Tethered Caps Market Size and Growth

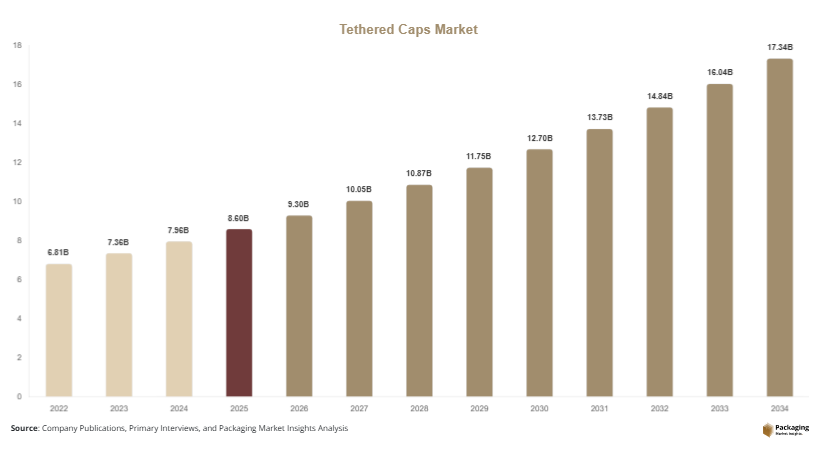

The global tethered caps market size was valued at approximately USD 8.6 billion in 2025 and is expected to reach USD 9.3 billion in 2026. The market is forecast to attain USD 17.4 billion by 2034, expanding at a CAGR of 8.1% during the forecast period (2025–2034). The transition toward sustainable packaging systems and increasing investments in packaging innovation continue to support market expansion.

The tethered caps market is gaining significant momentum as beverage, food, personal care, and household product manufacturers increasingly adopt packaging solutions that improve recyclability and reduce packaging waste. Tethered caps are closures that remain attached to the container after opening, preventing cap loss and improving collection rates during recycling processes. The market has experienced accelerated growth due to regulatory initiatives promoting circular economy practices, particularly in developed regions. Manufacturers are redesigning packaging formats to comply with evolving environmental regulations while maintaining consumer convenience and product integrity.

Key Highlights

- Europe dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 8.8%.

- Flip-Top Tethered Caps led the type segment with a 34.8% share.

- Polyethylene (PE) dominated the material segment with a 57.4% share.

- Food & Beverage applications led the market with a 68.2% share.

- The US remained the dominant country market with a market size of USD 1.9 billion in 2025 and USD 2.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Circular Packaging Designs

A major trend shaping the tethered caps market is the growing adoption of circular packaging principles. Brands are redesigning packaging formats to improve recyclability and reduce littering caused by detached caps. Beverage manufacturers are introducing tethered closure systems that remain connected to bottles throughout product use and disposal. For example, leading bottled water and soft drink companies have transitioned large portions of their product portfolios to tethered cap designs to align with sustainability objectives. This trend is expected to accelerate as packaging regulations become more stringent globally. Future developments will likely focus on lightweight cap structures, reduced resin usage, and enhanced compatibility with recycling systems, creating additional growth opportunities for manufacturers.

Integration of Consumer-Friendly Closure Technologies

Packaging companies are increasingly developing tethered cap designs that enhance user convenience without compromising sustainability goals. Consumers expect closures that are easy to open, reseal, and use while maintaining product freshness. Manufacturers are therefore investing in ergonomic hinge systems and advanced molding technologies. For example, dairy beverage producers have introduced tethered caps that remain securely attached while allowing comfortable pouring and drinking experiences. As competition intensifies, brands are expected to differentiate products through improved closure functionality. Future innovations may include smart closure systems, tamper-evident features, and enhanced dispensing mechanisms that strengthen consumer acceptance of tethered packaging solutions.

Market Drivers

Stringent Packaging Waste Regulations

Government regulations focused on reducing plastic waste are a major driver for the tethered caps market. Regulatory frameworks increasingly require beverage containers to incorporate attached caps that remain connected during the product lifecycle. These measures aim to improve recycling rates and reduce environmental litter. The direct effect of such regulations is increased investment in cap redesign, manufacturing upgrades, and packaging innovation. For example, beverage producers across Europe have accelerated the implementation of tethered cap solutions to comply with new sustainability standards. As additional countries adopt similar policies, demand for compliant packaging systems is expected to rise substantially throughout the forecast period.

Sustainability Commitments from Consumer Goods Companies

Global consumer goods companies are establishing ambitious sustainability targets that emphasize recyclable packaging and waste reduction. Tethered caps help brands achieve environmental goals by improving collection efficiency and supporting circular economy initiatives. The cause-and-effect relationship is evident as corporate sustainability commitments directly influence packaging procurement decisions. For example, multinational beverage brands are converting billions of bottles annually to tethered-cap formats to demonstrate environmental responsibility. As investors, consumers, and regulators increasingly evaluate sustainability performance, packaging suppliers offering innovative tethered cap solutions are expected to experience growing demand across multiple industries.

Market Restraint

High Conversion Costs and Manufacturing Complexity

Despite favorable growth prospects, the tethered caps market faces challenges related to conversion costs and production complexity. Transitioning from traditional closures to tethered cap designs often requires substantial investment in tooling, manufacturing equipment, testing procedures, and packaging line modifications. Small and medium-sized packaging companies may encounter financial constraints when implementing these changes. Additionally, maintaining closure performance while ensuring consumer convenience presents engineering challenges. For example, beverage manufacturers frequently conduct extensive testing to verify that tethered caps maintain sealing integrity and usability throughout the product lifecycle. These factors can increase operational costs and slow adoption in cost-sensitive markets. While economies of scale and technological advancements are expected to reduce costs over time, implementation expenses remain a significant market restraint.

Market Opportunities

Expansion Across Emerging Beverage Markets

Emerging economies present substantial opportunities for tethered cap manufacturers. Rising urbanization, increasing bottled beverage consumption, and expanding retail networks are driving packaging demand in regions such as Asia Pacific, Latin America, and parts of Africa. As governments introduce waste management initiatives and environmental policies, local beverage producers are expected to adopt tethered closure systems. Future applications extend beyond water and soft drinks to include juices, dairy beverages, energy drinks, and functional nutrition products. Manufacturers capable of providing cost-effective tethered cap solutions tailored to regional market requirements are likely to benefit from significant growth opportunities.

Development of Recycled and Bio-Based Closure Materials

The increasing focus on sustainable materials creates opportunities for innovation within the tethered caps market. Packaging companies are exploring recycled plastics and bio-based polymers that reduce environmental impact while maintaining closure performance. Future product development is expected to emphasize compatibility with circular economy objectives and consumer sustainability preferences. For example, several packaging suppliers are testing closures manufactured using high percentages of recycled polyethylene. These innovations can support brand sustainability targets while addressing regulatory requirements. As material technologies mature, demand for environmentally responsible tethered cap solutions is expected to expand across beverage, personal care, and household product applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.6 Billion |

| Market Size in 2026 | USD 9.3 Billion |

| Market Size in 2034 | USD 17.4 Billion |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flip-Top Tethered Caps dominated the market in 2024, accounting for approximately 34.8% of total revenue. Their leadership position is attributed to ease of use, effective sealing performance, and widespread adoption across beverage applications. Consumers prefer flip-top designs because they provide convenient opening and resealing functions while remaining attached to the container. Beverage manufacturers also benefit from compatibility with high-speed filling lines and established production systems. Applications include bottled water, dairy beverages, sports drinks, and juice products. The segment's dominance is further supported by growing regulatory compliance requirements and increasing investments in sustainable packaging technologies.

Sports Tethered Caps are expected to register the fastest growth, expanding at a CAGR of 9.2% during the forecast period. Rising demand for functional beverages, sports nutrition products, and on-the-go hydration solutions is driving adoption. Manufacturers are introducing advanced dispensing mechanisms that improve consumer convenience and product differentiation. Future growth will also be supported by packaging innovations that enhance portability and sustainability performance. As active lifestyle trends continue to expand globally, sports tethered caps are expected to gain substantial market share.

By Material

Polyethylene (PE) dominated the material segment in 2024, holding approximately 57.4% of market share. PE remains the preferred material due to its flexibility, durability, chemical resistance, and cost-effectiveness. Closure manufacturers widely utilize high-density and low-density polyethylene grades to produce tethered caps for beverage and food applications. The material's compatibility with existing recycling streams further supports its widespread use. Packaging companies continue to optimize PE formulations to reduce material consumption while maintaining performance standards.

Recycled Plastics are projected to be the fastest-growing material category, recording a CAGR of 9.5% through 2034. Sustainability objectives, regulatory pressures, and consumer preferences are encouraging increased use of recycled content in packaging components. Manufacturers are investing in advanced recycling technologies that improve material quality and consistency. Future developments are expected to enhance the performance characteristics of recycled polymers, enabling broader adoption across beverage, personal care, and household packaging applications.

By End-Use

Food & Beverage represented the largest end-use segment in 2024, accounting for approximately 68.2% of total market revenue. High consumption volumes of bottled beverages, dairy products, juices, and liquid nutrition products support segment dominance. Regulatory requirements related to packaging sustainability have accelerated the adoption of tethered caps within this industry. Beverage companies continue to redesign packaging formats to improve recyclability and align with environmental commitments. Strong consumer demand for convenient packaging further reinforces segment leadership.

Personal Care is expected to emerge as the fastest-growing end-use segment, expanding at a CAGR of 8.7% during the forecast period. Manufacturers of shampoos, lotions, liquid soaps, and cosmetic products are increasingly evaluating tethered closure solutions to enhance sustainability performance. Growth is also supported by consumer demand for environmentally responsible packaging formats. Future opportunities include premium dispensing systems, lightweight closure designs, and increased use of recycled materials. As sustainability becomes a core purchasing criterion, adoption within personal care applications is expected to accelerate significantly.

Tethered Caps Market Segmentations

By Type

- Flip-Top Tethered Caps

- Screw Tethered Caps

- Sports Tethered Caps

- Snap-On Tethered Caps

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Recycled Plastics

- Bio-Based Plastics

By End-User

- Food & Beverage

- Personal Care

- Household Products

- Pharmaceuticals

Regional Analysis

North America

North America accounted for approximately 24.8% of the global tethered caps market share in 2025 and is projected to grow at a CAGR of 7.7% through 2034. The region benefits from advanced packaging infrastructure, strong beverage consumption, and increasing investments in sustainable packaging solutions. Major beverage manufacturers are implementing tethered cap designs across water, carbonated drinks, and dairy products to support corporate sustainability commitments. Rising consumer awareness regarding recycling practices is also contributing to market growth. Furthermore, retailers are increasingly favoring packaging formats that align with environmental objectives, encouraging widespread adoption across consumer goods industries.

The United States dominates the regional market. A unique growth driver is the rapid expansion of sustainability-focused packaging procurement by multinational beverage companies. Many brands are redesigning packaging portfolios to meet environmental commitments and improve recycling outcomes. For example, leading bottled water producers have expanded the use of tethered closures across multiple product categories. Continued investment in recycling infrastructure and circular packaging initiatives is expected to support long-term market development in the country.

Europe

Europe represented approximately 38.6% of the global market share in 2025 and is expected to register a CAGR of 8.0% through 2034. The region remains the largest market due to regulatory mandates promoting attached cap designs on beverage containers. Packaging manufacturers and beverage producers have rapidly adapted operations to comply with evolving environmental requirements. Demand remains particularly strong across bottled water, soft drinks, dairy products, and liquid food applications. Sustainability regulations continue to influence packaging innovation, encouraging investments in lightweight designs and recyclable materials.

Germany is the dominant country within Europe. A unique growth driver is the country's leadership in sustainable packaging technology and manufacturing automation. Packaging companies continue to invest in advanced molding equipment and closure engineering solutions that improve efficiency and product performance. For example, several closure manufacturers have expanded production capacity to meet rising demand from beverage producers. This trend supports continued market growth throughout the forecast period.

Asia Pacific

Asia Pacific held approximately 27.5% of the global market share in 2025 and is forecast to expand at a CAGR of 8.5% through 2034. The region benefits from rising bottled beverage consumption, growing urban populations, and expanding food processing industries. Increasing awareness regarding plastic waste management is encouraging governments and manufacturers to evaluate sustainable packaging alternatives. Large-scale beverage production activities across multiple countries create significant demand for innovative closure systems. Continued industrialization and retail expansion are expected to strengthen market growth.

China leads the Asia Pacific market. A unique growth factor is the country's extensive beverage manufacturing ecosystem. Producers are increasingly adopting modern packaging technologies to improve environmental performance and align with evolving consumer expectations. For example, large beverage companies have initiated packaging redesign programs incorporating tethered closures. Growing investment in recycling infrastructure further supports adoption throughout the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.8% of global market share in 2025 and is projected to grow at a CAGR of 7.9% through 2034. Rising bottled water consumption, expanding urban populations, and increasing environmental awareness are contributing to market growth. Demand for convenient and sustainable beverage packaging formats is increasing across both developed and emerging economies within the region. Government efforts to improve waste management systems are also supporting industry development.

Saudi Arabia dominates the regional market. A unique growth driver is the strong demand for bottled drinking water resulting from climatic conditions and population growth. Beverage producers are investing in packaging innovations that support sustainability objectives while maintaining operational efficiency. For example, regional bottling companies are evaluating tethered closure technologies to improve packaging compliance and environmental performance. These developments create favorable conditions for market expansion.

Latin America

Latin America represented approximately 5.3% of the global market share in 2025 and is expected to record the fastest CAGR of 8.8% through 2034. Rising consumption of packaged beverages, increasing environmental awareness, and modernization of packaging infrastructure are supporting market growth. Regional beverage manufacturers are investing in sustainable packaging solutions to improve competitiveness and comply with emerging environmental standards. Growth in organized retail channels is further strengthening demand for innovative packaging formats.

Brazil remains the dominant country in Latin America. A unique growth driver is the rapid expansion of the packaged beverage industry, particularly bottled water and soft drinks. Manufacturers are increasingly implementing sustainable packaging initiatives to meet consumer expectations and retailer requirements. For example, several beverage producers have introduced pilot programs featuring tethered closures. Such initiatives are expected to support accelerated adoption throughout the forecast period.

Competitive Landscape

The tethered caps market is moderately consolidated, with major packaging and closure manufacturers competing through innovation, sustainability initiatives, and strategic capacity expansion. Berry Global Group, Inc. is recognized as a leading market participant due to its extensive closure portfolio, global manufacturing footprint, and continuous investments in sustainable packaging technologies. The company has expanded production capabilities for tethered closure systems designed for beverage applications.

Other significant companies include AptarGroup, Inc., Silgan Holdings Inc., Bericap Holding GmbH, and Closure Systems International. These companies focus on advanced closure engineering, lightweight designs, and regulatory-compliant packaging solutions. Recent developments include the launch of next-generation tethered caps, investments in recycled-content closure materials, and partnerships with beverage manufacturers seeking sustainable packaging alternatives. Competitive strategies increasingly emphasize innovation, material optimization, and production efficiency.

Key Players List

- Berry Global Group, Inc.

- AptarGroup, Inc.

- Silgan Holdings Inc.

- Bericap Holding GmbH

- Closure Systems International

- ALPLA Group

- United Caps

- Guala Closures Group

- Weener Plastics Group

- Pact Group Holdings Ltd.

- Mold-Rite Plastics

- O.Berk Company

- Georg MENSHEN GmbH

- Comar LLC

- Tecnocap Group