Plastic Trays Market Size and Growth

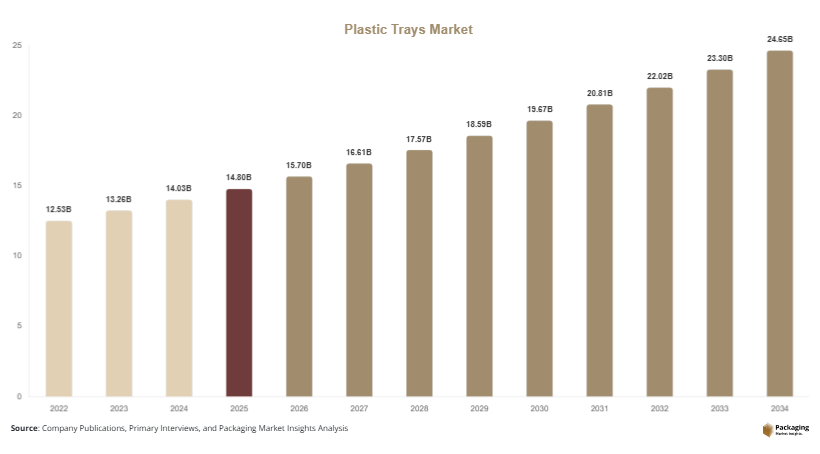

The global plastic trays market size was valued at USD 14.8 billion in 2025 and is projected to reach USD 15.7 billion in 2026. By 2034, the market is expected to attain approximately USD 24.6 billion, growing at a CAGR of 5.8% during the forecast period (2025–2034). The plastic trays market is experiencing steady expansion due to increasing demand from food packaging, healthcare, electronics, and industrial sectors. Plastic trays provide durability, lightweight handling, product protection, and cost efficiency, making them a preferred packaging solution across multiple industries. The market is also benefiting from advances in recyclable materials, thermoforming technologies, and growing adoption of modified atmosphere packaging solutions.

Several factors are contributing to market growth. First, the rapid expansion of packaged food consumption is increasing demand for rigid packaging formats that provide convenience and product safety. Second, healthcare and pharmaceutical industries are increasingly utilizing plastic trays for sterile packaging, medical devices, and diagnostic products. Third, rising e-commerce activities and organized retail channels are creating demand for protective packaging solutions capable of minimizing product damage during transportation.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.5%.

- Thermoformed trays led the type segment with a 46.8% share.

- PET-based trays dominated the material segment with a 41.9% share.

- Food & beverage applications led the market with a 52.6% share.

- The US remained the dominant country with a market size of USD 2.8 billion in 2025 and USD 3.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Recyclable and Recycled Plastic Trays

Sustainability initiatives are significantly influencing the plastic trays market. Brand owners, retailers, and packaging manufacturers are increasingly adopting recyclable and recycled materials to meet environmental objectives and regulatory requirements. Recycled PET trays are gaining popularity due to their ability to reduce virgin plastic consumption while maintaining product performance. Several food retailers are transitioning from conventional packaging to high-recycled-content trays for fresh produce, meat, and bakery applications. The future impact of this trend is expected to include greater investment in recycling infrastructure, improved collection systems, and broader adoption of circular packaging models across developed and emerging markets.

Increasing Demand for Smart and Functional Packaging Trays

The integration of smart packaging features into plastic trays is emerging as an important industry trend. Manufacturers are incorporating QR codes, RFID tags, freshness indicators, and tamper-evident technologies to improve product traceability and consumer engagement. For example, food processors are using intelligent trays with freshness-monitoring features to extend shelf life and reduce food waste. Healthcare companies are also implementing traceable packaging systems to improve inventory management and regulatory compliance. Going forward, advancements in digital packaging technologies are expected to create new opportunities for premium tray solutions while enhancing supply chain transparency and operational efficiency.

Market Drivers

Expansion of Packaged Food Consumption

The increasing demand for packaged food products remains a major growth driver for the plastic trays market. Urbanization, changing lifestyles, and rising disposable incomes are encouraging consumers to purchase ready-to-eat meals, fresh produce, frozen foods, and convenience products. Plastic trays offer superior product visibility, hygiene, and transportation protection, making them highly suitable for food packaging applications. For example, supermarkets and food delivery platforms rely heavily on plastic trays for meat, poultry, fruits, and prepared meal packaging. As food processing industries continue to expand globally, demand for innovative tray solutions is expected to increase significantly.

Rising Healthcare and Pharmaceutical Packaging Demand

Healthcare and pharmaceutical industries are increasingly utilizing plastic trays for medical devices, surgical instruments, diagnostic kits, and pharmaceutical packaging. These trays provide protection against contamination while ensuring product integrity throughout storage and transportation. Growing healthcare expenditure, expanding pharmaceutical production, and increasing demand for sterile packaging solutions are contributing to market growth. For instance, medical device manufacturers frequently use customized thermoformed trays to protect sensitive instruments. As healthcare infrastructure expands in developing countries, demand for specialized plastic tray packaging is projected to grow steadily.

Market Restraint

Environmental Regulations and Plastic Waste Concerns

Environmental concerns related to plastic waste represent a significant restraint for the plastic trays market. Governments across multiple regions are implementing regulations aimed at reducing single-use plastics and promoting sustainable packaging alternatives. These regulations can increase compliance costs for manufacturers and encourage end users to explore alternative materials such as molded fiber, paperboard, and biodegradable packaging solutions.

For example, several European countries have introduced stringent recycling targets and extended producer responsibility regulations, requiring packaging manufacturers to improve recyclability and reduce environmental impact. Small and medium-sized tray manufacturers often face challenges in upgrading production facilities to comply with these standards. In addition, consumer awareness regarding plastic pollution continues to influence purchasing decisions, particularly in developed markets. Although recycled and recyclable tray solutions are gaining traction, transitioning to sustainable production systems requires substantial investment. Consequently, environmental regulations and plastic waste concerns may limit market expansion in certain regions over the forecast period.

Market Opportunities

Growth of Recycled PET and Circular Packaging Solutions

The transition toward circular packaging systems presents a significant opportunity for market participants. Companies are increasingly investing in recycled PET technologies and closed-loop recycling systems to meet sustainability goals and regulatory requirements. Food-grade recycled materials are becoming more widely available, enabling manufacturers to produce environmentally responsible packaging without compromising quality. Future opportunities include partnerships between recyclers, retailers, and packaging producers to establish integrated recycling ecosystems. As sustainability becomes a key purchasing criterion, demand for recycled plastic trays is expected to accelerate across food, healthcare, and industrial applications.

Expansion of E-Commerce and Food Delivery Services

Rapid growth in e-commerce and online food delivery platforms is creating new opportunities for plastic tray manufacturers. Products shipped through digital channels require protective packaging capable of maintaining product integrity during transportation. Plastic trays provide structural strength, lightweight performance, and product organization benefits. For example, meal-kit providers utilize compartment trays to separate ingredients and preserve freshness. As online grocery shopping and direct-to-consumer delivery models continue expanding globally, demand for customized tray solutions with enhanced protective features is expected to rise substantially during the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.8 Billion |

| Market Size in 2026 | USD 15.7 Billion |

| Market Size in 2034 | USD 24.6 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Thermoformed trays dominated the market in 2024 with a share of 46.8%. Their leadership position is attributed to cost efficiency, design flexibility, and widespread use in food packaging applications. Thermoformed trays can be customized into various shapes and sizes, making them suitable for fresh produce, bakery items, meat products, and ready meals. Their lightweight construction reduces transportation expenses while maintaining structural integrity. Food processors and retailers continue to favor thermoformed trays due to attractive product presentation and compatibility with automated packaging systems.

Compartment trays are projected to be the fastest-growing subsegment, registering a CAGR of 6.7% during the forecast period. Rising demand for meal kits, ready-to-eat foods, and food delivery services is supporting adoption. These trays enable effective separation of ingredients while maintaining product quality. Future growth will be supported by innovations in recyclable materials, enhanced barrier properties, and increasing demand for convenient food packaging formats across global markets.

By Material

PET emerged as the dominant material segment in 2024, accounting for 41.9% of market revenue. PET trays offer transparency, durability, and strong barrier performance, making them suitable for food and healthcare packaging applications. Their compatibility with recycling systems further strengthens market adoption. Food manufacturers frequently use PET trays to showcase products while ensuring freshness and protection. Ongoing investments in PET recycling infrastructure continue to enhance the segment's competitive position.

Recycled PET (rPET) is expected to record the fastest CAGR of 7.1% through 2034. Growing sustainability requirements and consumer demand for environmentally responsible packaging are major growth drivers. Regulatory initiatives encouraging recycled content utilization are accelerating market adoption. Packaging companies are expanding production capacity for food-grade recycled PET trays. Future developments in recycling technology and circular packaging systems are expected to create additional growth opportunities.

By End-Use

Food & beverage remained the largest end-use segment in 2024, capturing 52.6% of total market share. The segment benefits from increasing consumption of packaged foods, fresh produce, meat products, and convenience meals. Plastic trays provide product visibility, protection, and efficient shelf presentation. Food processors rely on tray packaging to improve product handling and extend shelf life. The expansion of organized retail and food delivery services continues to support segment growth globally.

Healthcare is projected to be the fastest-growing end-use segment with a CAGR of 6.8% during the forecast period. Rising pharmaceutical production, medical device manufacturing, and healthcare spending are supporting demand. Plastic trays are increasingly used for sterile packaging applications and protective transport of sensitive products. Future opportunities will emerge from advancements in medical packaging technologies, increasing healthcare access, and expanding diagnostic testing activities worldwide.

Plastic Trays Market Segmentations

By Type

- Thermoformed Trays

- Compartment Trays

- Clamshell Trays

- Vacuum Formed Trays

By Material

- PET

- Polypropylene (PP)

- Polystyrene (PS)

- Recycled PET (rPET)

- Others

By End-User

- Food & Beverage

- Healthcare

- Electronics

- Consumer Goods

- Industrial

Regional Analysis

North America

North America accounted for approximately 27.8% of the plastic trays market share in 2025 and is projected to expand at a CAGR of 5.4% through 2034. The region benefits from a highly developed food processing industry, advanced healthcare infrastructure, and strong retail distribution networks. Rising demand for packaged foods, convenience meals, and fresh produce packaging continues to drive tray consumption. Investments in sustainable packaging technologies and recycled plastic materials are also supporting market growth. Manufacturers are focusing on lightweight packaging formats to reduce transportation costs while meeting environmental compliance requirements.

The United States dominates the regional market due to its large food manufacturing sector and widespread adoption of advanced packaging technologies. A unique growth driver is the rapid expansion of meal-kit delivery services and online grocery platforms. Companies increasingly require durable and compartmentalized tray packaging to ensure product quality during shipment. This trend is encouraging innovation in recyclable tray solutions and enhancing market opportunities across food and healthcare applications.

Europe

Europe represented approximately 24.6% of global market revenue in 2025 and is expected to grow at a CAGR of 5.2% over the forecast period. Demand is supported by stringent food safety standards, rising consumption of packaged foods, and increasing adoption of recyclable packaging materials. The region has established recycling infrastructure that encourages the use of sustainable plastic packaging products. Food retailers and consumer goods companies continue investing in environmentally responsible tray solutions to align with regulatory requirements and consumer expectations.

Germany remains the dominant country within Europe due to its strong manufacturing base and advanced packaging industry. A unique growth factor is the widespread implementation of circular economy initiatives that promote packaging recovery and recycling. Several retailers are replacing conventional packaging formats with high-recycled-content trays. This transition is supporting innovation in recyclable PET trays while driving investment in sustainable production technologies across the region.

Asia Pacific

Asia Pacific held the largest share of the plastic trays market at 39.2% in 2025 and is forecast to register a CAGR of 6.3% through 2034. Rapid urbanization, population growth, and expanding food processing industries are major contributors to regional demand. Increasing disposable incomes and changing consumption patterns are driving demand for packaged food products, fresh produce, and ready-to-eat meals. Significant investments in manufacturing and retail infrastructure are also strengthening market growth throughout the region.

China remains the leading country in Asia Pacific due to its extensive food processing sector and large consumer base. A unique growth driver is the expansion of modern retail chains and cold chain logistics infrastructure. Supermarkets and e-commerce platforms increasingly rely on durable tray packaging for fresh food distribution. This trend is stimulating demand for innovative thermoformed and recyclable tray solutions across multiple end-use industries.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.8% of the global market share in 2025 and is projected to grow at a CAGR of 5.6%. Increasing investments in food processing facilities, healthcare infrastructure, and retail development are supporting market expansion. Rising urban populations and changing dietary preferences are creating greater demand for packaged foods and hygienic packaging solutions. Manufacturers are also exploring lightweight tray products suitable for regional transportation and storage conditions.

Saudi Arabia dominates the regional market due to its expanding food manufacturing sector and ongoing industrial diversification efforts. A unique growth driver is the development of large-scale food security initiatives aimed at improving domestic food production and distribution. These projects are increasing demand for protective packaging formats, including plastic trays used in fresh produce and processed food applications.

Latin America

Latin America held approximately 3.6% of the plastic trays market in 2025 and is anticipated to register the fastest CAGR of 6.5% through 2034. The region is benefiting from growth in food processing, retail modernization, and healthcare investments. Demand for packaged food products continues to increase as urban populations expand and consumer lifestyles evolve. International packaging manufacturers are also increasing their regional presence to capitalize on emerging market opportunities.

Brazil remains the dominant country in Latin America due to its large food and beverage industry. A unique growth driver is the expansion of agricultural exports requiring efficient packaging and transportation solutions. Food processors increasingly utilize durable plastic trays for produce handling and distribution. This trend is expected to support sustained market growth while encouraging investment in advanced packaging technologies throughout the region.

Competitive Landscape

The plastic trays market is moderately consolidated, with leading companies focusing on sustainability, product innovation, and capacity expansion. Key participants include Amcor plc, Sonoco Products Company, Berry Global Inc., Pactiv Evergreen Inc., and Sealed Air Corporation.

Amcor plc remains a leading market participant due to its extensive global manufacturing network and focus on sustainable packaging innovations. The company continues to invest in recyclable and recycled-content tray solutions to meet evolving customer requirements.

Berry Global has expanded its portfolio of lightweight packaging products, while Sonoco continues to develop high-performance food packaging solutions. Sealed Air focuses on protective packaging technologies and smart packaging integration. Pactiv Evergreen maintains a strong presence in foodservice and consumer packaging applications.

Recent competitive strategies include acquisitions, investments in recycled material production, and development of circular economy initiatives. Manufacturers are increasingly collaborating with retailers and recycling organizations to improve packaging sustainability and strengthen long-term market positioning.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sonoco Products Company

- Sealed Air Corporation

- Pactiv Evergreen Inc.

- Genpak LLC

- Sabert Corporation

- D&W Fine Pack LLC

- Coveris Holdings S.A.

- Huhtamaki Oyj

- DS Smith plc

- Klöckner Pentaplast Group

- Faerch Group

- Anchor Packaging LLC

- Plastipak Holdings Inc.