Blister Packs Pharmaceutical Packaging Market Size and Growth

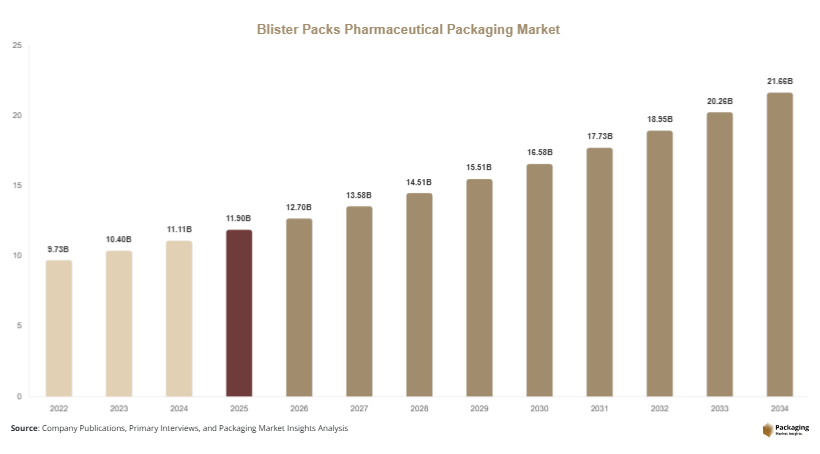

The global blister packs pharmaceutical packaging market size is estimated at USD 11.9 billion in 2025 and is projected to reach USD 12.7 billion in 2026. By 2034, the market is expected to reach approximately USD 21.8 billion, expanding at a CAGR of 6.9% during the forecast period (2025–2034). The market is benefiting from increasing demand for over-the-counter (OTC) medications, rising prevalence of chronic diseases, and growing pharmaceutical exports across developed and emerging economies.

The blister packs pharmaceutical packaging market is experiencing steady growth due to the increasing demand for unit-dose drug packaging, rising pharmaceutical production, and stricter regulatory requirements related to drug safety and traceability. Blister packaging is widely used for tablets, capsules, lozenges, and other solid-dose medications because it provides excellent barrier protection against moisture, oxygen, contamination, and physical damage. Pharmaceutical manufacturers continue to adopt blister packs as they improve patient compliance, facilitate dosage tracking, and enhance product security throughout the supply chain.

Key Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.4%.

- Thermoformed blister packs led the type segment with a 62.8% share.

- PVC-based materials dominated the material segment with a 46.9% share.

- Prescription drugs led the end-use segment with a 58.4% share.

- The US remained the dominant country with a market size of USD 2.4 billion in 2025 and USD 2.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Blister Packaging Solutions

Sustainability has become a major focus area within the blister packs pharmaceutical packaging market. Pharmaceutical manufacturers are increasingly seeking packaging materials that reduce environmental impact without compromising product protection. Traditional multi-material blister packs often present recycling challenges, encouraging packaging suppliers to develop mono-material and recyclable alternatives. For example, several pharmaceutical companies have introduced recyclable blister formats using advanced polymer structures and reduced aluminum content. Regulatory pressure and corporate sustainability commitments are accelerating this transition. Over the coming years, packaging manufacturers are expected to invest further in eco-friendly material innovations, creating blister pack solutions that support circular economy initiatives while maintaining pharmaceutical-grade barrier performance.

Integration of Smart Packaging and Serialization Technologies

The pharmaceutical industry is increasingly adopting smart packaging features within blister pack systems to improve drug traceability, patient engagement, and supply chain security. QR codes, NFC tags, digital authentication labels, and serialization technologies are becoming more common in pharmaceutical packaging applications. For instance, pharmaceutical companies are incorporating unique identification codes into blister packs to comply with anti-counterfeiting regulations and improve product tracking. Smart packaging also enables patients to access dosage information and medication reminders through mobile applications. As digital healthcare adoption expands globally, integration of connected packaging technologies is expected to become a key trend supporting market growth and enhancing pharmaceutical supply chain transparency.

Market Drivers

Rising Demand for Unit-Dose Packaging and Patient Compliance

The increasing focus on patient safety and medication adherence is a major driver of the blister packs pharmaceutical packaging market. Blister packs allow medications to be organized into individual doses, reducing the likelihood of dosing errors and improving treatment compliance. Healthcare providers increasingly recommend unit-dose packaging for chronic disease treatments, where adherence plays a critical role in therapeutic outcomes. For example, medications used in cardiovascular and diabetes management are frequently packaged in blister formats to help patients track daily dosages. This growing emphasis on patient-centric packaging continues to drive demand for advanced blister packaging solutions across global pharmaceutical markets.

Expansion of Generic Pharmaceutical Manufacturing

The rapid growth of generic drug production is significantly contributing to market expansion. Generic drug manufacturers require cost-efficient, scalable, and regulatory-compliant packaging solutions capable of supporting high-volume production. Blister packaging provides excellent protection while enabling efficient automated filling processes. For example, pharmaceutical companies in India, the United States, and Europe utilize blister packs extensively for generic tablet and capsule packaging. As governments encourage the use of affordable generic medicines to reduce healthcare costs, pharmaceutical production volumes continue to rise. This trend directly increases demand for blister packaging materials, equipment, and value-added packaging technologies.

Market Restraint

Complexity of Recycling Multi-Material Blister Packaging

One of the primary restraints affecting the blister packs pharmaceutical packaging market is the difficulty associated with recycling traditional multi-material blister packs. Many blister packages combine plastic films and aluminum foil layers to achieve the required barrier properties for pharmaceutical products. While these materials offer excellent protection, they can be challenging to separate and recycle through conventional waste management systems. As environmental regulations become stricter, pharmaceutical companies face increasing pressure to reduce packaging waste and improve recyclability. For example, several European markets have introduced packaging sustainability targets that require manufacturers to evaluate alternative materials. Although innovative recyclable blister structures are emerging, transitioning existing packaging systems involves substantial investment and operational adjustments. This challenge may slow adoption among cost-sensitive pharmaceutical manufacturers.

Market Opportunities

Expansion of Specialty Pharmaceuticals and Biologics

The growing market for specialty pharmaceuticals and biologic therapies presents significant opportunities for blister packaging manufacturers. Specialty drugs often require enhanced protection against environmental factors, creating demand for advanced barrier packaging solutions. Cold-formed blister packs and high-performance material structures are increasingly used for sensitive pharmaceutical products. For example, oncology treatments and specialty therapies frequently utilize advanced blister packaging formats to maintain product stability. As pharmaceutical research continues to generate innovative therapies, packaging suppliers have opportunities to develop customized solutions tailored to emerging drug formulations. This trend is expected to support long-term market growth.

Increasing Pharmaceutical Production in Emerging Markets

Emerging economies across Asia Pacific, Latin America, and parts of Africa are becoming important pharmaceutical manufacturing hubs. Governments are investing in domestic drug production capabilities to improve healthcare access and reduce import dependence. This expansion creates substantial opportunities for blister packaging suppliers. For example, pharmaceutical manufacturing facilities in India, Brazil, and Southeast Asia are increasing demand for high-volume packaging systems capable of supporting generic and OTC medication production. Future opportunities will likely emerge from local pharmaceutical investments, export-oriented manufacturing strategies, and growing healthcare consumption across developing economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.9 Billion |

| Market Size in 2026 | USD 12.7 Billion |

| Market Size in 2034 | USD 21.8 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Thermoformed blister packs dominated the market in 2024, accounting for approximately 62.8% of total revenue share. These packaging formats are widely used due to their cost efficiency, manufacturing flexibility, and suitability for high-volume pharmaceutical production. Thermoforming processes enable manufacturers to produce customized cavity designs that accommodate a wide range of tablet and capsule sizes. Pharmaceutical companies favor thermoformed blister packs because they provide adequate protection while maintaining competitive production costs. For example, OTC medications and generic pharmaceutical products frequently utilize thermoformed blister packaging due to its scalability and compatibility with automated production systems. The segment continues to benefit from strong demand across global pharmaceutical markets.

Cold-formed blister packs are projected to be the fastest-growing type segment, expanding at a CAGR of 7.6% through 2034. Growth is driven by increasing demand for enhanced barrier protection for moisture-sensitive and oxygen-sensitive drugs. These blister packs provide superior protection compared to traditional thermoformed alternatives, making them suitable for specialty medicines and biologics. Pharmaceutical manufacturers are increasingly utilizing cold-form technology for high-value drug formulations. Future demand is expected to increase as pharmaceutical companies continue developing advanced therapies that require improved packaging performance.

By Material

PVC-based materials dominated the market in 2024 with approximately 46.9% market share. PVC remains one of the most widely used blister packaging materials due to its clarity, processability, and cost-effectiveness. Pharmaceutical manufacturers utilize PVC-based structures for a broad range of prescription and OTC products. The material supports efficient thermoforming operations while providing acceptable barrier performance for many pharmaceutical applications. For example, commonly prescribed tablets and capsules are frequently packaged using PVC blister formats. Established manufacturing infrastructure and widespread regulatory acceptance continue to support the segment's leadership position.

Recyclable polymer materials are expected to register the fastest CAGR of 8.1% during the forecast period. Growing sustainability initiatives and increasing regulatory attention toward packaging waste are driving adoption of recyclable alternatives. Packaging manufacturers are developing innovative material structures that maintain pharmaceutical protection requirements while improving environmental performance. Pharmaceutical companies are increasingly evaluating recyclable blister solutions as part of broader sustainability strategies. Future growth is expected to be supported by material innovation and stronger demand for environmentally responsible packaging.

By End-Use

Prescription drugs dominated the end-use segment in 2024, accounting for approximately 58.4% of total market share. The segment's leadership is driven by growing prescription medication consumption, increasing prevalence of chronic diseases, and expanding pharmaceutical production. Blister packaging offers significant advantages for prescription drugs, including dosage control, product protection, and patient adherence support. Healthcare providers and pharmaceutical companies increasingly rely on blister packaging to improve treatment outcomes and reduce medication errors. Continued growth in prescription drug demand is expected to support the segment's dominant position.

Biologics and specialty medicines are projected to be the fastest-growing end-use segment, registering a CAGR of 7.8% through 2034. Growth is supported by rising investments in advanced therapeutics, personalized medicine, and specialty drug development. These products often require enhanced barrier protection and specialized packaging solutions to maintain stability and efficacy. Packaging manufacturers are introducing advanced blister technologies specifically designed for sensitive pharmaceutical formulations. Continued innovation within biologics and specialty medicine markets is expected to create significant opportunities for blister packaging suppliers.

Blister Packs Pharmaceutical Packaging Market Segmentations

By Type

- Thermoformed Blister Packs

- Cold-Formed Blister Packs

- Carded Blister Packs

- Child-Resistant Blister Packs

By Material

- PVC

- PVDC

- Aluminum Foil

- Recyclable Polymer Materials

By End-User

- Prescription Drugs

- Over-the-Counter (OTC) Drugs

- Biologics & Specialty Medicines

- Clinical Trial Packaging

Regional Analysis

North America

North America accounted for approximately 29.7% of the global blister packs pharmaceutical packaging market share in 2025 and is expected to grow at a CAGR of 6.5% through 2034. The region benefits from advanced pharmaceutical manufacturing capabilities, strong healthcare infrastructure, and stringent regulatory requirements related to drug packaging and safety. Demand for blister packaging continues to increase as pharmaceutical companies focus on patient compliance and anti-counterfeiting measures. Growth is also supported by increasing consumption of prescription medications and expanding specialty pharmaceutical markets. The presence of major pharmaceutical manufacturers and packaging suppliers contributes to continuous innovation within the regional market.

The United States dominates the North American market. A unique growth driver is the widespread adoption of medication adherence programs supported by healthcare providers and insurance organizations. Pharmaceutical companies increasingly utilize calendarized blister packs and patient-friendly packaging formats to improve treatment outcomes. For example, chronic disease management programs often rely on unit-dose blister packaging to encourage consistent medication usage. This focus on patient adherence continues to strengthen demand for advanced blister packaging solutions across the country.

Europe

Europe represented approximately 25.8% of global market share in 2025 and is projected to register a CAGR of 6.7% during the forecast period. The region benefits from strong pharmaceutical production, strict drug packaging regulations, and increasing emphasis on sustainable packaging solutions. Pharmaceutical manufacturers are investing in advanced blister packaging technologies to meet evolving regulatory requirements and environmental goals. Demand remains strong across prescription medicines, OTC products, and specialty pharmaceutical applications. Growing adoption of recyclable blister materials is also contributing to market development.

Germany remains the leading country within Europe. A unique growth factor is the country's focus on pharmaceutical serialization and packaging automation. German pharmaceutical companies continue to invest in advanced blister packaging lines capable of integrating digital traceability features. For example, automated packaging facilities are increasingly utilizing smart inspection technologies to ensure product quality and regulatory compliance. These investments continue to support Germany's leadership within the European market.

Asia Pacific

Asia Pacific dominated the market with a 38.1% share in 2025 and is forecast to expand at a CAGR of 7.5% through 2034. Rapid growth in pharmaceutical manufacturing, increasing healthcare expenditure, and rising demand for affordable medicines are supporting market expansion. Countries such as China, India, Japan, and South Korea are investing heavily in pharmaceutical production capacity and packaging modernization. Growing exports of generic medicines further contribute to demand for blister packaging solutions. Additionally, increasing urbanization and healthcare access continue to stimulate pharmaceutical consumption throughout the region.

China is the dominant country within Asia Pacific. A unique growth driver is the country's expansion of domestic pharmaceutical supply chains. Chinese pharmaceutical manufacturers are investing in automated blister packaging systems to improve production efficiency and product quality. For example, large-scale generic drug production facilities increasingly utilize high-speed blister packaging lines to meet both domestic and export demand. This manufacturing expansion continues to drive significant growth in blister packaging consumption.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.4% of global market share in 2025 and is expected to grow at a CAGR of 6.4% through 2034. Increasing healthcare investments, expanding pharmaceutical imports, and growing access to medical treatments are supporting market development. Governments across the region are implementing healthcare modernization programs that encourage pharmaceutical manufacturing and distribution improvements. Demand for blister packaging is rising as healthcare providers seek packaging formats that enhance medication safety and storage stability.

Saudi Arabia remains the dominant country within the region. A unique growth factor is the government's pharmaceutical localization strategy aimed at increasing domestic drug manufacturing. Local pharmaceutical producers are expanding production facilities and adopting advanced packaging technologies to support national healthcare goals. For example, new pharmaceutical industrial zones are creating demand for blister packaging materials and equipment. These initiatives continue to strengthen regional market opportunities.

Latin America

Latin America held approximately 3.0% of global market share in 2025 and is projected to grow at the fastest CAGR of 7.4% during the forecast period. Increasing pharmaceutical production, rising healthcare awareness, and expanding access to prescription medications are supporting regional market growth. Pharmaceutical companies are investing in local manufacturing facilities to improve supply chain resilience and reduce import dependency. Demand for blister packaging is also increasing due to growth in OTC medication sales and generic drug adoption.

Brazil dominates the Latin American market. A unique growth driver is the country's expanding public healthcare initiatives focused on improving medication accessibility. Pharmaceutical manufacturers are increasing production volumes of essential medicines, creating higher demand for efficient packaging solutions. For example, large-scale distribution programs for chronic disease treatments frequently utilize blister packaging due to its convenience and product protection benefits. These developments continue to support market expansion throughout the country.

Competitive Landscape

The blister packs pharmaceutical packaging market is moderately consolidated, with leading companies focusing on material innovation, sustainable packaging development, and pharmaceutical compliance solutions. Amcor plc remains a leading market participant due to its extensive pharmaceutical packaging portfolio, global manufacturing presence, and continuous investment in recyclable blister packaging technologies.

Other major companies include Constantia Flexibles, Sonoco Products Company, Bilcare Limited, and Klöckner Pentaplast Group. These firms continue to invest in advanced barrier materials, smart packaging technologies, and high-performance blister structures designed for pharmaceutical applications. Strategic collaborations with pharmaceutical manufacturers remain a common growth strategy.

Recent developments include the introduction of recyclable blister packaging solutions, expansion of pharmaceutical packaging facilities, and investments in digital serialization technologies. Market participants are also focusing on improving sustainability performance while maintaining regulatory compliance and product protection standards.

Key Players List

- Amcor plc

- Constantia Flexibles

- Sonoco Products Company

- Bilcare Limited

- Klöckner Pentaplast Group

- Honeywell International Inc.

- WestRock Company

- Tekni-Plex Inc.

- AptarGroup, Inc.

- Huhtamaki Oyj

- Winpak Ltd.

- UFlex Limited

- Liveo Research AG

- Formpaks International Co. Ltd.

- ACG Worldwide