3D Printed Packaging Market Size and Growth

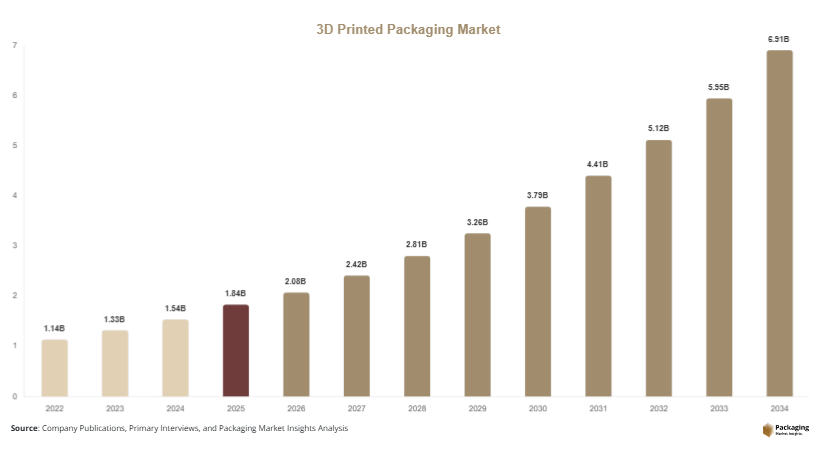

The global 3D printed packaging market was valued at USD 1.84 billion in 2025 and is expected to reach USD 2.08 billion in 2026. The market is projected to attain USD 6.91 billion by 2034, registering a CAGR of 16.2% during the forecast period from 2025 to 2034. The rapid growth trajectory reflects increasing investments in additive manufacturing infrastructure and broader adoption of digital manufacturing solutions across packaging value chains.

The 3D printed packaging market is emerging as a transformative segment within the global packaging industry, driven by advancements in additive manufacturing technologies, demand for customized packaging solutions, and growing emphasis on sustainable production methods. 3D printing enables manufacturers to produce packaging prototypes, molds, customized containers, and limited-production packaging with greater design flexibility and reduced material waste compared to conventional manufacturing processes. Industries including food & beverages, cosmetics, pharmaceuticals, electronics, and luxury goods are increasingly exploring 3D-printed packaging to enhance branding, product protection, and supply chain efficiency.

Key Market Highlights

- Asia Pacific dominated the market with a 36.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 17.5%.

- Customized packaging solutions led the type segment with a 34.8% share.

- Polymer materials dominated with a 57.2% share.

- Food & beverage applications led the market with a 31.7% share.

- The US remained the dominant country with a market size of USD 0.51 billion in 2025 and USD 0.58 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Integration of Mass Customization in Packaging Design

Mass customization is becoming a significant trend in the 3D printed packaging market as brands seek differentiated packaging formats that enhance consumer engagement. Traditional manufacturing methods often require costly tooling and lengthy production cycles, limiting customization opportunities. In contrast, 3D printing allows companies to create personalized packaging designs, limited-edition packaging, and promotional packaging with minimal setup costs. Cosmetic brands, luxury product manufacturers, and specialty food companies are increasingly adopting additive manufacturing to develop distinctive packaging formats. For example, several premium skincare brands have introduced customized packaging designs tailored to specific customer segments. Looking ahead, advances in digital design platforms and automated printing technologies are expected to accelerate the adoption of customized packaging solutions across mainstream consumer product categories.

Expansion of Sustainable Additive Manufacturing Materials

Sustainability remains a key trend influencing packaging innovation. Packaging manufacturers are increasingly developing recyclable, bio-based, and biodegradable materials suitable for additive manufacturing processes. These materials help reduce waste generation because 3D printing uses only the required amount of material during production. Several packaging companies are experimenting with plant-derived polymers and recycled feedstocks to improve environmental performance. For example, packaging innovators in Europe are introducing biodegradable filament materials designed specifically for consumer packaging applications. The future impact of this trend is expected to be substantial as governments implement stricter sustainability regulations and brands pursue carbon reduction goals. Increased material innovation is likely to broaden the commercial viability of sustainable 3D-printed packaging solutions.

Market Drivers

Rising Demand for Rapid Prototyping and Product Development

The increasing need for rapid packaging development is a major driver of the 3D printed packaging market. Traditional packaging development often involves multiple design iterations, tooling investments, and extended production timelines. Additive manufacturing enables companies to quickly create prototypes, evaluate packaging performance, and modify designs without significant costs. This capability significantly reduces time-to-market for new products. For example, beverage and cosmetics companies frequently use 3D printing to test container shapes, closure systems, and branding elements before committing to full-scale manufacturing. The cause-and-effect relationship is clear: faster prototyping improves innovation cycles, enabling brands to launch products more efficiently and respond quickly to changing consumer preferences.

Growth of Personalized Consumer Products

Consumer demand for personalized products is creating substantial opportunities for packaging customization. Brands increasingly seek packaging formats that strengthen customer engagement and improve product differentiation. 3D printing provides the flexibility required to produce small-batch and customized packaging economically. Luxury goods, cosmetics, healthcare products, and specialty food manufacturers are actively exploring customized packaging solutions. For instance, personalized gift packaging and limited-edition promotional packaging have become common applications for additive manufacturing. As personalization continues to influence purchasing behavior, demand for flexible packaging production technologies is expected to increase, supporting sustained growth in the 3D printed packaging market.

Market Restraint

High Production Costs and Limited Large-Scale Manufacturing Capability

Despite significant technological progress, high production costs remain a major restraint for the 3D printed packaging market. Additive manufacturing systems, specialized materials, and post-processing requirements can increase overall production expenses compared to conventional packaging manufacturing methods. While 3D printing is highly effective for prototypes and customized packaging runs, large-scale production often remains more economical using traditional processes such as injection molding or thermoforming.

The impact of this limitation is particularly noticeable among small and medium-sized enterprises that may face budget constraints when investing in advanced printing infrastructure. For example, consumer goods manufacturers producing millions of packaging units annually often continue relying on conventional manufacturing due to cost efficiencies and higher production speeds. Additionally, certain additive manufacturing materials may not yet meet all regulatory or performance requirements for food-contact applications. Although ongoing innovation is reducing costs and improving scalability, production economics continue to limit broader adoption across high-volume packaging segments.

Market Opportunities

Expansion of Smart and Connected Packaging Solutions

The convergence of additive manufacturing and smart packaging technologies presents a significant growth opportunity. Packaging manufacturers are exploring the integration of sensors, QR codes, tracking elements, and interactive features into 3D-printed packaging structures. These innovations can improve supply chain visibility, consumer engagement, and product authentication. For example, pharmaceutical companies can utilize smart packaging to monitor product handling conditions and improve traceability. Future applications may include embedded communication technologies, anti-counterfeiting features, and connected packaging experiences. As digital transformation accelerates across industries, smart 3D-printed packaging solutions are expected to gain broader adoption and create new revenue opportunities.

Adoption Across Healthcare and Pharmaceutical Applications

Healthcare and pharmaceutical sectors represent attractive opportunities for market expansion. These industries increasingly require specialized packaging solutions for medical devices, diagnostic kits, biologics, and personalized medicines. 3D printing enables the production of highly customized packaging designs that address unique product protection requirements. Pharmaceutical companies can also leverage additive manufacturing for rapid prototyping and low-volume production applications. Future growth is expected to be supported by personalized medicine initiatives, expansion of biologics distribution networks, and increasing demand for customized healthcare packaging. As regulatory frameworks evolve and material performance improves, healthcare applications are likely to become a key growth area within the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.84 Billion |

| Market Size in 2026 | USD 2.08 Billion |

| Market Size in 2034 | USD 6.91 Billion |

| CAGR | 16.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Customized packaging solutions dominated the market in 2024, accounting for approximately 34.8% of total revenue. This segment leads due to growing demand for product differentiation, personalized branding, and short-run packaging production. Companies across cosmetics, food, luxury goods, and promotional packaging categories increasingly utilize additive manufacturing to create unique packaging formats. The ability to produce complex geometries without tooling investments provides a significant competitive advantage. For example, premium cosmetic brands often employ 3D printing to develop exclusive product packaging designs for limited-edition collections. The segment also benefits from increasing demand for consumer engagement strategies that rely on personalization and customized product experiences.

Smart 3D-printed packaging is projected to be the fastest-growing subsegment, expanding at a CAGR of 18.1% through 2034. Growth is driven by increasing interest in connected packaging solutions capable of enhancing traceability, product authentication, and consumer interaction. Integration of digital features such as QR codes, embedded tracking elements, and intelligent identification systems is becoming more common. Future developments may include sensor-enabled packaging and interactive consumer experiences. As digital transformation initiatives continue across supply chains, demand for smart packaging applications is expected to accelerate significantly.

By Material

Polymer materials dominated the market in 2024 with a share of approximately 57.2%. Polymers remain the preferred material category because they offer versatility, cost efficiency, and compatibility with multiple additive manufacturing technologies. Materials such as PLA, PETG, ABS, and nylon are widely used for packaging prototypes and customized packaging production. Packaging manufacturers favor polymer-based materials because they support complex designs while maintaining structural integrity. Numerous consumer goods companies utilize polymer materials for product development and specialized packaging applications.

Biodegradable materials represent the fastest-growing segment and are expected to register a CAGR of 17.8% during the forecast period. Growth is supported by increasing environmental concerns and stricter sustainability regulations. Packaging manufacturers are developing bio-based materials that combine performance characteristics with improved environmental profiles. Applications include food packaging, retail packaging, and specialty consumer products. Future advancements in material science are expected to improve durability and commercial scalability, supporting broader market adoption across various industries.

By End-Use

Food & beverage applications accounted for the largest market share of approximately 31.7% in 2024. The segment benefits from growing demand for innovative packaging designs, rapid product development, and enhanced branding opportunities. Food manufacturers increasingly utilize additive manufacturing for packaging prototypes, promotional packaging, and customized packaging solutions. Beverage companies also employ 3D printing to test container designs and optimize packaging aesthetics before commercial production. The combination of consumer demand for differentiated products and increasing packaging innovation supports the segment's dominant position.

Healthcare packaging is anticipated to be the fastest-growing end-use segment, expanding at a CAGR of 18.4% through 2034. Growth is driven by rising demand for customized packaging formats, personalized medical products, and specialized pharmaceutical packaging solutions. Additive manufacturing enables healthcare companies to develop packaging tailored to specific medical devices and treatment requirements. Future demand is expected to benefit from personalized medicine initiatives, biologics distribution growth, and increasing healthcare innovation. Continued advancements in medical-grade materials are likely to support broader adoption within this segment.

3D Printed Packaging Market Segmentations

By Type

- Customized Packaging Solutions

- Prototyping Packaging

- Smart 3D-Printed Packaging

- Decorative Packaging

- Functional Packaging Components

By Material

- Polymers

- Metals

- Biodegradable Materials

- Composite Materials

By End-User

- Food & Beverage

- Healthcare

- Cosmetics & Personal Care

- Electronics

- Consumer Goods

Regional Analysis

North America

North America accounted for approximately 31.4% of the global 3D printed packaging market share in 2025 and is projected to grow at a CAGR of 15.4% through 2034. The region benefits from advanced additive manufacturing infrastructure, strong technology adoption rates, and significant investment in packaging innovation. Demand is driven by consumer goods companies seeking customized packaging formats and rapid product development capabilities. The presence of leading 3D printing technology providers further supports regional growth. Increasing adoption among healthcare, electronics, and food manufacturers is expanding commercial opportunities while supporting broader acceptance of additive manufacturing technologies across packaging applications.

The United States dominates the regional market due to its established additive manufacturing ecosystem and strong innovation culture. A unique growth driver is the widespread use of rapid prototyping among consumer packaged goods companies. Several major beverage, cosmetics, and healthcare brands utilize 3D printing to accelerate packaging development and reduce product launch timelines. The increasing commercialization of industrial-scale additive manufacturing systems is expected to strengthen market growth throughout the forecast period.

Europe

Europe held approximately 27.8% of the market share in 2025 and is expected to register a CAGR of 15.8% through 2034. The region's growth is supported by strong sustainability initiatives, advanced manufacturing capabilities, and increasing investment in circular economy solutions. Packaging companies are actively exploring additive manufacturing to reduce waste generation and improve resource efficiency. Regulatory support for sustainable packaging innovation is encouraging broader adoption of environmentally friendly production methods. Demand is particularly strong across luxury packaging, food packaging, and healthcare sectors.

Germany represents the dominant country within Europe. A unique growth driver is the country's emphasis on Industry 4.0 manufacturing strategies. German packaging companies increasingly integrate digital design tools and additive manufacturing technologies into production workflows. Several packaging innovation centers are collaborating with industrial manufacturers to develop advanced packaging applications. This trend is expected to support continued technological advancement and market expansion.

Asia Pacific

Asia Pacific dominated the market with a share of 36.9% in 2025 and is forecast to grow at a CAGR of 17.2% during the study period. Rapid industrialization, expanding consumer markets, and increasing investment in advanced manufacturing technologies are driving growth throughout the region. Packaging manufacturers are adopting additive manufacturing to improve production flexibility and support product customization. Rising e-commerce activity and growing demand for innovative packaging solutions further contribute to market expansion. Countries across the region are also investing in digital manufacturing infrastructure to strengthen competitiveness.

China remains the leading country in Asia Pacific. A unique growth driver is the rapid expansion of domestic additive manufacturing capacity. Chinese manufacturers are increasingly deploying industrial-scale 3D printing systems to serve packaging, electronics, and consumer goods sectors. The growth of domestic e-commerce platforms and demand for customized product packaging continue to create substantial opportunities for additive manufacturing providers.

Middle East & Africa

The Middle East & Africa accounted for approximately 2.7% of market revenue in 2025 and is expected to grow at a CAGR of 15.1% through 2034. Market development is supported by increasing industrial diversification efforts, investments in advanced manufacturing technologies, and growing demand for innovative packaging solutions. Governments across several countries are promoting technology adoption as part of broader economic transformation initiatives. Packaging companies are exploring additive manufacturing to improve efficiency and reduce production lead times.

The United Arab Emirates leads the regional market. A unique growth driver is the country's investment in advanced manufacturing and innovation ecosystems. Several technology parks and industrial hubs support the deployment of additive manufacturing solutions across multiple industries. Packaging companies serving luxury retail, cosmetics, and specialty consumer goods sectors increasingly utilize 3D printing for customized packaging development and promotional applications.

Latin America

Latin America represented approximately 1.2% of the global market in 2025 and is expected to register the fastest CAGR of 17.5% during the forecast period. Growing industrial modernization, increasing adoption of digital manufacturing technologies, and rising demand for customized packaging are supporting regional growth. Consumer goods manufacturers are exploring additive manufacturing to enhance product differentiation and reduce packaging development costs. Expanding retail markets and rising disposable incomes further contribute to demand.

Brazil remains the dominant country in the region. A unique growth driver is the increasing adoption of additive manufacturing among packaging service providers serving consumer goods companies. Several packaging firms are investing in digital manufacturing capabilities to support customized packaging projects and rapid product launches. The growing popularity of personalized products is expected to strengthen market demand in the coming years.

Competitive Landscape

The 3D printed packaging market is characterized by a combination of additive manufacturing technology providers, packaging manufacturers, and material developers. Competition focuses on technological innovation, material development, sustainability initiatives, and strategic partnerships.

Stratasys Ltd. is recognized as a market leader due to its broad additive manufacturing portfolio, strong industrial customer base, and continuous investment in packaging applications. The company recently expanded its packaging prototyping capabilities through advanced multi-material printing solutions designed for consumer goods manufacturers.

Other major participants include 3D Systems Corporation, HP Inc., EOS GmbH, and Materialise NV. These companies focus on expanding industrial printing capabilities, improving material compatibility, and enhancing production efficiency. Strategic collaborations between packaging producers and technology providers are becoming increasingly common as the market evolves.

Recent industry strategies include investment in sustainable materials, development of industrial-scale additive manufacturing platforms, and expansion of application-specific packaging solutions. Market participants are also focusing on improving production speed and scalability to address commercial manufacturing requirements.

Key Players List

- Stratasys Ltd.

- 3D Systems Corporation

- HP Inc.

- EOS GmbH

- Materialise NV

- Desktop Metal Inc.

- Carbon Inc.

- SLM Solutions Group AG

- Ultimaker BV

- Proto Labs Inc.

- Formlabs Inc.

- voxeljet AG

- Tethon 3D

- ExOne Company

- Xometry Inc.

- Markforged Holding Corporation