Ovenable Paperboard Trays Market Size and Growth

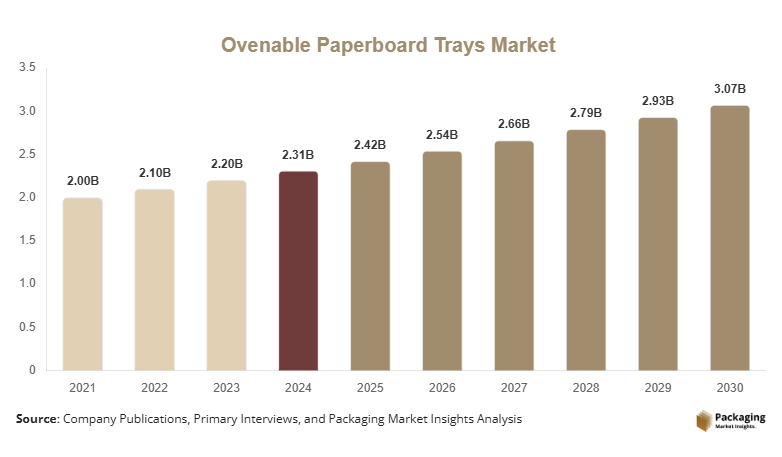

The global ovenable paperboard trays market size was valued at USD 2.31 billion in 2024 and is projected to grow from USD 2.42 billion in 2025 to reach approximately USD 3.08 billion by 2030, expanding at a CAGR of 4.9% during the forecast period (2025–2030).

The ovenable paperboard trays market growth is primarily driven by the rapid shift toward sustainable and plastic-free food packaging, rising consumption of ready-to-eat and ready-to-cook meals, and continuous advancements in heat-resistant and barrier-coated paperboard technologies

Key Market Insights

- Sustainability-led packaging adoption is accelerating, with food manufacturers increasingly replacing plastic and aluminum trays with recyclable and fiber-based ovenable paperboard alternatives.

- Ready-to-eat and frozen food packaging remains the largest application segment, supported by urban lifestyles, higher disposable incomes, and time-constrained consumers globally.

- Europe dominates the global market, driven by stringent regulations on single-use plastics and strong consumer preference for eco-friendly packaging solutions.

- Asia-Pacific is the fastest-growing region, fueled by rising frozen food consumption, rapid urbanization, and expanding food processing industries in China and India.

- Technological innovation in barrier coatings, including bio-based and water-based solutions, is improving grease resistance, moisture control, and oven performance.

- Direct B2B supply contracts with food processors and QSR chains account for the majority of sales, ensuring stable volumes and long-term revenue visibility for manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Latest Market Trends

Shift Toward Plastic-Free and Fiber-Based Food Packaging

The ovenable paperboard trays market is witnessing a strong transition away from conventional plastic and aluminum food trays toward fiber-based, recyclable solutions. Governments across Europe, North America, and parts of Asia have introduced regulations restricting single-use plastics, compelling food brands to redesign packaging formats. Ovenable paperboard trays offer a balance of sustainability, heat resistance, and branding appeal, making them an increasingly preferred choice for frozen meals, bakery products, and institutional catering. Manufacturers are also highlighting lifecycle carbon reduction benefits, which is strengthening adoption among ESG-focused food companies.

Advancements in Heat-Resistant and Barrier Coating Technologies

Continuous innovation in coating technologies is reshaping the market. Modern ovenable paperboard trays can now withstand temperatures above 220°C while maintaining structural integrity and food safety. Developments in PLA-based, silicone, and water-based dispersion coatings are enhancing grease resistance and moisture barriers without compromising recyclability. These advancements are expanding the use of paperboard trays into applications previously dominated by metal trays, such as high-fat ready meals and airline catering.

Market Drivers

Growth in Ready-to-Eat and Ready-to-Cook Foods

Global RTE food consumption has grown at over 6% annually, directly driving demand for ovenable packaging that supports reheating without food transfer. Paperboard trays offer superior branding, stackability, and sustainability credentials.

Sustainability & Carbon Footprint Reduction Goals

Food companies are committing to carbon neutrality targets. Paperboard trays, with lower lifecycle emissions compared to aluminum or plastic, are increasingly preferred for ESG compliance.

Market Restraints

Higher Cost Compared to Plastic Alternatives

Ovenable paperboard trays cost 15–25% more than plastic equivalents, impacting price-sensitive markets.

Recycling Infrastructure Limitations

In regions lacking advanced recycling systems, coated paperboard trays face disposal challenges, slowing adoption.

Market Opportunities

Regulatory Push Toward Plastic Substitution

Government bans on single-use plastics across Europe, Canada, and parts of Asia are creating sustained demand for paper-based ovenable alternatives. Food manufacturers are proactively redesigning packaging to comply with Extended Producer Responsibility (EPR) laws, presenting opportunities for tray manufacturers to secure long-term supply contracts.

Expansion of Frozen & Ready Meal Consumption in Emerging Markets

Rising disposable incomes and urban lifestyles in India, Southeast Asia, and Latin America are accelerating demand for frozen and ready-to-eat meals. Local food brands are increasingly adopting ovenable paperboard trays to improve shelf appeal and align with sustainability narratives, opening regional manufacturing and joint venture opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 2.31 Billion |

| Market Size in 2025 | USD 2.42 Billion |

| Market Size in 2030 | USD 3.08 Billion |

| CAGR | 4.9% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Composition

The Virgin Fiber Paperboard subsegment accounted for a dominant 42% share of the global ovenable paperboard trays market in 2024. This strong position is primarily attributed to its superior strength, thermal stability, and compliance with stringent food safety regulations. Virgin fiber paperboard offers better rigidity and heat resistance compared to recycled alternatives, making it the preferred choice for high-temperature applications such as ready meals and frozen food packaging. Additionally, premium food brands favor virgin fiber trays due to their superior print quality and clean sustainability perception, further reinforcing demand across developed markets.

The Coated Paperboard subsegment is projected to be the fastest-growing, registering a CAGR of 10.2% during 2025–2030. Growth in this segment is driven by rapid advancements in bio-based and water-dispersion coatings that enhance grease resistance, moisture barriers, and oven performance. These coatings enable paperboard trays to withstand temperatures exceeding 220°C, expanding their application scope into fatty foods, bakery products, and airline catering, thereby accelerating market adoption.

By Tray Structure

The Single-Compartment Trays subsegment held the largest share at 48% of the global market in 2024. This dominance is largely due to their widespread use in frozen meals, ready-to-eat foods, and institutional catering, where standardized portion sizes and simplified packaging formats are preferred. Single-compartment trays offer cost efficiency, ease of mass production, and compatibility with automated filling lines, making them the most commercially viable option for large-scale food processors.

The Multi-Compartment Trays subsegment is anticipated to grow at the fastest CAGR of 9.6% from 2025 to 2030. Rising consumer demand for portion-controlled meals, combination foods, and premium ready meals is driving the adoption of multi-compartment designs. These trays allow separation of food components during heating, improving food quality and consumer experience, particularly in premium retail and airline catering segments.

By Heat Resistance Capability

The 180°C–220°C heat resistance segment accounted for approximately 46% of the market share in 2024, making it the leading category. This temperature range aligns with standard household and commercial oven requirements, making it suitable for the majority of ready meals, frozen foods, and bakery products. The balance between performance and cost has positioned this segment as the most widely adopted heat resistance category globally.

The Above 220°C segment is expected to witness the fastest growth at a CAGR of 10.8% during the forecast period. Demand is being driven by premium food applications, including high-fat ready meals and professional foodservice operations, where higher baking temperatures are required. Technological improvements in multilayer structures and advanced coatings are enabling wider commercialization of high-temperature paperboard trays.

By Application

The Ready-to-Eat (RTE) Meals subsegment represented the largest share, accounting for nearly 34% of global market revenue in 2024. This leadership is driven by increasing urbanization, time-constrained lifestyles, and the growing popularity of convenient meal solutions across both developed and emerging economies. Ovenable paperboard trays offer RTE meal producers a sustainable alternative to plastic trays while maintaining reheating performance and shelf appeal.

The Frozen Food Packaging subsegment is projected to grow at the fastest CAGR of 9.9% from 2025 to 2030. Rising frozen food exports, expansion of cold-chain infrastructure, and increased penetration of frozen meals in Asia-Pacific and Latin America are key factors supporting this growth. Ovenable paperboard trays enable seamless transition from freezer to oven, enhancing convenience for consumers and boosting adoption.

By End-Use Industry

The Food Processing Companies subsegment dominated the market with a 51% share in 2024. This dominance is attributed to large-scale production volumes, long-term supply contracts, and the growing emphasis on sustainable packaging by multinational food manufacturers. Food processors increasingly prefer ovenable paperboard trays to meet regulatory requirements and corporate sustainability goals while maintaining operational efficiency.

The Foodservice and Quick Service Restaurants (QSRs) subsegment is expected to register the fastest growth at a CAGR of 10.1% during 2025–2030. QSR chains are rapidly transitioning toward eco-friendly packaging to align with brand sustainability commitments and evolving consumer expectations. The expansion of take-and-bake meals, ghost kitchens, and premium foodservice offerings is further accelerating demand for ovenable paperboard trays within this segment.

By Distribution Channel

The Direct Sales (B2B Contracts) subsegment accounted for the largest share of the ovenable paperboard trays market in 2024, representing approximately 58% of total revenue. This dominance is driven by long-term supply agreements between tray manufacturers and large food processing companies, QSR chains, and private-label food brands. Direct sales ensure consistent volumes, customized product specifications, and stable pricing, making them the preferred channel for high-volume buyers.

The Packaging Distributors subsegment held a moderate share of the market, primarily serving small- and mid-sized food manufacturers that require flexible order quantities and regional supply support. Distributors play a critical role in expanding market reach, particularly in emerging economies where direct manufacturer presence is limited.

The Private Label / Contract Manufacturing subsegment is expected to witness the fastest growth during the forecast period. Increasing outsourcing by retailers and food brands seeking cost optimization and faster market entry is driving demand for contract manufacturing partnerships, supporting the steady expansion of this distribution channel.

Ovenable Paperboard Trays Market Segmentations

By Material Composition

- Virgin Fiber Paperboard

- Recycled Fiber Paperboard

- Coated Paperboard (PET, PE, PLA, Silicone)

- Multi-layer Laminated Paperboard

By Tray Structure

- Single-Compartment Trays

- Dual-Compartment Trays

- Multi-Compartment Trays

By Heat Resistance Capability

- Up to 180°C

- 180°C–220°C

- Above 220°C

By Application

- Ready-to-Eat Meals

- Ready-to-Cook Meals

- Bakery & Confectionery

- Frozen Food Packaging

- Meat, Poultry & Seafood

- Institutional & Catering Meals

By End-Use Industry

- Food Processing Companies

- Foodservice & Quick Service Restaurants (QSRs)

- Retail & Private Label Brands

- Airline, Rail & Institutional Catering

By Distribution Channel

- Direct Sales (B2B Contracts)

- Packaging Distributors

- Private Label / Contract Manufacturing

Regional Analysis

North America

North America remains a key demand center for ovenable paperboard trays, led by the United States and Canada. High consumption of frozen and ready-to-eat foods, combined with strong sustainability commitments from major food brands, is driving adoption. Large food processors and private-label retailers are increasingly shifting toward paperboard trays to improve shelf differentiation and meet corporate sustainability targets. The region benefits from advanced recycling infrastructure and high consumer awareness regarding eco-friendly packaging, supporting steady market growth.

Europe

Europe holds the largest share of the global ovenable paperboard trays market, accounting for approximately 36% of total demand in 2024. Countries such as Germany, France, the U.K., Italy, and the Nordic nations are leading adoption due to strict packaging waste regulations and high acceptance of fiber-based food packaging. European consumers actively favor recyclable and compostable packaging, prompting retailers and food brands to accelerate the transition. The region also hosts several leading paperboard tray manufacturers, strengthening supply chain maturity and innovation.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market, expanding at a CAGR exceeding 10% during the forecast period. China, Japan, India, and South Korea are witnessing rising demand due to rapid urbanization, increasing penetration of frozen foods, and growth in modern retail formats. In China, large-scale food processing and export-oriented frozen food production are driving high-volume demand. India is experiencing strong growth as packaged and ready meals gain popularity among urban consumers. Expanding cold-chain infrastructure and improving recycling capabilities are further supporting market expansion across the region.

Latin America

Latin America represents a developing but promising market for ovenable paperboard trays. Brazil and Mexico are the primary contributors, driven by growth in frozen food consumption and expanding food processing industries. While cost sensitivity remains a challenge, multinational food brands operating in the region are gradually introducing sustainable packaging formats, supporting incremental demand growth. Adoption is particularly visible in bakery and meat-based ready meals.

Middle East & Africa

The Middle East & Africa region is witnessing gradual adoption, supported by growth in institutional catering, airline meals, and tourism-related food services. Countries such as the UAE, Saudi Arabia, and South Africa are leading demand due to premium foodservice segments and increasing sustainability awareness. In Africa, South Africa remains the largest market, while the Middle East benefits from strong import demand and expanding hospitality industries.

Competitive Landscape

The ovenable paperboard trays market is moderately consolidated, with the top five players collectively accounting for approximately 41% of global market share. Leading manufacturers benefit from strong relationships with multinational food processors, proprietary coating technologies, and global manufacturing footprints. While large players dominate high-volume contracts, regional manufacturers remain competitive in local and private-label segments, maintaining healthy competitive intensity across the market.

Top Key Players in Ovenable Paperboard Trays Market

- Huhtamaki Oyj

- Graphic Packaging International

- Smurfit Kappa Group

- Stora Enso

- Mondi Group

- DS Smith

- BillerudKorsnäs

- WestRock

- International Paper

- AR Packaging

- ITC Packaging

- Nippon Paper Industries