Healthcare Packaging Market Size and Growth

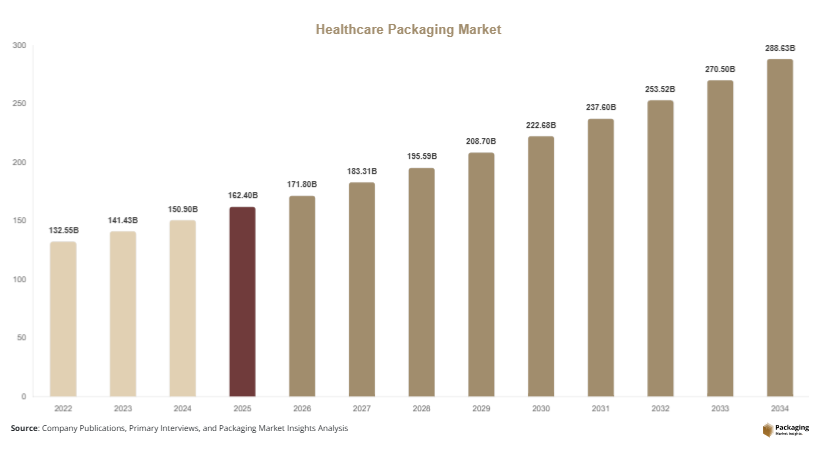

The healthcare packaging market size was valued at approximately USD 162.4 billion in 2025 and is projected to reach USD 171.8 billion in 2026. The market is expected to grow significantly and reach nearly USD 289.6 billion by 2034, expanding at a CAGR of 6.7% during 2025–2034. Growth in pharmaceutical exports, increasing biologics production, and rising healthcare spending are major factors driving market expansion globally. In addition, rapid development of temperature-sensitive medicines and personalized therapies is increasing the demand for advanced protective packaging formats.

The global healthcare packaging market is witnessing substantial growth due to increasing pharmaceutical production, rising demand for medical devices, and expanding healthcare infrastructure across developed and emerging economies. Healthcare packaging plays a critical role in ensuring product safety, sterility, stability, and regulatory compliance for pharmaceuticals, biologics, diagnostics, and medical equipment. Packaging solutions such as blister packs, vials, pouches, bottles, prefilled syringes, and sterile wraps are becoming increasingly important as healthcare supply chains become more complex and quality-focused.

Key Highlights

- North America dominated the market with a 34.8% share in 2025.

- Asia Pacific is projected to grow at the fastest CAGR of 7.4%.

- Blister packaging led the type segment with a 31.6% share.

- Plastic materials dominated with a 48.7% share.

- Pharmaceutical applications led the end-use segment with 52.4% share.

- The US remained the dominant country with a market size of USD 46.2 billion in 2025 and USD 48.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Smart and Trackable Packaging

One of the major trends influencing the healthcare packaging market is the growing integration of smart packaging technologies. Pharmaceutical companies are increasingly implementing RFID tags, QR codes, NFC-enabled labels, and digital serialization systems to improve product authentication and supply chain visibility. These technologies help reduce counterfeit medicines while improving inventory monitoring and patient safety. For example, several pharmaceutical manufacturers in North America and Europe are deploying track-and-trace packaging systems for high-value biologics and specialty drugs. Smart packaging also supports automated recalls and expiration tracking, improving healthcare logistics efficiency. Future demand for connected healthcare systems and digital compliance solutions is expected to accelerate adoption of intelligent healthcare packaging technologies globally.

Rising Demand for Sustainable Medical Packaging

Another important trend is the increasing shift toward sustainable healthcare packaging materials. Pharmaceutical companies and healthcare providers are focusing on reducing plastic waste while maintaining strict sterility and safety standards. Packaging manufacturers are introducing recyclable blister packs, mono-material pouches, lightweight bottles, and bio-based polymers for pharmaceutical applications. For example, several European healthcare packaging companies are developing recyclable thermoform blister packaging designed for over-the-counter medicines. Hospitals and healthcare systems are also exploring reusable transport packaging solutions for medical devices and diagnostics. Future regulatory pressure regarding medical waste reduction is expected to strengthen investment in environmentally responsible healthcare packaging solutions.

Market Drivers

Growing Pharmaceutical Production and Drug Consumption

The increasing production and consumption of pharmaceutical products is one of the key drivers supporting the healthcare packaging market. Rising prevalence of chronic diseases, aging populations, and expanding healthcare access are increasing demand for prescription medicines and over-the-counter drugs worldwide. Pharmaceutical companies require secure and compliant packaging solutions to maintain product integrity throughout manufacturing, transportation, and storage processes. Blister packs, bottles, vials, and pouches are witnessing strong demand due to rising tablet, capsule, and injectable drug production. For example, India and China are significantly expanding pharmaceutical manufacturing capacities, increasing demand for primary and secondary healthcare packaging products. Growth in generic medicines and self-medication trends is also supporting higher packaging consumption globally.

Expansion of Biologics and Temperature-Sensitive Therapies

The rapid growth of biologics, vaccines, and specialty injectable drugs is another major market driver. These products often require advanced cold-chain packaging systems that protect medicines from temperature fluctuations and contamination risks. Pharmaceutical companies are investing heavily in insulated containers, temperature-monitoring devices, and sterile packaging systems to support biologics distribution. For instance, global vaccine distribution programs and expansion of personalized medicine are increasing demand for specialized healthcare packaging solutions. Rising adoption of prefilled syringes and injectable drug delivery systems is also supporting packaging innovation. Continued growth in biologics production is expected to create strong long-term demand for advanced protective healthcare packaging technologies.

Market Restraint

Stringent Regulatory Compliance and High Packaging Costs

One of the primary restraints affecting the healthcare packaging market is the high cost associated with regulatory compliance and advanced packaging technologies. Healthcare packaging products must meet strict safety, sterility, labeling, and traceability standards established by regulatory authorities across different countries. Manufacturers often face significant investment requirements related to cleanroom facilities, quality control systems, serialization technologies, and compliance testing. In addition, advanced sterile barrier packaging and temperature-controlled solutions can increase operational and material costs. Smaller pharmaceutical companies and regional packaging suppliers may struggle to adopt sophisticated compliance systems due to limited financial resources. For example, serialization mandates in pharmaceutical packaging require extensive digital tracking infrastructure and packaging line modifications. Regulatory complexity across multiple international markets can also create supply chain delays and higher administrative costs. These challenges may limit profit margins and slow packaging innovation in cost-sensitive healthcare sectors.

Market Opportunities

Expansion of Home Healthcare and Online Pharmacy Services

The rapid growth of home healthcare and online pharmacy distribution is creating substantial opportunities for the healthcare packaging market. Patients increasingly prefer remote healthcare services and direct-to-home medicine delivery, increasing demand for durable and tamper-resistant packaging solutions. Pharmaceutical companies and logistics providers are adopting secure packaging systems that maintain product stability during transportation. Temperature-sensitive medicines, insulin products, and specialty drugs require advanced insulated packaging for home delivery applications. Countries such as the United States, Germany, and Japan are witnessing significant growth in e-pharmacy platforms and telehealth services. Future demand for patient-friendly packaging formats and smart delivery tracking systems is expected to support market expansion.

Rising Demand for Sustainable Sterile Packaging Solutions

The growing focus on environmentally responsible healthcare systems presents another major opportunity for market participants. Hospitals, pharmaceutical manufacturers, and regulators are increasingly seeking recyclable and lightweight healthcare packaging solutions that reduce medical waste. Packaging suppliers are developing mono-material sterile pouches, recyclable blister packaging, and eco-friendly medical containers to support sustainability targets. For example, healthcare packaging companies in Europe are investing in recyclable polymer technologies that maintain sterility while improving recyclability. Increasing pressure to reduce carbon emissions and packaging waste is expected to accelerate adoption of sustainable healthcare packaging innovations over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 162.4 Billion |

| Market Size in 2026 | USD 171.8 Billion |

| Market Size in 2034 | USD 289.6 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Blister packaging dominated the market in 2024 with approximately 31.6% share due to its strong protection capabilities, dosage convenience, and widespread pharmaceutical use. Blister packs are commonly used for tablets, capsules, and over-the-counter medicines because they provide excellent moisture resistance and product visibility. Pharmaceutical companies increasingly prefer blister packaging because it improves patient compliance and extends product shelf life. In Europe and North America, unit-dose blister packaging is widely adopted for prescription drug management and hospital dispensing systems. Packaging manufacturers are also integrating recyclable blister materials and smart labeling technologies to improve sustainability and product traceability. Rising pharmaceutical production and patient safety requirements continue to support segment dominance globally.

Prefilled syringes are expected to emerge as the fastest-growing type segment, registering a CAGR of 7.9% during the forecast period. The increasing use of biologics, vaccines, and injectable therapies is driving strong demand for ready-to-use syringe packaging solutions. Prefilled syringes improve dosing accuracy, reduce contamination risks, and simplify drug administration for healthcare providers and patients. Pharmaceutical companies are increasingly adopting advanced glass and polymer syringe packaging systems for specialty drugs and self-administered therapies. Countries including the United States, Germany, and Japan are witnessing rising adoption of injectable biologics for chronic disease treatment. Continued growth in personalized medicine and home healthcare services is expected to strengthen future demand for prefilled syringe packaging technologies.

By Material

Plastic materials dominated the healthcare packaging market in 2024 with approximately 48.7% share due to their lightweight structure, durability, and cost efficiency. Materials such as polyethylene, polypropylene, PVC, and PET are widely used in bottles, blister packs, pouches, and sterile medical packaging applications. Plastic packaging offers strong barrier protection against moisture and contamination while supporting large-scale pharmaceutical production processes. Manufacturers increasingly prefer high-performance polymers because they improve transportation efficiency and compatibility with automated filling systems. In addition, medical-grade plastics are essential for biologics packaging and sterile device protection. Continued demand for flexible and lightweight healthcare packaging solutions is expected to maintain strong segment dominance globally.

Recyclable paper-based packaging is projected to be the fastest-growing material segment with a CAGR of 7.1% during the forecast period. Pharmaceutical companies and healthcare providers are increasingly seeking sustainable alternatives to reduce medical packaging waste. Packaging suppliers are developing recyclable paperboard cartons, fiber-based secondary packaging, and mono-material paper solutions for pharmaceutical products. European healthcare systems are particularly focused on improving sustainability without compromising sterility and compliance standards. Technological improvements in barrier coatings and moisture-resistant paper materials are expanding the commercial viability of recyclable paper-based healthcare packaging. Continued sustainability initiatives and regulatory pressure regarding plastic waste reduction are expected to support long-term segment growth.

By End-Use

Pharmaceutical applications dominated the market in 2024 with approximately 52.4% share due to rising global medicine consumption and expanding pharmaceutical manufacturing activities. Packaging products such as blister packs, bottles, vials, pouches, and cartons are essential for protecting tablets, capsules, syrups, and injectable drugs during distribution and storage. Pharmaceutical companies increasingly require high-performance packaging solutions that ensure sterility, compliance, and product stability. Rapid growth in generic medicine production across Asia Pacific and Latin America is also increasing packaging demand. In addition, expansion of online pharmacy services and retail drug distribution networks continues to support strong demand for pharmaceutical packaging products globally.

Biologics and specialty drugs are expected to register the fastest growth with a CAGR of 8.2% during the forecast period. These therapies often require highly specialized packaging systems designed for temperature control, sterility, and contamination prevention. Pharmaceutical companies are increasingly investing in advanced cold-chain packaging solutions and high-barrier containers for biologics distribution. Rising prevalence of autoimmune diseases, cancer therapies, and personalized medicines is driving demand for injectable biologics worldwide. Countries such as the United States, China, and Switzerland are significantly expanding biologics manufacturing capacities, creating strong opportunities for advanced healthcare packaging suppliers. Continued growth in specialty pharmaceuticals is expected to support long-term market expansion.

Healthcare Packaging Market Segmentations

By Type

- Blister Packaging

- Bottles & Containers

- Vials & Ampoules

- Prefilled Syringes

- Pouches & Bags

By Material

- Plastic Packaging

- Glass Packaging

- Paper & Paperboard

- Aluminum Foil

By End-User

- Pharmaceuticals

- Medical Devices

- Biologics & Specialty Drugs

- Diagnostic Products

Regional Analysis

North America

North America accounted for approximately 34.8% of the global market share in 2025 and is projected to grow at a CAGR of 6.1% during the forecast period. The region benefits from advanced pharmaceutical manufacturing infrastructure, high healthcare expenditure, and strong regulatory standards for medical packaging. Pharmaceutical companies across the United States and Canada are investing heavily in sterile packaging systems, cold-chain solutions, and anti-counterfeiting technologies. Rising demand for biologics and specialty drugs is also increasing the need for advanced healthcare packaging products. In addition, expansion of online pharmacy services and home healthcare delivery is driving adoption of temperature-controlled and tamper-evident packaging systems throughout the region.

The United States dominates the North American market due to its large pharmaceutical industry and high biologics production capacity. A unique growth driver in the country is the increasing investment in personalized medicine and specialty injectable therapies. Pharmaceutical manufacturers are expanding production of biologics that require high-performance sterile packaging and temperature-sensitive transportation systems. Major healthcare packaging suppliers are also investing in smart labeling and digital serialization technologies to improve supply chain visibility and regulatory compliance. Continued innovation in cold-chain logistics and patient-centric packaging is expected to strengthen future market growth in the United States.

Europe

Europe represented nearly 27.2% market share in 2025 and is forecasted to expand at a CAGR of 6.0% through 2034. Strong pharmaceutical exports, strict healthcare regulations, and increasing sustainability initiatives are major factors supporting regional market growth. Countries including Germany, France, Switzerland, and the United Kingdom are witnessing rising demand for sterile medical packaging and high-barrier pharmaceutical containers. Healthcare packaging manufacturers are introducing recyclable blister packs and lightweight medical packaging materials to align with European sustainability targets. In addition, rising biologics production and vaccine manufacturing activities are increasing demand for specialized vials, ampoules, and cold-chain packaging systems.

Germany remains the dominant country in the European market because of its advanced pharmaceutical manufacturing sector and strong export activities. A unique growth factor in Germany is the increasing adoption of sustainable pharmaceutical packaging technologies. Pharmaceutical companies are collaborating with packaging suppliers to develop recyclable healthcare packaging materials that comply with strict European waste management regulations. The country is also investing heavily in automated pharmaceutical packaging systems integrated with digital tracking capabilities. Continued expansion of biologics production and sustainable healthcare initiatives is expected to support long-term market demand across Germany.

Asia Pacific

Asia Pacific held approximately 24.5% share of the global healthcare packaging market in 2025 and is expected to register the fastest CAGR of 7.4% during the forecast period. Rapid pharmaceutical manufacturing expansion, increasing healthcare investments, and growing medical device production are major factors supporting market growth across the region. Countries such as China, India, Japan, and South Korea are expanding pharmaceutical exports and investing in advanced healthcare infrastructure. Rising demand for affordable medicines and over-the-counter healthcare products is increasing the need for cost-efficient and durable packaging solutions. Flexible pharmaceutical packaging and blister packs remain particularly popular in densely populated economies due to lower production and transportation costs.

China dominates the Asia Pacific market due to its large pharmaceutical production base and expanding healthcare infrastructure. A unique growth driver in China is the rapid development of domestic biologics manufacturing and vaccine production capabilities. Pharmaceutical companies are increasingly investing in sterile packaging technologies and cold-chain transportation systems to support export-oriented drug manufacturing. In addition, the expansion of e-commerce pharmaceutical platforms is increasing demand for secure secondary healthcare packaging solutions. Continued investment in pharmaceutical innovation and healthcare modernization is expected to strengthen future market growth across China.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.1% market share in 2025 and is projected to expand at a CAGR of 6.5% during the forecast period. Increasing healthcare infrastructure investments and growing pharmaceutical imports are supporting demand for healthcare packaging products across the region. Governments are investing in hospital expansion, vaccine distribution programs, and local pharmaceutical manufacturing facilities to improve healthcare access. Packaging suppliers are increasingly providing sterile pouches, medical containers, and temperature-sensitive transport packaging for regional healthcare systems. In addition, rising awareness regarding counterfeit medicines is encouraging adoption of tamper-evident and trackable packaging technologies.

Saudi Arabia dominates the regional market because of strong healthcare investments and expanding pharmaceutical distribution networks. A unique growth factor in the country is the rapid development of domestic pharmaceutical manufacturing under national healthcare diversification strategies. Local pharmaceutical companies are increasing production of generic medicines and injectable therapies, driving demand for compliant healthcare packaging systems. The country is also investing in cold-chain logistics infrastructure to support vaccine and biologics distribution. Future growth in hospital infrastructure and pharmaceutical manufacturing is expected to support continued healthcare packaging demand across Saudi Arabia.

Latin America

Latin America accounted for nearly 7.4% market share in 2025 and is projected to grow at a CAGR of 6.9% through 2034. Rising pharmaceutical manufacturing activities and expanding healthcare access are driving market demand across Brazil, Mexico, and Argentina. Governments are increasing healthcare spending and encouraging local pharmaceutical production to reduce import dependency. Packaging suppliers are introducing affordable blister packaging, medical pouches, and sterile containers for generic medicines and healthcare products. Growing retail pharmacy networks and increasing self-medication trends are also supporting higher consumption of packaged healthcare products across the region.

Brazil remains the dominant country in the Latin American market due to its expanding pharmaceutical production sector and large healthcare consumer base. A unique growth driver in Brazil is the increasing domestic production of generic medicines and vaccines. Pharmaceutical manufacturers are investing in compliant packaging systems designed for large-scale drug distribution and export activities. In addition, healthcare packaging companies are expanding local production facilities to improve regional supply chain efficiency. Rising public healthcare investments and continued pharmaceutical industry expansion are expected to support long-term market growth in Brazil.

Competitive Landscape

The global healthcare packaging market is highly competitive, with major companies focusing on sterile packaging technologies, sustainability initiatives, and smart packaging innovation. Market participants are investing heavily in advanced barrier materials, temperature-sensitive packaging systems, and anti-counterfeiting technologies to strengthen market position. Increasing pharmaceutical exports and rising biologics production are encouraging packaging suppliers to expand global manufacturing capacities and cold-chain logistics solutions.

Amcor plc remains one of the leading players in the market due to its extensive healthcare packaging portfolio and strong global distribution network. Other major companies including West Pharmaceutical Services, Gerresheimer AG, Berry Global Inc., and AptarGroup Inc. are focusing on pharmaceutical packaging innovation and sustainable material development. Companies are increasingly collaborating with pharmaceutical manufacturers to develop customized sterile packaging solutions for biologics, vaccines, and specialty injectable drugs. Recent investments in recyclable healthcare packaging and smart labeling technologies are expected to intensify market competition during the forecast period.

Key Players List

- Amcor plc

- West Pharmaceutical Services, Inc.

- Gerresheimer AG

- Berry Global Inc.

- AptarGroup Inc.

- SCHOTT AG

- Sonoco Products Company

- Constantia Flexibles

- Sealed Air Corporation

- DuPont de Nemours, Inc.

- SGD Pharma

- Nipro Corporation

- Becton, Dickinson and Company

- Catalent, Inc.

- Oliver Healthcare Packaging