Transfer Molded Pulp Packaging Market Size and Growth

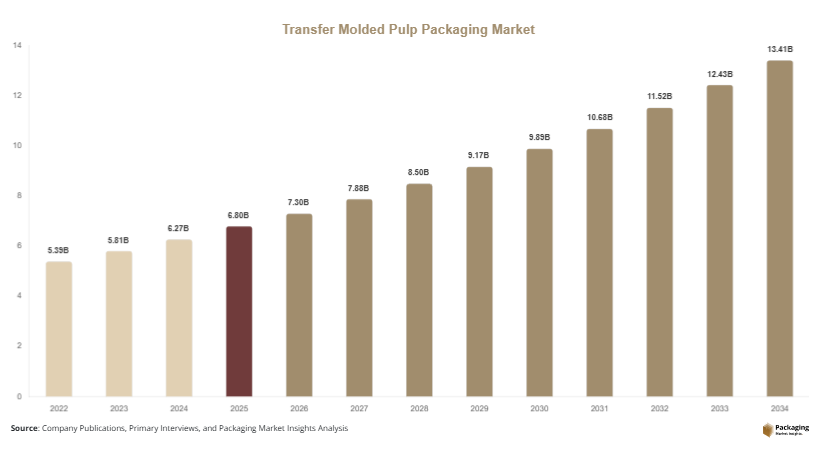

The global transfer molded pulp packaging market size is estimated at USD 6.8 billion in 2025 and is projected to reach USD 7.3 billion in 2026. By 2034, the market is expected to reach approximately USD 13.9 billion, growing at a CAGR of 7.9% during the forecast period (2025–2034). The transfer molded pulp packaging market is expected to show steady expansion between 2025 and 2034, driven by sustainability regulations, packaging innovation, and increasing demand from multiple end-use industries.

One of the primary growth factors is the global shift toward eco-friendly packaging materials. Companies are actively replacing plastic-based protective packaging with molded pulp alternatives to reduce carbon emissions and meet ESG targets. Another key factor is the expansion of e-commerce logistics networks, where molded pulp packaging is widely used for cushioning and product protection. Additionally, technological advancements in high-precision molding processes are enabling complex shapes and improved structural integrity.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Protective molded pulp inserts led the type segment with a 32.1% share.

- Recycled paper pulp dominated with a 58.6% share.

- Electronics & consumer goods led the segment with 44.3% share.

- The US remained the dominant country with a market size of USD 6.1 billion in 2025 and USD 6.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Plastic-Free Protective Packaging Solutions

A major trend in the transfer molded pulp packaging market is the replacement of plastic foam and plastic inserts with molded fiber alternatives. Industries such as electronics, automotive components, and cosmetics are rapidly transitioning to molded pulp due to regulatory pressure and sustainability commitments. For example, smartphone manufacturers are increasingly using molded pulp trays instead of plastic clamshell packaging to protect devices during shipment. This transition is particularly strong in Europe, where plastic bans are strict. In the future, improvements in coating technologies will enhance moisture resistance, enabling molded pulp to replace plastic in more demanding environments such as frozen food packaging.

Innovation in High-Strength and Premium Molded Pulp Designs

Another key trend is the development of high-strength molded pulp packaging with improved surface finishing. Manufacturers are introducing advanced molding techniques that allow sharper edges, smoother surfaces, and higher load-bearing capacity. This is enabling molded pulp packaging to enter premium segments such as luxury cosmetics and electronics retail packaging. For instance, high-end perfume brands are adopting molded pulp inserts with embossed branding. In the future, integration of hybrid fiber composites and water-resistant coatings is expected to expand applications into industrial and pharmaceutical packaging.

Market Drivers

Rising Environmental Regulations Against Plastic Packaging

One of the strongest drivers is the global enforcement of regulations restricting plastic packaging usage. Governments are banning expanded polystyrene (EPS) and non-recyclable plastics, pushing industries toward biodegradable alternatives like molded pulp. For example, several countries in Europe have implemented strict packaging waste directives that encourage recyclable fiber-based materials. This has significantly increased demand from food delivery, electronics, and retail sectors. The cause-effect relationship is clear: stricter regulations lead to increased substitution of plastic with molded pulp solutions, driving market expansion.

Growth of E-commerce and Fragile Goods Transportation

The expansion of e-commerce has significantly increased the need for protective packaging solutions. Transfer molded pulp packaging is widely used for cushioning fragile goods such as electronics, glassware, and cosmetics. For example, global e-commerce platforms use molded pulp inserts to ensure product safety during long-distance shipping. The increasing volume of cross-border trade and logistics complexity is further strengthening demand. As e-commerce continues to grow globally, molded pulp packaging is expected to become a standard solution for protective packaging.

Market Restraint

Limited Water Resistance and Structural Constraints

A key restraint in the transfer molded pulp packaging market is its limited resistance to moisture and structural deformation under extreme conditions. Although advancements have improved durability, molded pulp still faces challenges in high-humidity environments and long-term storage applications. For example, in tropical regions, food packaging using molded pulp may require additional coatings to prevent moisture absorption. This increases production cost and reduces competitiveness compared to plastic-based alternatives. As a result, some industries remain cautious in adopting molded pulp packaging for high-moisture or heavy-duty applications.

Market Opportunities

Expansion in Food Service and Quick Commerce Packaging

The growing food delivery and quick commerce industry presents a major opportunity for molded pulp packaging. Restaurants and QSR chains are increasingly adopting molded pulp trays, containers, and cup holders as sustainable alternatives to plastic packaging. For example, several global fast-food chains have introduced molded fiber packaging for takeaway meals. This trend is expected to expand further as consumer demand for eco-friendly food packaging increases. In the future, heat-resistant and grease-resistant pulp innovations will unlock wider adoption across hot and cold food delivery applications.

Growth in Electronics and Industrial Protective Packaging

Another significant opportunity lies in the electronics and industrial sectors. Molded pulp packaging is widely used for protecting fragile electronic components during transportation. For example, laptop manufacturers use molded pulp inserts for internal cushioning of devices. The increasing production of consumer electronics in Asia is expected to further boost demand. In the future, customized molded pulp designs with anti-static properties will enhance adoption in high-tech industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.8 Billion |

| Market Size in 2026 | USD 7.3 Billion |

| Market Size in 2034 | USD 13.9 Billion |

| CAGR | 7.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Protective inserts accounted for 36.2% market share in 2024 due to their extensive use in electronics and fragile goods packaging. These inserts are designed to absorb shocks and prevent damage during transportation. For example, smartphone and laptop manufacturers widely use molded pulp inserts for internal cushioning.

Custom molded packaging is expected to grow at a CAGR of 7.4% due to increasing demand for brand-specific packaging designs. Companies are adopting customized shapes for premium product presentation and improved logistics efficiency.

By Material

Recycled paper pulp held 58.6% market share in 2024 due to its availability and low cost. It is widely used in standard packaging applications across industries.

Agricultural fiber pulp is expected to grow at a CAGR of 6.8% due to sustainability trends and availability of raw materials like bagasse and wheat straw.

By End-Use

This segment accounted for 44.3% market share in 2024 due to high demand for protective packaging in electronics shipments.

Food service packaging is expected to grow at a CAGR of 7.2% due to rising adoption of eco-friendly takeaway packaging.

Transfer Molded Pulp Packaging Market Segmentations

By Type

- Protective Inserts

- End Caps

- Clamshell Packaging

- Custom Molded Packaging

By Material

- Recycled Paper Pulp

- Kraft Pulp

- Agricultural Fiber Pulp

- Hybrid Fiber Materials

By End-Use

- Electronics & Consumer Goods

- Food Service Packaging

- Healthcare & Pharmaceuticals

- Automotive Components

- Retail & E-commerce

Regional Analysis

North America

North America accounted for 28.9% of the transfer molded pulp packaging market in 2025 and is projected to grow at a CAGR of 7.5% through 2034. The region is driven by strong demand from e-commerce, electronics, and food delivery industries. Sustainability regulations and corporate ESG commitments are encouraging rapid adoption of molded fiber packaging solutions. Growth is also supported by consumer preference for eco-friendly packaging formats.

The United States dominates the region due to its large logistics and retail infrastructure. A key driver is the expansion of e-commerce packaging demand, particularly for electronics and fragile goods. For example, major U.S. retailers are transitioning from plastic foam to molded pulp inserts in shipping operations to reduce environmental impact.

Europe

Europe held 26.4% market share in 2025 and is expected to grow at a CAGR of 8.1% through 2034. The region is highly influenced by strict environmental regulations and circular economy policies. Demand for biodegradable packaging is strong across food, cosmetics, and electronics sectors.

Germany leads the regional market due to its advanced manufacturing capabilities and strong sustainability focus. A key driver is the widespread adoption of plastic bans, which has accelerated molded pulp substitution in retail packaging. For example, French cosmetic brands are increasingly using molded fiber trays for luxury product packaging.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is expected to grow at a CAGR of 8.7% through 2034. Rapid industrialization, expanding e-commerce platforms, and low-cost manufacturing capabilities are key drivers. The region also benefits from strong demand in electronics production.

China is the dominant country due to its large electronics manufacturing ecosystem. A key driver is the integration of molded pulp packaging in export-oriented electronics shipments. India is also emerging as a strong market due to rising food delivery services and sustainable packaging initiatives.

Middle East & Africa

Middle East & Africa accounted for 4.9% market share in 2025 and is projected to grow at a CAGR of 6.4% through 2034. Growth is driven by retail expansion, tourism, and increasing environmental awareness. Food service packaging is a key application segment.

The United Arab Emirates leads the region due to strong hospitality and retail industries. A key driver is the adoption of sustainable food packaging in hotels and restaurants, particularly in Dubai’s premium dining sector.

Latin America

Latin America held 7.4% market share in 2025 and is projected to grow at a CAGR of 6.2% through 2034. Economic development, urbanization, and expanding retail sectors are driving demand for molded pulp packaging.

Brazil dominates the region due to its large food and beverage industry. A key driver is the growing adoption of eco-friendly packaging in food delivery services. Mexico also contributes significantly due to expanding electronics assembly operations.

Competitive Landscape

The transfer molded pulp packaging market is moderately consolidated with key players focusing on sustainability, capacity expansion, and product innovation. Major companies include Huhtamaki Oyj, UFP Technologies, Inc., Pactiv Evergreen Inc., Henry Molded Products, and Brødrene Hartmann A/S. Huhtamaki Oyj is a leading player due to its strong global presence and advanced molded fiber technology capabilities.

Companies are investing in automation, R&D for water-resistant pulp materials, and expansion into emerging markets. Strategic partnerships with e-commerce and food service companies are also increasing.

Key Players

- Huhtamaki Oyj

- UFP Technologies, Inc.

- Pactiv Evergreen Inc.

- Brødrene Hartmann A/S

- Henry Molded Products Inc.

- CKF Inc.

- Protopak Engineering Corp.

- EnviroPAK Corporation

- Keiding, Inc.

- FiberCel Packaging LLC

- Nippon Molded Fiber Co.

- Taiwan Pulp Molding Co.

- Sabert Corporation

- Genpak LLC

- Sonoco Products Company