Lubricant Packaging Market Size and Growth

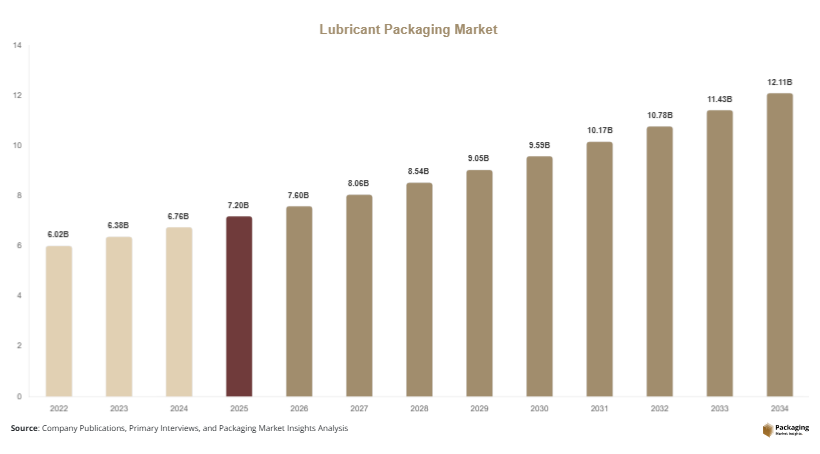

The global lubricant packaging market size was valued at approximately USD 7.2 billion in 2025 and is projected to reach USD 7.6 billion in 2026. With increasing consumption of engine oils, hydraulic fluids, and industrial lubricants across both developed and emerging economies, the market is expected to reach USD 12.9 billion by 2034, growing at a CAGR of 6.0% during the forecast period from 2025 to 2034. The growth reflects increasing industrial activity, vehicle parc expansion, and rising maintenance requirements across multiple end-use industries. The lubricant packaging market is experiencing steady expansion driven by rising demand from automotive, industrial machinery, and manufacturing sectors.

One of the primary growth factors is the continuous expansion of the global automotive sector. Increasing vehicle production and ownership rates are directly driving demand for lubricants, which in turn increases the need for efficient packaging solutions. Lubricant packaging plays a key role in ensuring product safety, preventing leakage, and enabling convenient handling during storage and distribution. Another important factor is the rising industrialization across emerging economies, where manufacturing activity is increasing demand for machinery lubricants and associated packaging solutions.

Key Market Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.5%.

- Plastic containers led the type segment with a 44.7% share, while biodegradable lubricant packaging is expected to grow at a CAGR of 6.8%.

- Bottles dominated with a 36.9% share, while flexible pouches are forecasted to grow at a CAGR of 6.6%.

- Automotive applications led the segment with 49.2% share, while industrial machinery is expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 1.8 billion in 2025 and USD 1.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Packaging Materials

The lubricant packaging market is witnessing a strong shift toward sustainable packaging solutions as environmental regulations become stricter across global markets. Manufacturers are increasingly adopting recyclable plastics, bio-based materials, and lightweight containers to reduce environmental impact. Lubricant packaging traditionally relies heavily on plastic drums and bottles, but growing concerns about plastic waste are pushing companies to innovate eco-friendly alternatives. Many packaging producers are investing in materials that can be reused multiple times without compromising durability. This trend is particularly visible in Europe and North America, where regulatory frameworks strongly support circular economy practices. The adoption of sustainable packaging is also being driven by end-user companies aiming to improve environmental compliance and corporate sustainability goals.

Growth of Smart and Industrial-Grade Packaging Solutions

Another emerging trend in the lubricant packaging market is the development of smart and industrial-grade packaging systems designed to improve efficiency and safety. These advanced packaging solutions include tamper-evident seals, precision dispensing systems, and RFID-enabled tracking containers. Industrial users are increasingly demanding packaging that enhances operational control and reduces product wastage. Smart packaging technologies are helping companies monitor lubricant usage, track inventory, and improve supply chain transparency. In large-scale manufacturing and automotive sectors, these innovations are improving maintenance efficiency and reducing downtime. The integration of automation and digital tracking systems is expected to further enhance the value proposition of lubricant packaging solutions.

Market Drivers

Expansion of Automotive Production and Vehicle Ownership

The rapid growth of the global automotive industry is a major driver of the lubricant packaging market. Increasing vehicle production, especially in emerging economies, is boosting demand for engine oils and maintenance fluids. As the global vehicle fleet expands, the need for lubricant replacement and servicing increases significantly. This directly drives demand for efficient packaging solutions that ensure safe storage and distribution. Lubricant packaging is essential for preventing leakage, maintaining product quality, and enabling easy handling during servicing operations. The rise in electric vehicles is also contributing indirectly, as hybrid systems still require lubricants for components such as transmissions and cooling systems.

Increasing Industrialization and Machinery Maintenance Needs

Industrial expansion across manufacturing, construction, and mining sectors is another key driver of the lubricant packaging market. Industrial machinery requires regular lubrication to maintain efficiency and prevent wear and tear. As industrial operations expand globally, especially in Asia Pacific and Latin America, demand for lubricants is increasing steadily. This growth is directly linked to packaging demand, as industrial users require durable, large-capacity containers such as drums and intermediate bulk containers. Packaging solutions must ensure chemical resistance, durability, and ease of transport. The rising emphasis on predictive maintenance and operational efficiency is further supporting lubricant consumption and packaging demand.

Market Restraint

Fluctuating Raw Material Prices and Environmental Regulations

One of the key restraints affecting the lubricant packaging market is the volatility in raw material prices, particularly plastics and polymers used in packaging production. Price fluctuations in crude oil-based materials directly impact manufacturing costs, making it difficult for packaging companies to maintain stable pricing. Additionally, stringent environmental regulations regarding plastic usage and waste management are increasing compliance costs for manufacturers. For example, bans on single-use plastics in certain regions are forcing companies to redesign packaging formats, which requires additional investment in research and development. These factors can slow market expansion, particularly for small and medium-sized packaging manufacturers operating with limited financial flexibility.

Market Opportunities

Expansion of Industrial Lubricant Demand in Emerging Economies

Emerging economies present significant opportunities for the lubricant packaging market due to rapid industrialization and infrastructure development. Countries in Asia Pacific, Africa, and Latin America are witnessing increased manufacturing activity, which drives demand for industrial lubricants. This creates a parallel need for durable and cost-effective packaging solutions. Local production facilities are expanding, and multinational lubricant companies are entering these regions, increasing packaging consumption. The growth of construction and mining sectors further supports demand for bulk packaging formats such as drums and IBCs. Packaging companies that establish strong regional supply chains are expected to benefit from this growing demand base.

Development of Lightweight and High-Efficiency Packaging Systems

Innovation in lightweight packaging materials is creating new opportunities in the lubricant packaging market. Manufacturers are focusing on reducing material usage while maintaining durability and chemical resistance. Lightweight packaging helps reduce transportation costs and improves supply chain efficiency. Advanced polymers and hybrid materials are being used to develop containers that are easier to handle and more environmentally friendly. These innovations are particularly beneficial for large-scale industrial users who require cost-efficient logistics solutions. The increasing focus on sustainability and operational efficiency is expected to drive adoption of these advanced packaging systems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.2 Billion |

| Market Size in 2026 | USD 7.6 Billion |

| Market Size in 2034 | USD 12.9 Billion |

| CAGR | 6.0% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Packaging Type

Plastic containers dominated the lubricant packaging market in 2024 with approximately 44.7% share. These containers are widely used due to their lightweight nature, cost efficiency, and chemical resistance. Plastic packaging is commonly used for engine oils and industrial lubricants in bottles and jerry cans. Their durability and ease of manufacturing make them a preferred choice for both small and large-scale applications. The growing automotive aftermarket continues to support demand for plastic-based lubricant packaging solutions.

Biodegradable lubricant packaging is expected to grow at the fastest CAGR of 6.8%. This growth is driven by increasing environmental concerns and regulatory pressure to reduce plastic waste. Manufacturers are developing bio-based materials that offer similar durability to conventional plastics. These solutions are gaining traction among companies focused on sustainability goals and green packaging initiatives.

By Product Type

Lubricant bottles dominated the market in 2024 with approximately 36.9% share. Bottles are widely used in automotive and retail applications due to their convenience and ease of handling. They are available in various sizes and are suitable for engine oils and transmission fluids. Their strong sealing properties help prevent leakage during storage and transportation.

Flexible pouches are expected to grow at the fastest CAGR of 6.6%. This growth is driven by increasing demand for lightweight and cost-effective packaging solutions. Pouches reduce material usage and transportation costs, making them attractive for bulk lubricant distribution. Their flexibility and compact design support efficient logistics and storage.

By End-Use

The automotive segment dominated the lubricant packaging market in 2024 with approximately 49.2% share. This dominance is driven by high lubricant consumption in passenger and commercial vehicles. Regular maintenance requirements ensure continuous demand for lubricant packaging solutions. Packaging plays a key role in ensuring product safety and ease of use during servicing.

Industrial machinery is expected to grow at the fastest CAGR of 6.3%. Growth in manufacturing and construction sectors is driving demand for lubricants used in heavy machinery. Packaging solutions in this segment must provide durability and chemical resistance for bulk handling applications.

Lubricant Packaging Market Segmentations

By Packaging Type

- Plastic Containers

- Metal Containers

- Flexible Packaging

- Biodegradable Packaging

By Product Type

- Bottles

- Drums

- Jerry Cans

- Pouches

By End-Use

- Automotive

- Industrial Machinery

- Marine

- Aerospace

Regional Analysis

North America

North America accounted for approximately 22.7% of the lubricant packaging market share in 2025 and is expected to grow at a CAGR of 5.4%. The region benefits from a mature automotive industry and strong industrial base. Demand for lubricant packaging is driven by high vehicle ownership rates and well-established manufacturing activities. Sustainability initiatives are also influencing packaging innovation across the region.

The United States dominates the market due to its large automotive fleet and industrial maintenance requirements. A key growth factor is the increasing adoption of advanced packaging materials that support environmental compliance and operational efficiency.

Europe

Europe held a 20.9% market share in 2025 and is projected to grow at a CAGR of 5.6%. The region is driven by strict environmental regulations and strong automotive manufacturing presence. Demand for eco-friendly lubricant packaging is increasing across industries.

Germany leads the European market due to its strong automotive and machinery manufacturing sectors. A key growth factor is the rising adoption of recyclable and reusable packaging solutions supported by regulatory policies.

Asia Pacific

Asia Pacific dominated the lubricant packaging market with a 38.1% share in 2025 and is expected to grow at a CAGR of 6.8%. Rapid industrialization and vehicle production are key drivers. The region has a strong manufacturing base that supports lubricant consumption.

China is the dominant country due to its large-scale industrial and automotive sectors. A key growth factor is the expansion of manufacturing activities requiring continuous machinery lubrication and packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for 8.3% of the market share in 2025 and is expected to grow at a CAGR of 6.2%. Growth is driven by oil and gas industries and increasing industrial development.

Saudi Arabia leads the region due to its strong petroleum sector. A key growth factor is the high demand for industrial lubricants used in energy and infrastructure projects.

Latin America

Latin America held a 9.9% market share in 2025 and is projected to grow at the fastest CAGR of 6.5%. The region is experiencing industrial growth and increasing automotive demand.

Brazil dominates the market due to its large automotive and industrial base. A key growth factor is expanding manufacturing activity that increases lubricant consumption.

Competitive Landscape

The lubricant packaging market is moderately competitive with several global players focusing on innovation, sustainability, and material efficiency. Companies such as Amcor plc, Berry Global Inc., and Greif Inc. are leading the market with strong product portfolios and global distribution networks. These companies are investing in recyclable packaging materials and lightweight container designs to improve operational efficiency.

Amcor plc remains a key leader in the market due to its advanced packaging technologies and global presence. The company recently introduced lightweight industrial lubricant containers designed to reduce material usage while improving durability and transport efficiency.

Key Players List

- Amcor plc

- Berry Global Inc.

- Greif Inc.

- Sonoco Products Company

- Mondi Group

- Sealed Air Corporation

- Huhtamaki Group

- DS Smith plc

- Smurfit Kappa Group

- RPC Group (Berry Global)

- Nampak Ltd.

- ALPLA Group

- Time Technoplast Ltd.

- Balmer Lawrie & Co. Ltd.

- SCHÜTZ GmbH & Co. KGaA