Pharmaceutical Polymer Vials Market Size and Growth

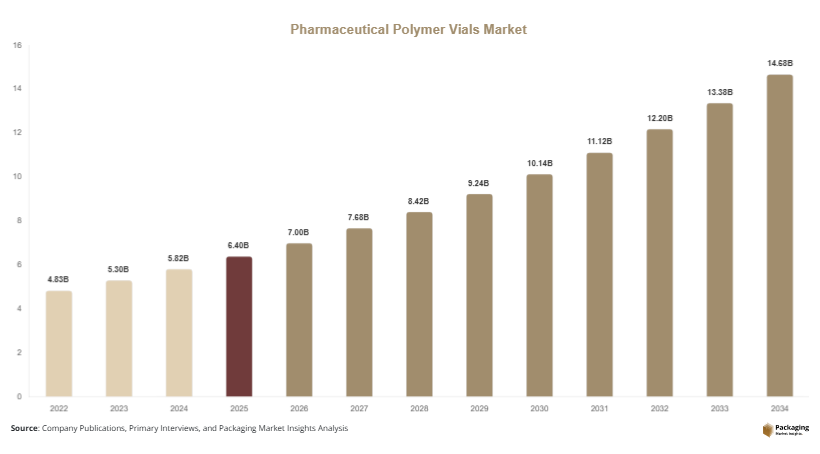

The global Pharmaceutical Polymer Vials Market size is estimated at USD 6.4 Billion in 2025 and is projected to reach USD 7.0 Billion in 2026. By 2034, the market is expected to attain a value of USD 14.8 Billion, growing at a CAGR of 9.7% during 2025–2034. This growth reflects the shift from traditional glass vials to advanced polymer-based alternatives in pharmaceutical packaging.The pharmaceutical polymer vials market is witnessing steady expansion, driven by increasing demand for lightweight, shatter-resistant, and contamination-free drug packaging solutions across global healthcare systems.

Key growth factors include the rising demand for biologics and injectable drugs, increasing concerns regarding breakage and contamination in glass packaging, and the expansion of cold chain pharmaceutical logistics. Additionally, regulatory support for high-performance and sterile packaging materials is further strengthening market adoption. Growing investments in healthcare infrastructure and pharmaceutical manufacturing are also contributing to sustained demand across developed and emerging economies.

Key Highlights

- Market size in 2025 was valued at USD 6.4 billion, reflecting steady expansion driven by increasing demand for advanced pharmaceutical packaging solutions. Growth is supported by rising adoption of polymer-based vials across global healthcare systems.

- Market size is expected to reach USD 7.0 billion in 2026, indicating continued momentum in short-term industry growth. The increase is attributed to higher production of injectable drugs and improved packaging technologies.

- The market is projected to reach USD 14.8 billion by 2034, showcasing strong long-term expansion potential. This growth is fueled by increasing biologics manufacturing and demand for high-performance packaging materials.

- The market is anticipated to grow at a CAGR of 9.7% during 2025–2034, highlighting consistent industry development. Rising investments in pharmaceutical packaging innovation are contributing to this steady growth rate.

- Strong demand from biologics, injectables, and vaccine packaging is significantly driving market expansion. Increasing global immunization programs and chronic disease treatments are further supporting this demand.

- Rising adoption of lightweight and break-resistant packaging materials is enhancing product safety and efficiency. These materials help reduce transportation risks and improve handling across pharmaceutical supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Advanced Drug Delivery-Compatible Polymer Vials

The pharmaceutical industry is increasingly adopting polymer vials designed for compatibility with advanced drug delivery systems, particularly biologics and injectable formulations. These vials offer improved chemical resistance, reduced adsorption of sensitive molecules, and better stability under extreme storage conditions. Manufacturers are focusing on multi-layer polymer structures and fluoropolymer coatings to enhance barrier properties. The trend is further supported by rising demand for personalized medicine and high-value biologic drugs that require highly stable packaging environments. Pharmaceutical companies are investing in packaging innovation to reduce product loss and improve drug efficacy across global supply chains.

Integration of Sustainable and Recyclable Polymer Materials

Sustainability is becoming a key trend in the pharmaceutical polymer vials market, with manufacturers developing recyclable and bio-based polymer solutions. Regulatory pressure to reduce plastic waste and carbon emissions is encouraging companies to adopt eco-friendly packaging materials. Pharmaceutical firms are increasingly selecting polymers that maintain sterility while offering reduced environmental impact. This trend is also influenced by global sustainability initiatives within healthcare supply chains. As a result, innovation in biodegradable polymers and reusable vial systems is gaining traction, particularly in Europe and North America, where environmental regulations are stricter.

Market Drivers

Rising Demand for Injectable and Biologic Drugs

The rapid expansion of biologics, biosimilars, and injectable therapies is a major driver of the pharmaceutical polymer vials market. These drug categories require highly stable and contamination-free packaging, making polymer vials an attractive alternative to glass. Increasing prevalence of chronic diseases such as cancer, diabetes, and autoimmune disorders is boosting demand for injectable treatments. Polymer vials provide advantages such as reduced breakage risk, lighter weight, and improved transport safety. Pharmaceutical companies are scaling up production facilities, further driving demand for reliable and high-performance packaging solutions.

Safety and Breakage Concerns in Glass Packaging

Traditional glass vials are prone to breakage, chemical leaching, and contamination risks during transportation and handling. This has led to a growing shift toward polymer-based vials, which offer higher durability and flexibility. Hospitals, clinics, and pharmaceutical distributors are increasingly adopting polymer vials to reduce operational losses and ensure patient safety. Additionally, polymer vials minimize downtime in production lines caused by breakage-related disruptions. The growing emphasis on supply chain efficiency and reduced product wastage is significantly contributing to market expansion.

Market Restraint

High Cost and Regulatory Validation Challenges

Despite strong growth potential, the pharmaceutical polymer vials market faces restraints due to high production costs and stringent regulatory approval processes. Polymer vials require extensive testing for drug compatibility, sterility, and long-term stability, which increases development timelines and costs. Regulatory agencies such as the FDA and EMA require detailed validation for packaging materials used in injectable drugs. This slows down product commercialization and limits adoption among small and mid-sized pharmaceutical companies. Additionally, advanced polymer materials and multilayer technologies increase manufacturing complexity, making cost optimization a significant challenge.

Market Opportunities

Expansion of Biopharmaceutical Manufacturing

The global expansion of biopharmaceutical production presents a significant opportunity for the pharmaceutical polymer vials market. Increasing investment in biologics manufacturing facilities, particularly in Asia Pacific and North America, is driving demand for high-performance packaging solutions. Polymer vials are well-suited for sensitive biologic formulations due to their chemical stability and reduced interaction with drug compounds. As more biologic drugs enter clinical pipelines, packaging requirements are becoming more advanced, creating opportunities for innovation in vial design and materials.

Growth in Emerging Healthcare Markets

Emerging economies in Asia Pacific, Latin America, and the Middle East are experiencing rapid healthcare infrastructure development. Rising access to healthcare services and increased pharmaceutical production capacity are boosting demand for advanced packaging solutions. Polymer vials are gaining traction due to their affordability, durability, and suitability for mass vaccination and injectable drug distribution programs. Governments are investing in local pharmaceutical manufacturing, creating opportunities for packaging suppliers to expand their regional footprint and strengthen supply chain integration.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.4 Billion |

| Market Size in 2026 | USD 7.0 Billion |

| Market Size in 2034 | USD 14.8 Billion |

| CAGR | 9.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Polyethylene (PE) and polypropylene (PP) vials dominated the market with approximately 46% share in 2024, due to their cost efficiency, chemical resistance, and suitability for a wide range of pharmaceutical formulations. These materials are widely used in injectable drug packaging, hospital supply systems, and liquid drug storage applications. Their flexibility, durability, and compatibility with mass production systems make them the preferred choice among pharmaceutical manufacturers.

Fluoropolymer-based vials are expected to register the fastest CAGR of 10.5% (2025–2034), driven by increasing demand for high-barrier packaging solutions for sensitive biologics and specialty drugs. These advanced materials offer superior chemical resistance and reduced interaction with drug formulations, making them highly suitable for next-generation pharmaceutical products.

By Capacity

Small-volume vials (1–10 ml) held the dominant share of approximately 52% in 2024, driven by their widespread use in injectable drugs, vaccines, and clinical applications. Their precision dosing capability and compatibility with high-volume pharmaceutical production make them essential in global healthcare supply chains.

Medium and large-capacity vials are expected to grow at the fastest CAGR of 9.9% (2025–2034), supported by increasing demand for biologic drug storage, hospital-level bulk medication handling, and specialty drug distribution systems. Rising demand for long-duration therapies is also supporting segment growth.

By End-Use

Pharmaceutical companies dominated the market with approximately 58% share in 2024, due to large-scale drug manufacturing and high adoption of polymer-based packaging solutions for injectables and biologics. Their focus on improving drug safety and reducing contamination risks continues to drive demand.

Contract manufacturing organizations (CMOs) are projected to grow at the fastest CAGR of 10.2% (2025–2034), driven by increasing outsourcing of pharmaceutical production and packaging operations. CMOs are rapidly adopting polymer vials to improve scalability, efficiency, and compliance with global regulatory standards.

Pharmaceutical Polymer Vials Market Segmentations

By Material Type

- Polyethylene (PE)

- Polypropylene (PP)

- Fluoropolymers

- Other Advanced Polymers

By Capacity

- Small Volume (1–10 ml)

- Medium Volume (10–50 ml)

- Large Volume (Above 50 ml)

By End-Use

- Pharmaceutical Companies

- Contract Manufacturing Organizations

- Hospitals & Clinics

- Research Laboratories

Regional Analysis

North America

North America accounted for approximately 35% share of the pharmaceutical polymer vials market in 2025, and is projected to grow at a CAGR of 9.4% (2025–2034). The region’s dominance is supported by advanced pharmaceutical manufacturing capabilities, strong biologics production, and early adoption of high-performance packaging solutions. Increasing demand for injectable drugs and vaccines continues to strengthen market expansion across the region.

The United States leads the North American market due to its large pharmaceutical production base and strong R&D ecosystem. A key growth factor is the rapid adoption of advanced drug delivery systems requiring contamination-free, lightweight, and break-resistant polymer vial solutions.

Europe

Europe held around 27% share in 2025, with a projected CAGR of 9.2% (2025–2034). Growth in the region is driven by strict regulatory standards for pharmaceutical packaging, increasing sustainability requirements, and rising demand for biologics. Pharmaceutical companies in Europe are increasingly shifting toward polymer-based solutions to improve safety and reduce packaging waste.

Germany dominates the regional market due to its strong pharmaceutical manufacturing and packaging engineering industry. A key growth factor is the implementation of stringent EU regulations promoting sustainable and recyclable pharmaceutical packaging materials.

Asia Pacific

Asia Pacific accounted for approximately 28% share in 2025, and is expected to record the fastest CAGR of 10.3% (2025–2034). Growth is supported by expanding pharmaceutical manufacturing, rising healthcare expenditure, and increasing production of generic and biologic drugs. Rapid urbanization and healthcare modernization are further supporting demand for advanced packaging solutions.

China leads the regional market due to its large-scale pharmaceutical production and strong export-oriented supply chain. A key growth factor is increasing government investment in domestic drug manufacturing and vaccine production capabilities.

Middle East & Africa

The Middle East & Africa region held approximately 5% share in 2025, with a projected CAGR of 8.6% (2025–2034). Growth is driven by improving healthcare infrastructure, increasing pharmaceutical imports, and rising demand for safe and contamination-resistant packaging solutions. The region is gradually adopting modern pharmaceutical packaging technologies.

Saudi Arabia leads the regional market due to ongoing healthcare modernization programs. A key growth factor is the expansion of pharmaceutical distribution networks and government initiatives to strengthen vaccine storage and cold chain systems.

Latin America

Latin America accounted for approximately 5% share in 2025, with a projected CAGR of 8.9% (2025–2034). Growth is driven by increasing pharmaceutical consumption, expanding healthcare access, and modernization of drug distribution systems. Countries in the region are increasingly adopting advanced packaging formats to reduce contamination risks.

Brazil dominates the regional market due to its strong pharmaceutical production base. A key growth factor is rising government investment in healthcare infrastructure and expansion of domestic drug manufacturing capabilities.

Competitive Landscape

The pharmaceutical polymer vials market is moderately consolidated, with key players focusing on innovation, material enhancement, and regulatory compliance. Major companies include Gerresheimer AG, SCHOTT AG, West Pharmaceutical Services, Nipro Corporation, and Berry Global Inc. These companies are investing in advanced polymer technologies and expanding production capacity to meet rising global demand.

Gerresheimer AG leads the market, supported by its strong product portfolio in pharmaceutical packaging. A recent development includes expansion of its polymer packaging production facility in Europe to meet growing biologics demand.

Key Players List

- Gerresheimer AG

- SCHOTT AG

- West Pharmaceutical Services

- Nipro Corporation

- Berry Global Inc.

- Amcor plc

- Corning Incorporated

- Stevanato Group

- AptarGroup Inc.

- Ompi (Stevanato Group)

- Becton Dickinson and Company

- Vetter Pharma International

- Shandong Pharmaceutical Glass

- Raepak Ltd.

- RPC Group