Dairy Packaging Market Size and Growth

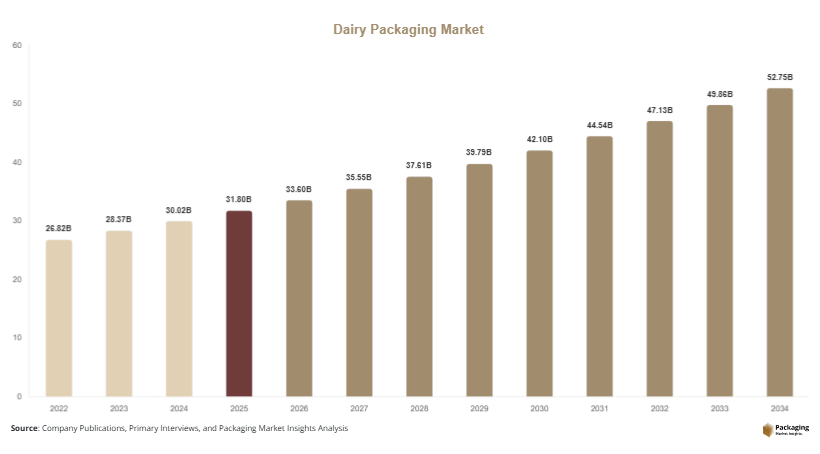

The global dairy packaging market was valued at USD 31.8 billion in 2025 and is projected to reach USD 33.6 billion in 2026. By 2034, the market is expected to reach USD 52.9 billion, expanding at a CAGR of 5.8% during the forecast period from 2025 to 2034. The market continues to benefit from increasing dairy consumption, growing demand for packaged food products, and expanding cold-chain infrastructure across developing economies.

The dairy packaging market plays a critical role in preserving product freshness, extending shelf life, ensuring food safety, and supporting efficient distribution across the dairy value chain. Packaging solutions for milk, yogurt, cheese, butter, cream, ice cream, and dairy-based beverages are evolving rapidly as manufacturers respond to changing consumer preferences, sustainability requirements, and regulatory standards. Modern dairy packaging incorporates advanced barrier technologies, lightweight materials, and recyclable formats designed to maintain product quality while reducing environmental impact.

Key Market Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.6%.

- Bottles and containers led the type segment with a 34.7% share.

- Plastic packaging dominated the material segment with a 51.8% share.

- Milk packaging applications led the market with a 42.5% share.

- The US remained the dominant country with a market size of USD 4.8 billion in 2025 and USD 5.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Dairy Packaging Solutions

Sustainability is becoming a major trend within the dairy packaging market as manufacturers seek to reduce environmental impact and comply with stricter packaging regulations. Dairy producers are increasingly replacing conventional packaging materials with recyclable paperboard, mono-material plastics, bio-based polymers, and lightweight packaging structures. Several milk and yogurt brands have introduced packaging made with recycled content to support corporate sustainability goals. For example, dairy processors across Europe are transitioning toward paper-based milk cartons with renewable material sourcing. The future impact of this trend is expected to be significant as governments implement packaging waste reduction targets and consumers increasingly favor environmentally responsible brands. Investment in sustainable packaging technologies is likely to accelerate throughout the forecast period.

Expansion of Smart and Functional Packaging Technologies

The integration of smart packaging solutions is becoming increasingly common in dairy product packaging. Technologies such as QR codes, freshness indicators, tamper-evident features, and digital traceability systems help improve food safety and consumer engagement. Dairy manufacturers are utilizing these technologies to provide product origin information, nutritional data, and supply chain transparency. For example, several premium dairy brands now use QR-enabled packaging that allows consumers to access sourcing and production information through mobile devices. Looking ahead, smart packaging is expected to enhance quality control, reduce food waste, and improve inventory management throughout the dairy supply chain.

Market Drivers

Rising Consumption of Packaged Dairy Products

The growing consumption of packaged dairy products is a major factor driving the dairy packaging market. Urbanization, changing dietary habits, and increasing disposable incomes are encouraging consumers to purchase packaged milk, yogurt, cheese, and dairy beverages. Packaging is essential for preserving freshness, ensuring food safety, and facilitating transportation. For example, demand for ready-to-drink dairy beverages and flavored milk products has increased significantly in Asia Pacific and North America, creating additional packaging requirements. As dairy product consumption continues expanding globally, demand for innovative and efficient packaging solutions is expected to rise accordingly.

Growth of Organized Retail and Cold Chain Infrastructure

The expansion of supermarkets, hypermarkets, convenience stores, and refrigerated logistics networks is supporting market growth. Modern retail channels require packaging that can withstand transportation, storage, and merchandising conditions while maintaining product quality. Dairy packaging solutions with improved barrier properties and durability are increasingly preferred by retailers and producers. For example, organized retail chains in emerging economies are expanding refrigerated product offerings, leading to greater demand for advanced dairy packaging formats. This development is expected to contribute significantly to long-term market expansion.

Market Restraint

Volatility in Raw Material Prices and Recycling Challenges

One of the primary restraints affecting the dairy packaging market is the fluctuation in raw material prices, particularly for plastics, paperboard, aluminum, and specialty barrier materials. Packaging manufacturers face challenges in maintaining profitability when material costs increase unexpectedly. These cost pressures can be passed on to dairy producers, resulting in higher overall packaging expenses.

The issue is compounded by recycling and waste management challenges associated with multi-layer packaging structures. Many dairy packaging formats require specialized barrier layers to preserve freshness and extend shelf life, making recycling more complex. For example, certain aseptic cartons contain multiple material layers that require dedicated recycling infrastructure. Smaller dairy companies may struggle to adopt sustainable alternatives due to budget constraints. While industry participants continue investing in recyclable materials and circular economy initiatives, cost volatility and recycling limitations remain key obstacles to broader market growth.

Market Opportunities

Development of Eco-Friendly Packaging Materials

The growing focus on sustainability presents substantial opportunities for eco-friendly dairy packaging solutions. Manufacturers are developing biodegradable plastics, renewable paper-based packaging, and recyclable mono-material structures designed to reduce environmental impact. These materials can be applied across milk cartons, yogurt containers, and cheese packaging formats. For example, several packaging suppliers are introducing plant-based polymers suitable for dairy applications. Future opportunities are expected to emerge from innovations that combine sustainability with enhanced product protection. As regulatory requirements become stricter and consumer preferences evolve, demand for environmentally responsible packaging is likely to increase significantly.

Expansion of Premium and Functional Dairy Products

The rising popularity of premium dairy products creates new opportunities for packaging innovation. Consumers increasingly purchase organic milk, probiotic yogurt, specialty cheese, and protein-enriched dairy beverages, which often require differentiated packaging formats. Packaging manufacturers can benefit by developing premium designs, enhanced barrier properties, and convenient dispensing features. For example, premium yogurt brands frequently utilize customized containers and decorative labeling to strengthen shelf appeal. As value-added dairy products gain market share, packaging suppliers are expected to experience increased demand for high-performance and visually appealing packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 31.8 Billion |

| Market Size in 2026 | USD 33.6 Billion |

| Market Size in 2034 | USD 52.9 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Bottles and containers dominated the market in 2024, accounting for approximately 34.7% of total revenue. Their leadership position is supported by extensive use in milk, flavored milk, cream, and dairy beverage packaging applications. These packaging formats offer excellent product protection, ease of handling, and compatibility with automated filling systems. Manufacturers favor bottles and containers because they provide branding flexibility and consumer convenience. Industry examples include high-density polyethylene milk bottles and PET-based dairy beverage containers widely used across retail channels. The segment also benefits from increasing demand for resealable packaging solutions that improve product usability and reduce waste. Continuous innovation in lightweight bottle designs further strengthens market dominance.

Pouch packaging is expected to be the fastest-growing subsegment, registering a CAGR of 6.8% during the forecast period. Growth is driven by increasing demand for flexible packaging, lower transportation costs, and reduced material consumption. Dairy manufacturers increasingly utilize pouches for yogurt, milk, and dairy beverage products due to their convenience and cost efficiency. Packaging innovations such as spouted pouches and recyclable flexible materials are supporting adoption. Future demand is expected to increase as sustainability initiatives encourage lightweight packaging solutions. Emerging markets are likely to play a major role in segment expansion due to affordability advantages.

By Material

Plastic packaging dominated the market in 2024 with a share of approximately 51.8%. Plastic materials remain widely used because of their durability, lightweight nature, affordability, and excellent barrier performance. Applications include milk bottles, yogurt cups, cheese packaging, and dairy beverage containers. Manufacturers continue utilizing plastic packaging because it supports efficient transportation and extended product shelf life. Industry examples include HDPE milk containers and polypropylene yogurt packaging formats. The segment also benefits from advances in recyclable and recycled-content plastics designed to improve sustainability performance.

Paper-based packaging is anticipated to be the fastest-growing material segment, expanding at a CAGR of 6.4% through 2034. Growth is supported by increasing environmental concerns and consumer demand for sustainable alternatives. Packaging manufacturers are introducing renewable paperboard cartons, recyclable sleeves, and fiber-based dairy packaging formats. Future opportunities are expected to emerge from innovations that improve moisture resistance and barrier properties. As sustainability targets become more ambitious, paper-based packaging adoption is likely to accelerate significantly across dairy product categories.

By End-Use

Milk packaging accounted for the largest market share of approximately 42.5% in 2024. Milk remains the most widely consumed dairy product globally, generating substantial packaging demand across retail, institutional, and foodservice channels. Packaging solutions for milk require strong barrier properties, durability, and compatibility with refrigerated distribution systems. Industry examples include aseptic cartons, HDPE bottles, and flexible pouches used by major dairy producers. Consistent consumer demand and high production volumes continue to support segment dominance.

Yogurt packaging is projected to be the fastest-growing end-use segment, registering a CAGR of 6.7% through 2034. Growth is driven by increasing consumption of probiotic, functional, and premium yogurt products. Packaging manufacturers are developing innovative containers, resealable lids, and sustainable packaging formats tailored to yogurt applications. Future demand is expected to benefit from health-conscious consumer trends and product diversification. Premium packaging aesthetics and convenience features are likely to become increasingly important within this segment.

Dairy Packaging Market Segmentations

By Type

- Bottles & Containers

- Cartons

- Cups & Tubs

- Pouches

- Bags & Wraps

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Biodegradable Materials

By End-User

- Milk

- Yogurt

- Cheese

- Butter & Cream

- Dairy-Based Beverages

Regional Analysis

North America

North America accounted for approximately 26.4% of the global dairy packaging market share in 2025 and is expected to grow at a CAGR of 5.3% through 2034. The region benefits from high dairy consumption, advanced cold chain infrastructure, and strong demand for packaged food products. Dairy processors continue investing in innovative packaging technologies to improve shelf life and sustainability performance. The growing popularity of single-serve dairy products and functional beverages is creating demand for convenient packaging formats. Increasing adoption of recyclable materials further supports market development.

The United States dominates the regional market. A unique growth driver is the rapid growth of protein-rich dairy beverages and value-added milk products. These products require specialized packaging formats capable of maintaining freshness and supporting brand differentiation. For example, several leading dairy brands have introduced resealable packaging solutions for ready-to-drink protein beverages. This trend is expected to sustain packaging demand throughout the forecast period.

Europe

Europe held approximately 24.7% of the market share in 2025 and is projected to register a CAGR of 5.4% through 2034. The region benefits from stringent food safety regulations, advanced packaging technologies, and strong sustainability initiatives. Dairy producers are increasingly adopting recyclable and renewable packaging materials to meet environmental targets. Demand remains strong across milk, cheese, and yogurt categories. Investments in circular economy programs are encouraging packaging innovation and material recovery improvements throughout the region.

Germany remains the dominant country in Europe. A unique growth driver is the expansion of organic dairy product consumption. Organic milk and dairy brands often prioritize environmentally responsible packaging, creating demand for recyclable and paper-based formats. Several dairy cooperatives have adopted sustainable packaging programs to strengthen consumer trust and align with environmental goals.

Asia Pacific

Asia Pacific dominated the market with a share of 39.2% in 2025 and is expected to expand at a CAGR of 6.3% through 2034. Rapid urbanization, population growth, and increasing dairy consumption are key contributors to regional market expansion. Rising disposable incomes and expanding retail networks support demand for packaged dairy products. Packaging manufacturers continue investing in cost-effective and high-performance packaging solutions tailored to regional consumption patterns. Growth in dairy imports and domestic processing capacity further strengthens market opportunities.

China remains the leading country within Asia Pacific. A unique growth driver is the increasing demand for premium dairy nutrition products among middle-income consumers. Dairy companies are introducing advanced packaging solutions that emphasize product safety, traceability, and freshness. This trend has accelerated investment in aseptic packaging technologies and smart packaging features across the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.8% of market revenue in 2025 and is forecast to grow at a CAGR of 5.9% through 2034. Rising urban populations, expanding food retail networks, and increasing dairy imports support market growth. Demand for long-shelf-life dairy products is particularly strong due to climatic conditions and distribution challenges. Packaging solutions capable of preserving product quality are therefore gaining importance across the region.

Saudi Arabia remains the dominant country in the region. A unique growth driver is the expansion of domestic dairy production and processing capacity. Several major dairy companies are investing in modern packaging technologies to improve efficiency and product quality. The growing popularity of flavored milk and yogurt products is also supporting packaging demand.

Latin America

Latin America represented approximately 4.9% of the market in 2025 and is expected to register the fastest CAGR of 6.6% during the forecast period. Growing dairy consumption, retail modernization, and expanding food processing industries are supporting market development. Packaging suppliers are increasing investments in sustainable and cost-efficient solutions to address changing consumer preferences. Demand for packaged milk and yogurt products continues to rise throughout the region.

Brazil remains the dominant country in Latin America. A unique growth driver is the expansion of regional dairy exports. Export-oriented dairy producers increasingly require advanced packaging solutions capable of maintaining product quality during long-distance transportation. Several dairy companies are adopting improved barrier packaging formats to support international trade and enhance product shelf life.

Competitive Landscape

The dairy packaging market is characterized by strong competition among global packaging manufacturers focused on innovation, sustainability, and operational efficiency. Companies are investing in recyclable materials, lightweight packaging designs, and advanced barrier technologies to strengthen market positions.

Amcor plc remains a leading player in the market due to its extensive packaging portfolio, global manufacturing footprint, and focus on sustainable packaging innovation. The company recently expanded its recyclable dairy packaging solutions to support circular economy objectives and meet customer sustainability goals.

Other major participants include Tetra Pak International S.A., Berry Global Group, Inc., Sealed Air Corporation, and Mondi Group. These companies continue investing in material innovation, production capacity expansion, and strategic partnerships with dairy producers. Technological advancements such as smart packaging and aseptic packaging systems remain important competitive differentiators.

Market participants are increasingly focusing on reducing packaging weight, improving recyclability, and enhancing product protection. As environmental regulations become stricter and dairy consumption grows, competition is expected to intensify across both developed and emerging markets.

Key Players List

- Amcor plc

- Tetra Pak International S.A.

- Berry Global Group, Inc.

- Sealed Air Corporation

- Mondi Group

- Sonoco Products Company

- Huhtamaki Oyj

- SIG Group AG

- WestRock Company

- DS Smith Plc

- Smurfit Westrock

- Graphic Packaging International LLC

- International Paper Company

- Coveris Holdings S.A.

- Elopak AS

- Stora Enso Oyj

- Evergreen Packaging LLC