Recycled Containerboard Market Size and Growth

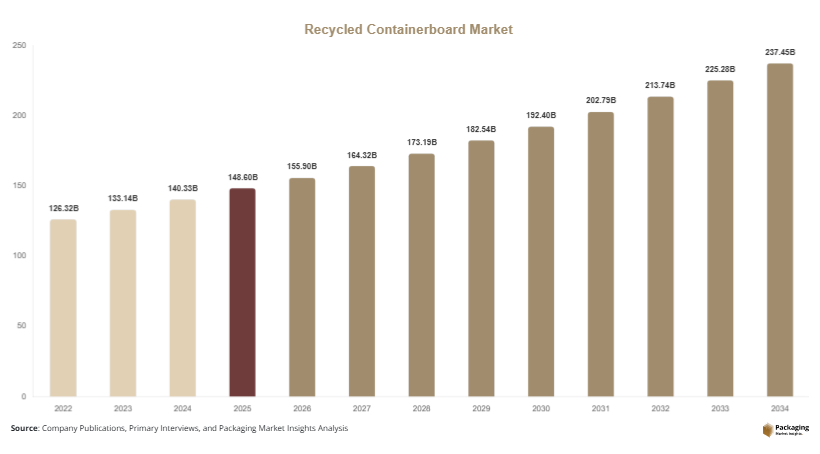

The global recycled containerboard market size was valued at approximately USD 148.6 billion in 2025 and is projected to reach USD 155.9 billion in 2026. The market is expected to attain a value of nearly USD 236.8 billion by 2034, registering a CAGR of 5.4% during the forecast period (2025–2034). Market growth is being supported by increasing recycling rates across developed and developing economies, substantial investments in paper recovery infrastructure, and growing adoption of fiber-based packaging alternatives to plastic packaging.

The recycled containerboard market is experiencing sustained growth as industries increasingly prioritize sustainable packaging solutions and circular economy practices. Recycled containerboard, manufactured primarily from recovered paper and fiber materials, is widely used in corrugated boxes, retail-ready packaging, shipping containers, and industrial packaging applications. Growing environmental regulations, rising consumer preference for eco-friendly products, and the expansion of e-commerce activities are contributing significantly to market demand worldwide.

Key Market Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.3% through 2034.

- Recycled linerboard led the type segment with a 42.8% share.

- Old corrugated containers (OCC) dominated the material segment with a 54.6% share.

- Food & beverage applications led the end-use segment with 37.9% share.

- The US remained the dominant country with a market size of USD 27.8 billion in 2025 and USD 29.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Lightweight Containerboard Solutions

Containerboard manufacturers are increasingly focusing on lightweight recycled grades that deliver comparable strength while reducing raw material consumption and transportation costs. Packaging producers are adopting advanced fiber engineering techniques to optimize board performance without increasing basis weight. Retailers and logistics companies are actively seeking packaging solutions that lower shipping expenses and reduce carbon emissions throughout the supply chain.

For example, several packaging converters have introduced lightweight corrugated box designs for e-commerce shipments while maintaining stacking strength and product protection. This trend is expected to gain further momentum as transportation costs rise and sustainability metrics become more important in procurement decisions. Over the forecast period, lightweight recycled containerboard products are likely to improve operational efficiency while supporting environmental objectives across multiple industries.

Expansion of Closed-Loop Recycling Programs

The development of closed-loop recycling systems is becoming a significant trend within the recycled containerboard market. Large retailers, e-commerce platforms, and packaging manufacturers are collaborating to recover used corrugated packaging and reintroduce fibers into production cycles. These initiatives help secure raw material supply while reducing landfill waste and improving resource efficiency.

For instance, major distribution centers increasingly collect used corrugated boxes and return them to recycling facilities for reprocessing into new containerboard products. This approach strengthens circular economy models and helps companies achieve sustainability targets. Looking ahead, increasing investment in collection infrastructure, digital waste-tracking systems, and automated sorting technologies is expected to enhance fiber recovery rates and support long-term market growth.

Market Drivers

Rapid Growth of E-Commerce Packaging Demand

The expansion of global e-commerce activities continues to drive significant demand for recycled containerboard products. Online retail transactions require extensive use of corrugated packaging to ensure safe transportation of goods across complex logistics networks. As parcel volumes increase, packaging manufacturers require larger quantities of recycled containerboard to meet demand efficiently.

The cause-and-effect relationship is clear: rising online shopping activity directly increases corrugated box consumption, which subsequently boosts demand for recycled containerboard production. For example, large fulfillment centers handling millions of daily shipments rely heavily on recycled fiber packaging solutions due to cost-effectiveness and sustainability benefits. As cross-border e-commerce and direct-to-consumer business models continue expanding, this driver is expected to remain a major contributor to market growth.

Regulatory Support for Sustainable Packaging

Governments worldwide are implementing policies that encourage recycling, reduce landfill waste, and restrict the use of certain plastic packaging materials. These regulations are creating favorable conditions for recycled containerboard manufacturers and packaging converters. Many jurisdictions now require minimum recycled content levels or promote extended producer responsibility programs.

For example, several countries have introduced packaging waste reduction targets that encourage the use of recyclable fiber-based materials. As a result, brand owners are increasingly incorporating recycled containerboard into their packaging portfolios. This regulatory environment is accelerating investment in recycling infrastructure and supporting long-term demand for recycled paper packaging products across multiple industries.

Market Restraint

Volatility in Recovered Paper Supply and Pricing

One of the major restraints affecting the recycled containerboard market is the volatility associated with recovered paper availability and pricing. Recycled containerboard production depends heavily on a consistent supply of recovered fiber materials such as old corrugated containers and mixed paper waste. Fluctuations in collection rates, trade restrictions, contamination levels, and seasonal waste generation patterns can disrupt supply chains and increase production costs.

This challenge impacts manufacturers by creating uncertainty in raw material procurement and operational planning. For example, periods of reduced paper recovery can lead to significant increases in recovered fiber prices, compressing profit margins for containerboard producers. Additionally, contamination in collected waste streams often requires additional processing, increasing operational expenses. Smaller manufacturers may face greater difficulties managing these fluctuations compared to larger integrated companies with established recycling networks. Although investments in collection infrastructure and automated sorting technologies are helping address these issues, raw material volatility remains a persistent challenge for industry participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 148.6 Billion |

| Market Size in 2026 | USD 155.9 Billion |

| Market Size in 2034 | USD 236.8 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Recycled linerboard dominated the market in 2024, accounting for approximately 42.8% of total market share. The segment maintains leadership due to its extensive use as the outer facing material in corrugated packaging applications. Recycled linerboard offers a balance of strength, printability, and cost efficiency, making it suitable for shipping containers, retail-ready packaging, and industrial transport boxes. The growing need for sustainable packaging across e-commerce, food distribution, and consumer goods sectors has further reinforced its market position. Manufacturers continue investing in advanced production technologies to improve fiber bonding and board performance while maintaining high recycled content levels.

Recycled white-top containerboard is projected to be the fastest-growing subsegment, expanding at a CAGR of 6.7% through 2034. Growth is driven by increasing demand for premium graphics and branding capabilities in retail packaging applications. Companies are seeking packaging materials that combine sustainability with enhanced visual appeal. Innovations in coating technologies and printing compatibility are supporting adoption across food, beverage, and consumer products sectors. Future demand is expected to increase as brands continue shifting toward environmentally responsible packaging solutions that also support marketing objectives.

By Material

Old Corrugated Containers (OCC) represented the dominant material segment in 2024, holding approximately 54.6% market share. OCC remains the preferred raw material due to its widespread availability, established collection systems, and favorable fiber characteristics. The material is extensively used in recycled containerboard manufacturing because it provides strong fiber recovery potential and supports high-performance corrugated packaging production. Large-scale recovery programs implemented by retailers, warehouses, and municipalities ensure a consistent supply of OCC feedstock. Continued improvements in collection and sorting technologies are further strengthening the segment's market position.

Mixed recovered paper is expected to register the fastest growth, with a projected CAGR of 6.1% during the forecast period. Increasing efforts to maximize recycling efficiency are encouraging manufacturers to process a broader range of recovered paper streams. Advanced fiber separation technologies are improving the quality of mixed-paper feedstocks, enabling wider use in containerboard production. Growing sustainability initiatives and investments in recycling infrastructure are expected to expand utilization rates. Future opportunities are likely to emerge as producers seek diversified raw material sources to enhance supply security.

By End-Use

The food & beverage industry dominated the end-use segment in 2024, accounting for approximately 37.9% of market share. The segment benefits from extensive demand for transport packaging, retail-ready packaging, and bulk distribution containers. Food producers increasingly utilize recycled containerboard packaging to align with sustainability objectives and regulatory requirements. Corrugated packaging provides product protection, logistical efficiency, and recyclability, making it highly suitable for food supply chains. Growth in packaged food consumption and organized retail channels continues supporting segment leadership.

E-commerce packaging is projected to be the fastest-growing end-use category, expanding at a CAGR of 7.0% through 2034. The growth is driven by rising online shopping activity, increasing parcel shipments, and expanding digital retail platforms worldwide. Packaging providers are developing innovative containerboard solutions optimized for shipping performance, lightweight construction, and sustainability. Demand from electronics, apparel, household goods, and direct-to-consumer brands is expected to accelerate adoption. As e-commerce penetration increases globally, the segment is likely to become one of the most significant contributors to future market expansion.

Recycled Containerboard Market Segmentations

By Type

- Recycled Linerboard

- Recycled Medium

- Recycled White-Top Containerboard

By Material

- Old Corrugated Containers (OCC)

- Mixed Recovered Paper

- Newspapers & Magazines

- Other Recovered Fibers

By End-User

- Food & Beverage

- E-Commerce Packaging

- Consumer Goods

- Electronics

- Industrial Packaging

- Healthcare

Regional Analysis

North America

North America accounted for approximately 27.8% of the global recycled containerboard market share in 2025 and is expected to expand at a CAGR of 4.9% through 2034. The region benefits from mature recycling infrastructure, strong corrugated packaging demand, and high recovery rates for paper-based materials. Growing online retail sales continue to generate substantial demand for shipping boxes manufactured from recycled fibers. In addition, sustainability commitments from major consumer goods companies are encouraging broader adoption of recycled packaging materials throughout supply chains. Investments in modern paper mills and advanced recycling technologies further support regional market expansion.

The United States remains the dominant market within North America. A unique growth driver is the increasing deployment of automated fulfillment centers requiring standardized corrugated packaging solutions. Major retailers are implementing packaging optimization programs that prioritize recycled fiber content while reducing packaging weight. The growing trend toward same-day and next-day delivery services has increased demand for durable shipping containers, supporting higher consumption of recycled containerboard across domestic logistics networks.

Europe

Europe represented approximately 24.6% of global market share in 2025 and is projected to register a CAGR of 5.0% during the forecast period. The region benefits from stringent environmental regulations, advanced waste management systems, and high consumer awareness regarding sustainable packaging. Growing adoption of circular economy principles has encouraged manufacturers to increase recycled fiber utilization. Retail packaging demand remains strong, particularly across food distribution, consumer goods, and industrial sectors. Investments in recycling efficiency and fiber recovery technologies continue strengthening regional production capabilities.

Germany leads the European market due to its established paper recycling infrastructure and strong manufacturing base. A unique growth driver is the increasing adoption of paper-based transport packaging by industrial exporters seeking to meet environmental compliance standards. Many European manufacturers are replacing plastic transport packaging with recycled containerboard solutions. Industry initiatives promoting high recycling rates and fiber recovery have further reinforced Germany's position as a leading market for recycled containerboard products.

Asia Pacific

Asia Pacific dominated the market with a 39.1% share in 2025 and is anticipated to expand at a CAGR of 6.1% through 2034. Rapid industrialization, urbanization, and growing consumer spending are driving substantial packaging demand across the region. Expanding manufacturing activities and increasing e-commerce penetration have significantly boosted corrugated packaging consumption. Governments are also encouraging waste recycling and sustainable packaging adoption, creating favorable market conditions. Large-scale investments in paper production facilities and recycling infrastructure continue supporting regional market growth.

China remains the dominant country within Asia Pacific. A unique growth driver is the expansion of domestic manufacturing exports requiring cost-effective shipping and transport packaging. Chinese packaging producers are increasing production capacity to meet demand from electronics, consumer goods, and industrial sectors. Furthermore, investments in advanced paper recycling facilities are improving fiber utilization rates and supporting sustainable packaging development throughout the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.9% of market share in 2025 and is forecast to grow at a CAGR of 5.5% during the assessment period. Economic diversification initiatives, expanding retail sectors, and increasing packaging requirements are contributing to regional demand. Improvements in recycling awareness and investments in waste collection systems are gradually strengthening the supply of recovered paper materials. Growing food imports and industrial development are also creating opportunities for corrugated packaging manufacturers.

The United Arab Emirates represents the leading market in the region. A unique growth driver is the rapid development of logistics and distribution hubs serving international trade routes. Warehousing and re-export activities require significant quantities of corrugated transport packaging. Businesses operating in free trade zones are increasingly adopting recycled containerboard solutions to support sustainability goals while meeting packaging performance requirements.

Latin America

Latin America held approximately 3.6% of global market share in 2025 and is expected to achieve the fastest regional CAGR of 6.3% through 2034. Rising consumer goods production, expanding retail networks, and increasing agricultural exports are stimulating demand for recycled packaging materials. Several countries are investing in recycling infrastructure to improve waste collection rates and reduce landfill dependence. Growth in food processing industries is also supporting broader use of corrugated packaging products.

Brazil dominates the Latin American market. A unique growth driver is the expansion of agricultural exports requiring durable and sustainable packaging for domestic and international transportation. Fruit, meat, and processed food exporters increasingly rely on recycled containerboard packaging to maintain product integrity while meeting environmental requirements from overseas buyers. This trend is expected to strengthen future market growth across the country.

Competitive Landscape

The recycled containerboard market is characterized by the presence of several global and regional manufacturers competing through capacity expansion, recycling investments, product innovation, and strategic partnerships. International Paper Company remains a leading participant due to its extensive recycling network, integrated manufacturing operations, and broad product portfolio.

Other major companies including Smurfit Westrock, DS Smith, Mondi Group, and Packaging Corporation of America are focusing on sustainable packaging development and operational efficiency improvements. Companies are increasingly investing in modern paper mills, fiber recovery systems, and lightweight containerboard technologies to enhance competitiveness. Strategic acquisitions are also being used to strengthen regional market presence and secure raw material supply chains.

Recent developments across the industry include capacity expansion projects, investments in circular economy initiatives, and adoption of digital manufacturing technologies. Leading players are emphasizing recycled fiber utilization and carbon reduction strategies to align with customer sustainability requirements and evolving environmental regulations.

Key Players

- International Paper Company

- Smurfit Westrock

- DS Smith Plc

- Mondi Group

- Packaging Corporation of America

- Nine Dragons Paper Holdings

- Lee & Man Paper Manufacturing

- Pratt Industries

- Stora Enso Oyj

- Nippon Paper Industries

- Oji Holdings Corporation

- Svenska Cellulosa Aktiebolaget (SCA)

- Cascades Inc.

- Klabin S.A.

- Rengo Co., Ltd.

- Georgia-Pacific LLC

- Mayr-Melnhof Karton AG