Bottle Caps Market Size and Growth

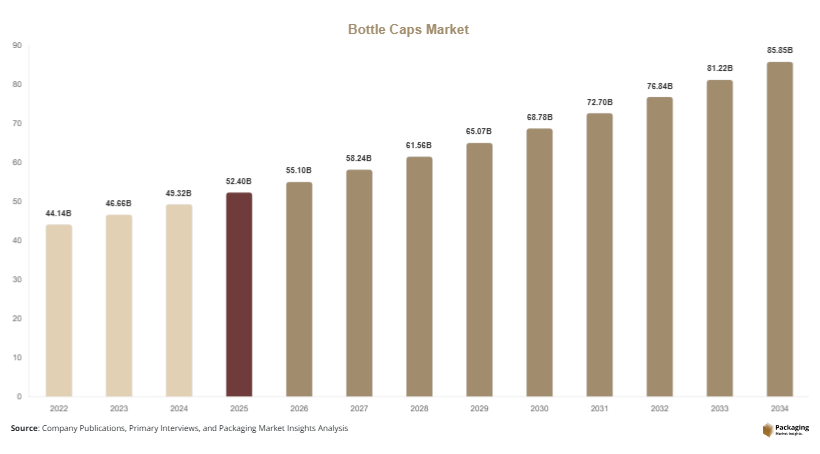

The global bottle caps market was valued at approximately USD 52.4 billion in 2025 and is estimated to reach USD 55.1 billion in 2026. The market is projected to expand at a CAGR of 5.7% from 2025 to 2034, reaching nearly USD 90.2 billion by the end of the forecast period. The increasing consumption of packaged beverages, rising pharmaceutical production, and expanding demand for convenient packaging solutions are driving steady growth across the global market.

Bottle caps play a critical role in maintaining product safety, preventing leakage, extending shelf life, and supporting brand differentiation. Manufacturers across beverage, food, healthcare, cosmetics, and household product industries are increasingly investing in advanced closure systems to improve functionality and consumer convenience. The growing popularity of bottled water, carbonated drinks, energy beverages, dairy products, and ready-to-drink beverages is significantly supporting demand for plastic and metal bottle caps worldwide.

Key Highlights

- Asia Pacific dominated the market with a 39.3% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.3%.

- Screw caps led the type segment with a 46.8% share.

- Plastic material dominated with a 61.5% share.

- Beverage applications led the segment with 58.4% share.

- The US remained the dominant country with a market size of USD 8.1 billion in 2025 and USD 8.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable and Tethered Closures

Sustainability regulations are increasingly influencing the bottle caps market, particularly in Europe and North America where governments are implementing policies to reduce plastic waste. Beverage manufacturers and packaging companies are introducing tethered caps that remain attached to bottles after opening, helping improve recycling collection rates and reduce littering. This trend is becoming increasingly common among bottled water, soft drink, and dairy beverage manufacturers.

Packaging companies are also investing in lightweight plastic closures and recycled resin materials to reduce raw material usage. Several multinational beverage producers have announced plans to shift toward fully recyclable bottle cap systems over the next decade. The adoption of bio-based polymers and post-consumer recycled plastics is expected to increase as environmental regulations become stricter. Over the long term, sustainable cap innovations are likely to influence packaging procurement strategies across global beverage and food industries.

Increasing Demand for Smart and Functional Bottle Caps

Smart packaging technologies are becoming an important trend in the bottle caps market as manufacturers seek to improve product security, consumer interaction, and supply chain transparency. Bottle caps integrated with QR codes, NFC technology, and authentication systems are increasingly used in premium beverages, pharmaceuticals, and nutritional products.

For example, beverage brands are using connected bottle caps to provide digital marketing experiences and product traceability features. Pharmaceutical companies are also adopting smart caps with dosage monitoring and tamper-evident mechanisms to improve patient safety and regulatory compliance. Functional innovations such as resealable caps, child-resistant closures, and anti-spill dispensing systems are gaining popularity across healthcare and household product industries. Future advancements in connected packaging technologies are expected to create new opportunities for interactive and data-driven packaging solutions.

Market Drivers

Rising Consumption of Packaged Beverages Worldwide

The increasing consumption of packaged beverages is one of the strongest growth drivers for the bottle caps market. Bottled water, carbonated drinks, fruit juices, dairy beverages, sports drinks, and ready-to-drink coffee products require secure closure systems that maintain freshness and prevent contamination. Bottle caps provide sealing performance, tamper evidence, and ease of use, making them essential for beverage packaging applications.

Rapid urbanization and changing consumer lifestyles are increasing demand for portable beverage packaging in emerging economies. Beverage companies are also expanding premium product lines that require customized closure designs and improved branding features. For example, bottled water producers are introducing lightweight caps to reduce plastic consumption and improve sustainability performance. The expansion of supermarkets, convenience stores, and e-commerce beverage distribution is expected to continue supporting long-term demand for bottle caps.

Growth in Pharmaceutical and Healthcare Packaging

The expansion of pharmaceutical manufacturing and healthcare product consumption is another major factor driving the bottle caps market. Pharmaceutical companies require advanced closure systems that protect medicines from contamination, leakage, and unauthorized access. Child-resistant caps, tamper-proof closures, and dosage-control systems are increasingly used in prescription medicine and over-the-counter healthcare products.

Growing healthcare expenditure and rising pharmaceutical exports from countries such as India, China, Germany, and the United States are contributing to higher packaging demand. Pharmaceutical packaging companies are investing in high-performance closures with anti-counterfeit and traceability features to comply with regulatory standards. Nutritional supplements and liquid medicine packaging are also increasing the use of advanced cap technologies. This growing healthcare packaging sector is expected to create stable long-term demand for specialized bottle closure solutions.

Market Restraint

Environmental Concerns Related to Plastic Waste

Environmental concerns related to plastic waste remain a major restraint affecting the bottle caps market. Plastic caps are widely used because they are lightweight, durable, and cost-effective, but growing concerns regarding marine pollution and landfill waste are increasing regulatory pressure on packaging manufacturers. Governments in Europe, North America, and parts of Asia are introducing strict policies aimed at reducing single-use plastic packaging and improving recycling performance.

Bottle cap manufacturers may face rising compliance costs as they transition toward recyclable materials and sustainable production systems. Small and medium-sized packaging companies often struggle to invest in recycled resin processing technologies and advanced manufacturing equipment. Beverage companies are also under pressure to redesign packaging systems to meet sustainability commitments.

For example, manufacturers using conventional virgin plastic closures may need to adopt recycled materials or tethered cap technologies to comply with environmental regulations. These changes can increase production complexity and raw material costs. In addition, inconsistent recycling infrastructure across developing economies limits the effective recovery of plastic bottle caps. These environmental and regulatory challenges may slow market expansion in price-sensitive regions during the forecast period.

Market Opportunities

Expansion of Recyclable and Bio-Based Bottle Caps

The increasing focus on sustainable packaging presents significant opportunities for the bottle caps market. Beverage and food companies are actively searching for recyclable and bio-based cap materials that reduce environmental impact while maintaining sealing performance. Packaging manufacturers are investing in caps made from recycled polyethylene, bio-based polymers, and lightweight materials to align with sustainability goals.

Several beverage companies have introduced tethered caps and recyclable closure systems designed to improve plastic collection rates. Future opportunities are expected to emerge from biodegradable cap materials and plant-based polymers used in bottled beverage applications. Developing economies are also increasing investments in recycling infrastructure and waste collection systems, which is likely to strengthen demand for environmentally compatible bottle closure technologies.

Growth of Smart Packaging and Connected Closures

Connected packaging technologies are creating long-term growth opportunities for the bottle caps market. Smart bottle caps equipped with authentication systems, QR codes, NFC chips, and freshness indicators are becoming increasingly important in beverage, healthcare, and nutritional product packaging.

Premium beverage brands are integrating digital engagement features into bottle caps to improve customer interaction and support marketing campaigns. Pharmaceutical companies are also using connected closures to monitor dosage usage and improve medication safety. Future applications may include temperature-sensitive closures for cold-chain pharmaceutical products and refillable smart packaging systems for household products. Advancements in low-cost sensor technologies and digital printing are expected to encourage broader adoption of connected bottle cap solutions across multiple industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 52.4 Billion |

| Market Size in 2026 | USD 55.1 Billion |

| Market Size in 2034 | USD 90.2 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Screw caps dominated the bottle caps market and accounted for approximately 46.8% of the global market share in 2024. Their dominance is mainly attributed to strong sealing performance, low manufacturing costs, and compatibility with high-speed production lines. Screw caps are extensively used across bottled water, soft drinks, edible oil, dairy beverages, pharmaceutical syrups, and household product packaging applications. Beverage manufacturers prefer screw caps because they provide resealability and consumer convenience while reducing leakage risks during transportation. Plastic screw caps are particularly popular because of their lightweight structure and cost efficiency. Packaging companies are increasingly investing in customized screw cap designs and tamper-evident technologies to improve product security and branding opportunities. The growth of ready-to-drink beverages and e-commerce beverage distribution continues to support strong demand for screw cap solutions worldwide.

Tethered caps are expected to register the fastest CAGR of 6.9% during the forecast period due to increasing environmental regulations and sustainability initiatives. Tethered closures remain attached to beverage containers after opening, improving recycling collection rates and reducing plastic litter. Beverage manufacturers across Europe are rapidly adopting tethered cap systems to comply with regulatory requirements related to single-use plastic reduction. Packaging companies are also developing lightweight tethered closure designs that maintain consumer convenience while reducing material usage. Future growth is expected to be driven by increasing adoption among bottled water, juice, and dairy beverage manufacturers. Emerging economies are also likely to witness stronger demand for tethered caps as sustainability regulations expand globally.

By Material

Plastic material dominated the bottle caps market with a 61.5% share in 2024 due to its lightweight structure, durability, and low production cost. Plastic caps are widely used across beverage, food, pharmaceutical, and household product packaging because they provide flexibility and compatibility with automated filling systems. Polypropylene and polyethylene are among the most commonly used materials because they support tamper-evident and resealable closure systems. Beverage manufacturers prefer plastic caps for bottled water, carbonated drinks, and dairy beverages because they are economical and suitable for large-scale production. Packaging suppliers are increasingly introducing lightweight plastic caps to reduce raw material consumption and transportation costs. Advanced molding technologies and digital printing capabilities are also improving the functionality and branding potential of plastic bottle caps.

Recycled plastic materials are projected to witness the fastest CAGR of 6.7% during the forecast period because of rising sustainability goals and environmental regulations. Beverage and packaging companies are increasingly integrating post-consumer recycled plastics into cap manufacturing to reduce carbon emissions and support circular economy initiatives. Several multinational beverage companies have announced targets to increase recycled material usage across packaging components, including bottle caps. Packaging suppliers are investing in advanced recycling systems and resin purification technologies to improve the quality of recycled materials. Future demand is expected to rise as governments strengthen regulations related to plastic waste management and packaging recyclability. Emerging economies are also improving recycling infrastructure, creating additional growth opportunities for recycled plastic bottle caps.

By End-Use

Beverage applications accounted for nearly 58.4% of the global bottle caps market in 2024, making it the dominant end-use segment. Rising consumption of bottled water, carbonated drinks, fruit juices, dairy beverages, and ready-to-drink coffee products continues to support strong demand for bottle caps. Beverage manufacturers require reliable closure systems that prevent contamination, maintain carbonation, and support convenient resealing. Bottle caps are also increasingly used as branding elements through customized colors, logos, and promotional printing technologies. The rapid expansion of convenience retail and e-commerce beverage distribution is further contributing to segment growth. Packaging companies are introducing lightweight and recyclable closures designed specifically for high-volume beverage production environments.

Pharmaceutical packaging is expected to register the fastest CAGR of 6.4% through 2034 due to increasing healthcare expenditure and growing pharmaceutical manufacturing activities worldwide. Pharmaceutical companies require advanced closure systems that ensure product safety, dosage protection, and tamper evidence. Child-resistant caps and anti-counterfeit technologies are becoming increasingly important for liquid medicine packaging and healthcare products. Growth in nutritional supplements and over-the-counter healthcare products is also increasing demand for specialized bottle closures. Future opportunities are expected to emerge from smart pharmaceutical caps equipped with dosage monitoring and connected packaging technologies. Expanding healthcare access in emerging economies is likely to support long-term growth in pharmaceutical bottle cap demand.

Bottle Caps Market Segmentations

By Type

- Screw Caps

- Crown Caps

- Snap-On Caps

- Tethered Caps

- Dispensing Caps

By Material

- Plastic

- Metal

- Recycled Plastic

- Aluminum

By End-User

- Beverage

- Pharmaceutical

- Food

- Personal Care & Cosmetics

- Household Products

Regional Analysis

North America

North America accounted for approximately 25.8% of the global bottle caps market in 2025 and is projected to grow at a CAGR of 5.1% through 2034. The region benefits from high packaged beverage consumption, advanced pharmaceutical manufacturing, and strong retail infrastructure. Bottle caps are extensively used across bottled water, carbonated beverages, dairy products, healthcare packaging, and household product applications. The increasing shift toward lightweight and recyclable packaging solutions is supporting market expansion. Beverage manufacturers are also adopting tethered closures and recycled plastic materials to comply with environmental regulations and sustainability targets.

The United States remains the dominant country within the regional market due to its large beverage industry and advanced packaging manufacturing capabilities. One unique growth driver in the region is the rapid expansion of functional beverage categories, including energy drinks, flavored water, and nutritional beverages. Beverage companies are increasingly introducing customized cap designs and resealable closures to improve convenience and brand differentiation. Several packaging manufacturers are also investing in smart cap technologies with digital authentication features for premium beverages and healthcare products.

Europe

Europe represented nearly 23.6% of the global bottle caps market in 2025 and is anticipated to register a CAGR of 5.3% during the forecast period. The region is strongly influenced by sustainability regulations, circular economy initiatives, and high recycling standards. Governments across Europe are encouraging the use of recyclable bottle caps and tethered closure systems to reduce plastic waste. Beverage manufacturers are increasingly replacing traditional closures with lightweight recyclable alternatives.

Germany remains the leading country in the European market because of its strong beverage production and advanced packaging technology sector. One important growth driver is the implementation of strict European Union regulations requiring tethered caps for beverage containers. Packaging manufacturers are investing in recyclable polymer technologies and lightweight cap designs to comply with these standards. Demand for premium bottled beverages, dairy products, and pharmaceutical packaging is also increasing the adoption of advanced bottle closure systems across the region.

Asia Pacific

Asia Pacific dominated the global bottle caps market with a 39.3% share in 2025 and is projected to register a CAGR of 6.0% through 2034. Rapid urbanization, population growth, and expanding packaged food and beverage industries are major factors supporting regional market expansion. Rising consumption of bottled water, carbonated drinks, ready-to-drink tea, and dairy beverages is significantly increasing demand for plastic and metal bottle caps.

China remains the dominant country in the regional market due to its large beverage production capacity and extensive packaging manufacturing industry. One unique growth driver is the rapid expansion of e-commerce beverage delivery and convenience retail channels. Beverage manufacturers are investing in lightweight closures and automated cap manufacturing systems to improve production efficiency and reduce logistics costs. India is emerging as another high-growth market because of rising pharmaceutical exports and increasing demand for affordable packaged beverages. Governments across the region are also encouraging investments in recycling infrastructure and sustainable packaging technologies.

Middle East & Africa

The Middle East & Africa accounted for approximately 6.2% of the global bottle caps market in 2025 and is expected to grow at a CAGR of 5.6% through 2034. Increasing urbanization, expanding beverage production, and rising healthcare packaging demand are supporting regional market development. Bottled water consumption is particularly strong in Gulf countries due to hot climatic conditions and growing tourism activity. Beverage companies are increasingly adopting lightweight plastic closures to improve transportation efficiency and reduce packaging costs.

Saudi Arabia remains the dominant country in the regional market due to its expanding food and beverage industry and strong investment in packaging manufacturing. One major growth driver is the increasing demand for bottled water and functional beverages among urban consumers. Regional beverage companies are introducing customized cap designs and tamper-evident closures to improve product safety and brand visibility. In Africa, pharmaceutical packaging demand is also increasing because of expanding healthcare access and rising imports of packaged medicines.

Latin America

Latin America held nearly 5.1% of the global bottle caps market in 2025 and is projected to expand at the fastest CAGR of 6.3% during the forecast period. Rising beverage consumption, expanding retail distribution, and increasing packaged food demand are supporting market growth across the region. Beverage manufacturers are increasingly adopting lightweight bottle caps to improve transportation efficiency and reduce overall packaging costs.

Brazil remains the leading country in the Latin American market because of its strong beverage industry and large bottled water consumption base. One unique growth driver is the expansion of affordable packaged beverage products targeted at middle-income consumers. Beverage companies are introducing innovative closure systems for flavored drinks, dairy beverages, and fruit juices to improve convenience and product differentiation. Mexico is also witnessing increasing demand for advanced bottle caps due to growth in beverage exports and pharmaceutical manufacturing activities.

Competitive Landscape

The bottle caps market is highly competitive, with major packaging manufacturers focusing on sustainability, lightweight closure technologies, and smart packaging innovations to strengthen market presence. Companies are increasing investments in recyclable materials, automated manufacturing systems, and advanced closure designs to meet changing consumer and regulatory requirements.

Berry Global remains one of the leading companies in the market due to its broad packaging portfolio and strong global manufacturing network. The company has expanded its recyclable bottle cap solutions and invested in lightweight closure technologies designed for beverage and healthcare applications.

Silgan Holdings, AptarGroup, Crown Holdings, and Closure Systems International are also major participants in the market. These companies are focusing on strategic partnerships, regional expansion projects, and advanced molding technologies to strengthen competitiveness. Packaging manufacturers are increasingly developing tethered caps, child-resistant closures, and connected packaging systems to address evolving industry requirements.

Regional companies in Asia Pacific and Latin America are also expanding production capacity to support rising demand for bottled beverages and pharmaceutical packaging. Collaboration between beverage producers and packaging suppliers is increasing as companies seek customized bottle closure systems with improved sustainability and branding performance.

Key Players List

- Berry Global

- Silgan Holdings Inc.

- AptarGroup Inc.

- Crown Holdings Inc.

- Closure Systems International

- Bericap GmbH & Co. KG

- Guala Closures Group

- Amcor plc

- O.Berk Company LLC

- Mold-Rite Plastics

- Nippon Closures Co., Ltd.

- Tecnocap Group

- UNITED CAPS

- Cap & Seal Pvt. Ltd.

- Pact Group Holdings Ltd.

- Phoenix Closures Inc.

- CL Smith Company