Thermoformed Cellulose Packaging Market Size and Growth

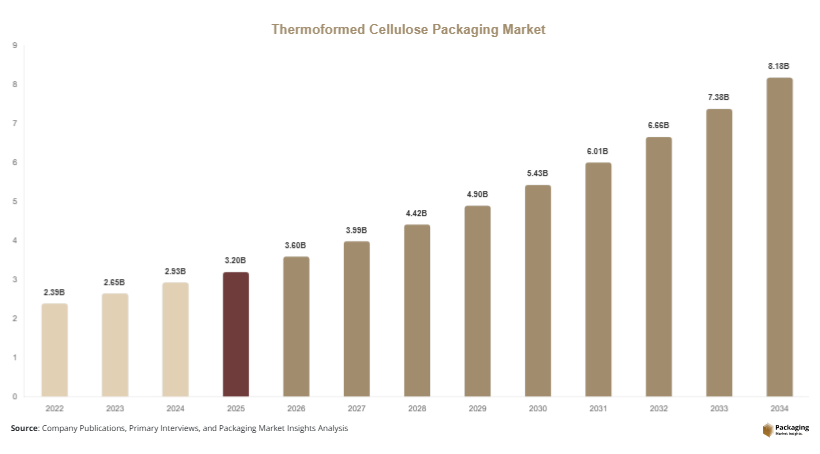

The global thermoformed cellulose packaging market size is estimated at USD 3.2 billion in 2025 and is projected to reach USD 3.6 billion in 2026, supported by rising demand for eco-friendly packaging solutions across food service, consumer goods, and electronics industries. Over the forecast period 2025–2034, the market is expected to grow at a CAGR of 10.8%, reaching approximately USD 8.1 billion by 2034. The thermoformed cellulose packaging market is gaining steady traction as industries transition toward sustainable, fiber-based, and biodegradable packaging alternatives.

One of the key growth factors is the increasing global shift away from plastic-based packaging. Regulatory restrictions on single-use plastics in North America, Europe, and parts of Asia Pacific are accelerating adoption of cellulose-based thermoformed packaging materials. These solutions offer biodegradability, compostability, and lower environmental impact, making them suitable for sustainable packaging mandates.

Key Highlights:

- The market size reached USD 3.2 billion in 2025, driven by increasing adoption of sustainable and fiber-based packaging solutions across multiple industries. Demand is primarily supported by food service, FMCG, and electronics packaging applications.

- It is projected to reach USD 8.1 billion by 2034, reflecting steady expansion as companies shift toward biodegradable and compostable packaging alternatives. Growth is further reinforced by global sustainability initiatives and material innovation.

- The market is expected to register a CAGR of 10.8% during 2025–2034, indicating strong and sustained adoption of thermoformed cellulose packaging solutions worldwide.

- Strong demand from food service, FMCG, and electronics packaging sectors continues to be a key growth driver. These industries are increasingly replacing plastic-based packaging with eco-friendly cellulose alternatives.

- Increasing regulatory push toward plastic substitution is accelerating market growth, as governments implement bans and restrictions on single-use plastics across major economies.

- Rising corporate sustainability and ESG adoption across industries is further supporting market expansion, as companies align packaging strategies with environmental goals and carbon reduction commitments.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Fully Compostable Packaging Systems

A major trend shaping the thermoformed cellulose packaging market is the growing adoption of fully compostable packaging systems. Manufacturers are increasingly developing cellulose-based solutions that break down completely in industrial and home composting environments. This trend is driven by rising environmental awareness and regulatory restrictions on plastic waste. Companies in food packaging, especially in Europe and North America, are replacing plastic trays and clamshells with molded cellulose alternatives. The demand is further supported by retailers and food service providers aiming to improve sustainability ratings and reduce landfill waste contributions. Technological advancements in fiber processing are also enabling better durability and moisture resistance in compostable packaging formats.

Integration of Advanced Pulp Molding Technologies

Another key trend is the integration of advanced pulp molding and thermoforming technologies to improve packaging performance. Manufacturers are adopting high-precision molding systems that enhance strength, surface finish, and design flexibility of cellulose packaging. These innovations allow production of complex shapes suitable for electronics, cosmetics, and premium food packaging applications. Automation and AI-driven manufacturing systems are also improving production efficiency and reducing material waste. This trend is particularly important as industries seek scalable alternatives to plastic while maintaining cost efficiency and product protection standards.

Market Drivers

Increasing Restrictions on Single-Use Plastics

The growing enforcement of bans and restrictions on single-use plastics is a major driver of the thermoformed cellulose packaging market. Governments across Europe, North America, and Asia Pacific are implementing strict regulations to reduce plastic waste and promote sustainable alternatives. These policies are pushing manufacturers to adopt cellulose-based packaging materials for compliance. Industries such as food service, retail, and e-commerce are transitioning rapidly to biodegradable packaging solutions to avoid regulatory penalties and meet sustainability targets. This regulatory pressure is significantly accelerating market adoption.

Rising Demand for Sustainable Food Packaging Solutions

The increasing demand for sustainable food packaging is another key growth driver. Consumers are becoming more environmentally conscious and prefer packaging made from renewable and biodegradable materials. Thermoformed cellulose packaging is widely used in trays, containers, and takeaway packaging due to its safety, light weight, and eco-friendly properties. The expansion of online food delivery services and quick-service restaurants is further boosting demand. Food brands are also adopting cellulose packaging to enhance brand image and align with sustainability goals.

Market Restraint

Limited Moisture and Heat Resistance Compared to Plastics

One of the key restraints in the thermoformed cellulose packaging market is its relatively limited moisture and heat resistance compared to conventional plastic packaging. While cellulose-based materials perform well in dry applications, they may lose structural integrity when exposed to high humidity, oils, or extreme temperatures.

This limitation restricts their use in certain food and industrial applications, especially where long shelf life or high barrier protection is required. For example, frozen food packaging or liquid-based products often require additional coatings or hybrid materials, which increases production costs and complexity. As a result, some manufacturers hesitate to fully replace plastic packaging, slowing broader adoption in performance-critical segments.

Market Opportunities

Expansion in E-Commerce and Food Delivery Packaging

The rapid growth of e-commerce and food delivery services presents a significant opportunity for thermoformed cellulose packaging. These industries require lightweight, durable, and sustainable packaging solutions for transportation and delivery applications. Cellulose-based trays, inserts, and protective packaging formats are increasingly being used to replace plastic-based materials. The rise of online grocery delivery and meal kit services further supports demand. Companies are also investing in branded sustainable packaging to enhance customer experience and reduce environmental impact.

Innovation in Barrier-Coated Cellulose Materials

The development of barrier-coated cellulose materials presents another major opportunity in the market. Manufacturers are investing in bio-based coatings that improve moisture resistance, grease resistance, and shelf stability. These innovations expand the application scope of thermoformed cellulose packaging into sectors such as frozen foods, dairy products, and cosmetics. As material science advances, cellulose packaging is expected to become more competitive with traditional plastic packaging in performance-sensitive applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.2 Billion |

| Market Size in 2026 | USD 3.6 Billion |

| Market Size in 2034 | USD 8.1 Billion |

| CAGR | 10.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

Thermoformed cellulose trays dominated the market in 2024, accounting for approximately 43% share. Their dominance is driven by widespread use in food service applications such as ready-to-eat meals, airline catering, and institutional food packaging. Trays offer strong structural integrity, lightweight design, and compostability, making them a preferred alternative to plastic-based packaging. They are extensively used by quick-service restaurants and retail food brands that are transitioning toward sustainable packaging formats.

Clamshell packaging is expected to be the fastest-growing subsegment, expanding at a CAGR of 11.8%. Growth is driven by increasing demand from food delivery and takeaway services. These packaging formats provide secure closure, portability, and leak resistance while maintaining eco-friendly properties. Rising adoption in online food delivery platforms and quick-service restaurants is further accelerating demand for molded cellulose clamshell solutions.

By Application

Food packaging dominated the application segment in 2024 with approximately 56% share of the market. The segment benefits from strong demand across restaurants, supermarkets, catering services, and online food delivery platforms. Thermoformed cellulose materials are widely used due to their compostability, safety for direct food contact, and suitability for hot and cold food applications. Increasing sustainability requirements from global food brands are further strengthening this segment.

Electronics packaging is projected to be the fastest-growing application segment, registering a CAGR of 12.6% during the forecast period. Growth is driven by increasing demand for protective, lightweight, and shock-absorbing packaging for sensitive electronic components. Cellulose-based thermoformed packaging is gaining traction as a sustainable alternative to plastic foams and molded plastics used in device protection and transportation.

By End-Use Industry

Food service industry dominated in 2024 with approximately 49% share of the global market. The segment is driven by strong demand from quick-service restaurants, cafés, catering services, and institutional food providers. Thermoformed cellulose packaging is widely adopted due to its compostability, cost efficiency, and suitability for single-use food applications.

E-commerce and retail is expected to be the fastest-growing end-use segment, expanding at a CAGR of 13.0%. Growth is driven by rising online shopping activity and increasing demand for sustainable protective packaging solutions. Companies are shifting toward molded fiber packaging to reduce plastic waste while ensuring product safety during shipping and handling.

Thermoformed Cellulose Packaging Market Segmentations

By Product Type

- Trays

- Clamshells

- Cups & Containers

- Protective Inserts

By Application

- Food Packaging

- Electronics Packaging

- Healthcare Packaging

- Industrial Packaging

By End-Use Industry

- Food Service

- Retail & FMCG

- E-commerce

- Industrial Manufacturing

Regional Analysis

North America

North America accounted for approximately 30% market share in 2025, with a projected CAGR of 10.2% during 2025–2034. The region is supported by strong regulatory pressure against single-use plastics and increasing adoption of sustainable packaging in food service, retail, and e-commerce sectors. Growing consumer preference for eco-friendly materials is also accelerating market penetration across major industries.

The United States dominates the regional market due to large-scale adoption of fiber-based packaging by quick-service restaurants and retail chains. A key growth factor is the increasing shift toward compostable food packaging solutions driven by corporate sustainability commitments and state-level plastic ban regulations.

Europe

Europe held around 35% market share in 2025, with a projected CAGR of 11.3%. The region leads global adoption due to strict environmental regulations, strong recycling infrastructure, and aggressive plastic reduction policies. Demand is high across food packaging, retail, and institutional catering applications.

Germany leads the European market due to its advanced packaging manufacturing base and strong environmental compliance culture. A key growth factor is the enforcement of EU Single-Use Plastics Directive, which is pushing rapid adoption of cellulose-based thermoformed packaging across food service and FMCG sectors.

Asia Pacific

Asia Pacific accounted for approximately 25% market share in 2025, with the highest CAGR of 12.1% during the forecast period. Growth is driven by rapid urbanization, expanding food delivery services, and increasing government initiatives promoting biodegradable packaging alternatives.

China dominates the region due to its large manufacturing base and expanding food packaging industry. A key growth factor is rising government investment in green packaging technologies and increasing restrictions on plastic waste in major urban centers.

Middle East & Africa

The region held approximately 6% market share in 2025, with a projected CAGR of 9.4%. Market growth is supported by rising hospitality industries, expanding tourism, and gradual adoption of sustainable packaging practices in urban centers.

The United Arab Emirates leads the region due to its strong hospitality and food service industry. A key growth factor is increasing demand for eco-friendly packaging in premium restaurants, hotels, and airline catering services.

Latin America

Latin America accounted for approximately 4% market share in 2025, with a projected CAGR of 9.8%. Growth is driven by increasing awareness of sustainable packaging, expansion of food delivery services, and gradual regulatory developments on plastic reduction.

Brazil dominates the regional market due to its large FMCG and food service industry. A key growth factor is growing adoption of biodegradable packaging solutions in retail and restaurant sectors driven by environmental awareness campaigns.

Competitive Landscape

The thermoformed cellulose packaging market is moderately fragmented, with companies focusing on sustainability innovation, production scalability, and material performance enhancement. Competition is driven by advancements in pulp molding technology and bio-based material development.

Huhtamaki is a leading player in the market, known for its strong portfolio of fiber-based packaging solutions. The company recently expanded its molded fiber production capacity in Europe to meet growing demand for sustainable packaging in food service applications.

Key Players List

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- UFP Technologies Inc.

- Sealed Air Corporation

- Brødrene Hartmann A/S

- Eco-Products Inc.

- Fabri-Kal Corporation

- Dart Container Corporation

- Sabert Corporation

- Genpak LLC

- PulpWorks Inc.

- Henry Molded Products Inc.

- EnviroPAK Corporation

- UFP Packaging

- CKF Inc.