Metalized Flexible Packaging Market Size and Growth

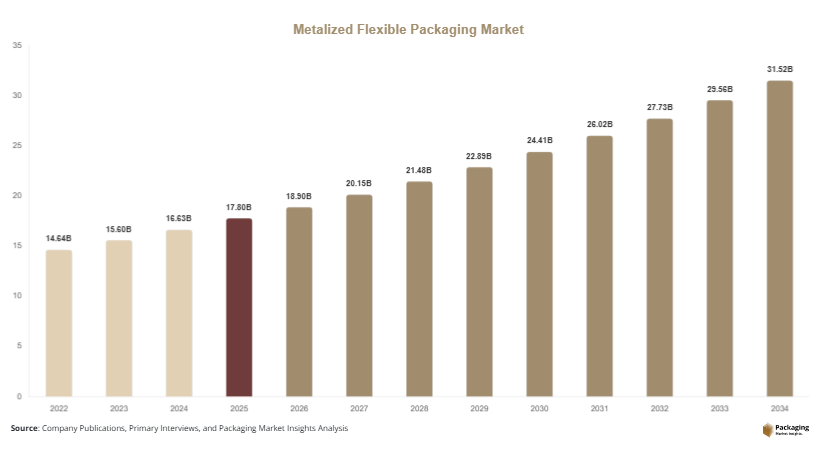

The global metalized flexible packaging market size is estimated at USD 17.8 billion in 2025 and is projected to reach USD 18.9 billion in 2026. By 2034, the market is expected to attain approximately USD 31.6 billion, registering a CAGR of 6.6% during the forecast period (2025–2034). Increasing demand for packaged food products, growth in pharmaceutical packaging requirements, and rising adoption of flexible packaging formats are among the primary factors driving market growth.

One major growth factor is the expanding food and beverage sector, where metalized packaging provides excellent barrier properties that help preserve product quality and freshness. Another significant factor is the increasing shift from rigid packaging to flexible alternatives due to transportation efficiency, lower material consumption, and reduced storage requirements. Additionally, advances in vacuum metallization technology and recyclable flexible packaging structures are improving product performance while supporting sustainability objectives.

Key Market Insights

- Asia Pacific dominated the market with a 41.3% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.2%.

- Metalized films led the type segment with a 58.4% share.

- Plastic substrates dominated the material segment with a 64.7% share.

- Food & beverage applications led the end-use segment with a 52.8% share.

- The US remained the dominant country with a market size of USD 3.8 billion in 2025 and USD 4.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Recyclable Metalized Packaging Structures

A significant trend in the metalized flexible packaging market is the growing development of recyclable metalized packaging formats. Packaging manufacturers are investing in mono-material structures that maintain barrier performance while improving recyclability. Traditional multilayer packaging has often faced recycling challenges, prompting companies to redesign packaging architectures. For example, several food brands are adopting recyclable metalized polyethylene packaging for snacks and confectionery products. These innovations help companies meet sustainability targets while preserving product protection. The future impact of this trend is expected to be substantial as regulatory frameworks increasingly emphasize recyclability and waste reduction. Continued advancements in material science will likely accelerate the commercialization of recyclable metalized packaging solutions.

Expansion of High-Barrier Packaging for Premium Food Products

Demand for high-barrier packaging solutions is increasing across premium food categories, driving adoption of metalized flexible packaging. Products such as coffee, ready-to-eat meals, pet food, and specialty snacks require packaging capable of protecting flavor, aroma, and freshness. Metalized films provide effective barriers against oxygen, moisture, and ultraviolet light while maintaining attractive visual appeal. For example, coffee manufacturers frequently utilize metalized pouches to preserve aroma and extend shelf life. Looking ahead, rising consumption of premium packaged foods and convenience products is expected to strengthen demand for advanced barrier packaging technologies, supporting long-term market growth.

Market Drivers

Growing Demand for Packaged Food and Beverage Products

The increasing consumption of packaged food and beverage products is a major driver of the metalized flexible packaging market. Urbanization, changing lifestyles, and rising demand for convenience foods have encouraged manufacturers to adopt packaging solutions that enhance product protection and shelf life. Metalized flexible packaging offers strong barrier performance while remaining lightweight and cost-efficient. For example, snack foods, confectionery products, and beverage powders commonly utilize metalized films to maintain freshness. The direct relationship between packaged food demand and packaging requirements continues to create substantial growth opportunities. As food processing industries expand globally, demand for metalized flexible packaging is expected to increase steadily.

Shift Toward Lightweight and Cost-Efficient Packaging

Manufacturers are increasingly replacing rigid packaging formats with flexible alternatives to reduce transportation costs, storage requirements, and material consumption. Metalized flexible packaging provides a lightweight solution while maintaining excellent protective properties. This shift helps companies improve operational efficiency and reduce environmental impact associated with packaging logistics. For example, pet food manufacturers are increasingly utilizing metalized pouches instead of rigid containers due to improved transportation efficiency. The resulting cost savings and sustainability benefits are driving broader adoption across industries. Continued emphasis on supply chain optimization is expected to support long-term market growth.

Market Restraint

Recycling Challenges Associated with Multi-Layer Structures

A major restraint affecting the metalized flexible packaging market is the recycling complexity associated with traditional multi-layer packaging structures. Many metalized flexible packaging products consist of multiple material layers designed to provide superior barrier performance. However, separating these layers during recycling processes can be difficult, limiting recyclability and creating waste management challenges. For example, certain metalized laminates used in food packaging may not be compatible with existing recycling infrastructure. These limitations have raised concerns among regulators, environmental organizations, and brand owners. While manufacturers are developing recyclable alternatives, adoption remains gradual due to technological and economic considerations. As sustainability expectations continue to rise, addressing recycling challenges will remain an important priority for industry participants.

Market Opportunities

Growth of Sustainable Metalized Packaging Technologies

Sustainability initiatives present significant opportunities for the development of environmentally responsible metalized packaging solutions. Manufacturers are investing in recyclable films, bio-based substrates, and low-metal-content coatings that improve environmental performance without compromising functionality. Brands increasingly seek packaging solutions that align with circular economy objectives and consumer expectations regarding sustainability. Future innovations may include compostable metalized structures and advanced recycling-compatible materials. As environmental regulations continue to evolve, companies capable of delivering sustainable metalized packaging technologies are expected to gain competitive advantages.

Expansion in Pharmaceutical and Healthcare Packaging

The pharmaceutical sector offers strong growth opportunities for metalized flexible packaging suppliers. Many pharmaceutical products require protection from moisture, oxygen, and light exposure to maintain efficacy and stability. Metalized packaging provides effective barrier performance while supporting lightweight packaging requirements. Applications include sachets, blister packaging components, diagnostic kits, and medical device packaging. Future growth is expected to be supported by increasing healthcare expenditures, expansion of pharmaceutical manufacturing, and rising demand for specialty medicines. Technological advancements in pharmaceutical-grade packaging materials will likely create additional opportunities for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.8 Billion |

| Market Size in 2026 | USD 18.9 Billion |

| Market Size in 2034 | USD 31.6 Billion |

| CAGR | 6.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Metalized films dominated the market in 2024, accounting for approximately 58.4% of total revenue. Their leadership is attributed to extensive utilization across food, beverage, pharmaceutical, and personal care applications. Metalized films offer excellent barrier properties while maintaining flexibility, lightweight characteristics, and cost efficiency. Food manufacturers frequently use metalized films for snack foods, coffee packaging, confectionery products, and dry food applications. The segment also benefits from compatibility with high-speed packaging machinery and advanced printing technologies. Continuous improvements in metallization processes and film performance continue to support market dominance.

Metalized pouches are expected to be the fastest-growing type segment, expanding at a CAGR of 7.1% through 2034. Growth is driven by increasing demand for stand-up pouches, resealable packaging, and convenience-oriented formats. Consumers increasingly prefer packaging that offers portability and ease of use, encouraging adoption across food and household product categories. Manufacturers are introducing recyclable pouch structures and improved closure systems to meet evolving consumer preferences. Future growth opportunities are expected to emerge from premium packaging applications and e-commerce packaging requirements.

By Material

Plastic substrates held the largest market share in 2024, representing approximately 64.7% of total market revenue. These materials remain widely used because they offer excellent flexibility, durability, and compatibility with metallization technologies. Common substrate materials include polyethylene, polypropylene, and polyester films. Industry examples include snack packaging, beverage pouches, pet food packaging, and pharmaceutical sachets. Plastic substrates also support high-quality printing and efficient processing capabilities. Ongoing material innovation aimed at improving recyclability and reducing environmental impact continues to strengthen the segment's market position.

Paper-based substrates are projected to be the fastest-growing material segment, registering a CAGR of 7.4% through 2034. Sustainability concerns and regulatory pressures are encouraging adoption of renewable packaging materials. Metalized paper packaging provides attractive visual appeal while supporting improved recyclability compared to some traditional plastic structures. Growth is particularly evident in confectionery, premium food, and consumer goods applications. Future developments are expected to focus on improving moisture resistance and barrier performance through innovative coating technologies. These advancements are likely to expand adoption across multiple industries.

By End-Use

Food & beverage applications accounted for the largest market share in 2024, contributing approximately 52.8% of total revenue. The segment benefits from increasing demand for shelf-life extension, product freshness preservation, and attractive packaging formats. Metalized flexible packaging is widely used for snacks, coffee, dairy products, powdered beverages, confectionery, and ready-to-eat foods. The excellent barrier performance of metalized structures helps maintain product quality during storage and transportation. Rising consumption of convenience foods and premium packaged products continues to support segment growth across global markets.

Pharmaceutical packaging is expected to be the fastest-growing end-use segment, registering a CAGR of 7.0% through 2034. Growth is driven by increasing pharmaceutical production, expanding healthcare expenditures, and rising demand for moisture-sensitive medicines. Metalized packaging provides protection against environmental factors that may compromise product stability. Applications include sachets, medical device packaging, and specialized pharmaceutical packaging formats. Future growth will be supported by increasing healthcare access, growth in specialty pharmaceuticals, and ongoing innovation in packaging technologies designed for regulated healthcare applications.

Metalized Flexible Packaging Market Segmentations

By Type

- Metalized Films

- Metalized Pouches

- Metalized Bags

- Metalized Wraps

By Material

- Plastic Substrates

- Paper-Based Substrates

- Aluminum-Based Structures

By End-User

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Products

- Household Products

Regional Analysis

North America

North America accounted for approximately 26.7% of the global metalized flexible packaging market share in 2025 and is projected to expand at a CAGR of 6.1% through 2034. The region benefits from strong demand for packaged food products, advanced packaging technologies, and growing sustainability initiatives among major consumer brands. Food manufacturers are increasingly utilizing metalized packaging to improve shelf life and maintain product quality. The region also benefits from well-established retail and e-commerce sectors that require durable and lightweight packaging solutions. Investments in recyclable flexible packaging technologies are further supporting market expansion across North America.

The United States dominates the regional market. A unique growth driver is the strong demand for premium packaged snacks and convenience foods. Manufacturers are increasingly adopting high-barrier metalized packaging formats to preserve freshness and improve product presentation. An industry trend involves the introduction of recyclable metalized films by leading packaging companies to meet retailer sustainability requirements. This growing focus on premium food packaging and sustainability is expected to support continued market growth.

Europe

Europe held approximately 24.5% market share in 2025 and is expected to register a CAGR of 6.3% during the forecast period. Market growth is supported by stringent packaging regulations, sustainability objectives, and increasing demand for resource-efficient packaging formats. European manufacturers are investing in recyclable metalized packaging solutions to comply with environmental standards and reduce packaging waste. Food processing industries remain major consumers of metalized flexible packaging. Rising demand for premium food products and expanding private-label packaging activities are also contributing to regional market growth.

Germany remains the dominant country within Europe. A unique growth factor is the country's emphasis on circular economy principles and packaging innovation. Packaging manufacturers are actively developing recyclable metalized structures compatible with existing waste management systems. An emerging industry trend involves collaboration between food producers and packaging suppliers to improve packaging sustainability while maintaining barrier performance. These efforts are expected to support continued market expansion across the German market.

Asia Pacific

Asia Pacific dominated the market with a 41.3% share in 2025 and is projected to grow at a CAGR of 7.0% through 2034. Rapid urbanization, increasing disposable incomes, and expanding food processing industries are driving regional demand. Growth in packaged food consumption and e-commerce activities has increased the need for lightweight, protective packaging solutions. Investments in manufacturing infrastructure and packaging technology upgrades are also contributing to market development. Several countries within the region are emerging as important production hubs for flexible packaging materials.

China leads the Asia Pacific market. A unique growth driver is the rapid expansion of domestic packaged food manufacturing. Food producers are increasingly utilizing metalized packaging to enhance product preservation and improve retail shelf appeal. Industry trends indicate growing adoption of high-performance metalized pouches for snacks, beverages, and convenience foods. As consumption of packaged products continues to rise, demand for advanced flexible packaging solutions is expected to remain strong throughout the forecast period.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.6% of global market revenue in 2025 and is forecast to expand at a CAGR of 6.7%. Increasing demand for packaged foods, expanding retail networks, and growth in healthcare sectors are supporting market development. Harsh climatic conditions in several countries increase the importance of high-barrier packaging capable of protecting products from moisture and temperature fluctuations. Food imports and pharmaceutical distribution activities continue to generate demand for metalized flexible packaging solutions. Investments in packaging manufacturing capacity are expected to contribute to future growth.

The United Arab Emirates dominates the regional market. A unique growth factor is the country's role as a regional trade and logistics hub. Imported food and consumer goods frequently utilize metalized packaging to maintain product quality throughout transportation and storage. An emerging trend involves increasing demand for premium packaged food products within modern retail channels. These developments are expected to support continued adoption of metalized packaging technologies across the region.

Latin America

Latin America represented approximately 3.9% market share in 2025 and is expected to register the fastest CAGR of 7.2% during the forecast period. Market growth is driven by expanding food processing industries, increasing urban populations, and rising demand for packaged consumer products. Manufacturers are adopting flexible packaging formats to improve operational efficiency and reduce packaging costs. Growing exports of processed foods are also creating demand for high-barrier packaging materials. Improvements in retail infrastructure and distribution networks continue to support market expansion throughout the region.

Brazil remains the dominant country in Latin America. A unique growth driver is the increasing export of processed food products requiring extended shelf life and product protection. Food manufacturers are utilizing metalized packaging solutions to meet international quality standards and preserve product integrity during transportation. Industry trends indicate growing investment in flexible packaging production facilities to support export-oriented industries. These developments are expected to contribute to sustained market growth.

Competitive Landscape

The metalized flexible packaging market is characterized by the presence of global packaging manufacturers competing through innovation, sustainability initiatives, production expansion, and strategic partnerships. Companies are focusing on developing recyclable packaging structures while maintaining high barrier performance and operational efficiency.

Amcor plc is recognized as a leading company in the market due to its extensive flexible packaging portfolio, global manufacturing presence, and continued investment in sustainable packaging technologies. The company recently introduced recyclable metalized packaging solutions designed for food applications while maintaining barrier performance.

Other major participants include Mondi plc, Berry Global Inc., Constantia Flexibles, and Huhtamaki Oyj. These companies continue investing in advanced metallization technologies, recyclable substrate development, and packaging innovation. Strategic collaborations with food and consumer goods manufacturers remain common approaches for expanding market presence. Sustainability-focused product development and capacity expansion initiatives are expected to remain important competitive strategies throughout the forecast period.

Key Players List

- Amcor plc

- Mondi plc

- Berry Global Inc.

- Constantia Flexibles Group GmbH

- Huhtamaki Oyj

- Sealed Air Corporation

- UFlex Limited

- Cosmo Films Ltd.

- Jindal Poly Films Ltd.

- ProAmpac LLC

- Coveris Holdings S.A.

- Sonoco Products Company

- Transcontinental Inc.

- Winpak Ltd.

- Glenroy Inc.

- FlexFilms

- Toray Plastics Inc.

- Innovia Films Ltd.