Eyewear Packaging Market Size and Growth

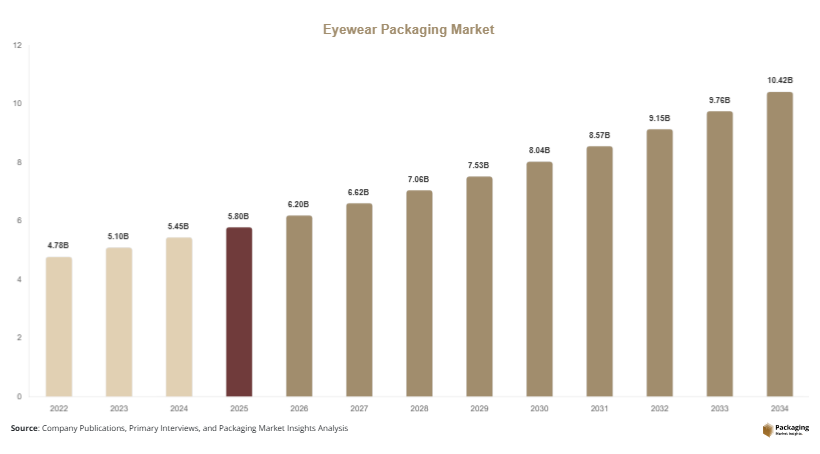

The global eyewear packaging market was valued at USD 5.8 billion in 2025 and is projected to reach USD 6.2 billion in 2026. By 2034, the market is expected to attain USD 10.4 billion, registering a CAGR of 6.7% during the forecast period from 2025 to 2034. Market growth is supported by increasing global eyewear consumption, rising demand for premium eyewear products, and expanding online eyewear retail channels.

The eyewear packaging market is experiencing steady expansion as eyewear manufacturers, luxury brands, optical retailers, and e-commerce companies increasingly invest in protective, sustainable, and aesthetically appealing packaging solutions. Eyewear packaging serves multiple functions, including product protection, brand presentation, transportation safety, and customer experience enhancement. The market encompasses hard cases, soft pouches, folding cartons, premium boxes, display packaging, and sustainable packaging formats designed for prescription eyewear, sunglasses, safety glasses, and fashion eyewear products.

Key Market Highlights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.4%.

- Hard eyewear cases led the type segment with a 41.2% share.

- Paper & paperboard packaging dominated the material segment with a 36.9% share.

- Prescription eyewear applications led the market with a 44.8% share.

- The US remained the dominant country, with a market size of USD 0.9 billion in 2025 and USD 1.0 billion in 2026

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Eyewear Packaging

Sustainability has become a central trend within the eyewear packaging market as brands respond to consumer demand for environmentally responsible products. Eyewear manufacturers are increasingly replacing plastic-based packaging components with recyclable paperboard, molded fiber, and biodegradable materials. Several global eyewear brands have introduced packaging made from recycled paper and plant-based materials to reduce environmental impact. For example, premium eyewear companies in Europe are transitioning toward plastic-free packaging formats for sunglasses and prescription eyewear. This trend is expected to gain momentum as governments strengthen packaging waste regulations and consumers prioritize sustainable purchasing decisions. Over the forecast period, environmentally friendly packaging innovations are likely to become a key competitive differentiator across the eyewear industry.

Premiumization and Enhanced Unboxing Experiences

Premium packaging design is becoming increasingly important as eyewear brands seek to strengthen customer engagement and brand perception. Luxury eyewear manufacturers are investing in rigid boxes, magnetic closures, embossed branding, and customized inserts that create memorable unboxing experiences. For example, designer eyewear brands frequently package premium sunglasses in decorative cases accompanied by branded accessories and protective pouches. This trend is extending beyond luxury categories as online retailers seek to improve customer satisfaction and encourage social media engagement. Looking ahead, premium packaging formats and personalized presentation solutions are expected to support higher-value product positioning and stronger customer loyalty.

Market Drivers

Rising Global Demand for Prescription Eyewear

The increasing prevalence of vision impairment and corrective eyewear usage is a major driver of the eyewear packaging market. Growing screen exposure, aging populations, and increasing awareness regarding eye health are contributing to higher demand for prescription glasses. As eyewear production expands, packaging demand increases proportionally. Packaging solutions are essential for protecting lenses and frames throughout distribution channels. For example, optical retailers across North America and Europe continue to expand prescription eyewear offerings, creating sustained demand for protective packaging. The direct relationship between eyewear sales growth and packaging consumption is expected to support market expansion throughout the forecast period.

Expansion of Online Eyewear Retail Channels

The rapid growth of e-commerce platforms specializing in eyewear sales is accelerating demand for durable packaging solutions. Online purchases require packaging capable of protecting fragile eyewear products during transportation and delivery. This has increased demand for rigid cases, protective inserts, and shock-resistant packaging materials. For example, direct-to-consumer eyewear brands increasingly use reinforced packaging systems to reduce product returns and damage rates. As digital retail channels continue expanding globally, demand for reliable shipping-ready packaging solutions is expected to increase significantly, supporting long-term market growth.

Market Restraint

Fluctuating Raw Material Costs and Packaging Production Expenses

One of the key restraints affecting the eyewear packaging market is the volatility of raw material prices and packaging production costs. Materials such as paperboard, plastics, fabrics, metals, and specialty coatings are subject to fluctuations caused by supply chain disruptions, inflationary pressures, and changing global trade conditions. Rising production costs can reduce profit margins for packaging manufacturers and increase overall packaging expenses for eyewear brands.

The impact is particularly significant for premium packaging applications that require decorative finishes, customized printing, and specialized materials. For example, luxury eyewear brands often utilize rigid packaging structures and premium surface treatments that increase manufacturing complexity and cost. Small and medium-sized eyewear companies may face challenges in adopting advanced packaging formats due to budget limitations. Although manufacturers are implementing efficiency improvements and material optimization strategies, cost volatility remains a notable challenge that may influence purchasing decisions and market growth rates over the forecast period.

Market Opportunities

Growth of Sustainable Luxury Packaging Solutions

The intersection of sustainability and luxury branding presents a major opportunity for market participants. Consumers increasingly expect premium products to be packaged using environmentally responsible materials without compromising aesthetics or quality. Packaging manufacturers are developing recyclable rigid boxes, molded fiber cases, and biodegradable packaging formats specifically designed for luxury eyewear brands. Applications extend across designer sunglasses, premium prescription eyewear, and limited-edition collections. Future growth opportunities are expected to emerge from innovative materials that combine environmental performance with high-end visual appeal, creating value for both manufacturers and consumers.

Smart Packaging Integration for Product Authentication

Smart packaging technologies offer significant opportunities within the eyewear industry. Brands are increasingly incorporating QR codes, NFC tags, and digital authentication features into packaging to combat counterfeit products and enhance consumer engagement. These technologies allow customers to verify product authenticity and access product information through mobile devices. For example, premium eyewear manufacturers are implementing digital verification systems within packaging to strengthen brand protection. Future applications may include interactive customer experiences, warranty registration, and personalized marketing campaigns. As digital transformation continues, smart packaging solutions are expected to become increasingly common across premium eyewear categories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.8 Billion |

| Market Size in 2026 | USD 6.2 Billion |

| Market Size in 2034 | USD 10.4 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Hard eyewear cases dominated the market in 2024, accounting for approximately 41.2% of total revenue. These products remain the preferred packaging format due to their superior protective capabilities and durability. Hard cases effectively protect lenses and frames from physical damage during transportation, storage, and consumer use. Prescription eyewear manufacturers, luxury brands, and optical retailers widely utilize hard cases as standard packaging components. The segment also benefits from increasing demand for reusable packaging formats that provide long-term product protection. Industry examples include premium optical chains and designer eyewear brands that include branded hard cases with nearly every product purchase. Their durability, perceived value, and branding opportunities continue to support segment dominance.

Premium gift packaging is anticipated to be the fastest-growing subsegment, registering a CAGR of 7.8% during the forecast period. Growth is driven by increasing consumer demand for luxury eyewear products and premium gifting experiences. Packaging manufacturers are introducing rigid presentation boxes, magnetic closures, custom inserts, and decorative finishes designed specifically for premium eyewear categories. Sustainability trends are also encouraging innovation through recyclable luxury packaging materials. Future demand is expected to increase as brands focus on enhancing customer experiences and strengthening product differentiation. The rise of premium online retail channels and luxury eyewear collections will continue supporting growth across this segment.

By Material

Paper & paperboard packaging held the largest market share of approximately 36.9% in 2024. The segment benefits from growing environmental awareness, regulatory support for sustainable packaging, and broad material availability. Paper-based packaging is commonly used for folding cartons, rigid boxes, inserts, and retail packaging applications. Eyewear brands increasingly favor paperboard solutions because they offer strong branding opportunities while supporting sustainability objectives. Industry examples include leading eyewear manufacturers replacing plastic packaging with recyclable paperboard formats. The segment's versatility, printability, and compatibility with premium packaging designs continue to support its leading market position.

Biodegradable materials represent the fastest-growing material category and are projected to expand at a CAGR of 8.1% through 2034. Growth is supported by increasing sustainability commitments from eyewear manufacturers and retail brands. Packaging companies are developing innovative biodegradable materials derived from agricultural fibers, plant-based polymers, and renewable resources. These materials offer environmentally responsible alternatives while maintaining packaging performance standards. Future opportunities are expected to emerge from luxury eyewear packaging applications and eco-conscious consumer segments. As sustainability regulations strengthen globally, biodegradable packaging adoption is expected to accelerate significantly.

By End-Use

Prescription eyewear applications accounted for the largest market share of approximately 44.8% in 2024. Rising global demand for corrective eyewear continues to drive packaging consumption across optical retail channels. Packaging solutions are essential for protecting prescription lenses and frames throughout manufacturing, distribution, and retail processes. The segment benefits from increasing rates of myopia, aging populations, and expanding access to vision care services. Industry examples include optical chains and healthcare providers that distribute millions of prescription eyewear units annually. Consistent demand and large sales volumes support the segment's dominant position within the eyewear packaging market.

Luxury eyewear packaging is expected to register the fastest CAGR of 7.9% during the forecast period. Growth is fueled by rising consumer spending on designer eyewear, premium sunglasses, and limited-edition collections. Luxury brands increasingly utilize sophisticated packaging formats to reinforce exclusivity and enhance customer experiences. Packaging innovations include premium textures, customized inserts, branded accessories, and sustainable luxury materials. Future demand is expected to benefit from premiumization trends, increasing online luxury sales, and growing consumer preference for high-end eyewear products. These factors collectively support strong growth prospects for the segment.

Eyewear Packaging Market Segmentations

By Type

- Hard Eyewear Cases

- Soft Pouches

- Folding Cartons

- Premium Gift Packaging

- Display Packaging

By Material

- Paper & Paperboard

- Plastic

- Fabric & Textile

- Metal

- Biodegradable Materials

By End-User

- Prescription Eyewear

- Sunglasses

- Safety Eyewear

- Sports Eyewear

- Luxury Eyewear

Regional Analysis

North America

North America accounted for approximately 27.8% of the global eyewear packaging market share in 2025 and is expected to grow at a CAGR of 6.2% through 2034. The region benefits from strong eyewear consumption, established retail networks, and increasing adoption of premium packaging formats. Demand is supported by rising prescription eyewear usage and growing online eyewear sales. Packaging manufacturers are investing in protective and sustainable packaging solutions to meet evolving customer expectations. Increasing consumer awareness regarding eco-friendly packaging is also influencing purchasing decisions across the region.

The United States dominates the North American market. A unique growth driver is the rapid expansion of direct-to-consumer eyewear brands. Companies increasingly rely on durable shipping-ready packaging to protect products during delivery and enhance customer satisfaction. The popularity of subscription eyewear services and online vision care platforms continues to generate additional packaging demand. These trends are expected to support sustained market growth throughout the forecast period.

Europe

Europe held approximately 24.9% of the market share in 2025 and is projected to register a CAGR of 6.4% through 2034. The region's growth is driven by strong sustainability regulations, premium eyewear consumption, and advanced packaging innovation. Packaging manufacturers are actively developing recyclable and reusable packaging materials to align with environmental objectives. Demand remains particularly strong in luxury eyewear and fashion eyewear segments. Retailers and brands continue investing in premium packaging formats that enhance product presentation and strengthen brand differentiation.

Germany remains the dominant country in Europe. A unique growth driver is the country's emphasis on sustainable manufacturing and circular economy practices. Several eyewear companies operating in Germany have introduced recyclable packaging programs and environmentally responsible packaging materials. Growing demand for premium optical products and luxury eyewear continues to create opportunities for packaging suppliers serving high-value product categories.

Asia Pacific

Asia Pacific dominated the market with a share of 38.6% in 2025 and is forecast to expand at a CAGR of 7.2% through 2034. The region benefits from large-scale eyewear manufacturing operations, rising disposable incomes, and growing consumer awareness regarding eye care. Expanding urban populations and increasing eyewear adoption rates support packaging demand across multiple countries. Additionally, the growth of e-commerce platforms and fashion-oriented eyewear consumption is contributing to market expansion. Packaging suppliers continue investing in cost-efficient and sustainable packaging solutions.

China remains the leading country within Asia Pacific. A unique growth driver is the country's extensive eyewear manufacturing ecosystem. Numerous global eyewear brands source products from Chinese manufacturing facilities, generating substantial demand for protective packaging solutions. The growth of domestic eyewear brands and online retail platforms further supports packaging consumption and innovation across the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.2% of market revenue in 2025 and is expected to grow at a CAGR of 6.5% through 2034. Rising healthcare awareness, increasing eyewear adoption, and expanding retail infrastructure are contributing to market growth. Demand for premium sunglasses and prescription eyewear is increasing among urban consumers. Packaging companies are introducing attractive and durable packaging formats to support luxury and fashion-oriented product categories. Retail modernization is also supporting greater packaging demand across the region.

The United Arab Emirates leads the regional market. A unique growth driver is the strong demand for luxury eyewear products among affluent consumers and tourists. Premium retail outlets frequently emphasize high-quality packaging to complement luxury eyewear purchases. This trend continues to create opportunities for packaging suppliers specializing in decorative and premium packaging solutions.

Latin America

Latin America represented approximately 4.5% of the global market in 2025 and is projected to grow at the fastest CAGR of 7.4% through 2034. Expanding middle-class populations, increasing eyewear awareness, and retail modernization are supporting market development. Demand for affordable prescription eyewear and fashion sunglasses continues to rise across several countries. Packaging suppliers are expanding production capabilities to serve growing regional demand while introducing sustainable packaging alternatives.

Brazil remains the dominant country in Latin America. A unique growth driver is the expansion of optical retail chains and vision care services. Increased accessibility to prescription eyewear products is creating higher packaging demand. Several domestic eyewear brands are investing in customized packaging formats to strengthen brand visibility and improve customer experiences, supporting continued market expansion.

Competitive Landscape

The eyewear packaging market is moderately fragmented, with packaging manufacturers competing through design innovation, sustainability initiatives, material development, and customization capabilities. Companies are increasingly focusing on environmentally responsible packaging solutions while maintaining premium aesthetics and product protection performance.

WestRock Company is recognized as a leading participant in the market due to its extensive packaging portfolio, strong global presence, and focus on sustainable packaging innovation. The company recently expanded its premium paperboard packaging offerings targeting luxury consumer products, including eyewear packaging applications.

Other major companies include Smurfit Westrock, DS Smith Plc, Stora Enso Oyj, and Mondi Group. These organizations continue investing in recyclable packaging materials, digital printing technologies, and customized packaging solutions. Strategic collaborations with eyewear manufacturers are becoming increasingly common as brands seek differentiated packaging formats.

Industry participants are also introducing lightweight materials, biodegradable packaging solutions, and enhanced decorative capabilities to address changing consumer preferences. As sustainability and premiumization trends continue shaping the market, competition is expected to focus increasingly on innovation, customization, and circular economy initiatives.

Key Players List

- WestRock Company

- Smurfit Westrock

- DS Smith Plc

- Stora Enso Oyj

- Mondi Group

- International Paper Company

- Graphic Packaging International LLC

- Sonoco Products Company

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

- Packlane Inc.

- GPA Global

- Taylor Box Company

- Robinson Plc

- Elite Packaging Company

- PakFactory

- Sunrise Packaging Inc.