medical consumables is increasing demand for flexible pouches, films, and sterilization packaging products. Chinese manufacturers are also investing in recyclable healthcare packaging materials to meet export regulations and sustainability goals. The rapid growth of e-commerce pharmaceutical distribution and government healthcare modernization initiatives are expected to strengthen long-term market growth across the country.

Middle East & Africa

The Middle East & Africa market accounted for 4.9% of the global medical flexible packaging market in 2025 and is projected to expand at a CAGR of 5.7% through 2034. Increasing healthcare investments, expanding hospital infrastructure, and growing pharmaceutical imports are supporting regional market development. Governments across Gulf countries are focusing on healthcare modernization programs and local pharmaceutical manufacturing, which is increasing demand for medical packaging products. Flexible packaging solutions are gaining traction because they reduce logistics costs and improve product shelf life in hot climatic conditions.

Saudi Arabia dominates the regional market due to its rising healthcare expenditure and pharmaceutical sector expansion. The country is witnessing increased demand for sterile packaging solutions for imported medicines and locally manufactured healthcare products. Healthcare providers are also investing in modern packaging technologies to improve patient safety and pharmaceutical storage efficiency. In addition, rising demand for disposable medical products during healthcare emergencies has accelerated the use of flexible sterile packaging formats across hospitals and clinics.

Latin America

Latin America held 2.8% of the medical flexible packaging market share in 2025 and is expected to register the fastest CAGR of 6.8% during the forecast period. The region is benefiting from expanding pharmaceutical distribution networks, rising healthcare awareness, and growing medical device imports. Flexible packaging demand is increasing across Brazil, Mexico, Argentina, and Chile due to improvements in healthcare access and pharmaceutical manufacturing capabilities. Medical packaging suppliers are increasingly targeting the region because of rising investments in healthcare infrastructure and retail pharmacy expansion.

Brazil emerged as the dominant country in the Latin American market owing to its growing pharmaceutical manufacturing industry and expanding healthcare system. Demand for flexible medical packaging is increasing across over-the-counter medicines, hospital consumables, and diagnostic kits. Brazilian packaging companies are also investing in sustainable flexible packaging materials to align with environmental regulations and export standards. Rising urbanization and increasing healthcare spending are expected to support continued market growth in the country over the next decade.

Competitive Landscape

The medical flexible packaging market is moderately consolidated with the presence of several global and regional manufacturers competing through product innovation, sustainability initiatives, and strategic partnerships. Leading companies are focusing on developing recyclable medical packaging solutions, high-barrier films, and advanced sterile packaging systems to strengthen their market positions.

Amcor plc remains one of the leading players in the market due to its extensive product portfolio, global manufacturing presence, and strong investment in sustainable medical packaging technologies. The company has introduced recyclable flexible healthcare packaging solutions designed for pharmaceutical and medical device applications. Berry Global Inc. is focusing on high-performance healthcare films and customized sterile packaging products. Sealed Air Corporation is expanding its healthcare packaging portfolio with advanced barrier materials and automation-friendly packaging solutions.

Mondi Group is investing in eco-friendly flexible packaging technologies to support pharmaceutical sustainability goals, while Sonoco Products Company continues expanding its sterile medical packaging operations through acquisitions and product innovation strategies. Companies are also investing in smart packaging systems integrated with traceability and anti-counterfeit features to improve healthcare supply chain security.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Sonoco Products Company

- Huhtamaki Oyj

- Constantia Flexibles

- Coveris Holdings S.A.

- Winpak Ltd.

- Glenroy Inc.

- UFlex Ltd.

- ProAmpac LLC

- Clondalkin Group

- Bischof + Klein SE

- Tekni-Plex Inc.