Lubricants Oil Drum Market Size and Growth

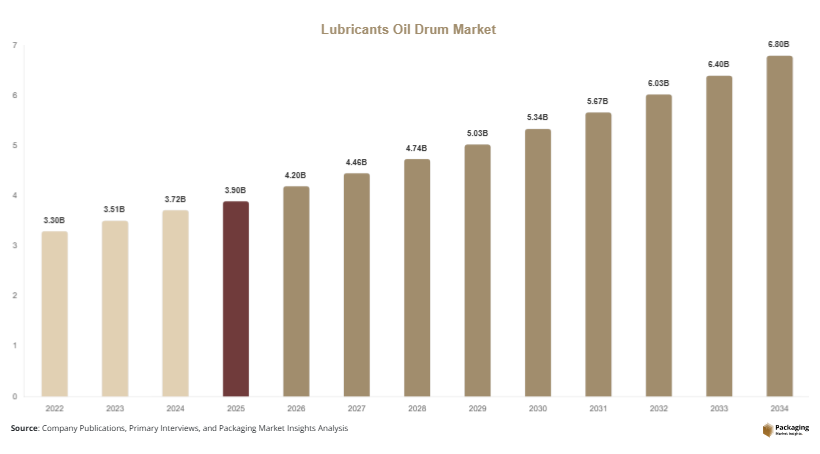

The global lubricants oil drum market size is estimated at USD 3.9 billion in 2025, and it is projected to reach USD 4.2 billion in 2026. By 2034, the market is expected to reach approximately USD 7.1 billion, registering a CAGR of 6.2% during 2025–2034. Growth is strongly linked to expanding industrial output, rising automotive maintenance demand, and increasing global trade of lubricants. The lubricants oil drum market is expanding steadily due to rising global demand for industrial lubricants, automotive oils, and bulk storage solutions that ensure safe, efficient, and contamination-free transport of oil-based products. Oil drums remain a critical packaging format across manufacturing, automotive servicing, marine operations, and heavy machinery industries due to their durability, cost efficiency, and compatibility with long-distance logistics.

One of the major growth factors is the expansion of automotive production and aftermarket services. As global vehicle fleets grow, demand for engine oils, transmission fluids, and industrial lubricants continues to rise, directly driving demand for oil drums used in bulk distribution. Another key factor is industrialization in emerging economies, particularly in Asia Pacific and Latin America, where manufacturing growth requires large-scale lubrication systems. Additionally, the increasing complexity of machinery in industries such as mining, construction, and energy is driving higher lubricant consumption, which supports steady demand for secure and standardized drum packaging.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Steel drums led the type segment with a 31.9% share.

- Metal packaging dominated with a 52.3% share.

- Automotive applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Reusable and Reconditioned Drums

The lubricants oil drum market is witnessing a strong shift toward reusable and reconditioned packaging solutions. Industries are increasingly adopting steel drums that can be cleaned, refurbished, and reused multiple times, reducing packaging waste and lowering operational costs. For example, lubricant distributors in Europe and North America are partnering with drum reconditioning service providers to implement circular packaging systems. This reduces dependency on new steel production and aligns with sustainability regulations. Companies in the automotive lubricant supply chain are particularly active in adopting returnable drum systems for bulk oil distribution. In the future, digital tracking systems using RFID tags are expected to enhance drum lifecycle management, improving efficiency in reuse cycles and reducing loss rates.

Adoption of Smart Tracking and Leak-Proof Drum Technologies

Another key trend is the integration of smart tracking and advanced sealing technologies in lubricant oil drums. Manufacturers are introducing drums equipped with QR codes, RFID tags, and IoT sensors to monitor shipment conditions, location, and usage history. This is particularly important for high-value synthetic lubricants used in aviation and industrial machinery. For example, logistics companies in Japan and Germany are using digitally traceable drum systems to improve supply chain transparency. In parallel, innovations in sealing technology, such as double-lock closures and anti-leak coatings, are improving safety during long-distance transport. This trend is expected to enhance operational efficiency and reduce product loss in global lubricant distribution networks.

Market Drivers

Growth in Automotive and Industrial Machinery Usage

The increasing global demand for automotive vehicles and industrial machinery is a major driver of the lubricants oil drum market. As vehicle production and usage rise, the need for engine oils, gear oils, and hydraulic fluids increases significantly. Oil drums serve as the primary bulk packaging solution for transporting these lubricants to service centers, manufacturing plants, and distributors. For example, automotive hubs in India, China, and Mexico rely heavily on steel drums for lubricant distribution across aftermarket service networks. Similarly, industrial machinery used in construction, mining, and manufacturing requires continuous lubrication, further increasing demand for bulk oil storage solutions. This sustained consumption pattern ensures stable growth for the oil drum packaging industry.

Expansion of Global Lubricant Trade and Petrochemical Industry

The expansion of global trade in lubricants and petrochemical products is another key growth driver. International shipping of industrial oils requires standardized, durable packaging solutions that ensure product safety and regulatory compliance. Oil drums are widely used due to their resistance to pressure, corrosion, and temperature variation. For example, Middle Eastern petrochemical exporters ship large volumes of lubricants in steel drums to Asia and Europe. Additionally, rising investments in refinery capacity expansion in countries such as Saudi Arabia and the United States are increasing lubricant output, further boosting drum demand. This global trade network ensures consistent demand across industrial supply chains.

Market Restraint

Volatility in Raw Material Prices and Environmental Regulations

A major restraint in the lubricants oil drum market is the volatility in raw material prices, particularly steel and petroleum-based plastics. Fluctuations in global steel prices directly impact drum manufacturing costs, making pricing unstable for end-users. Additionally, strict environmental regulations regarding metal production emissions and plastic waste disposal are increasing compliance costs for manufacturers. For example, European Union regulations on industrial packaging waste are pushing companies to adopt recyclable or reusable drum systems, which require higher initial investment. In developing economies, limited recycling infrastructure further complicates sustainable disposal of used drums. These factors collectively increase operational complexity and reduce profit margins for manufacturers.

Market Opportunities

Growth in Refillable and Circular Packaging Systems

The growing emphasis on circular economy models presents a significant opportunity for refillable and reusable oil drum systems. Companies are increasingly investing in closed-loop logistics, where drums are collected, cleaned, and reused multiple times. This reduces raw material consumption and transportation waste. For instance, lubricant suppliers in Germany and the Netherlands have implemented returnable drum programs for industrial clients. These systems are gaining traction in automotive and manufacturing sectors where bulk lubricant usage is consistent. As sustainability regulations tighten globally, demand for circular drum systems is expected to grow significantly.

Opportunity 2: Expansion in Emerging Industrial Economies

Emerging economies offer strong growth opportunities due to rapid industrialization and infrastructure development. Countries in Asia Pacific, Africa, and Latin America are experiencing rising demand for machinery, transportation, and manufacturing output, all of which require lubricants. This directly increases demand for oil drums as primary packaging solutions. For example, industrial expansion in Vietnam and Indonesia is driving lubricant consumption in construction and manufacturing sectors. Similarly, Brazil’s growing automotive aftermarket industry is increasing demand for bulk lubricant storage solutions. These regions present long-term expansion opportunities for drum manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.9 Billion |

| Market Size in 2026 | USD 4.2 Billion |

| Market Size in 2034 | USD 7.1 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Steel drums dominated the market in 2024 with a 31.9% share due to their durability, recyclability, and high load-bearing capacity. They are widely used in industrial lubricant transportation, particularly in automotive and petrochemical sectors. Steel drums offer excellent resistance to pressure and contamination, making them suitable for long-distance export of lubricants. For example, refineries in the Middle East rely heavily on steel drums for global distribution. Their ability to be reused and reconditioned further strengthens their dominance.

Composite drums are the fastest-growing subsegment with a CAGR of 6.8%. Growth is driven by their lightweight structure, corrosion resistance, and cost efficiency. These drums are increasingly used in specialty lubricant transportation where weight reduction is important. Industries are adopting composite solutions to reduce logistics costs and improve handling efficiency.

By Material

Metal drums dominated in 2024 with a 52.3% share, primarily due to their strength, durability, and suitability for industrial-grade lubricants. They are widely used in automotive and heavy machinery sectors.

Plastic drums are the fastest-growing subsegment with a CAGR of 5.9%, driven by their lightweight nature and ease of handling. They are increasingly used in small-scale lubricant distribution and chemical applications.

By End-Use

Automotive applications dominated in 2024 with a 43.1% share, driven by high consumption of engine oils and transmission fluids. Service centers and workshops rely heavily on bulk drum packaging.

Industrial machinery lubrication is the fastest-growing segment with a CAGR of 6.3%, driven by increasing automation and manufacturing expansion globally.

Lubricants Oil Drum Market Segmentations

By Type

- Steel Drums

- Plastic Drums

- Composite Drums

- Fiber Drums

By Material

- Metal

- Plastic

- Composite

- Fiber

By End-Use

- Automotive

- Industrial Machinery

- Petrochemical

- Marine & Offshore

Regional Analysis

North America

North America accounted for approximately 28.9% of the lubricants oil drum market in 2025 and is projected to grow at a CAGR of 5.7%. The region benefits from a mature automotive industry, strong industrial base, and advanced logistics infrastructure. Demand for lubricants in manufacturing and transportation sectors remains consistently high, supporting drum consumption. Sustainability initiatives are also influencing packaging choices, with increasing adoption of reusable steel drums.

The United States dominates the regional market due to its large automotive aftermarket and industrial machinery base. A unique growth driver is the expansion of shale oil and gas operations, which require large volumes of industrial lubricants packaged in durable drums for field operations. Oilfield service companies frequently use corrosion-resistant drums for remote site logistics.

Europe

Europe held a 24.6% market share in 2025 and is expected to grow at a CAGR of 5.4%. The region is strongly influenced by environmental regulations promoting reusable and recyclable packaging systems. Industrial manufacturers are increasingly shifting toward steel drum reuse models to reduce carbon footprint.

Germany leads the European market due to its strong manufacturing and engineering industries. A key growth factor is the adoption of circular packaging systems in automotive supply chains, where lubricant drums are returned, refurbished, and reused multiple times to reduce waste and operational costs.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is expected to grow at a CAGR of 7.0%. Rapid industrialization, automotive production growth, and expanding petrochemical output are driving strong demand for lubricant packaging solutions. China, India, and Southeast Asia are key contributors.

China dominates the region due to its massive manufacturing and automotive industries. A key growth driver is the expansion of domestic lubricant production facilities, which require high-volume drum packaging systems for distribution across industrial and export markets.

Middle East & Africa

The Middle East & Africa accounted for 5.8% of the market in 2025 and is projected to grow at a CAGR of 6.1%. Growth is driven by petrochemical exports, oil refining capacity expansion, and industrial development projects. The region plays a critical role in global lubricant supply chains.

The UAE leads the region due to its advanced logistics and oil export infrastructure. A unique growth factor is the increasing export of industrial-grade lubricants to Asia and Africa, requiring standardized, high-durability drum packaging for long-distance shipping.

Latin America

Latin America held a 3.3% market share in 2025 and is expected to grow at the fastest CAGR of 6.2%. Growth is supported by expanding automotive sectors, industrialization, and increasing lubricant consumption in manufacturing.

Brazil dominates the region due to its large automotive aftermarket industry. A key driver is the rising demand for cost-effective lubricant distribution systems in rural and semi-urban industrial zones, where oil drums remain the most efficient packaging format.

Competitive Landscape

The lubricants oil drum market is moderately consolidated with global packaging and industrial container manufacturers competing on durability, cost efficiency, and sustainability. Key players include Greif Inc., Mauser Packaging Solutions, Schutz Container Systems, Time Technoplast Ltd., and Balmer Lawrie & Co. Ltd. Among these, Greif Inc. holds a leading position due to its extensive global drum manufacturing network and strong presence in industrial packaging solutions.

Companies are focusing on reusable drum systems, lightweight material innovation, and expansion in emerging markets. Strategic partnerships with lubricant manufacturers and petrochemical companies are also common.

Key Players List

- Greif Inc.

- Mauser Packaging Solutions

- Schutz Container Systems

- Time Technoplast Ltd.

- Balmer Lawrie & Co. Ltd.

- TPL Plastech Ltd.

- Sicagen India Ltd.

- Industrial Container Services (ICS)

- Orlando Drum & Container Corp.

- Peninsula Drums

- Balaji Industrial Products Ltd.

- Snyder Industries Inc.

- Patrick J. Kelly Drums

- Hoover Ferguson Group

- National Oilwell Varco (NOV) Packaging