Steel Drums Market Size and Growth

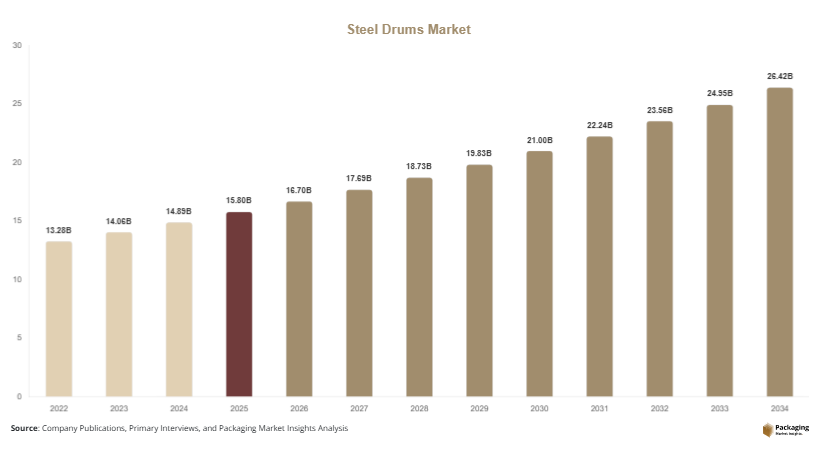

The global steel drums market size was valued at USD 15.8 billion in 2025 and is projected to reach USD 16.7 billion in 2026. By 2034, the market is forecast to attain approximately USD 26.4 billion, registering a CAGR of 5.9% during 2025–2034. Rising industrial production, increasing cross-border transportation of chemicals, and growing adoption of recyclable packaging materials are among the primary factors supporting market growth.

The steel drums market continues to play a critical role in global industrial packaging due to its durability, reusability, high load-bearing capacity, and ability to safely transport hazardous and non-hazardous materials. Steel drums are widely used across chemicals, petroleum products, food ingredients, pharmaceuticals, paints, lubricants, and industrial manufacturing sectors. As supply chains become increasingly globalized, demand for reliable bulk packaging solutions has strengthened, supporting the market's long-term expansion.

Key Highlights

- Asia Pacific dominated the market with a 38.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.5%.

- Tight Head Drums led the type segment with a 42.8% share.

- Carbon Steel dominated the material segment with a 74.1% share.

- Chemicals applications led the end-use segment with 45.3% share.

- The US remained the dominant country with a market size of USD 2.9 billion in 2025 and USD 3.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Reconditioned Steel Drums

Sustainability initiatives are driving demand for reconditioned steel drums across industrial supply chains. Companies are increasingly adopting circular economy practices to reduce packaging waste and lower environmental impact. Reconditioned drums undergo cleaning, inspection, and refurbishment processes before re-entering the market, helping organizations reduce packaging costs while complying with environmental regulations. Chemical manufacturers and lubricant suppliers are among the largest users of reconditioned drums. Future market growth is expected to be supported by expanding refurbishment infrastructure and rising investments in closed-loop packaging systems. The trend is particularly visible in developed economies where sustainability reporting and waste reduction targets influence procurement decisions.

Integration of Smart Tracking and Supply Chain Monitoring

The adoption of digital technologies in industrial packaging is creating opportunities for smart steel drum solutions. Manufacturers are incorporating RFID tags, QR codes, and IoT-enabled monitoring systems into drum packaging to improve inventory visibility and traceability. For example, logistics companies transporting hazardous chemicals increasingly use digitally tracked drums to monitor movement and ensure compliance with safety standards. Smart packaging solutions help reduce product loss, improve warehouse efficiency, and support regulatory reporting. As industrial supply chains become more digitized, demand for connected steel drums is expected to increase significantly throughout the forecast period.

Market Drivers

Growth of the Global Chemical Industry

The expansion of chemical manufacturing activities worldwide remains a primary driver for the steel drums market. Chemicals require secure packaging solutions capable of handling corrosive, hazardous, and sensitive materials during transportation and storage. Steel drums provide high structural integrity and comply with international transportation regulations. As emerging economies continue expanding petrochemical and specialty chemical production facilities, demand for industrial packaging solutions rises accordingly. For example, increasing exports of industrial chemicals from Asia-Pacific countries have generated significant demand for steel drums used in international shipping operations. This direct relationship between chemical production and industrial packaging demand continues to support market growth.

Rising Demand for Bulk Industrial Packaging

Industrial sectors increasingly require packaging formats that can safely transport large quantities of liquids and powders. Steel drums offer durability, stackability, and resistance to external damage, making them suitable for bulk transportation applications. Industries such as lubricants, paints, coatings, food ingredients, and pharmaceuticals rely on steel drums to minimize product losses during handling and shipping. Growth in global manufacturing activities has increased demand for bulk logistics solutions, creating favorable conditions for steel drum manufacturers. As industrial output expands across both developed and emerging markets, demand for heavy-duty packaging formats is expected to remain strong.

Market Restraint

Volatility in Raw Material Prices

Fluctuations in steel prices represent a major challenge for market participants. Steel drum manufacturing relies heavily on steel sheet availability and pricing stability. Changes in global steel supply, trade restrictions, energy costs, and geopolitical factors can significantly impact production expenses. When steel prices increase rapidly, manufacturers face margin pressures that may reduce profitability or lead to higher product prices. Such increases can encourage customers to evaluate alternative packaging materials such as plastic drums or intermediate bulk containers.

For example, periods of elevated steel costs have prompted certain chemical distributors to diversify packaging strategies and reduce dependence on steel-based containers. Smaller manufacturers are particularly vulnerable because they often have limited purchasing power compared to larger industry players. Furthermore, unpredictable raw material pricing complicates long-term contract negotiations and production planning. Although demand fundamentals remain positive, steel price volatility continues to create operational and financial challenges throughout the value chain.

Market Opportunities

Expansion of Pharmaceutical Manufacturing

The growing pharmaceutical industry presents significant opportunities for steel drum suppliers. Pharmaceutical manufacturers increasingly require secure bulk packaging solutions for active pharmaceutical ingredients, solvents, and intermediate compounds. Steel drums offer contamination resistance and compliance with stringent regulatory requirements. Expansion of pharmaceutical production facilities across North America, Europe, and Asia-Pacific is expected to create additional demand for specialized drum packaging. Future opportunities are likely to emerge from biologics manufacturing and advanced pharmaceutical ingredient transportation, where high-quality packaging standards remain essential.

Increasing Demand for Hazardous Material Transportation

Growing international trade in hazardous chemicals and industrial materials is creating opportunities for certified steel drum products. Governments and regulatory agencies continue strengthening transportation standards for dangerous goods, increasing demand for UN-certified packaging solutions. Steel drums are widely recognized for their ability to safely contain hazardous substances while minimizing leakage risks. Future applications are expected to include specialty chemicals, battery materials, industrial solvents, and energy-sector products. Companies capable of offering advanced safety features and regulatory compliance certifications are likely to benefit from expanding market opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.8 Billion |

| Market Size in 2026 | USD 16.7 Billion |

| Market Size in 2034 | USD 26.4 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Tight Head Drums dominated the market in 2024, accounting for approximately 42.8% share. These drums are widely used for transporting liquids, chemicals, oils, and hazardous materials due to their leak-resistant design. Industries favor tight head drums because they provide enhanced safety and regulatory compliance. Their durability and ability to withstand demanding transportation conditions contribute to their extensive adoption. Growing chemical exports and increasing industrial production continue supporting demand for this segment.

Stainless Steel Drums represent the fastest-growing type segment and are projected to expand at a CAGR of 6.8% through 2034. Growth is driven by increasing demand for high-purity packaging solutions across pharmaceutical, food, and specialty chemical industries. Stainless steel offers corrosion resistance, long service life, and contamination prevention benefits. As industries adopt higher-quality packaging standards and focus on reusable solutions, demand for stainless steel drums is expected to accelerate significantly.

By Material

Carbon Steel held the largest market share of approximately 74.1% in 2024. Carbon steel remains the preferred material because of its strength, affordability, and suitability for industrial transportation applications. Manufacturers utilize carbon steel drums across chemicals, lubricants, coatings, and petroleum products. The material provides excellent structural performance while maintaining cost efficiency. Large-scale industrial operations continue to rely heavily on carbon steel drums for bulk packaging requirements.

Stainless Steel is projected to be the fastest-growing material segment, expanding at a CAGR of 6.4%. Demand is rising because industries increasingly require corrosion-resistant and reusable packaging solutions. Pharmaceutical manufacturing, specialty chemicals, and food ingredient transportation are key application areas. Future growth is expected to be supported by stricter quality standards and increasing investments in premium industrial packaging solutions.

By End-Use

Chemicals dominated the end-use segment with approximately 45.3% market share in 2024. Chemical manufacturers depend on steel drums for the safe transportation and storage of hazardous and non-hazardous substances. Regulatory requirements, product safety concerns, and export activities contribute to strong demand. The segment benefits from ongoing growth in petrochemicals, industrial chemicals, and specialty chemicals worldwide.

Pharmaceuticals represent the fastest-growing end-use segment, projected to register a CAGR of 6.9% through 2034. Rising pharmaceutical production, expanding biologics manufacturing, and increasing global healthcare investments are driving demand. Steel drums offer reliable protection for pharmaceutical intermediates and raw materials. As drug manufacturing capacity expands globally, pharmaceutical applications are expected to become an increasingly important source of market growth.

Steel Drums Market Segmentations

By Type

- Tight Head Drums

- Open Head Drums

- Composite Steel Drums

- Specialty Steel Drums

By Capacity

- Up to 100 Liters

- 100–250 Liters

- Above 250 Liters

By End-User

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals

- Paints & Coatings

- Oil & Lubricants

- Agriculture

- Others

Regional Analysis

North America

North America accounted for approximately 26.8% of the steel drums market share in 2025 and is projected to expand at a CAGR of 5.6% through 2034. The region benefits from strong chemical manufacturing, oil refining activities, and advanced industrial logistics networks. Demand for steel drums remains steady across lubricant, petrochemical, and industrial chemical applications. Sustainability initiatives encouraging reusable industrial packaging further support market growth. Growing investments in manufacturing reshoring projects and expanding industrial production capacity are expected to contribute to long-term demand across the United States and Canada.

The United States dominates the regional market due to its extensive chemical production base and industrial exports. A unique growth driver is the country's strong hazardous material transportation sector. Industrial manufacturers increasingly require UN-certified steel drums to meet stringent transportation regulations. Recent investments in specialty chemical manufacturing facilities have increased demand for industrial packaging solutions. The ongoing modernization of logistics and warehouse infrastructure also supports the adoption of advanced steel drum technologies.

Europe

Europe held approximately 24.6% market share in 2025 and is anticipated to register a CAGR of 5.4% during the forecast period. The region's mature industrial base, strong environmental regulations, and extensive recycling infrastructure support steel drum consumption. Chemical production hubs across Germany, France, and the Netherlands continue generating demand for bulk packaging solutions. Circular economy policies encourage drum refurbishment and reuse, creating additional market opportunities for service providers and manufacturers throughout the region.

Germany remains the dominant country within Europe. A unique growth driver is the country's emphasis on industrial sustainability and closed-loop packaging systems. German manufacturers increasingly use reconditioned steel drums to reduce environmental impact and comply with waste management regulations. Recent industrial collaborations focused on packaging reuse programs demonstrate the growing importance of sustainable packaging strategies across European supply chains.

Asia Pacific

Asia Pacific led the global market with a 38.2% share in 2025 and is forecast to expand at a CAGR of 6.3% through 2034. Rapid industrialization, rising exports, and growing chemical production capacities continue to drive regional demand. Countries across the region are investing heavily in manufacturing infrastructure and industrial logistics. Expanding petrochemical facilities and increasing industrial output create strong demand for durable packaging formats capable of supporting large-scale transportation operations.

China dominates the Asia Pacific market due to its extensive manufacturing ecosystem and chemical export industry. A unique growth driver is the expansion of specialty chemical exports serving global markets. Chinese manufacturers increasingly require industrial packaging solutions capable of meeting international transportation standards. Growth in export-oriented production facilities and industrial clusters is expected to sustain long-term demand for steel drums throughout the forecast period.

Middle East & Africa

The Middle East & Africa represented approximately 5.8% of the global market in 2025 and is expected to grow at a CAGR of 5.7%. The region benefits from expanding petrochemical production and energy-sector investments. Demand for steel drums is supported by oil-related industries, industrial chemicals, and infrastructure development activities. Several countries are investing in downstream petrochemical manufacturing, creating additional opportunities for industrial packaging suppliers and logistics providers.

Saudi Arabia is the dominant country in the region. A unique growth driver is the expansion of petrochemical diversification projects aimed at increasing value-added industrial output. Large-scale industrial investments continue generating demand for secure packaging solutions. The development of integrated industrial zones and export-oriented chemical facilities is expected to support long-term steel drum consumption across the country.

Latin America

Latin America accounted for approximately 4.6% market share in 2025 and is projected to register the fastest CAGR of 6.5% during the forecast period. Growth is supported by expanding agricultural chemical production, industrial manufacturing, and regional trade activities. Increasing exports of chemicals, coatings, and industrial products require durable packaging solutions that can withstand long-distance transportation. Investments in logistics infrastructure are further supporting market development.

Brazil remains the leading country within Latin America. A unique growth driver is the expansion of the agricultural chemicals sector, which relies heavily on steel drums for safe transportation and storage. Growing demand for crop protection products and industrial chemicals has increased packaging requirements. Recent improvements in logistics networks and export capabilities are expected to strengthen market growth throughout the forecast period.

Competitive Landscape

The steel drums market is moderately consolidated, with leading companies focusing on product innovation, geographic expansion, sustainability initiatives, and strategic partnerships. Manufacturers are investing in lightweight drum designs, advanced coatings, and refurbishment programs to strengthen competitiveness. The growing emphasis on circular economy principles has encouraged suppliers to expand reconditioning services and reusable packaging offerings.

Greif, Inc. remains a leading player in the market due to its extensive global manufacturing network and comprehensive industrial packaging portfolio. The company continues to invest in sustainable packaging solutions and drum reconditioning capabilities. Recent developments include expanded industrial packaging operations and increased investments in circular packaging programs.

Other major participants such as Mauser Packaging Solutions, Schutz, Balmer Lawrie, and Time Technoplast focus on strengthening production capacities and expanding regional presence. Strategic collaborations with chemical manufacturers and logistics providers are becoming increasingly important. Companies are also integrating digital tracking technologies and advanced coatings to enhance product performance and meet evolving customer requirements.

Key Players List

- Greif, Inc.

- Mauser Packaging Solutions

- Schutz GmbH & Co. KGaA

- Balmer Lawrie & Co. Ltd.

- Time Technoplast Ltd.

- Sicagen India Ltd.

- Great Western Containers Inc.

- Rahway Steel Drum Company

- The Cary Company

- Peninsula Drums CC

- Cloud Manufacturing Company

- Orlando Drum & Container Corporation

- Eagle Manufacturing Company

- TPL Plastech Limited

- Industrial Container Services