Rigid Paper Packaging Market Size and Growth

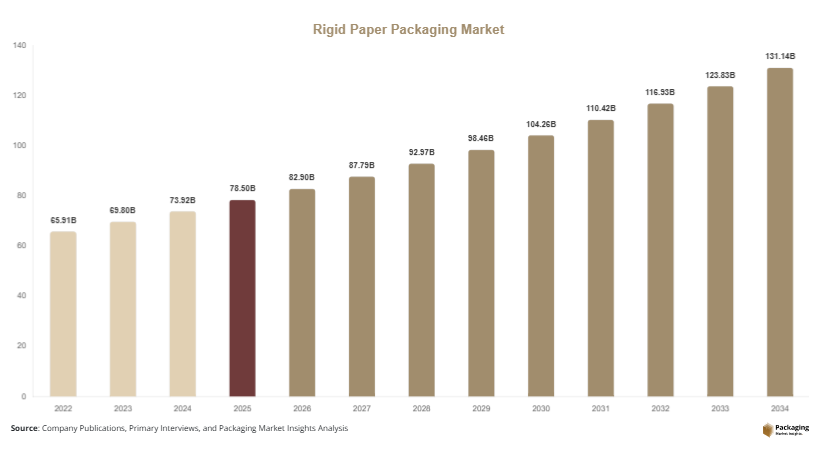

The global rigid paper packaging market size is estimated at USD 78.5 billion in 2025 and is projected to reach USD 82.9 billion in 2026, supported by rising demand across food & beverage, personal care, electronics, and industrial packaging sectors. Over the forecast period 2025–2034, the market is expected to grow at a CAGR of 5.9%, reaching approximately USD 132.4 billion by 2034. The rigid paper packaging market is witnessing steady expansion as industries shift toward recyclable, renewable, and fiber-based packaging solutions.

One of the primary growth factors is the global shift toward sustainable packaging alternatives. Governments and regulatory bodies across Europe, North America, and Asia Pacific are implementing strict policies to reduce plastic waste, encouraging adoption of rigid paper packaging solutions. These materials are widely used due to their recyclability, biodegradability, and lower environmental footprint compared to plastic-based alternatives.

Key Highlights:

- Market size reached USD 78.5 billion in 2025, supported by steady growth in demand from sustainable packaging across multiple end-use industries. Expansion is mainly driven by food & beverage, retail, and e-commerce sectors, where rigid paper packaging is increasingly replacing plastic-based alternatives.

- It is projected to reach USD 132.4 billion by 2034, reflecting consistent long-term adoption of recyclable and fiber-based packaging solutions across global markets. Growth is also supported by advancements in paperboard strength, coating technologies, and premium packaging design.

- The market is expected to register an CAGR of 5.9% during 2025–2034, indicating stable expansion driven by sustainability trends and regulatory alignment across developed and emerging economies.

- Strong demand from food & beverage, retail, and e-commerce sectors continues to be a key growth driver, as companies prioritize eco-friendly packaging solutions that balance durability and branding requirements.

- Increasing regulatory push toward sustainable and recyclable packaging is accelerating the shift away from plastic materials, with governments implementing stricter waste reduction and recycling policies.

- Rising adoption in premium product and luxury packaging applications is further strengthening market growth, as brands increasingly use rigid paper packaging to enhance product presentation and support sustainability-focused branding strategies.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Premium and Luxury Paper Packaging

A major trend in the rigid paper packaging market is the increasing adoption of premium and luxury packaging formats. Brands in cosmetics, electronics, and high-end food products are using rigid paperboard packaging to enhance product presentation and brand value. This trend is driven by consumer preference for aesthetically appealing and sustainable packaging solutions. Manufacturers are investing in advanced printing technologies such as embossing, foil stamping, and textured finishes to improve visual appeal. This has significantly expanded the role of rigid paper packaging in premium retail environments, where packaging plays a key role in influencing purchasing decisions.

Integration of Smart and Functional Packaging Features

Another key trend is the integration of smart packaging elements such as QR codes, RFID tags, and interactive labeling into rigid paper packaging structures. This allows brands to enhance consumer engagement, provide product authentication, and improve supply chain transparency. The trend is particularly strong in the food and pharmaceutical sectors, where traceability and consumer information are important. Additionally, functional enhancements such as moisture-resistant coatings and tamper-evident designs are being incorporated to improve packaging performance without compromising sustainability goals.

Market Drivers

Increasing Demand for Sustainable Packaging Solutions

The rising global focus on sustainability is a major driver of the rigid paper packaging market. Governments are enforcing regulations to reduce plastic usage, encouraging industries to adopt recyclable and biodegradable materials. Rigid paper packaging offers an eco-friendly alternative with lower carbon emissions and improved recyclability. Industries such as food service, FMCG, and retail are increasingly transitioning to paper-based solutions to meet environmental compliance and consumer expectations.

Expansion of E-commerce and Retail Packaging Needs

The rapid growth of e-commerce is significantly boosting demand for rigid paper packaging. Online retailers require durable and protective packaging solutions that can ensure product safety during shipping. Rigid paperboard is widely used for electronics, apparel, cosmetics, and luxury goods due to its strength and branding capabilities. The rise of subscription boxes and premium unboxing experiences has further increased demand for customized rigid paper packaging solutions.

Market Restraint

Limited Moisture Resistance Compared to Plastic Alternatives

One of the key restraints in the rigid paper packaging market is its relatively lower resistance to moisture and humidity compared to plastic-based packaging materials. While coatings and laminations can improve performance, they also increase production costs and may reduce recyclability.

This limitation restricts its use in certain applications such as frozen food, liquid-heavy products, and long-term storage environments. For example, food manufacturers often require additional barrier layers to maintain product freshness, which increases manufacturing complexity and cost. As a result, adoption in high-moisture environments remains limited despite growing sustainability demand.

Market Opportunities

Growth in Sustainable Luxury Packaging Segment

The increasing demand for sustainable luxury packaging presents a significant opportunity for the rigid paper packaging market. High-end brands in cosmetics, perfumes, and electronics are increasingly shifting toward rigid paperboard packaging to align with sustainability goals while maintaining premium product presentation. This trend is driving innovation in design, texture, and finishing techniques, allowing manufacturers to offer customized packaging solutions that enhance brand identity.

Expansion in Emerging Markets

Emerging economies in Asia Pacific, Latin America, and Africa present strong growth opportunities due to rising industrialization and increasing consumer spending. As retail and e-commerce sectors expand in these regions, demand for cost-effective and sustainable packaging solutions is increasing. Government initiatives promoting recycling and waste reduction are also supporting the adoption of rigid paper packaging across multiple industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.5 Billion |

| Market Size in 2026 | USD 82.9 Billion |

| Market Size in 2034 | USD 132.4 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

Rigid paper boxes dominated the market in 2024, accounting for approximately 44% share. Their dominance is attributed to widespread use across retail, cosmetics, electronics, and luxury goods packaging. These boxes offer strong structural integrity, excellent branding surface, and premium visual appeal, making them a preferred choice for high-value consumer products. Their ability to support customization and high-quality printing further strengthens their position in the packaging industry.

Trays and inserts are expected to be the fastest-growing subsegment, expanding at a CAGR of 6.6%. Growth is driven by rising demand in e-commerce and food delivery applications, where product protection during transportation is critical. These formats provide cushioning, organization, and eco-friendly packaging alternatives, replacing plastic-based inserts in multiple industries.

By Application

Food packaging dominated in 2024 with approximately 41% share of the market. The segment benefits from strong demand for takeaway packaging, bakery boxes, frozen food packaging, and ready-to-eat meal containers. Rigid paper packaging is widely preferred due to its safety, recyclability, and compliance with food-grade standards, making it suitable for direct food contact applications.

Electronics packaging is expected to be the fastest-growing application segment, registering a CAGR of 7.0%. Growth is driven by increasing demand for protective and sustainable packaging for smartphones, accessories, and consumer electronics. Manufacturers are shifting from plastic foam to molded rigid paper solutions to reduce environmental impact while ensuring product safety.

By End-Use Industry

Food & beverage dominated in 2024 with approximately 43% share, supported by rising packaged food consumption, food delivery services, and retail expansion. Rigid paper packaging is widely used in bakery, dairy, fast food, and beverage applications due to its convenience and eco-friendly nature.

E-commerce and retail is expected to be the fastest-growing segment, expanding at a CAGR of 7.3%. Growth is driven by increasing online shopping activity and rising demand for premium unboxing experiences. Companies are adopting rigid paper packaging to enhance brand identity while meeting sustainability goals and reducing plastic usage.

Rigid Paper Packaging Market Segmentations

By Product Type

- Rigid Paper Boxes

- Trays and Inserts

- Folding Cartons

- Paperboard Sleeves

By Application

- Food Packaging

- Electronics Packaging

- Cosmetics Packaging

- Industrial Packaging

By End-Use Industry

- Food & Beverage

- Retail & E-commerce

- FMCG

- Healthcare & Pharmaceuticals

Regional Analysis

North America

North America accounted for approximately 28% market share in 2025, with a projected CAGR of 5.8% during 2025–2034. The region continues to benefit from strong demand in e-commerce, food delivery, and retail packaging applications. Increasing corporate sustainability commitments and regulatory pressure on plastic packaging are further accelerating adoption of rigid paper-based solutions.

The United States dominates the regional market due to its highly developed retail and logistics infrastructure. A key growth factor is the rapid expansion of online shopping and subscription-based packaging models, which require durable, recyclable, and brand-friendly packaging formats.

Europe

Europe held the largest share at approximately 31% in 2025, with a projected CAGR of 6.2% during the forecast period. Strict environmental regulations and strong recycling systems continue to position Europe as a leading market for rigid paper packaging solutions.

Germany leads the regional market due to its advanced packaging manufacturing ecosystem. A key growth factor is the enforcement of EU Green Deal policies, which are pushing manufacturers to replace plastic packaging with fiber-based alternatives across multiple industries.

Asia Pacific

Asia Pacific accounted for approximately 29% market share in 2025, with the highest CAGR of 6.9%. Rapid industrialization, expanding consumer markets, and rising e-commerce penetration are driving strong demand for rigid paper packaging solutions.

China dominates the region due to large-scale manufacturing and export-oriented packaging production. A key growth factor is increasing domestic consumption of packaged goods supported by rising urban populations and growing retail modernization.

Middle East & Africa

The region held approximately 7% market share in 2025, with a projected CAGR of 5.4%. Growth is supported by expanding food service industries, tourism development, and gradual adoption of sustainable packaging practices.

The United Arab Emirates leads the region due to strong hospitality and retail sectors. A key growth factor is increasing demand for premium and sustainable packaging in hotels, airlines, and food delivery services.

Latin America

Latin America accounted for approximately 5% market share in 2025, with a projected CAGR of 5.7%. Growth is driven by FMCG expansion, retail modernization, and increasing awareness of sustainable packaging solutions.

Brazil dominates the region due to its large consumer base and growing food and beverage industry. A key growth factor is rising adoption of recyclable packaging materials driven by environmental awareness initiatives and regulatory developments.

Competitive Landscape

The rigid paper packaging market is highly competitive, with companies focusing on sustainability innovation, lightweight structures, and premium packaging design. Competition is driven by material advancements and expansion into eco-friendly product lines.

International Paper is a leading player in the market, supported by its strong global production network. The company recently expanded its sustainable packaging portfolio by increasing investment in recyclable paperboard manufacturing facilities to meet rising global demand.

Key Players List

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- Stora Enso Oyj

- Packaging Corporation of America

- Georgia-Pacific LLC

- Mayr-Melnhof Karton AG

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Graphic Packaging Holding Company

- Sonoco Products Company

- Rengo Co., Ltd.

- Holmen AB