Pharmaceutical Cold Chain Packaging Market Size and Growth

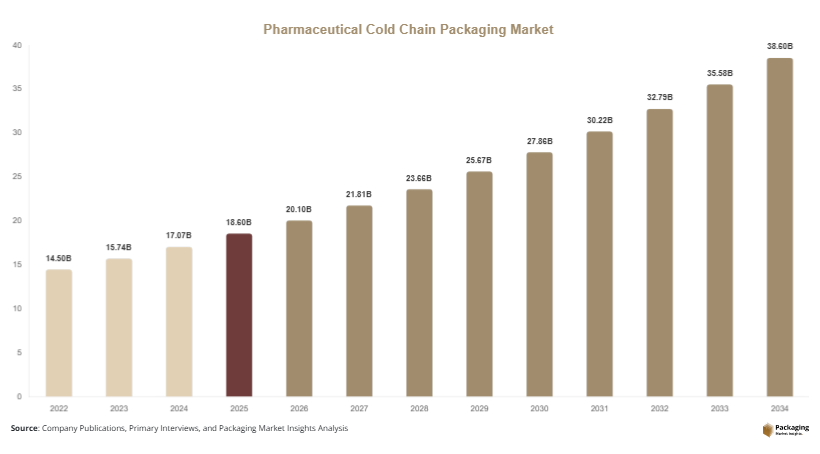

The global pharmaceutical cold chain packaging market size is estimated at USD 18.6 billion in 2025 and is projected to reach USD 20.1 billion in 2026. The market is forecast to attain approximately USD 38.9 billion by 2034, registering a CAGR of 8.5% during the forecast period (2025–2034). The growing adoption of biologic drugs, expansion of vaccine distribution programs, and increasing investments in pharmaceutical logistics infrastructure are among the primary factors supporting market growth.

One of the major growth factors is the rapid expansion of biologics and biosimilars. These products require strict temperature management throughout transportation, creating sustained demand for advanced insulated packaging systems. Another important factor is the increasing volume of global clinical trials, many of which involve temperature-sensitive materials that require specialized packaging solutions. Additionally, regulatory agencies worldwide continue to strengthen guidelines regarding pharmaceutical storage and transportation, encouraging greater adoption of validated cold chain packaging systems.

Key Market Insights

- Asia Pacific dominated the market with a 38.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 9.1%.

- Insulated shippers led the type segment with a 35.4% share.

- Plastic-based materials dominated with a 48.8% share.

- Biologics & vaccines applications led the end-use segment with 46.3% share.

- The US remained the dominant country with a market size of USD 4.6 billion in 2025 and USD 5.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of Smart Monitoring and Digital Tracking Technologies

The pharmaceutical cold chain packaging market is increasingly adopting smart monitoring technologies to improve shipment visibility and regulatory compliance. Manufacturers are integrating IoT sensors, RFID devices, GPS trackers, and cloud-based monitoring platforms into cold chain packaging systems. These technologies enable real-time temperature monitoring and provide alerts when temperature deviations occur during transportation. For example, pharmaceutical companies transporting biologics across continents are utilizing smart insulated containers that continuously transmit environmental data. This improves product safety and reduces losses caused by temperature excursions. Over the forecast period, growing digitalization of pharmaceutical logistics is expected to accelerate adoption of connected packaging solutions while improving operational efficiency and supply chain transparency.

Growing Adoption of Reusable and Sustainable Cold Chain Packaging

Sustainability has emerged as a major trend across pharmaceutical packaging supply chains. Pharmaceutical manufacturers and logistics providers are increasingly investing in reusable cold chain containers, recyclable insulation materials, and environmentally responsible packaging systems. Companies are replacing traditional single-use packaging with reusable solutions that lower waste generation and transportation costs. For instance, reusable insulated shippers are gaining popularity in vaccine distribution networks and clinical trial logistics. Future developments are expected to focus on sustainable insulation technologies and circular economy initiatives. As environmental regulations become stricter and sustainability targets gain importance, reusable pharmaceutical cold chain packaging is anticipated to witness strong growth globally.

Market Drivers

Rising Demand for Biologics, Vaccines, and Specialty Pharmaceuticals

The growing production and distribution of biologics, vaccines, and specialty pharmaceuticals is a major driver of the pharmaceutical cold chain packaging market. These products are highly temperature-sensitive and require strict thermal control throughout storage and transportation. Pharmaceutical companies are expanding biologics manufacturing capacity to meet increasing demand for treatments targeting chronic diseases, autoimmune disorders, and rare conditions. As a result, demand for advanced cold chain packaging systems continues to increase. For example, large-scale vaccine distribution programs require insulated packaging capable of maintaining specific temperature ranges for extended periods. The expansion of biologics pipelines worldwide is expected to create sustained growth opportunities for packaging manufacturers.

Expansion of Global Pharmaceutical Trade and Clinical Trials

The globalization of pharmaceutical manufacturing and distribution has significantly increased demand for cold chain packaging solutions. Pharmaceutical companies frequently transport products between manufacturing facilities, clinical trial sites, distribution centers, and healthcare providers located across multiple countries. This complex logistics environment requires reliable temperature-controlled packaging systems. For instance, multinational clinical trials often involve transportation of investigational drugs under highly regulated conditions. Increasing pharmaceutical exports from countries such as India, Germany, and Switzerland are further supporting market growth. The continued expansion of international pharmaceutical trade is expected to drive investments in advanced cold chain packaging technologies throughout the forecast period.

Market Restraint

High Cost of Advanced Cold Chain Packaging Solutions

One of the primary challenges affecting the pharmaceutical cold chain packaging market is the relatively high cost associated with advanced temperature-controlled packaging systems. Solutions incorporating vacuum insulated panels, phase change materials, reusable containers, and digital monitoring technologies often require substantial investment. While large pharmaceutical companies can absorb these costs, smaller manufacturers and healthcare providers may face budget constraints. The expense associated with validation, qualification, and regulatory compliance further increases operational costs. For example, transporting cell and gene therapies often requires specialized packaging systems that are significantly more expensive than conventional insulated solutions. These cost pressures can limit adoption in price-sensitive markets and create barriers for smaller participants. Although technological advancements are gradually improving efficiency, affordability remains an important consideration influencing purchasing decisions across the industry.

Market Opportunities

Growth of Cell and Gene Therapy Logistics

Cell and gene therapies represent one of the most promising opportunities within the pharmaceutical cold chain packaging market. These advanced therapies often require ultra-low temperature storage and transportation conditions to preserve product viability. As regulatory approvals for cell and gene therapies continue to increase, demand for highly specialized cold chain packaging solutions is expected to rise substantially. Packaging providers are developing systems capable of maintaining temperatures below -70°C while ensuring shipment integrity. Future applications are expected across oncology, rare disease treatment, and regenerative medicine, creating significant opportunities for innovative cold chain packaging manufacturers.

Expansion of Healthcare Infrastructure in Emerging Markets

Emerging economies are investing heavily in healthcare infrastructure, pharmaceutical manufacturing, and vaccine distribution networks. Countries across Asia Pacific, Latin America, and Africa are strengthening cold chain capabilities to support public health initiatives and pharmaceutical exports. This expansion creates substantial opportunities for packaging manufacturers offering cost-effective and scalable solutions. For example, increasing vaccine distribution programs in India and Brazil require reliable temperature-controlled packaging systems. Future growth is expected to be supported by government healthcare investments, rising pharmaceutical consumption, and improvements in logistics infrastructure throughout developing regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 20.1 Billion |

| Market Size in 2034 | USD 38.9 Billion |

| CAGR | 8.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Insulated shippers dominated the pharmaceutical cold chain packaging market in 2024, accounting for approximately 35.4% of total market revenue. Their leadership position is attributed to widespread use across vaccine distribution, biologics transportation, and pharmaceutical exports. Insulated shippers provide reliable thermal protection and can maintain required temperature ranges for extended transit periods. Pharmaceutical companies frequently utilize these systems to transport products through complex global supply chains. For example, insulated shippers are commonly employed for vaccine distribution campaigns and international biologics shipments. Advances in insulation materials and thermal performance have further strengthened their adoption. The combination of affordability, reliability, and compatibility with existing logistics networks continues to support the segment's dominance across global pharmaceutical supply chains.

Reusable cold chain containers are projected to be the fastest-growing type segment, expanding at a CAGR of 9.7% through 2034. Growth is driven by sustainability initiatives, cost optimization strategies, and increasing demand for long-duration temperature protection. Pharmaceutical companies are seeking reusable solutions that reduce packaging waste while improving shipment performance. Manufacturers are introducing durable insulated containers equipped with digital monitoring technologies and enhanced thermal materials. Future growth is expected to be supported by expanding biologics transportation, stricter environmental regulations, and increasing adoption of circular economy practices. As reusable systems demonstrate operational and environmental benefits, their market penetration is anticipated to increase significantly.

By Material

Plastic-based materials held the largest market share in 2024, representing approximately 48.8% of total revenue. These materials remain widely utilized due to their durability, lightweight characteristics, thermal insulation properties, and manufacturing flexibility. Expanded polystyrene, polyurethane, and other polymer-based materials are commonly used in insulated shippers and cold chain containers. Their ability to provide effective temperature control while maintaining cost efficiency has supported widespread adoption. Pharmaceutical companies continue to rely on plastic-based packaging for transporting vaccines, biologics, and specialty drugs. Additionally, ongoing material innovation is improving thermal performance and structural durability, reinforcing segment dominance.

Sustainable fiber-based materials are expected to register the fastest CAGR of 9.4% during the forecast period. Increasing environmental awareness and sustainability targets are encouraging pharmaceutical companies to adopt eco-friendly packaging alternatives. Manufacturers are developing fiber-based insulation systems capable of delivering competitive thermal performance while reducing environmental impact. Demand is particularly strong in Europe and North America, where sustainability regulations influence procurement decisions. Future innovations in biodegradable insulation materials and recyclable packaging structures are expected to strengthen segment growth. As pharmaceutical supply chains prioritize sustainability, fiber-based materials are likely to gain substantial market share.

By End-Use

Biologics and vaccines accounted for the largest market share in 2024, contributing approximately 46.3% of total revenue. These products require strict temperature control throughout transportation and storage processes, making cold chain packaging essential. Growing prevalence of chronic diseases, expanding vaccine programs, and increasing biologics approvals continue to support demand. Pharmaceutical companies are investing heavily in packaging systems capable of maintaining product stability during international shipments. Industry examples include monoclonal antibodies, recombinant proteins, and mRNA vaccines, all of which require specialized cold chain solutions. The continued growth of biologic therapies is expected to sustain segment leadership throughout the forecast period.

Cell and gene therapy applications are anticipated to be the fastest-growing end-use segment, expanding at a CAGR of 10.2% through 2034. These advanced therapies often require cryogenic or ultra-low temperature transportation conditions. Increasing commercialization of personalized medicines and regenerative therapies is driving demand for specialized packaging solutions. Manufacturers are developing innovative cryogenic containers and monitoring systems tailored to these requirements. Future growth will be supported by expanding clinical pipelines, regulatory approvals, and healthcare investments. As advanced therapies become more widely available, demand for highly specialized cold chain packaging is expected to accelerate substantially.

Pharmaceutical Cold Chain Packaging Market Segmentations

By Type

- Insulated Shippers

- Reusable Cold Chain Containers

- Refrigerants

- Thermal Blankets

- Temperature-Controlled Pallet Systems

By Material

- Plastic-Based Materials

- Fiber-Based Materials

- Vacuum Insulated Panels

- Polyurethane Foam

- Phase Change Materials

By End-User

- Biologics & Vaccines

- Cell & Gene Therapies

- Clinical Trial Materials

- Specialty Pharmaceuticals

- Blood Components

Regional Analysis

North America

North America accounted for approximately 31.4% of the global pharmaceutical cold chain packaging market share in 2025 and is expected to grow at a CAGR of 7.8% through 2034. The region benefits from a mature pharmaceutical industry, extensive biologics manufacturing capabilities, and well-established cold chain logistics networks. Demand remains strong due to increasing transportation of specialty pharmaceuticals and temperature-sensitive therapies. Pharmaceutical companies are actively investing in advanced packaging technologies that improve thermal protection and shipment monitoring. Furthermore, stringent regulatory requirements regarding drug transportation continue to encourage adoption of validated cold chain packaging solutions throughout the region.

The United States remains the dominant market within North America. A unique growth driver is the rapid expansion of cell and gene therapy commercialization. Pharmaceutical manufacturers are increasingly transporting highly sensitive therapies that require ultra-low temperature packaging systems. For example, multiple biotechnology companies are expanding production facilities to support advanced therapy distribution nationwide. This trend is driving demand for specialized insulated shippers, cryogenic packaging systems, and digital temperature monitoring solutions. Continued innovation in personalized medicine is expected to support long-term market expansion across the country.

Europe

Europe represented approximately 26.2% market share in 2025 and is forecast to expand at a CAGR of 8.0% through 2034. The region's growth is supported by strong pharmaceutical manufacturing activity, increasing biologics exports, and strict regulatory standards regarding product quality. Countries across Europe continue to invest in pharmaceutical logistics infrastructure to facilitate cross-border trade and maintain supply chain efficiency. Growing adoption of sustainable packaging practices is also influencing purchasing decisions among pharmaceutical manufacturers. The region remains a significant exporter of vaccines and specialty medicines, creating steady demand for advanced cold chain packaging solutions.

Germany dominates the European market due to its extensive pharmaceutical manufacturing base and export-oriented healthcare sector. A unique growth factor is the country's strong pharmaceutical export activity across Europe and international markets. German manufacturers increasingly rely on validated cold chain packaging systems to maintain product integrity during long-distance shipments. An emerging industry trend involves the use of reusable insulated containers to reduce transportation costs and support sustainability goals. This trend is expected to strengthen demand for advanced packaging technologies throughout the forecast period.

Asia Pacific

Asia Pacific held the largest market share of 38.1% in 2025 and is anticipated to register a CAGR of 9.0% through 2034. The region benefits from expanding pharmaceutical production, growing vaccine manufacturing capacity, and increasing healthcare expenditures. Governments across several countries are investing heavily in cold chain infrastructure to improve access to temperature-sensitive medicines. Rising pharmaceutical exports and growing demand for biologics are further supporting market growth. Additionally, increasing clinical trial activity across the region is creating new opportunities for cold chain packaging providers serving global pharmaceutical companies.

China leads the regional market due to its rapidly expanding pharmaceutical manufacturing sector and large domestic healthcare market. A unique growth driver is the country's increasing production of biologics and biosimilars for both domestic consumption and export markets. Pharmaceutical manufacturers are investing in advanced packaging systems capable of supporting long-distance international shipments. Industry trends indicate growing adoption of smart monitoring technologies integrated into cold chain packaging. These developments are expected to reinforce China's leadership position throughout the forecast period.

Middle East & Africa

The Middle East & Africa accounted for approximately 5.1% of the global market in 2025 and is projected to grow at a CAGR of 8.3%. Rising healthcare investments, vaccine distribution initiatives, and pharmaceutical imports are supporting market expansion. Governments are actively strengthening healthcare infrastructure and cold chain logistics networks to improve access to essential medicines. Increasing prevalence of chronic diseases and expanding immunization programs are also contributing to demand. The region presents significant opportunities for packaging providers capable of delivering cost-efficient and reliable cold chain solutions suited to diverse climatic conditions.

The United Arab Emirates remains the leading market in the region. A unique growth factor is its role as a pharmaceutical logistics hub connecting Asia, Europe, and Africa. The country's advanced transportation infrastructure supports efficient movement of temperature-sensitive pharmaceuticals across international markets. Industry participants are investing in temperature-controlled warehousing and distribution facilities to strengthen regional supply chains. These developments continue to create demand for high-performance cold chain packaging products throughout the region.

Latin America

Latin America held approximately 4.2% market share in 2025 and is expected to register the fastest CAGR of 9.1% during the forecast period. Market growth is supported by increasing pharmaceutical manufacturing activities, healthcare investments, and vaccine distribution programs. Governments throughout the region are prioritizing healthcare modernization and expanding access to specialty medicines. The growing presence of multinational pharmaceutical companies is also driving demand for advanced cold chain packaging systems capable of meeting international quality standards. Improvements in logistics infrastructure are further contributing to market expansion.

Brazil dominates the Latin American market. A unique growth driver is the country's expanding domestic vaccine manufacturing capacity and public immunization programs. Pharmaceutical producers require reliable temperature-controlled packaging systems to distribute products across large geographic areas. An emerging trend involves partnerships between pharmaceutical manufacturers and logistics providers to strengthen cold chain efficiency. These initiatives are expected to accelerate adoption of advanced packaging technologies throughout the forecast period.

Competitive Landscape

The pharmaceutical cold chain packaging market is characterized by strong competition among global packaging providers, temperature-controlled logistics specialists, and thermal packaging manufacturers. Companies compete through innovation, sustainability initiatives, global distribution capabilities, and thermal performance improvements.

Sonoco ThermoSafe remains a leading market participant due to its extensive cold chain packaging portfolio and strong presence across pharmaceutical logistics networks. The company recently expanded its reusable packaging solutions designed for biologics and specialty pharmaceutical transportation.

Other major companies include Cold Chain Technologies, Pelican BioThermal, Softbox Systems, and Envirotainer. These organizations continue investing in advanced insulation materials, smart monitoring technologies, and sustainable packaging platforms. Strategic partnerships with pharmaceutical manufacturers and logistics providers remain important competitive strategies. Additionally, manufacturers are expanding production capacities and regional distribution networks to meet rising demand from emerging markets. Continuous innovation in reusable and digitally connected packaging systems is expected to remain a key competitive differentiator throughout the forecast period.

Key Players List

- Sonoco ThermoSafe

- Cold Chain Technologies

- Pelican BioThermal

- Softbox Systems

- Envirotainer

- Va-Q-Tec AG

- Cryopak Industries

- Intelsius

- Sofrigam

- Tempack Packaging Solutions

- Inmark Packaging

- CSafe Global

- DHL Life Sciences & Healthcare

- Tower Cold Chain

- American Aerogel Corporation

- Emball'Iso

- SkyCell AG

- Snyder Industries