Flexible Foam Packaging Market Size and Growth

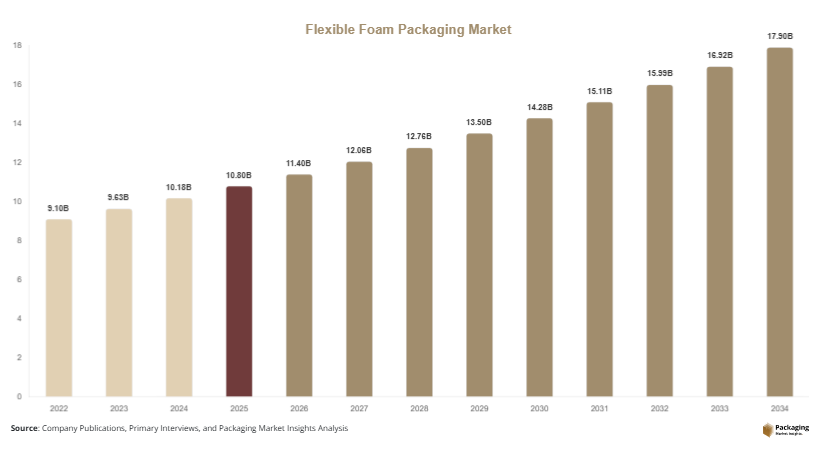

The global flexible foam packaging market size was valued at USD 10.8 billion in 2025 and is estimated to reach USD 11.4 billion in 2026. The market is projected to attain approximately USD 17.9 billion by 2034, registering a CAGR of 5.8% during the forecast period (2025–2034). Growth is being driven by rising online retail shipments, increasing demand for protective packaging in electronics manufacturing, and expanding pharmaceutical distribution networks. In addition, manufacturers are investing in recyclable and bio-based foam materials to address sustainability concerns and regulatory requirements.

The flexible foam packaging market is witnessing steady expansion as industries increasingly adopt lightweight, shock-absorbing, and cost-efficient packaging solutions for product protection and transportation. Flexible foam packaging materials are widely used across electronics, automotive components, healthcare products, consumer goods, and industrial equipment due to their ability to cushion delicate products and reduce damage during storage and transit. The growing importance of e-commerce logistics and global supply chain activities continues to support demand for advanced foam-based protective packaging.

Key Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.5% through 2034.

- Polyurethane foam led the type segment with a 41.7% share.

- Polyethylene material dominated the market with a 46.2% share.

- Electronics & consumer goods applications led the segment with a 35.4% share.

- The US remained the dominant country with a market size of USD 2.4 billion in 2025 and USD 2.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Foam Packaging Solutions

Sustainability is becoming a central focus in the flexible foam packaging market. Manufacturers are increasingly developing recyclable, reusable, and bio-based foam materials to reduce environmental impact while maintaining protective performance. Many packaging suppliers are introducing polyethylene and polyurethane foams containing recycled content to meet customer sustainability goals and regulatory requirements. For example, several electronics packaging providers now utilize recycled foam inserts for consumer electronics shipments. This trend is expected to accelerate as governments implement stricter waste reduction policies and corporations pursue circular economy initiatives. Future developments in biodegradable foams and closed-loop recycling systems are likely to reshape product design and material selection across the industry.

Expansion of Customized Protective Packaging for E-Commerce

The rapid growth of e-commerce is driving demand for customized flexible foam packaging designed to protect products during long-distance transportation. Online retailers require packaging solutions that minimize damage while reducing shipping costs and material usage. Flexible foam inserts, die-cut foam sheets, and molded cushioning products are increasingly being tailored to product dimensions and fragility levels. Consumer electronics, home appliances, and luxury goods are major adopters of customized foam solutions. Looking ahead, digital manufacturing technologies and automated packaging systems are expected to enhance customization capabilities, allowing suppliers to provide highly efficient and scalable protective packaging solutions for diverse product categories.

Market Drivers

Rising Demand for Electronics and Consumer Goods Protection

The increasing production and shipment of electronics and consumer goods are major drivers of the flexible foam packaging market. Smartphones, laptops, gaming devices, and home appliances require reliable protective packaging to prevent damage during transportation and storage. Flexible foam materials provide cushioning, shock absorption, and vibration resistance, making them suitable for fragile products. As global electronics manufacturing continues to expand, packaging demand is growing proportionally. For example, rising exports of consumer electronics from Asia Pacific manufacturing hubs have increased the use of polyethylene and polyurethane foam packaging. This trend supports long-term market growth as product protection remains a critical requirement across supply chains.

Expansion of Pharmaceutical and Medical Device Logistics

The healthcare industry is generating substantial demand for flexible foam packaging solutions. Medical devices, diagnostic equipment, and temperature-sensitive pharmaceutical products require secure packaging during transportation. Flexible foams offer excellent cushioning properties that reduce damage risks and improve product safety. Growth in healthcare spending, pharmaceutical exports, and medical device manufacturing is supporting market expansion. For instance, healthcare distributors increasingly use customized foam inserts to protect diagnostic instruments and surgical equipment. As healthcare supply chains become more globalized and regulatory standards become stricter, demand for advanced protective foam packaging solutions is expected to increase significantly.

Market Restraint

Environmental Concerns Related to Conventional Foam Materials

Despite strong market growth, environmental concerns surrounding conventional foam materials remain a significant restraint. Many flexible foam packaging products are derived from petroleum-based polymers that can be difficult to recycle and may contribute to landfill waste. Regulatory authorities in several countries are introducing restrictions on single-use plastics and non-recyclable packaging materials, creating compliance challenges for manufacturers. These regulations can increase production costs as companies invest in sustainable alternatives and recycling infrastructure.

For example, packaging producers supplying European markets must increasingly comply with extended producer responsibility programs and packaging waste regulations. Small and medium-sized manufacturers may face financial pressure when transitioning to recyclable or bio-based materials. In addition, fluctuations in raw material prices can further impact profitability. Although sustainable foam technologies are emerging, achieving the same performance characteristics and cost competitiveness as conventional products remains a challenge. As a result, environmental concerns and regulatory pressures continue to influence purchasing decisions and market dynamics across multiple regions.

Market Opportunities

Development of Bio-Based and Recyclable Foam Materials

The growing focus on sustainability presents significant opportunities for innovation in bio-based and recyclable flexible foam packaging. Manufacturers are investing in renewable raw materials and advanced recycling technologies to create environmentally responsible packaging products. Bio-based foams derived from plant-based feedstocks are attracting interest from consumer goods, electronics, and healthcare companies seeking sustainable packaging alternatives. These solutions can help reduce carbon footprints while meeting regulatory requirements. As material performance improves and production costs decline, adoption is expected to increase across various industries. Future opportunities also include closed-loop recycling systems that enable the recovery and reuse of foam materials.

Growth of Cold Chain and Healthcare Packaging Applications

The expansion of temperature-sensitive logistics offers another promising opportunity for the flexible foam packaging market. Pharmaceutical products, vaccines, biotechnology samples, and specialty medical devices require protective packaging that maintains product integrity throughout transportation. Flexible foam materials provide insulation and cushioning benefits that support cold chain operations. Growing investments in healthcare infrastructure and pharmaceutical manufacturing are increasing demand for specialized packaging solutions. Emerging markets are also expanding healthcare distribution networks, creating new opportunities for suppliers. As biologics and personalized medicines become more common, advanced foam packaging solutions designed for temperature-sensitive applications are expected to gain broader adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10.8 Billion |

| Market Size in 2026 | USD 11.4 Billion |

| Market Size in 2034 | USD 17.9 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polyurethane foam dominated the market in 2024 with a share of approximately 41.7%. Its leadership position is attributed to excellent cushioning performance, flexibility, and durability. Polyurethane foams are widely used in electronics, industrial equipment, medical devices, and consumer goods packaging. Manufacturers favor these materials because they provide reliable shock absorption while remaining lightweight. The increasing transportation of fragile products has strengthened demand for polyurethane-based packaging solutions across global supply chains.

Bio-based flexible foams are projected to be the fastest-growing subsegment, registering a CAGR of 7.1% through 2034. Growth is driven by sustainability initiatives, regulatory compliance requirements, and consumer demand for environmentally responsible packaging. Companies are investing in renewable feedstocks and advanced manufacturing technologies to improve product performance. As commercialization expands and production costs decline, bio-based foam adoption is expected to accelerate across multiple industries.

By Material

Polyethylene represented the largest material segment in 2024, accounting for approximately 46.2% of market revenue. Polyethylene foams offer moisture resistance, impact protection, and lightweight characteristics, making them suitable for electronics, automotive, and industrial applications. The material's versatility and cost-effectiveness have contributed to widespread adoption. Manufacturers continue to develop improved polyethylene formulations that enhance durability and protective performance while supporting operational efficiency.

Recycled polymer foams are expected to witness the fastest growth, with a forecast CAGR of 6.8%. Rising sustainability goals and circular economy initiatives are encouraging the use of recycled materials in packaging applications. Packaging companies are increasingly incorporating recycled content into foam products to reduce environmental impact and meet customer expectations. Future growth is expected to be supported by improved recycling technologies and stronger regulatory support for recycled packaging materials.

By End-Use

Electronics & consumer goods emerged as the leading end-use segment in 2024, holding approximately 35.4% market share. The segment benefits from high shipment volumes of fragile products requiring protective packaging during storage and transportation. Flexible foam packaging minimizes vibration and impact damage while maintaining product quality. Increasing demand for smartphones, laptops, home appliances, and wearable devices continues to support segment growth. Manufacturers frequently utilize customized foam inserts to improve packaging efficiency and product protection.

Healthcare is expected to be the fastest-growing end-use segment, expanding at a CAGR of 7.0% through 2034. Growth is driven by increasing pharmaceutical production, medical device shipments, and cold chain logistics requirements. Flexible foam packaging solutions help protect sensitive healthcare products and maintain quality throughout transportation. The expansion of biotechnology products and personalized medicine is expected to create additional opportunities for specialized healthcare packaging applications.

Flexible Foam Packaging Market Segmentations

By Type

- Polyurethane Foam

- Polyethylene Foam

- Expanded Polypropylene Foam

- Expanded Polystyrene Foam

- Other Flexible Foams

By Material

- Petroleum-Based Foam

- Recycled Foam

- Bio-Based Foam

By End-User

- Electronics

- Automotive

- Food & Beverage

- Healthcare & Pharmaceuticals

- Consumer Goods

- Industrial Products

- E-Commerce & Logistics

Regional Analysis

North America

North America accounted for approximately 28.4% of the flexible foam packaging market in 2025 and is projected to grow at a CAGR of 5.4% through 2034. The region benefits from strong demand across e-commerce, healthcare, electronics, and industrial sectors. Advanced logistics infrastructure and high consumer spending support continuous packaging innovation. The growing need for protective packaging solutions for high-value products is encouraging investments in customized foam technologies. Sustainability initiatives and corporate commitments to packaging waste reduction are also influencing product development and procurement strategies across the region.

The United States dominates the regional market due to its large e-commerce industry and extensive manufacturing base. A unique growth driver is the rapid expansion of automated fulfillment centers requiring efficient protective packaging solutions. Many retailers and logistics providers are integrating customized foam packaging into automated packing lines to reduce product damage and operational costs. Increasing healthcare shipments and medical device exports further strengthen demand.

Europe

Europe held approximately 24.6% market share in 2025 and is expected to register a CAGR of 5.3% during the forecast period. Demand is supported by strict packaging regulations, advanced manufacturing industries, and increasing sustainability initiatives. Companies across the region are investing in recyclable and reusable packaging materials to comply with environmental targets. The automotive and electronics industries continue to generate substantial demand for protective foam packaging solutions. Growth is also supported by cross-border trade activities and expanding e-commerce operations.

Germany represents the largest market within Europe. A unique growth driver is the country's strong industrial export sector, which requires durable packaging for machinery components and precision equipment. German manufacturers increasingly utilize engineered foam packaging to protect high-value exports during international transportation. This trend is supporting ongoing demand for advanced flexible foam products throughout the country.

Asia Pacific

Asia Pacific dominated the market with a 38.1% share in 2025 and is forecast to grow at a CAGR of 6.3% through 2034. The region benefits from rapid industrialization, strong electronics production, and expanding consumer goods manufacturing. Rising online retail activity and increasing export volumes are generating significant demand for protective packaging solutions. Investments in manufacturing facilities and logistics infrastructure continue to strengthen market growth. Countries across the region are also adopting sustainable packaging technologies to address environmental concerns.

China remains the leading market in Asia Pacific. A unique growth driver is the country's position as a global electronics manufacturing hub. The export of smartphones, computers, and consumer electronics requires large volumes of protective foam packaging. Manufacturers are increasingly developing lightweight and recyclable foam materials to support sustainability objectives while maintaining product protection standards.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.8% of global market share in 2025 and is projected to expand at a CAGR of 5.7%. Economic diversification programs, industrial development initiatives, and expanding retail sectors are supporting market growth. Increasing imports of consumer goods and medical products are generating demand for protective packaging solutions. Investments in logistics hubs and transportation infrastructure are also enhancing distribution capabilities across the region.

Saudi Arabia leads the regional market. A unique growth driver is the expansion of industrial manufacturing under economic diversification strategies. Industrial equipment and automotive component transportation require durable foam packaging to prevent damage during transit. The growth of regional warehousing and logistics operations is creating additional demand for customized protective packaging solutions.

Latin America

Latin America represented approximately 4.1% of the market in 2025 and is anticipated to grow at the fastest CAGR of 6.5% through 2034. Expanding retail sectors, increasing industrial production, and rising e-commerce activity are contributing to market growth. Consumer demand for electronics and household products is supporting protective packaging requirements. Growing investments in logistics infrastructure are improving distribution networks and facilitating market expansion across multiple countries.

Brazil dominates the Latin American market. A unique growth driver is the growth of domestic e-commerce and parcel delivery services. Online retailers increasingly rely on flexible foam packaging to protect products during transportation across large geographic distances. Rising demand for consumer electronics and healthcare products is expected to support continued growth throughout the forecast period.

Competitive Landscape

The flexible foam packaging market is moderately consolidated, with leading participants focusing on product innovation, sustainability, strategic acquisitions, and capacity expansion. Major companies are investing in recyclable materials and customized packaging solutions to strengthen their competitive positions. Partnerships with logistics providers, healthcare companies, and electronics manufacturers remain common strategies for expanding market reach.

Sealed Air Corporation is recognized as a market leader due to its broad product portfolio, global presence, and continuous investment in protective packaging innovation. Recently, the company expanded its sustainable packaging offerings by introducing packaging solutions containing higher levels of recycled content.

Other major companies include Pregis LLC, JSP Corporation, Zotefoams plc, and FoamPartner Group. These firms continue to focus on advanced foam technologies, sustainable product development, and regional expansion strategies. Industry competition is expected to intensify as demand for eco-friendly and high-performance packaging solutions increases across global markets.

Key Players List

- Sealed Air Corporation

- Pregis LLC

- JSP Corporation

- Zotefoams plc

- FoamPartner Group

- Sonoco Products Company

- ACH Foam Technologies

- UFP Technologies Inc.

- Rogers Corporation

- Recticel NV

- Armacell International S.A.

- Wisconsin Foam Products

- Kaneka Corporation

- BASF SE

- DS Smith plc