Carton Liner Market Size and Growth

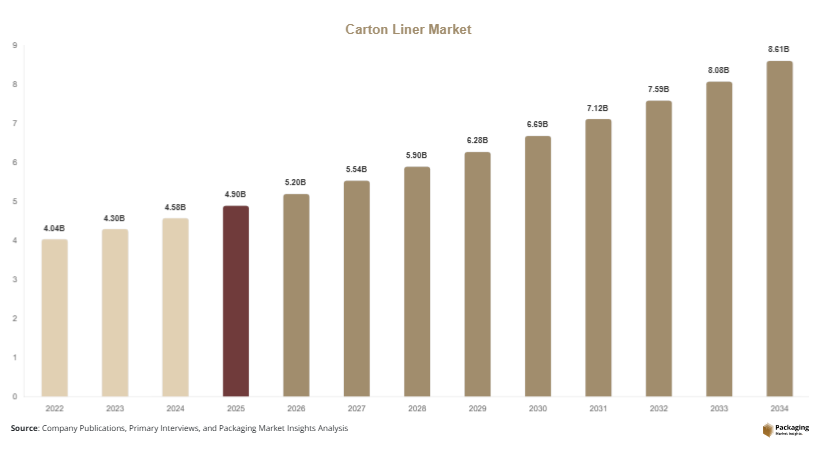

The global carton liner market size was valued at USD 4.9 billion in 2025 and is projected to reach USD 5.2 billion in 2026. By 2034, the market is expected to attain approximately USD 8.6 billion, registering a CAGR of 6.5% during the forecast period (2025–2034).

The carton liner market is witnessing steady growth as industries increasingly prioritize product protection, hygiene, moisture resistance, and supply chain efficiency. Carton liners are protective materials inserted within cartons, boxes, and corrugated packaging systems to safeguard products from contamination, moisture, dust, and physical damage during storage and transportation. These liners are widely used across food and beverage, pharmaceuticals, chemicals, agriculture, consumer goods, and industrial packaging applications.

Key Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.2%.

- Polyethylene liners led the type segment with a 36.8% share.

- Plastic-based materials dominated with a 58.4% share.

- Food & beverage applications led the end-use segment with 42.7% share.

- The US remained the dominant country with a market size of USD 0.95 billion in 2025 and USD 1.01 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Carton Liners

Sustainability has become a defining trend in the carton liner market. Packaging manufacturers and end-users are actively seeking environmentally responsible alternatives to conventional plastic liners. Growing regulatory pressure and corporate sustainability commitments are encouraging the adoption of recyclable, compostable, and biodegradable carton liner materials. Companies across food, consumer goods, and retail sectors are increasingly incorporating paper-based and bio-derived liners into their packaging portfolios.

For example, several food manufacturers have introduced recyclable carton liner solutions that maintain moisture resistance while reducing plastic content. These products help companies meet environmental targets without compromising packaging performance. The future impact of this trend is expected to be significant, as ongoing investments in material innovation will improve barrier properties and durability, enabling sustainable liners to compete more effectively with traditional plastic alternatives across a broader range of applications.

Growth of High-Barrier Packaging Solutions

Demand for high-barrier carton liners is increasing as manufacturers seek enhanced protection against moisture, oxygen, contaminants, and temperature fluctuations. Industries such as pharmaceuticals, specialty chemicals, and food processing require packaging solutions that maintain product quality throughout extended storage and transportation periods.

For instance, pharmaceutical companies increasingly use multilayer carton liners with advanced barrier technologies to preserve sensitive formulations. Similarly, food exporters rely on high-performance liners to protect products during long-distance shipments. Looking ahead, advancements in multilayer films, nano-coatings, and smart packaging technologies are expected to improve protective capabilities further. This trend will likely support the development of next-generation carton liners that provide enhanced performance while meeting sustainability and regulatory requirements.

Market Drivers

Expansion of Global Food Processing and Distribution Industries

The growing food processing and distribution sectors represent a major driver for the carton liner market. Increasing consumption of packaged foods, frozen products, and processed ingredients has created strong demand for protective packaging solutions that maintain product freshness and safety. Carton liners help prevent contamination, moisture penetration, and product deterioration throughout storage and transportation processes.

For example, large food manufacturers utilize polyethylene and barrier liners to safeguard powdered ingredients, grains, and dry food products. As food exports continue to expand globally, the need for reliable packaging solutions is increasing. This cause-and-effect relationship between food industry growth and packaging demand continues to support strong market expansion across developed and emerging economies.

Rising Demand for Pharmaceutical Packaging Protection

The pharmaceutical industry's focus on product integrity and regulatory compliance is significantly driving demand for carton liners. Medicines, active pharmaceutical ingredients, and healthcare products require specialized packaging solutions capable of protecting contents from environmental exposure and contamination.

For instance, pharmaceutical manufacturers increasingly use anti-static and moisture-resistant liners for sensitive drug formulations. The growing production of biologics, specialty medicines, and temperature-sensitive products is further strengthening demand. As healthcare expenditures rise globally and pharmaceutical supply chains expand, the requirement for advanced protective packaging solutions will continue to support market growth throughout the forecast period.

Market Restraint

Volatility in Raw Material Prices and Regulatory Challenges

One of the primary restraints affecting the carton liner market is the volatility of raw material prices. Polyethylene, polypropylene, specialty films, and paper-based materials are influenced by fluctuations in energy prices, supply chain disruptions, and global trade conditions. These factors can significantly impact manufacturing costs and profit margins.

For example, sudden increases in polymer prices can make plastic liner production more expensive, forcing manufacturers to adjust pricing strategies. Additionally, evolving environmental regulations regarding single-use plastics create compliance challenges for producers relying heavily on conventional materials. Companies may need to invest in research, development, and production modifications to meet regulatory requirements. While sustainable alternatives are emerging, transitioning to new materials often involves higher initial costs and operational adjustments. These challenges may temporarily limit market expansion, particularly among smaller manufacturers with constrained resources.

Market Opportunities

Development of Biodegradable and Compostable Liners

The growing emphasis on sustainability presents substantial opportunities for biodegradable and compostable carton liners. Businesses across food, retail, and consumer goods industries are actively searching for environmentally friendly packaging options that align with corporate sustainability goals and consumer expectations.

Manufacturers developing bio-based liners derived from renewable materials can capitalize on increasing market demand. Applications include food packaging, agricultural products, and e-commerce shipments. Future advancements in biodegradable barrier technologies are expected to improve product performance and expand adoption across multiple industries. This opportunity offers strong long-term growth potential as environmental regulations continue to encourage sustainable packaging solutions.

Expansion of E-Commerce and Logistics Packaging

The rapid growth of e-commerce is creating new opportunities for carton liner manufacturers. Online retailers require packaging solutions that protect products from damage, moisture, and contamination throughout increasingly complex logistics networks. Carton liners provide an additional layer of protection that enhances shipment reliability.

For example, electronics, personal care products, and specialty foods often require protective liners during transportation. As cross-border e-commerce expands and consumer expectations for product quality increase, demand for advanced carton liner solutions is expected to rise. Manufacturers capable of developing lightweight, durable, and sustainable liners tailored to e-commerce requirements will be well positioned to capture future growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.9 Billion |

| Market Size in 2026 | USD 5.2 Billion |

| Market Size in 2034 | USD 8.6 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polyethylene liners accounted for 36.8% of the market share in 2024, making them the leading type segment. Their dominance is attributed to excellent moisture resistance, durability, flexibility, and cost-effectiveness. Polyethylene liners are widely used across food processing, agriculture, pharmaceuticals, and industrial packaging applications. Manufacturers favor these liners because they provide reliable protection while remaining compatible with automated packaging systems. Their versatility allows them to accommodate diverse product categories ranging from dry ingredients to chemical compounds. Continued demand from multiple industries ensures their strong position within the market.

Biodegradable liners are expected to expand at a CAGR of 8.1% through 2034. Growth is driven by increasing environmental awareness and regulatory pressure to reduce plastic waste. Manufacturers are introducing innovative bio-based materials capable of delivering protective performance comparable to traditional liners. Adoption is accelerating across food packaging and consumer goods sectors. Future developments in renewable barrier technologies and compostable polymers are expected to enhance product functionality, creating additional growth opportunities for biodegradable liner solutions.

By Material

Plastic-based materials held 58.4% of the market share in 2024 due to their superior barrier performance, durability, and affordability. These materials provide effective protection against moisture, contaminants, and physical damage, making them suitable for demanding packaging applications. Industries such as food processing, chemicals, and pharmaceuticals continue to rely heavily on plastic liners because of their proven performance and widespread availability. Ongoing innovations in multilayer films further support market dominance.

Paper-based materials are projected to grow at a CAGR of 7.5% during the forecast period. Sustainability concerns and regulatory initiatives are encouraging companies to adopt renewable packaging solutions. Paper-based liners offer recyclability and reduced environmental impact while supporting corporate sustainability goals. Manufacturers are enhancing barrier properties through coatings and advanced fiber technologies. These improvements are expected to expand applications and strengthen future demand across multiple industries.

By End-Use

The food & beverage segment accounted for 42.7% of the market share in 2024. Carton liners play a critical role in protecting ingredients, processed foods, and packaged products from contamination and moisture. Growing demand for packaged foods, international food trade, and food safety compliance requirements continue to support segment dominance. Food manufacturers increasingly utilize advanced liner solutions to maintain product quality and extend shelf life during transportation and storage.

Pharmaceutical applications are expected to grow at a CAGR of 7.8% through 2034. Increasing production of specialty medicines, biologics, and healthcare products is driving demand for protective packaging solutions. Carton liners help maintain product integrity by providing barriers against environmental exposure and contamination. Future growth is expected to be supported by expanding pharmaceutical manufacturing capacity and increasingly stringent regulatory requirements regarding packaging performance.

Carton Liner Market Segmentations

By Type

- Polyethylene Liners

- Polypropylene Liners

- Aluminum Foil Liners

- Paper-Based Liners

- Barrier Liners

By Material

- Plastic

- Paper

- Aluminum Foil

- Composite Materials

By End-User

- Food & Beverage

- Pharmaceuticals

- Chemicals

- Agriculture

- Industrial Goods

- Consumer Products

Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Regional Analysis

North America

North America accounted for approximately 26.8% of the carton liner market in 2025 and is expected to expand at a CAGR of 6.1% through 2034. The region benefits from a highly developed packaging industry, advanced logistics infrastructure, and strong demand from food processing and pharmaceutical sectors. Companies continue investing in protective packaging solutions to improve supply chain efficiency and product safety. Sustainability initiatives are also accelerating the adoption of recyclable and bio-based liner materials. Growth is further supported by increasing demand for packaged foods and consumer products distributed through both traditional retail and e-commerce channels.

The United States dominates the regional market due to its extensive manufacturing and distribution network. A unique growth driver is the expansion of pharmaceutical production and healthcare logistics. Pharmaceutical companies increasingly utilize high-barrier carton liners to protect sensitive products during storage and transportation. Industry trends indicate rising adoption of automated packaging systems, which require high-quality liner materials capable of maintaining consistent performance across large-scale operations.

Europe

Europe represented 24.1% of the global market share in 2025 and is forecast to grow at a CAGR of 5.9% through 2034. The region's packaging industry is strongly influenced by environmental regulations and sustainability objectives. Companies are increasingly replacing traditional plastic liners with recyclable and compostable alternatives. Food safety standards and pharmaceutical packaging requirements further contribute to demand for advanced carton liner solutions. Growing exports of specialty foods and consumer goods also support packaging consumption across European markets.

Germany remains the leading country within Europe. A distinctive growth driver is the country's emphasis on circular economy initiatives. Packaging manufacturers are investing heavily in recyclable barrier materials and renewable packaging technologies. For example, several German packaging firms have expanded production capacities for fiber-based liners designed to reduce plastic waste. These developments are expected to strengthen regional growth while supporting sustainability targets.

Asia Pacific

Asia Pacific held the largest market share of 39.1% in 2025 and is anticipated to register a CAGR of 7.0% during the forecast period. Rapid industrialization, growing manufacturing activities, and expanding export industries are driving demand for carton liners throughout the region. Increasing food processing capacity, pharmaceutical production, and consumer goods manufacturing are creating significant opportunities for packaging suppliers. The region also benefits from rising e-commerce activity and expanding logistics infrastructure.

China dominates the Asia Pacific market due to its extensive manufacturing base and export-oriented economy. A unique growth driver is the growth of international trade and industrial packaging requirements. Exporters increasingly rely on moisture-resistant and high-barrier carton liners to protect products during long-distance transportation. Ongoing investments in packaging technology and logistics modernization are expected to sustain strong market growth throughout the forecast period.

Middle East & Africa

The Middle East & Africa accounted for approximately 5.2% of the market share in 2025 and is projected to grow at a CAGR of 6.6% through 2034. Expanding food imports, industrial development, and pharmaceutical investments are contributing to increasing demand for protective packaging materials. Governments across the region are investing in manufacturing diversification strategies that support packaging industry growth. Demand for moisture-resistant packaging is particularly important due to climatic conditions and transportation challenges.

Saudi Arabia represents the largest market within the region. A unique growth driver is the expansion of food processing and warehousing infrastructure. Companies are increasingly utilizing advanced packaging solutions to preserve product quality in high-temperature environments. Industry trends indicate growing interest in sustainable packaging materials as businesses align with broader environmental initiatives and international trade requirements.

Latin America

Latin America captured approximately 4.8% of the global market in 2025 and is forecast to register the fastest CAGR of 7.2% during the study period. The region is benefiting from rising agricultural exports, expanding food manufacturing activities, and increasing consumer goods production. Growing demand for packaging solutions that protect products during transportation is supporting market expansion. Improvements in logistics networks and retail distribution systems are further contributing to demand.

Brazil remains the dominant country in the region. A distinctive growth driver is the country's strong agricultural export sector. Producers increasingly use carton liners to protect grains, processed foods, and specialty agricultural products during international shipments. The adoption of protective packaging technologies continues to rise as exporters seek to improve product quality and reduce transit-related losses, supporting long-term market growth.

Competitive Landscape

The carton liner market is characterized by the presence of global packaging companies and specialized liner manufacturers competing through innovation, sustainability initiatives, and strategic partnerships.

Amcor plc is recognized as a market leader due to its extensive packaging portfolio, global manufacturing footprint, and ongoing investments in sustainable packaging technologies. The company continues to expand recyclable and high-barrier packaging solutions designed for food, pharmaceutical, and industrial applications.

Other major players include Berry Global Inc., Mondi Group, Sealed Air Corporation, and Sonoco Products Company. These companies focus on material innovation, production efficiency, and expanding sustainable product offerings. Recent developments include investments in recyclable film technologies, advanced barrier materials, and automation-compatible packaging solutions.

Competitive strategies increasingly emphasize sustainability, regulatory compliance, and enhanced packaging performance. Companies are also pursuing acquisitions and capacity expansions to strengthen regional presence and address growing demand across emerging markets.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Westrock plc

- DS Smith Plc

- International Paper Company

- Coveris Holdings S.A.

- Huhtamaki Oyj

- ProAmpac LLC

- Novolex Holdings LLC

- Winpak Ltd.

- Constantia Flexibles Group GmbH

- Pregis LLC