Gable Top Liquid Cartons Market Size and Growth

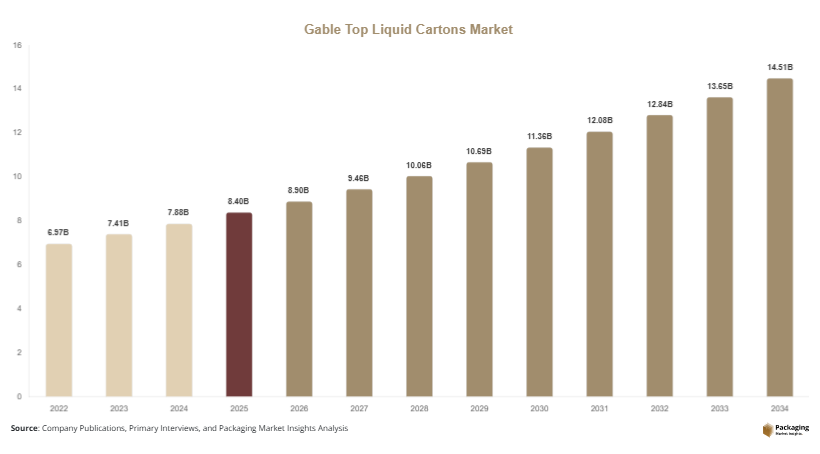

The global gable top liquid cartons market size is estimated at USD 8.4 billion in 2025, rising to USD 8.9 billion in 2026. By 2034, the market is projected to reach approximately USD 14.8 billion, registering a compound annual growth rate (CAGR) of 6.3% during 2025–2034. Growth is primarily driven by rising consumption of packaged dairy products, fruit juices, plant-based beverages, and ready-to-drink (RTD) beverages across both developed and emerging economies. The gable top liquid cartons market is experiencing steady expansion as industries increasingly shift toward sustainable, convenient, and lightweight liquid packaging formats.

A major growth driver is the global shift toward sustainable packaging alternatives. Gable top cartons, made primarily from paperboard with polyethylene or bio-based coatings, offer recyclability advantages compared to traditional plastic bottles. Governments and regulatory bodies in Europe and parts of Asia are actively promoting paper-based packaging, encouraging beverage manufacturers to transition toward carton formats. Another key factor is the rapid expansion of the dairy industry, especially in Asia Pacific and Latin America, where urbanization and income growth are increasing packaged milk consumption. Additionally, rising demand for safe, tamper-resistant packaging in liquid food products is further supporting adoption.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Aseptic gable top cartons led the type segment with a 32.8% share.

- Paperboard-based packaging dominated with a 55.1% share.

- Dairy applications led the segment with 46.5% share.

- The US remained the dominant country with a market size of USD 1.7 billion in 2025 and USD 1.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Bio-Based Carton Materials

One of the most significant trends shaping the gable top liquid cartons market is the transition toward sustainable and bio-based materials. Manufacturers are increasingly replacing fossil-based polyethylene coatings with bio-polyethylene derived from sugarcane and other renewable sources. This shift is largely driven by environmental regulations and corporate sustainability commitments. For example, leading beverage brands in Europe have started introducing cartons with fully recyclable fiber-based barriers. This reduces dependency on plastic and aligns with circular economy principles. Over time, the trend is expected to influence supply chain structures, pushing paperboard suppliers and packaging converters to adopt greener raw materials and closed-loop recycling systems.

Expansion of Aseptic and Extended Shelf-Life Packaging

Another important trend is the growing adoption of aseptic processing in gable top cartons. Aseptic cartons allow beverages such as milk, juice, and plant-based drinks to remain shelf-stable for extended periods without refrigeration. This has transformed distribution models, especially in regions with limited cold chain infrastructure. For instance, dairy companies in India and Southeast Asia are increasingly adopting aseptic gable top cartons to reach rural markets efficiently. The trend is also supported by advancements in sterilization and filling technologies, which reduce contamination risks. In the future, this will enable wider global distribution of premium beverage products and reduce food waste across supply chains.

Market Drivers

Rising Demand for Packaged Dairy and Beverages

The growth of the packaged dairy and beverage industry is a key driver of the gable top liquid cartons market. Increasing urbanization, rising disposable incomes, and changing dietary habits are fueling demand for milk, flavored dairy drinks, and juices. In countries like India and China, organized dairy distribution is expanding rapidly, replacing loose milk consumption with packaged alternatives. Gable top cartons are preferred due to their hygiene, ease of handling, and storage efficiency. For example, major dairy brands use these cartons for daily milk distribution in metropolitan areas, ensuring product safety and freshness. This rising consumption pattern directly strengthens market demand.

Sustainability Regulations and Plastic Reduction Policies

Government regulations aimed at reducing plastic waste are significantly driving adoption of paper-based gable top cartons. Many countries in Europe and parts of Asia have introduced strict guidelines restricting single-use plastics in beverage packaging. As a result, manufacturers are shifting toward recyclable carton solutions. Beverage companies are also under pressure to meet sustainability targets, leading them to replace PET bottles with carton-based packaging. For instance, several juice brands in Scandinavia have transitioned to fully recyclable gable top cartons as part of their carbon neutrality goals. This regulatory push is expected to continue driving long-term market expansion.

Market Restraint

High Production and Recycling Infrastructure Limitations

A major restraint in the gable top liquid cartons market is the relatively high cost associated with production and recycling infrastructure. While cartons are environmentally friendly, they require specialized multi-layer separation processes to recycle paperboard and plastic coatings efficiently. In many developing countries, such infrastructure is limited, resulting in lower recycling efficiency. This reduces the environmental advantage and increases disposal challenges. Additionally, production of aseptic cartons involves advanced machinery and sterilization systems, increasing capital costs for manufacturers. For small and medium beverage producers, this cost barrier can limit adoption, especially in price-sensitive markets.

Market Opportunities

Growth in Plant-Based and Functional Beverages

The rising popularity of plant-based beverages such as almond milk, oat milk, and soy-based drinks presents a strong opportunity for gable top cartons. These products require packaging that ensures freshness, shelf stability, and eco-friendly branding. Gable top cartons are increasingly preferred by health-conscious consumers due to their recyclable nature and clean-label appeal. For example, several plant-based beverage startups in North America and Europe exclusively use carton packaging to differentiate their products. As demand for dairy alternatives grows globally, packaging suppliers have opportunities to develop specialized barrier coatings and premium carton designs.

Expansion of Rural Beverage Distribution Networks

Another key opportunity lies in expanding beverage distribution into rural and semi-urban markets, particularly in Asia Pacific and Africa. Gable top cartons are well-suited for regions with limited refrigeration infrastructure due to their aseptic capabilities. Governments and private dairy companies are investing in rural supply chains to improve nutrition access, increasing demand for long-life packaged milk. For instance, dairy cooperatives in India use gable top cartons to distribute milk across remote villages efficiently. This expansion of distribution networks is expected to significantly increase carton penetration in untapped markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.4 Billion |

| Market Size in 2026 | USD 8.9 Billion |

| Market Size in 2034 | USD 14.8 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Aseptic gable top cartons dominated the market in 2024 with a share of approximately 34.6%. Their dominance is driven by their ability to extend shelf life without refrigeration, making them highly suitable for dairy and juice products. These cartons are widely used by large dairy brands and beverage manufacturers across Asia and Europe. The aseptic design ensures product safety, reduces spoilage, and supports long-distance distribution. For example, multinational dairy companies use aseptic cartons to distribute milk across rural and urban markets efficiently. Their reliability and scalability make them the preferred packaging format in mass distribution channels.

Bio-based coated cartons are the fastest-growing subsegment with a CAGR of 7.4%. Growth is driven by increasing environmental awareness and regulatory pressure to reduce plastic usage. These cartons use renewable coatings such as bio-polyethylene, improving recyclability. Beverage companies are adopting these cartons to strengthen sustainability branding. For example, plant-based beverage brands in Europe are shifting toward fully renewable carton structures. Future growth is expected as packaging innovation continues to focus on carbon-neutral and compostable solutions.

By Material

Paperboard-based cartons dominated the market in 2024 with a share of 55.1%. Paperboard provides structural strength, printability, and cost efficiency, making it the core material for gable top cartons. It is widely used in dairy and juice packaging across global markets. The material’s recyclability also supports sustainability initiatives. Major dairy companies rely on high-grade paperboard to maintain product quality and branding appeal. Its widespread availability ensures continued dominance in the market.

Hybrid bio-polymer coated cartons are the fastest-growing subsegment with a CAGR of 6.8%. Growth is driven by innovations in sustainable barrier coatings that replace traditional plastic layers. These materials enhance recyclability while maintaining moisture resistance. Beverage manufacturers are increasingly adopting hybrid coatings to meet regulatory requirements and sustainability goals. For example, European juice brands are integrating bio-coated cartons into premium product lines, signaling strong future adoption.

By End-Use

The dairy segment dominated the market in 2024 with a share of 46.5%. Milk remains the primary product packaged in gable top cartons due to its high consumption volume and perishability. Dairy cooperatives and large FMCG companies rely heavily on carton packaging for daily distribution. The segment benefits from strong demand in both developed and developing regions.

Plant-based beverages are the fastest-growing subsegment with a CAGR of 7.0%. Growth is driven by rising vegan and lactose-free dietary preferences. Almond milk, oat milk, and soy beverages are increasingly packaged in gable top cartons due to their eco-friendly appeal. Startups and established beverage brands are expanding their product lines, supporting future growth.

Gable Top Liquid Cartons Market Segmentations

By Type

- Aseptic Gable Top Cartons

- Non-Aseptic Gable Top Cartons

- Bio-Based Gable Top Cartons

By Material

- Paperboard

- Polyethylene Coated Materials

- Bio-Polymer Coated Materials

By End-User

- Dairy Products

- Juices

- Plant-Based Beverages

- Other Liquid Foods

Regional Analysis

North America

North America accounted for approximately 27.6% of the global market share in 2025, with a projected CAGR of 5.7% during the forecast period. The region benefits from strong beverage processing industries, advanced packaging technologies, and high consumer awareness of sustainable packaging. Demand for plant-based beverages and organic dairy products is particularly strong, supporting carton adoption. The presence of large retail chains also enhances product distribution efficiency.

The United States dominates the regional market due to its large dairy and juice industries. A key growth driver is the rapid expansion of functional beverages such as protein-enriched milk and probiotic drinks. For example, major U.S. dairy brands are increasingly launching health-focused beverages in aseptic gable top cartons to extend shelf life and improve convenience.

Europe

Europe held a market share of around 24.9% in 2025, growing at a CAGR of 6.1%. The region’s growth is driven by strict environmental regulations, strong recycling infrastructure, and consumer preference for sustainable packaging. Countries in the European Union are actively reducing plastic usage in beverage packaging.

Germany leads the European market due to its advanced packaging technology sector. A unique growth factor is the widespread adoption of fully recyclable fiber-based cartons in retail dairy packaging. For instance, German supermarkets increasingly stock milk and juice in eco-certified gable top cartons, supporting circular economy initiatives.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is projected to grow at a CAGR of 7.0%. Rapid urbanization, population growth, and expanding dairy consumption are key drivers. Rising demand for packaged beverages in China, India, and Southeast Asia significantly contributes to market expansion.

India is the dominant country due to its large dairy industry and cooperative milk distribution networks. A key growth driver is the expansion of rural cold-chain alternatives using aseptic carton packaging. For example, Indian dairy cooperatives distribute millions of liters of milk daily in gable top cartons without refrigeration.

Middle East & Africa

The region accounted for 5.8% market share in 2025, with a CAGR of 6.0%. Growth is supported by increasing imports of dairy and juice products and improving retail infrastructure. Urbanization and rising consumption of packaged beverages are also contributing factors.

Saudi Arabia leads the regional market due to its strong food import dependency. A unique driver is the growing demand for long-life milk in hot climatic conditions, where refrigeration access is limited. Gable top cartons provide a practical solution for extended shelf stability.

Latin America

Latin America held a 4.3% market share in 2025, with the fastest projected CAGR of 6.6%. Growth is driven by expanding dairy production, rising middle-class consumption, and improved retail distribution networks.

Brazil dominates the region due to its large dairy and beverage industry. A key growth factor is the expansion of supermarket chains offering private-label milk and juice in gable top cartons, increasing accessibility and affordability for consumers.

Competitive Landscape

The gable top liquid cartons market is moderately consolidated, with key players focusing on sustainability, aseptic technology, and material innovation. Major companies include Tetra Pak International S.A., SIG Combibloc Group, Elopak ASA, Nippon Paper Industries, and Stora Enso Oyj. Among these, Tetra Pak International S.A. is the leading player, known for its strong global distribution network and advanced aseptic packaging solutions.

Companies are investing in bio-based coatings, lightweight designs, and digital printing technologies to enhance product differentiation. Recent strategies include partnerships with dairy companies, expansion into emerging markets, and development of fully renewable carton structures. For example, Elopak has introduced cartons with reduced carbon footprints, aligning with sustainability goals.

Key Players List

- Tetra Pak International S.A.

- SIG Combibloc Group AG

- Elopak ASA

- Nippon Paper Industries Co., Ltd.

- Stora Enso Oyj

- Greatview Aseptic Packaging Co., Ltd.

- Adam Pack S.A.

- Billerud AB

- Mondi Group

- Uflex Ltd.

- Evergreen Packaging LLC

- Weyerhaeuser Company

- Oji Holdings Corporation

- DS Smith Plc

- Smurfit Kappa Group