Industrial Packaging Recycling Services Market Size and Growth

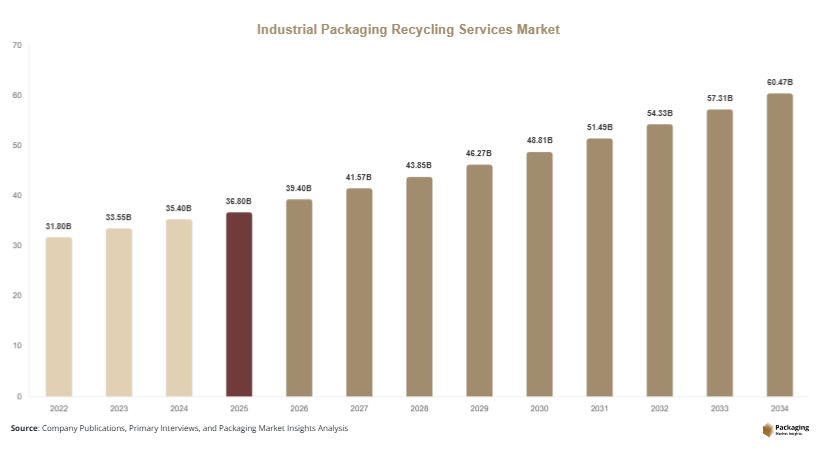

The global industrial packaging recycling services market was valued at USD 36.8 billion in 2025 and is estimated to reach USD 39.4 billion in 2026. The market is projected to reach USD 63.7 billion by 2034, expanding at a CAGR of 5.5% during the forecast period from 2025 to 2034. The market is witnessing steady growth due to increasing industrial waste generation, rising environmental regulations, and growing corporate commitments toward circular economy practices. Industrial packaging recycling services play an essential role in collecting, processing, refurbishing, and reusing industrial packaging materials such as plastic drums, intermediate bulk containers (IBCs), metal containers, wooden pallets, corrugated boxes, and flexible industrial packaging products.

Rapid industrialization and global trade expansion are significantly increasing the demand for sustainable industrial packaging management solutions. Manufacturing, chemicals, food processing, automotive, pharmaceutical, and logistics industries are increasingly focusing on reducing landfill waste and improving packaging reuse rates. Recycling service providers are expanding collection and reprocessing capabilities to support sustainable industrial operations while lowering raw material consumption.

Key Market Insights

- Asia Pacific dominated the market with a 38.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Plastic recycling services led the type segment with a 34.7% share.

- Plastic packaging materials dominated with a 46.9% share.

- Manufacturing applications led the end-use segment with 31.5% share.

- The US remained the dominant country with a market size of USD 8.4 billion in 2025 and USD 9.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Closed-Loop Industrial Packaging Recycling Systems

The industrial packaging recycling services market is increasingly witnessing the adoption of closed-loop recycling systems designed to reduce industrial waste and improve packaging reuse efficiency. Companies across chemicals, food processing, automotive, and pharmaceutical industries are implementing returnable packaging systems where used industrial containers, pallets, and drums are collected, refurbished, and reused multiple times before disposal. This approach helps reduce procurement costs and supports corporate sustainability targets.

Industrial recycling service providers are investing in cleaning, inspection, and refurbishment technologies for reusable packaging products such as intermediate bulk containers and steel drums. Several manufacturing companies in the United States and Germany are partnering with recycling firms to establish regional packaging recovery networks that reduce transportation costs and landfill dependency.

Future market growth is expected to benefit from increasing circular economy initiatives and rising demand for reusable industrial packaging systems. Closed-loop recycling programs are likely to become more common across logistics and manufacturing industries as companies continue focusing on waste reduction and sustainable supply chain management.

Integration of Smart Waste Monitoring and Automated Recycling Technologies

The integration of smart waste monitoring systems and automated recycling technologies is becoming a major trend in the industrial packaging recycling industry. Recycling companies are increasingly deploying AI-based sorting systems, RFID-enabled packaging tracking solutions, and robotic material handling technologies to improve recycling efficiency and reduce operational costs.

Digital tracking systems help companies monitor packaging usage cycles, identify recyclable materials, and optimize waste collection operations. Automated sorting technologies improve recovery rates for plastics, metals, paper, and composite industrial packaging materials. Several recycling facilities across Europe and Asia Pacific are adopting sensor-based waste identification systems capable of separating industrial packaging materials with higher precision than conventional methods.

The long-term impact of this trend is expected to include improved material recovery efficiency, lower recycling contamination rates, and enhanced operational productivity. As industrial sectors increasingly digitalize waste management operations, demand for technology-driven recycling services is likely to expand significantly during the forecast period.

Market Drivers

Rising Environmental Regulations and Sustainability Policies

Increasing environmental regulations related to industrial waste management and packaging disposal are significantly driving the industrial packaging recycling services market. Governments worldwide are implementing strict regulations focused on reducing landfill waste, increasing recycling rates, and promoting sustainable industrial packaging practices. Extended producer responsibility programs are requiring manufacturers and logistics companies to manage industrial packaging waste more effectively.

Industrial companies are increasingly investing in recycling partnerships to comply with waste management laws and sustainability reporting requirements. Recycling service providers are expanding material recovery infrastructure to support industrial customers operating in highly regulated sectors such as chemicals, pharmaceuticals, and food processing.

For example, several European countries have introduced strict industrial packaging recovery targets for plastics and metal containers. In North America, manufacturing companies are increasingly using recycled industrial packaging materials to reduce environmental impact and improve sustainability performance. The growing regulatory focus on industrial waste reduction is expected to remain a major growth driver throughout the forecast period.

Expansion of Industrial Manufacturing and Logistics Activities

Rapid expansion of industrial manufacturing and global logistics operations is another major factor driving market growth. Manufacturing industries generate substantial volumes of industrial packaging waste, including drums, pallets, corrugated packaging, shrink films, and bulk containers. Recycling service providers are increasingly offering collection, refurbishment, and material recovery solutions to industrial customers seeking efficient waste management systems.

Growth in international trade and warehousing activities is also contributing to rising demand for reusable industrial packaging products. Logistics companies are focusing on recycling and reconditioning programs to reduce packaging procurement costs and improve transportation efficiency.

Several automotive and consumer goods manufacturers across Asia Pacific are implementing industrial packaging reuse systems for supply chain operations. Food processing companies are additionally investing in recyclable transport packaging and pallet recovery programs. Continued expansion of manufacturing infrastructure and industrial distribution networks is expected to strengthen long-term demand for industrial packaging recycling services globally.

Market Restraint

High Operational Costs and Complex Waste Segregation Processes

High operational costs and complex waste segregation requirements remain major restraints for the industrial packaging recycling services market. Industrial packaging recycling operations require significant investment in transportation, sorting equipment, cleaning facilities, labor, and material processing infrastructure. Recycling industrial packaging materials is often more complicated than standard consumer waste recycling because industrial packaging frequently contains hazardous residues, mixed materials, or contamination from chemicals and industrial products.

Packaging materials such as multilayer plastics, coated packaging products, and contaminated industrial containers require specialized recycling procedures that increase operational costs. Recycling providers must additionally comply with environmental safety standards related to hazardous material handling and waste disposal.

For example, chemical and pharmaceutical packaging recycling operations require extensive cleaning and inspection procedures before materials can be reused or recycled. Smaller recycling providers in developing regions may face challenges related to limited recycling infrastructure and fluctuating recycled material prices. Transportation costs for collecting used industrial packaging from multiple industrial facilities can further affect profitability.

These factors may slow market expansion in cost-sensitive regions and limit recycling adoption among smaller manufacturing companies. However, ongoing investment in automation and digital waste management technologies is expected to gradually improve recycling efficiency and reduce operational costs during the forecast period.

Market Opportunities

Expansion of Reusable Industrial Packaging Programs

The growing adoption of reusable industrial packaging programs presents significant opportunities for market expansion. Industrial sectors are increasingly shifting from single-use packaging products toward reusable transport packaging systems designed to reduce waste generation and improve cost efficiency. Reusable pallets, containers, metal drums, and bulk packaging systems are gaining popularity across logistics, automotive, and manufacturing industries.

Recycling service providers are expanding refurbishment and reconditioning capabilities to support reuse-oriented packaging systems. Companies are increasingly implementing packaging return programs where industrial packaging products are collected, inspected, repaired, and redistributed for repeated use. This approach supports circular economy goals while lowering raw material consumption.

Several automotive manufacturers and retail distribution companies in Europe and North America are expanding reusable packaging networks across supply chains. Future opportunities are expected in smart packaging tracking systems, reusable plastic container management, and industrial pallet recovery solutions supporting sustainable industrial logistics operations.

Rising Investment in Advanced Plastic Recycling Infrastructure

Increasing investment in advanced plastic recycling technologies is creating strong opportunities within the industrial packaging recycling services market. Industrial packaging industries generate large volumes of plastic waste, including shrink films, bulk containers, industrial wraps, and transport packaging products. Recycling companies are increasingly investing in mechanical and chemical recycling systems capable of processing industrial plastic waste more efficiently.

Advanced recycling technologies allow recovery of higher-quality recycled plastic materials suitable for reuse in industrial packaging applications. Several recycling firms are establishing specialized industrial plastic recovery facilities designed to process contaminated and mixed plastic packaging materials.

For example, companies across Asia Pacific and Europe are investing in plastic-to-plastic recycling systems supporting circular packaging production. Future market opportunities are expected in recycled resin production, industrial packaging material recovery partnerships, and AI-powered waste sorting systems. Rising demand for recycled plastics within manufacturing industries is likely to support long-term investment in industrial packaging recycling infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36.8 Billion |

| Market Size in 2026 | USD 39.4 Billion |

| Market Size in 2034 | USD 63.7 Billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic recycling services dominated the industrial packaging recycling services market in 2024 with a market share of 34.7%. Industrial sectors generate substantial volumes of plastic packaging waste, including shrink wraps, industrial films, bulk containers, and plastic drums. Recycling service providers are increasingly investing in plastic collection, cleaning, and reprocessing systems to meet rising demand for recycled industrial plastics. Manufacturing and logistics industries are using recycled plastics in transport packaging and storage applications to reduce environmental impact and raw material costs. Several industrial packaging companies across North America and Europe are implementing closed-loop plastic recovery systems for reusable packaging products. Growth in industrial warehousing and export logistics activities continues supporting demand for industrial plastic recycling services globally.

Metal packaging recycling services are projected to witness the fastest CAGR of 6.6% during the forecast period due to increasing demand for reusable steel drums, aluminum containers, and industrial metal packaging products. Metal packaging recycling offers high material recovery value and supports long-term reuse applications across chemicals, food processing, and automotive industries. Recycling providers are increasingly expanding drum refurbishment and metal recovery operations to improve industrial packaging sustainability. Several chemical manufacturers are implementing returnable steel drum systems designed for repeated industrial use. Future market growth is expected to benefit from rising industrial metal recovery investments, expansion of reusable transport packaging systems, and increasing demand for recycled metal packaging materials across manufacturing sectors.

By Material

Plastic packaging materials accounted for the largest market share of 46.9% in 2024 due to widespread industrial usage of plastic containers, films, wraps, and transport packaging products. Plastic packaging materials are extensively used across chemicals, food processing, pharmaceuticals, electronics, and logistics industries because of their lightweight structure, durability, and cost efficiency. Recycling service providers are increasingly expanding industrial plastic recovery systems to process growing volumes of packaging waste generated by industrial operations. Several recycling facilities are investing in automated plastic sorting technologies and recycled resin production infrastructure to improve processing efficiency. Industrial companies are additionally adopting reusable plastic containers and pallets to reduce packaging procurement costs and improve sustainability performance. The rapid expansion of industrial manufacturing activities continues supporting segment dominance globally.

Paper-based industrial packaging materials are expected to witness the fastest CAGR of 6.1% during the forecast period due to increasing demand for recyclable and biodegradable transport packaging solutions. Corrugated boxes, paper pallets, kraft packaging materials, and protective paper wraps are increasingly replacing plastic packaging products across industrial logistics operations. Recycling providers are expanding paper recovery and fiber processing infrastructure to support sustainable industrial packaging demand. Several retail distribution and e-commerce companies are adopting recyclable paper transport packaging systems to reduce environmental impact. Future growth opportunities are expected in recycled corrugated packaging production, industrial fiber recovery systems, and sustainable paper packaging innovations supporting circular economy initiatives.

By End-Use

Manufacturing applications dominated the industrial packaging recycling services market in 2024 with a market share of 31.5%. Manufacturing industries generate large volumes of industrial packaging waste, including pallets, drums, corrugated packaging, protective films, and bulk transport containers. Recycling providers are increasingly offering packaging collection, refurbishment, and recovery services to manufacturing companies seeking cost-efficient waste management solutions. Automotive, electronics, machinery, and consumer goods manufacturers are implementing reusable transport packaging systems to reduce packaging procurement costs and improve operational sustainability. Several manufacturing facilities across Asia Pacific and Europe are adopting industrial packaging reuse programs supported by automated recycling and material recovery infrastructure. Expansion of industrial production activities continues strengthening demand for recycling services within manufacturing operations worldwide.

Pharmaceutical applications are projected to register the fastest CAGR of 6.7% during the forecast period due to increasing pharmaceutical production and rising demand for safe packaging waste management systems. Pharmaceutical companies use substantial volumes of plastic containers, corrugated packaging, protective films, and transport packaging products within supply chain operations. Recycling providers are increasingly offering specialized pharmaceutical packaging recovery services that comply with strict hygiene and environmental standards. Several pharmaceutical manufacturers are investing in recyclable packaging systems and reusable transport containers to improve sustainability performance. Future market growth is expected to benefit from expansion of pharmaceutical exports, growth in temperature-controlled logistics operations, and increasing adoption of sustainable healthcare packaging systems globally.

Industrial Packaging Recycling Services Market Segmentations

By Type

- Plastic Recycling Services

- Metal Packaging Recycling Services

- Paper & Corrugated Packaging Recycling Services

- Wooden Packaging Recycling Services

By Material

- Plastic Packaging Materials

- Metal Packaging Materials

- Paper-Based Packaging Materials

- Wooden Packaging Materials

By End-User

- Manufacturing

- Chemicals

- Food & Beverage

- Pharmaceuticals

- Logistics & Warehousing

Regional Analysis

North America

North America accounted for 27.8% of the global industrial packaging recycling services market share in 2025 and is projected to grow at a CAGR of 5.2% during the forecast period. The region benefits from advanced recycling infrastructure, strict environmental regulations, and strong adoption of sustainable industrial packaging practices. Manufacturing, chemicals, food processing, and logistics industries are increasingly implementing industrial packaging recovery and reuse programs to reduce waste disposal costs and improve sustainability performance. Recycling service providers are expanding regional collection and refurbishment operations for industrial drums, pallets, and bulk containers. The increasing focus on landfill diversion and recycled material usage is also supporting market growth across the United States and Canada.

The United States remained the dominant country in North America due to its extensive industrial manufacturing base and strong investment in recycling technologies. One important growth driver is the increasing adoption of reusable transport packaging systems within automotive and logistics industries. Several U.S. companies are implementing pallet recovery and industrial container refurbishment programs to reduce procurement costs and improve packaging lifecycle management. Canada is additionally witnessing rising demand for industrial plastic recycling services and paper packaging recovery systems. Expansion of sustainable warehousing and industrial distribution infrastructure continues supporting regional market growth.

Europe

Europe represented 25.6% of the global industrial packaging recycling services market share in 2025 and is expected to expand at a CAGR of 5.4% through 2034. The region continues benefiting from strict packaging waste directives, circular economy initiatives, and growing industrial sustainability investments. Industrial companies across Germany, France, Italy, and the United Kingdom are increasingly collaborating with recycling providers to improve packaging recovery rates and reduce environmental impact.

Germany emerged as the dominant country in Europe because of its advanced recycling systems and strong industrial packaging regulations. One unique growth driver is the rapid expansion of industrial packaging take-back programs within the chemicals and automotive sectors. German manufacturers are increasingly using reusable metal drums and returnable transport packaging systems to reduce waste generation. France and the Netherlands are additionally investing in smart waste tracking technologies and industrial plastic recovery infrastructure. Rising demand for recycled industrial packaging materials continues strengthening market growth across the European manufacturing sector.

Asia Pacific

Asia Pacific dominated the industrial packaging recycling services market with a 38.2% share in 2025 and is forecast to register a CAGR of 5.9% during the forecast period. Rapid industrialization, rising export activities, and growing manufacturing investments are major growth factors supporting regional market expansion. Countries such as China, Japan, India, and South Korea are witnessing increasing demand for industrial packaging recycling and refurbishment services across automotive, electronics, food processing, and pharmaceutical industries.

China remained the dominant country within the region due to large-scale manufacturing operations and increasing government focus on industrial waste reduction. One important growth driver is the rapid expansion of industrial plastic recycling infrastructure designed to support sustainable manufacturing activities. Chinese recycling companies are investing in automated sorting systems and recycled resin production facilities to improve industrial packaging recovery efficiency. Japan is also focusing on reusable industrial container systems and advanced material recovery technologies. India continues witnessing rising investment in industrial waste collection networks and packaging refurbishment operations driven by expanding manufacturing output.

Middle East & Africa

The Middle East & Africa accounted for 3.9% of the global industrial packaging recycling services market share in 2025 and is projected to grow at a CAGR of 4.8% through 2034. The market is gradually expanding due to increasing industrialization, rising sustainability awareness, and growing investment in waste management infrastructure across Gulf countries and South Africa. Industrial packaging recycling demand is increasing within oil & gas, chemicals, food processing, and logistics industries.

Saudi Arabia remained the dominant country in the region because of ongoing industrial diversification initiatives and expanding manufacturing infrastructure. One major growth driver is the increasing focus on industrial waste reduction within petrochemical and logistics operations. Recycling companies are increasingly providing drum cleaning, pallet recovery, and industrial plastic recycling services to large industrial facilities. The United Arab Emirates is additionally investing in smart recycling infrastructure and sustainable logistics programs. South Africa continues witnessing gradual growth in industrial paper packaging recovery and pallet refurbishment services.

Latin America

Latin America held 4.5% of the global industrial packaging recycling services market share in 2025 and is projected to witness the fastest CAGR of 6.4% during the forecast period. Rising manufacturing activities, growing export trade, and increasing environmental regulations are supporting regional market growth. Countries such as Brazil, Mexico, Argentina, and Chile are increasingly investing in industrial waste management and packaging recovery systems.

Brazil emerged as the dominant country within Latin America due to expanding food processing, agriculture, and automotive industries. One important growth driver is the increasing demand for reusable transport packaging systems within industrial logistics operations. Brazilian recycling companies are expanding pallet refurbishment and industrial plastic recovery services to support growing manufacturing and export activities. Mexico is also witnessing rising investment in corrugated packaging recycling and industrial waste segregation infrastructure. Government initiatives focused on reducing industrial landfill waste continue supporting long-term regional market development.

Competitive Landscape

The industrial packaging recycling services market is moderately consolidated with the presence of global waste management companies, industrial recycling providers, packaging recovery firms, and logistics support companies focusing on circular economy solutions and industrial waste reduction services.

Veolia is considered one of the leading companies in the market due to its strong global recycling infrastructure and industrial waste management capabilities. The company continues expanding industrial packaging recovery and plastic recycling operations across North America and Europe.

Waste Management Inc. focuses on industrial packaging recycling and landfill diversion services supported by automated material recovery technologies. Republic Services is investing in industrial waste sorting and plastic recycling infrastructure across the United States. SUEZ continues strengthening industrial recycling partnerships and circular packaging recovery programs across Europe and Asia Pacific. Clean Harbors focuses on industrial container cleaning, drum recycling, and hazardous packaging waste management services.

Companies are increasingly investing in AI-powered recycling systems, reusable industrial packaging networks, and sustainable material recovery technologies to strengthen market competitiveness and improve operational efficiency.

Key Players List

- Veolia

- Waste Management Inc.

- Republic Services

- SUEZ

- Clean Harbors

- Stericycle

- Biffa

- DS Smith Plc

- Remondis SE & Co. KG

- Tomra Systems

- Waste Connections

- FCC Environment

- Renewi plc

- Scholz Recycling GmbH

- Casella Waste Systems