Pharmaceutical Packaging Machines Market Size and Growth

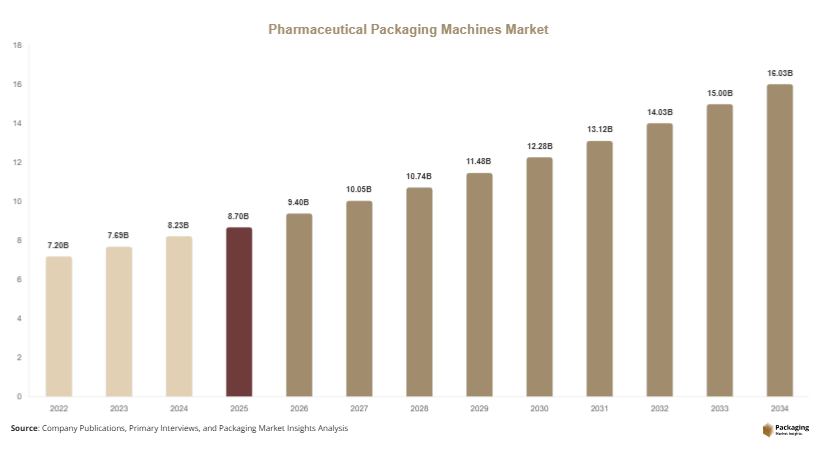

The global pharmaceutical packaging machines market was valued at USD 8.7 billion in 2025 and is estimated to reach USD 9.4 billion in 2026. Supported by rising medicine demand and stricter packaging standards, the market is projected to reach USD 16.1 billion by 2034, growing at a CAGR of 6.9% from 2025 to 2034. The market continues to benefit from increasing production of oral solids, injectables, biologics, and personalized medicine products that require highly controlled packaging processes. The pharmaceutical packaging machines market is expanding steadily as pharmaceutical manufacturers increase investment in automated production systems to improve safety, precision, and compliance.

One major growth factor is the increasing global demand for pharmaceutical products due to aging populations and the growing prevalence of chronic diseases. Drug manufacturers are scaling production capacity and adopting advanced packaging systems that improve throughput while reducing contamination risk. Another key growth factor is the rise of serialization requirements and track-and-trace regulations. Regulatory agencies are requiring pharmaceutical firms to implement machine systems that can print, inspect, and verify package data for product authentication and patient safety. These requirements are accelerating replacement of conventional machines with digital packaging systems.

Key Market Insights

- Asia Pacific dominated the market with a 36.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.2%.

- Blister packaging machines led the type segment with a 31.5% share, while labeling machines are expected to grow at a CAGR of 7.4%.

- Solid dosage packaging dominated with a 44.7% share, while injectable packaging is forecasted to grow at a CAGR of 7.6%.

- Pharmaceutical manufacturers led the end-use segment with 63.2% share, while contract packaging providers are expected to grow at a CAGR of 7.3%.

- The United States remained the dominant country with a market size of USD 1.9 billion in 2025 and USD 2.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of smart automation across packaging lines

The pharmaceutical packaging machines market is seeing greater adoption of smart automation technologies across production facilities. Manufacturers are deploying machines with vision inspection, robotic handling, and cloud-connected monitoring systems to improve consistency. Smart automation allows operators to track production data in real time, identify packaging defects early, and reduce downtime. Pharmaceutical companies are using these systems to maintain strict compliance while improving operational efficiency. Connected packaging machines also support predictive maintenance, helping facilities reduce repair costs and avoid unexpected shutdowns. This shift is becoming important as companies aim to increase productivity without compromising product quality.

Shift toward flexible machinery for multiple drug formats

Drug manufacturers increasingly need packaging machines that can manage varied dosage forms without long changeover periods. Machines capable of handling tablets, capsules, syringes, vials, and pouches on a shared platform are becoming more valuable. Flexible equipment allows pharmaceutical companies to package small batch therapies and specialty medicines more efficiently. This trend supports personalized medicine production where packaging requirements can differ between products. Machine suppliers are responding by developing modular equipment that can be upgraded or reconfigured. Flexible systems help producers lower capital costs while adapting to changing market demand and regulatory requirements.

Market Drivers

Rising pharmaceutical production worldwide

Growing pharmaceutical production is one of the strongest drivers for the pharmaceutical packaging machines market. Demand for prescription drugs, vaccines, and over-the-counter medicines continues to increase across developed and developing regions. Manufacturers are expanding plants and modernizing packaging operations to meet rising output targets. Packaging machines help improve speed while maintaining sterility and accuracy. Automated systems also reduce labor dependency and improve packaging consistency. As governments and healthcare systems invest in medicine availability, pharmaceutical companies continue purchasing advanced machinery that can support higher production volumes and stricter safety standards.

Stronger regulations for product safety and traceability

Regulatory requirements for serialization and anti-counterfeit protection are pushing investment in advanced packaging machinery. Authorities in many countries now require each pharmaceutical package to carry a unique identifier that can be tracked through the supply chain. Machines equipped with coding, scanning, and verification capabilities are becoming essential. These systems help reduce counterfeit medicine risks and improve recall management. Companies are also adopting tamper-evident packaging equipment to enhance patient safety. As compliance rules become more complex, pharmaceutical firms increasingly rely on modern packaging machines to meet legal standards efficiently.

Market Restraints

High equipment cost and validation complexity

A major restraint in the pharmaceutical packaging machines market is the high cost of equipment and validation procedures. Advanced pharmaceutical packaging systems require precise engineering, specialized software, and regulatory certification, making them expensive for smaller manufacturers. Beyond purchase costs, companies must spend time validating each machine before production begins. Validation includes performance testing, documentation, and regulatory review, which can delay implementation. For example, a mid-sized manufacturer upgrading from manual blister packing to a fully automated line may face substantial capital and training costs. These barriers can slow adoption, especially among regional pharmaceutical firms with limited investment capacity.

Market Opportunities

Expansion of biologics and specialty drug packaging

The rapid growth of biologics creates new opportunities for the pharmaceutical packaging machines market. Biologic medicines often require specialized packaging for temperature-sensitive injectables and sterile products. Machines designed for syringes, cartridges, and vials are becoming more important as pharmaceutical companies expand biologic pipelines. These products demand precise filling and sealing systems that maintain product stability. Machine suppliers can benefit by offering high-precision equipment for complex drug formats. As specialty medicines gain larger market share, demand for advanced packaging machinery tailored to these therapies is expected to rise.

Growth of pharmaceutical manufacturing in emerging economies

Emerging economies are becoming attractive growth areas for packaging machine suppliers. Countries across Asia Pacific, Latin America, and the Middle East are increasing local drug production to improve healthcare access and reduce import dependence. Governments are supporting pharmaceutical manufacturing through incentives and industrial investment programs. New production facilities need modern packaging equipment to meet international quality standards. Local manufacturers are also replacing older machinery with efficient automated systems. This shift creates long-term opportunities for machine suppliers that can offer scalable and cost-effective solutions for regional pharmaceutical producers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.7 Billion |

| Market Size in 2026 | USD 9.4 Billion |

| Market Size in 2034 | USD 16.1 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Machine Type

Blister packaging machines accounted for 31.5% of market revenue in 2024, making them the dominant machine type. These machines are widely used for tablets and capsules because they provide strong product protection, clear visibility, and unit-dose convenience. Pharmaceutical companies prefer blister systems because they improve compliance and reduce contamination risk. Modern blister lines now include integrated inspection systems that verify seal quality and product placement. Demand remains strong because oral solid dosage products continue to represent a large share of global pharmaceutical production. Their efficiency and compatibility with regulatory requirements support continued dominance in the segment.

Labeling machines are expected to grow at a CAGR of 7.4% through 2034. This growth is driven by stricter serialization rules and demand for accurate product identification. Advanced labeling systems can print and verify barcodes, patient information, and anti-counterfeit data in a single operation. Manufacturers are upgrading these machines to support flexible packaging formats and smaller production runs. Smart labeling equipment also integrates with digital production systems for better traceability. As pharmaceutical companies focus more on patient safety and compliance, labeling systems are becoming an increasingly important growth segment.

By Packaging Format

Solid dosage packaging held 44.7% of market share in 2024 because tablets and capsules remain the most common drug forms globally. Packaging machines designed for bottles, blister packs, and sachets support high-volume production and precise counting. Pharmaceutical firms rely on these systems to maintain dosage accuracy and reduce contamination. Automation in this segment continues to improve output and reduce operator intervention. Solid dosage packaging remains essential in both branded and generic drug manufacturing because of the large patient base served by oral medicines across multiple therapeutic areas.

Injectable packaging is forecast to grow at a CAGR of 7.6% through 2034. Growth is linked to rising demand for biologics, vaccines, and specialty drugs that require sterile filling. Machines used for syringes, cartridges, and vials need advanced controls to protect sensitive formulations. Manufacturers are investing in isolator technology and robotic systems to maintain sterile environments. The increase in chronic disease treatment and self-administered medicines is also encouraging investment in injectable packaging systems. These factors are supporting faster expansion of this segment.

By End Use

Pharmaceutical manufacturers accounted for 63.2% of market revenue in 2024, representing the largest end-use segment. Large drug companies invest heavily in automated packaging systems to improve productivity and maintain regulatory compliance. These firms require integrated lines that can perform filling, sealing, coding, inspection, and cartoning. Centralized manufacturing operations also support high-capacity machine installations. As medicine demand rises, internal packaging capacity remains important for protecting supply reliability and controlling quality standards. This keeps pharmaceutical manufacturers as the primary buyers of packaging machinery.

Contract packaging providers are projected to grow at a CAGR of 7.3% through 2034. Outsourcing trends are encouraging drug companies to partner with specialized providers for packaging operations. Contract firms need flexible machines that can handle multiple products and changing production volumes. Many providers are upgrading facilities with modular systems that reduce changeover time. Demand for outsourced packaging is increasing because it helps pharmaceutical companies reduce costs and improve speed to market. This makes contract packaging a fast-growing end-use segment.

Pharmaceutical Packaging Machines Market Segmentations

By Machine Type

- Blister Packaging Machines

- Filling Machines

- Labeling Machines

- Cartoning Machines

By Packaging Format

- Solid Dosage Packaging

- Injectable Packaging

- Liquid Packaging

- Powder Packaging

By End Use

- Pharmaceutical Manufacturers

- Contract Packaging Providers

- Biotechnology Companies

- Research Laboratories

Regional Analysis

North America

North America accounted for 29.4% of the pharmaceutical packaging machines market in 2025 and is expected to grow at a CAGR of 6.4% through 2034. The region benefits from advanced pharmaceutical manufacturing infrastructure and strong regulatory enforcement. Companies continue to invest in automated machinery to improve efficiency and meet serialization requirements. Demand for biologics and specialty medicines also supports installation of advanced packaging systems across pharmaceutical production sites.

The United States leads the regional market because of its extensive pharmaceutical industry and continued capital investment in packaging automation. A unique growth factor is the expansion of domestic drug manufacturing encouraged by supply chain security initiatives. Pharmaceutical firms are building new facilities and modernizing packaging lines to reduce overseas dependence while maintaining compliance with strict packaging standards.

Europe

Europe represented 25.7% of the market in 2025 and is projected to expand at a CAGR of 6.6% during the forecast period. Regional growth is supported by strong pharmaceutical exports and increasing adoption of sustainable machine technologies. European manufacturers are integrating digital systems that reduce material waste and improve production monitoring. Demand for compliant blister and carton packaging remains stable across the region.

Germany dominates the European market due to its strong pharmaceutical equipment manufacturing base and advanced industrial capabilities. A unique growth factor is the region’s emphasis on environmentally efficient packaging operations. Companies are adopting machinery that supports recyclable materials and lower energy consumption, which improves long-term operating efficiency and supports environmental targets.

Asia Pacific

Asia Pacific held 36.8% of the pharmaceutical packaging machines market in 2025 and is expected to grow at a CAGR of 7.1% through 2034. Rising healthcare spending and expanding generic drug production are supporting demand for packaging equipment. Regional manufacturers are investing in automated systems to improve competitiveness and meet export quality requirements. Growing domestic medicine demand also encourages equipment upgrades.

China remains the leading country in the region due to its large pharmaceutical manufacturing capacity and expanding healthcare sector. A unique growth factor is government support for domestic pharmaceutical modernization. Public incentives and industrial policy are encouraging companies to install advanced packaging lines that improve quality and strengthen global export competitiveness.

Middle East & Africa

The Middle East & Africa accounted for 4.5% of the market in 2025 and is projected to grow at a CAGR of 6.2% through 2034. The region is gradually increasing pharmaceutical production capacity to improve local medicine availability. Packaging machine demand is rising as manufacturers invest in more efficient systems that reduce waste and improve quality control.

Saudi Arabia leads the regional market because of expanding pharmaceutical manufacturing investment. A unique growth factor is government healthcare diversification programs that encourage domestic drug production. New industrial facilities require modern packaging equipment capable of meeting regional safety requirements and supporting local medicine supply objectives.

Latin America

Latin America held 3.6% of the pharmaceutical packaging machines market in 2025 and is expected to grow at a CAGR of 7.2% through 2034. Rising healthcare access and stronger pharmaceutical production are supporting equipment demand. Manufacturers are replacing aging systems with automated machinery that improves packaging accuracy and production speed. Regional modernization efforts continue to support market expansion.

Brazil dominates the regional market due to its established pharmaceutical sector and expanding healthcare infrastructure. A unique growth factor is the rise of regional contract manufacturing services. More international pharmaceutical firms are outsourcing packaging operations to Latin American facilities, increasing demand for modern packaging equipment across the country.

Competitive Landscape

The pharmaceutical packaging machines market is moderately consolidated, with established global manufacturers competing through innovation, compliance capability, and service support. Leading companies focus on developing machines that improve productivity while meeting strict pharmaceutical regulations. Strategic partnerships, acquisitions, and digital upgrades remain common as companies strengthen their global positions.

IMA Group remains a leading participant because of its broad portfolio of blister, filling, and cartoning equipment. The company recently introduced a new connected packaging platform that improves predictive maintenance and machine monitoring. Other major companies including Uhlmann Group, Marchesini Group, Körber AG, and Syntegon Technology continue expanding product lines that support flexible pharmaceutical packaging operations. Competition is increasingly centered on automation, validation support, and sustainability.

Key Players List

- IMA Group

- Uhlmann Group

- Marchesini Group S.p.A.

- Körber AG

- Syntegon Technology GmbH

- Romaco Group

- OPTIMA packaging group GmbH

- MG2 S.r.l.

- ACG Worldwide

- Coesia S.p.A.

- Bosch Packaging Systems

- Bausch+Ströbel

- Multivac Group

- Harro Höfliger

- Koruma GmbH