Corrugated Board Packaging Market Size and Growth

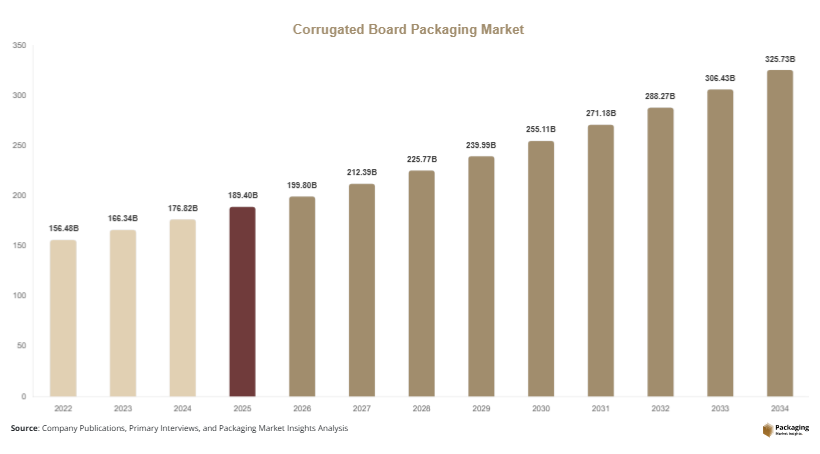

The global corrugated board packaging market size was valued at USD 189.4 billion in 2025 and is projected to reach USD 199.8 billion in 2026. The market is forecast to attain approximately USD 324.7 billion by 2034, registering a CAGR of 6.3% during the forecast period (2025–2034). Corrugated packaging remains a preferred solution for manufacturers and retailers due to its versatility, cost efficiency, and strong protective properties during transportation.

The corrugated board packaging market continues to experience robust growth due to increasing demand for sustainable, lightweight, and cost-effective packaging solutions across various industries. Corrugated board packaging is widely used for shipping, storage, retail display, and product protection applications owing to its durability, recyclability, and adaptability. The rapid expansion of e-commerce, increasing demand for consumer goods, and the shift toward environmentally friendly packaging alternatives are key factors supporting market expansion globally.

Key Market Highlights

- Asia Pacific dominated the market with a 39.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Single-wall corrugated board led the type segment with a 52.8% share.

- Recycled paper material dominated the market with a 58.2% share.

- Food & beverage applications led the end-use segment with a 34.7% share.

- The US remained the dominant country with a market size of USD 32.8 billion in 2025 and USD 34.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Digital Printing in Corrugated Packaging

Digital printing technology is transforming the corrugated board packaging industry by enabling high-quality graphics, shorter production runs, and enhanced customization capabilities. Brand owners are increasingly using digitally printed corrugated boxes to improve shelf appeal and strengthen customer engagement. For example, consumer goods manufacturers are utilizing personalized packaging designs for promotional campaigns and seasonal product launches. Digital printing also reduces setup costs and production waste compared to traditional printing methods. Looking ahead, advancements in printing technology are expected to enable more sophisticated packaging designs and smart packaging features, supporting broader adoption across retail, food, and e-commerce applications.

Rising Demand for Sustainable and Lightweight Packaging

Sustainability remains a defining trend in the corrugated board packaging market. Manufacturers are developing lightweight corrugated structures that reduce raw material consumption while maintaining strength and durability. For instance, major packaging suppliers are introducing lightweight corrugated solutions for e-commerce shipments to reduce transportation costs and carbon emissions. Consumers and retailers increasingly prefer packaging with higher recycled content and lower environmental impact. Future developments are likely to include enhanced fiber recovery systems, improved recyclability, and innovative paper-based alternatives to plastic packaging. This trend is expected to strengthen as environmental regulations become more stringent globally.

Market Drivers

Rapid Expansion of Global E-Commerce

The continued growth of online retailing is a major driver of the corrugated board packaging market. Every e-commerce shipment requires protective packaging, creating sustained demand for corrugated boxes and related products. As online shopping volumes increase, logistics providers and retailers require packaging solutions that offer durability, cost efficiency, and product protection. For example, large e-commerce platforms ship billions of packages annually using corrugated packaging. The direct relationship between rising parcel shipments and corrugated packaging demand continues to support market growth. Future expansion of cross-border e-commerce and direct-to-consumer sales channels is expected to further increase packaging requirements worldwide.

Growing Preference for Sustainable Packaging Materials

Increasing environmental concerns are driving businesses to replace plastic packaging with recyclable paper-based alternatives. Corrugated board packaging is widely recognized as a sustainable solution due to its renewable raw materials and high recyclability rates. Many multinational companies have established sustainability goals that prioritize paper-based packaging adoption. For example, food and beverage manufacturers are replacing plastic secondary packaging with corrugated alternatives. This shift creates strong demand throughout the packaging value chain. As environmental regulations continue to evolve and consumer awareness grows, corrugated board packaging is expected to gain further market share across multiple industries.

Market Restraint

Fluctuations in Raw Material Prices and Fiber Availability

A major restraint affecting the corrugated board packaging market is the volatility in raw material costs, particularly recycled paper and virgin fiber supplies. Corrugated packaging manufacturers depend heavily on paper-based raw materials, and fluctuations in supply can significantly affect production costs. Factors such as changes in recycling rates, trade policies, transportation costs, and energy prices often influence fiber availability and pricing.

For example, disruptions in recovered paper collection systems can lead to shortages and higher procurement costs for packaging producers. These price fluctuations can reduce profit margins and create challenges for long-term production planning. Smaller manufacturers may be particularly vulnerable due to limited purchasing power. Although investments in recycling infrastructure and fiber recovery technologies are helping improve supply stability, raw material cost volatility remains a significant challenge for the industry and may impact pricing strategies throughout the forecast period.

Market Opportunities

Expansion of Retail-Ready Packaging Solutions

Retail-ready packaging is creating significant opportunities for corrugated board manufacturers. Retailers increasingly seek packaging formats that simplify inventory management, improve shelf presentation, and reduce labor costs. Corrugated packaging is well-suited for these applications due to its structural flexibility and printability. For example, supermarkets are adopting shelf-ready corrugated trays for beverage and packaged food displays. Future opportunities are expected to emerge from increasing automation in retail environments and demand for efficient merchandising solutions. Packaging suppliers that offer customized retail-ready formats are likely to gain a competitive advantage.

Growth of Sustainable Packaging in Emerging Markets

Emerging economies represent substantial growth opportunities for the corrugated board packaging market. Rising industrialization, urbanization, and consumer spending are increasing demand for packaged goods across Asia Pacific, Latin America, and Africa. Governments in several countries are introducing policies to reduce plastic waste, encouraging adoption of recyclable packaging materials. For instance, consumer goods manufacturers in India and Southeast Asia are increasingly shifting toward corrugated packaging solutions. Future growth is expected to be supported by expanding retail networks, rising e-commerce penetration, and investments in domestic packaging production facilities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 189.4 Billion |

| Market Size in 2026 | USD 199.8 Billion |

| Market Size in 2034 | USD 324.7 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Single-wall corrugated board dominated the market in 2024, accounting for approximately 52.8% of total market share. This segment leads because it offers an effective balance between strength, weight, and cost efficiency. Single-wall boards are widely used for shipping consumer goods, electronics, food products, and retail merchandise. Manufacturers favor this format due to its versatility and compatibility with high-volume production processes. For example, e-commerce companies rely heavily on single-wall corrugated boxes for parcel deliveries. Continuous improvements in board strength and lightweight design have further enhanced segment performance. Growing demand for cost-effective packaging solutions is expected to sustain segment leadership throughout the forecast period.

Double-wall corrugated board is projected to be the fastest-growing subsegment, expanding at a CAGR of 7.0% through 2034. Growth is driven by increasing demand for heavy-duty packaging in industrial and export applications. Manufacturers require stronger packaging solutions for transporting machinery, automotive parts, and fragile products. Innovations in corrugated board engineering are improving load-bearing capacity while reducing material consumption. Future demand is expected to increase as international trade volumes expand and supply chains become more complex.

By Material

Recycled paper accounted for approximately 58.2% of market share in 2024, making it the dominant material segment. The widespread availability of recovered fiber and growing emphasis on sustainability have contributed significantly to segment growth. Recycled paper provides a cost-effective raw material source while supporting circular economy objectives. Packaging manufacturers increasingly incorporate recycled content into corrugated products to meet customer sustainability requirements. For example, many consumer goods companies specify minimum recycled fiber content for packaging procurement. Ongoing investments in recycling infrastructure are expected to further strengthen segment dominance.

Virgin kraft paper is expected to be the fastest-growing material segment, registering a CAGR of 6.8% during the forecast period. Demand is driven by applications requiring higher strength, durability, and moisture resistance. Industries such as electronics, industrial goods, and export packaging increasingly utilize virgin kraft-based corrugated products. Future growth will be supported by advancements in sustainable forestry practices and improved paper manufacturing technologies.

By End-Use

The Food & Beverage segment dominated the market in 2024 with approximately 34.7% market share. Corrugated packaging plays a critical role in transporting packaged foods, beverages, fresh produce, and processed products. The segment benefits from growing food consumption, expanding retail distribution networks, and increasing demand for sustainable packaging. Food manufacturers rely on corrugated packaging due to its protective properties, printability, and recyclability. Continued growth in packaged food production is expected to maintain strong demand throughout the forecast period.

E-commerce packaging represents the fastest-growing end-use segment and is projected to expand at a CAGR of 7.5% through 2034. Rising online shopping activity continues to drive demand for shipping containers and protective packaging formats. Packaging suppliers are introducing lightweight, customized, and right-sized corrugated packaging solutions designed specifically for e-commerce logistics. Future growth is expected to be supported by cross-border retail expansion, increasing parcel volumes, and innovations in sustainable shipping packaging.

Corrugated Board Packaging Market Segmentations

By Type

- Single-Wall Corrugated Board

- Double-Wall Corrugated Board

- Triple-Wall Corrugated Board

By Material

- Recycled Paper

- Virgin Kraft Paper

- Mixed Fiber Paper

By End-User

- Food & Beverage

- E-Commerce Packaging

- Consumer Goods

- Electronics

- Healthcare

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 26.8% of the global corrugated board packaging market share in 2025 and is expected to grow at a CAGR of 5.7% through 2034. The region benefits from mature retail markets, strong e-commerce penetration, and advanced packaging infrastructure. Demand remains high across food, beverage, electronics, and consumer goods sectors. Investments in automated packaging operations and sustainable manufacturing practices continue to support market growth. The increasing use of recyclable packaging by major retailers and consumer goods companies is also driving demand for corrugated board products.

The United States dominates the regional market. A unique growth driver is the rapid expansion of same-day and next-day delivery services. Logistics providers require lightweight yet durable packaging solutions capable of protecting products during extensive transportation networks. Major e-commerce companies continue investing in optimized corrugated packaging formats to reduce shipping costs and improve sustainability performance. This trend is expected to support long-term demand for corrugated packaging throughout the country.

Europe

Europe represented approximately 24.5% of global market share in 2025 and is forecast to expand at a CAGR of 5.9% during the forecast period. Strong environmental regulations, advanced recycling systems, and consumer demand for sustainable packaging are key factors supporting growth. Packaging manufacturers are increasingly utilizing recycled fibers to meet sustainability objectives. The region's strong food processing and retail sectors further contribute to corrugated packaging demand. Investments in circular economy initiatives continue strengthening the market landscape.

Germany remains the leading market in Europe. A unique growth driver is the expansion of industrial exports requiring reliable transportation packaging. Manufacturing industries across automotive, machinery, and consumer goods sectors rely heavily on corrugated packaging solutions. Companies are increasingly adopting high-performance corrugated packaging designs to improve logistics efficiency while meeting sustainability targets. This trend continues to reinforce Germany's leadership within the European market.

Asia Pacific

Asia Pacific dominated the global market with a 39.4% share in 2025 and is projected to grow at a CAGR of 7.0% through 2034. Rapid industrialization, urbanization, and rising consumer spending are driving substantial packaging demand throughout the region. Expanding manufacturing activities and increasing exports continue to generate strong requirements for corrugated packaging. Additionally, growing e-commerce penetration across China, India, and Southeast Asia is creating significant opportunities for market participants. Investments in paper production and packaging manufacturing facilities are further supporting regional growth.

China is the dominant country in Asia Pacific. A unique growth driver is the country's extensive manufacturing and export sector. Corrugated packaging is widely used for shipping electronics, consumer goods, and industrial products to global markets. The continued growth of domestic online retail platforms is also increasing packaging demand. Companies are investing in advanced production facilities to meet rising requirements while improving packaging efficiency and sustainability performance.

Middle East & Africa

The Middle East & Africa accounted for approximately 5.1% of market share in 2025 and is expected to grow at a CAGR of 6.5% during the forecast period. Economic diversification, retail expansion, and infrastructure development are supporting packaging demand across the region. Food imports and consumer goods distribution activities continue to create opportunities for corrugated packaging suppliers. Growing awareness of sustainable packaging solutions is also contributing to market development. Investments in logistics and warehousing infrastructure are enhancing packaging consumption.

The United Arab Emirates leads the regional market. A unique growth driver is the country's role as a major trade and logistics hub connecting Asia, Europe, and Africa. Increasing warehousing activities and re-export operations require substantial quantities of corrugated packaging for product transportation. The expansion of e-commerce and retail sectors is further supporting demand. These factors are expected to drive continued market growth in the UAE.

Latin America

Latin America held approximately 4.2% of global market share in 2025 and is projected to register the fastest CAGR of 7.1% through 2034. Growth is being driven by increasing consumption of packaged goods, expanding retail networks, and rising industrial activity. Governments are promoting sustainable packaging practices, encouraging greater use of recyclable materials. The food and beverage industry remains a major consumer of corrugated packaging across the region. Investments in manufacturing and distribution infrastructure continue supporting market expansion.

Brazil dominates the Latin American market. A unique growth driver is the country's growing agricultural export sector. Producers require durable corrugated packaging for fruits, vegetables, processed foods, and other agricultural products destined for domestic and international markets. The increasing focus on export-quality packaging is creating opportunities for packaging manufacturers. This trend is expected to contribute significantly to future market growth.

Competitive Landscape

The corrugated board packaging market is highly competitive, characterized by the presence of multinational packaging companies and regional manufacturers. International Paper Company remains a leading participant due to its integrated operations, extensive production capacity, and strong distribution network.

Other major players include Smurfit Westrock, DS Smith Plc, Mondi Group, and Packaging Corporation of America. These companies are focusing on sustainability initiatives, capacity expansions, and advanced packaging technologies to strengthen market position. Strategic investments in recycling infrastructure and digital printing capabilities are becoming increasingly common.

Recent industry developments include new corrugated production facilities, acquisitions, and product innovation programs focused on lightweight packaging and circular economy solutions. Companies are also partnering with retailers and e-commerce providers to develop customized packaging formats. As sustainability and e-commerce continue shaping market demand, competition is expected to intensify across key regions.

Key Players List

- International Paper Company

- Smurfit Westrock

- DS Smith Plc

- Mondi Group

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries

- Stora Enso Oyj

- Nine Dragons Paper Holdings

- Oji Holdings Corporation

- Nippon Paper Industries

- Cascades Inc.

- Klabin S.A.

- Rengo Co., Ltd.