Aluminum Beverage Bottles Market Size and Growth

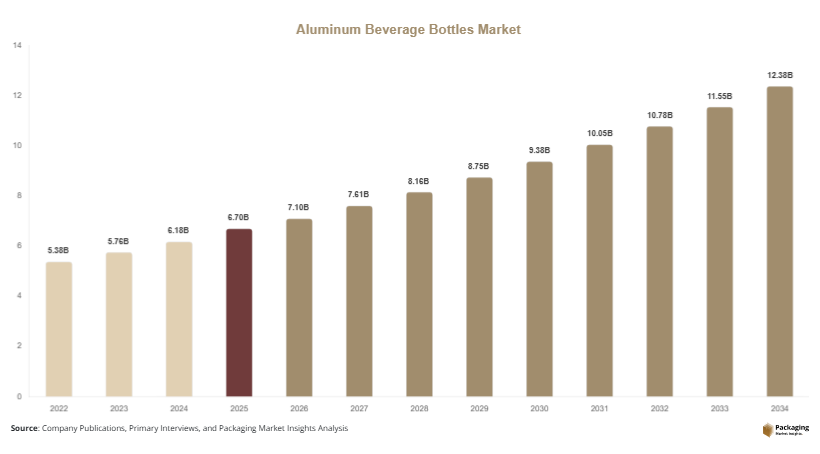

The global aluminum beverage bottles market size is estimated at USD 6.7 billion in 2025 and is projected to reach USD 7.1 billion in 2026. By 2034, the market is forecast to attain approximately USD 12.4 billion, registering a CAGR of 7.2% during the forecast period (2025–2034). Rising consumer preference for eco-friendly packaging, increasing demand for premium beverage products, and growing investments in sustainable packaging technologies are among the primary factors driving market growth.

The aluminum beverage bottles market is gaining significant momentum as beverage manufacturers increasingly adopt sustainable and recyclable packaging solutions. Aluminum bottles are becoming a preferred packaging format for carbonated drinks, energy beverages, bottled water, beer, ready-to-drink (RTD) products, and premium functional beverages due to their durability, lightweight properties, and high recycling efficiency. The growing emphasis on reducing plastic waste, combined with government regulations encouraging circular economy practices, continues to support market expansion worldwide.

Key Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.8%.

- Standard aluminum bottles led the type segment with a 48.6% share.

- Recycled aluminum dominated the material segment with a 56.4% share.

- Alcoholic beverages led the end-use segment with a 42.7% share.

- The US remained the dominant country with a market size of USD 1.5 billion in 2025 and USD 1.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Circular Packaging Models

Sustainability has become a defining trend in the aluminum beverage bottles market. Beverage brands are increasingly adopting circular packaging strategies that emphasize recyclability and material recovery. Aluminum bottles are particularly attractive because they can be recycled repeatedly without significant quality degradation. Major beverage manufacturers are integrating high percentages of post-consumer recycled aluminum into packaging production. For example, several bottled water and sports drink brands have introduced aluminum packaging to reduce plastic dependency and improve sustainability credentials. This trend is expected to accelerate as governments implement stricter packaging waste regulations and retailers prioritize environmentally responsible products. Future developments will likely include higher recycled content standards and broader deployment of closed-loop recycling systems.

Premiumization of Beverage Packaging

Premium beverage categories are increasingly utilizing aluminum bottles to enhance brand positioning and consumer engagement. The metallic finish, durability, and premium appearance of aluminum bottles support higher-value product offerings in categories such as craft beer, specialty coffee drinks, flavored water, and energy beverages. For example, several international beverage brands have launched limited-edition products in customized aluminum bottles to attract younger consumers and increase shelf visibility. As consumer demand for differentiated packaging grows, manufacturers are investing in advanced printing technologies and customized bottle designs. This trend is expected to expand into emerging beverage categories, supporting long-term demand for aluminum packaging solutions.

Market Drivers

Growing Demand for Sustainable Beverage Packaging

Environmental concerns are significantly influencing packaging decisions across the beverage industry. Consumers are increasingly choosing products packaged in recyclable materials, encouraging manufacturers to replace plastic bottles with aluminum alternatives. Aluminum offers a high recycling rate and lower long-term environmental impact when integrated into circular supply chains. As a result, beverage producers are expanding aluminum bottle portfolios across multiple product categories. For example, global water brands have introduced aluminum-packaged products to appeal to environmentally conscious consumers. This shift directly contributes to increased market demand and encourages investments in aluminum bottle manufacturing capacity.

Expansion of Premium and Functional Beverage Markets

The rapid growth of premium beverage segments is creating strong demand for innovative packaging formats. Functional beverages, energy drinks, sports drinks, and premium alcoholic beverages increasingly utilize aluminum bottles because they provide product differentiation and enhanced consumer appeal. Beverage companies often associate aluminum packaging with quality, convenience, and sustainability. For instance, premium craft beer producers frequently use aluminum bottles for special releases and limited-edition products. The expansion of these beverage categories is creating sustained demand for aluminum packaging and encouraging manufacturers to develop specialized bottle designs for diverse applications.

Market Restraint

High Production Costs Compared with Conventional Packaging

A significant challenge facing the aluminum beverage bottles market is the relatively high manufacturing cost compared with plastic packaging alternatives. Aluminum production requires substantial energy inputs and specialized processing technologies. Although recycling helps reduce environmental impact, fluctuations in aluminum prices can affect overall packaging costs. Small and medium-sized beverage companies may find aluminum bottles less economically viable than PET bottles, particularly in highly price-sensitive markets. For example, regional beverage producers in developing economies often prioritize low-cost packaging solutions to remain competitive. These cost considerations may slow adoption in certain market segments despite growing sustainability benefits. Additionally, investments required for aluminum bottling lines and filling equipment can create barriers for new entrants.

Market Opportunities

Growth of Aluminum-Packaged Water Products

The bottled water industry presents substantial opportunities for aluminum beverage bottle manufacturers. Growing consumer awareness regarding plastic pollution is encouraging water brands to adopt recyclable packaging formats. Aluminum bottles offer durability, portability, and strong sustainability credentials that appeal to environmentally conscious consumers. Several hospitality companies, airports, and sports venues have begun replacing plastic water bottles with aluminum alternatives. As governments continue restricting single-use plastics, demand for aluminum-packaged water products is expected to increase significantly. Future opportunities include premium mineral water, flavored water, and reusable aluminum bottle programs.

Expansion in Emerging Economies

Emerging markets represent an important growth avenue for the aluminum beverage bottles market. Rising disposable incomes, urbanization, and expanding retail infrastructure are increasing beverage consumption across Asia Pacific, Latin America, and parts of Africa. Consumers in these regions are showing growing interest in premium packaged beverages and sustainable products. Beverage companies are responding by introducing aluminum bottle packaging to strengthen brand positioning and meet environmental objectives. Future investments in recycling infrastructure and local aluminum production capacity are expected to further support market growth and create opportunities for packaging suppliers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.7 Billion |

| Market Size in 2026 | USD 7.1 Billion |

| Market Size in 2034 | USD 12.4 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Standard aluminum bottles dominated the market in 2024, accounting for approximately 48.6% of total revenue share. Their widespread adoption stems from their versatility across multiple beverage categories, including water, carbonated drinks, sports beverages, and alcoholic beverages. Manufacturers favor standard aluminum bottles because they are compatible with existing filling and distribution systems while offering strong durability and recyclability. Many global beverage companies utilize standard aluminum bottles to achieve sustainability objectives without significantly altering production processes. The segment also benefits from broad consumer acceptance and cost advantages compared with highly customized packaging formats. Increasing investments in lightweight bottle designs further reinforce the dominance of this segment.

Resealable aluminum bottles are projected to be the fastest-growing type segment, expanding at a CAGR of 8.1% through 2034. Growth is driven by consumer demand for convenience and portability. These bottles are particularly popular among energy drink, sports drink, and premium water brands targeting active lifestyles. Packaging innovations such as improved closure systems and lightweight designs are enhancing product functionality. Beverage manufacturers increasingly view resealable aluminum bottles as a premium packaging option capable of improving brand differentiation. Future growth is expected to be supported by expanding demand for on-the-go beverage consumption and sustainable packaging solutions.

By Material

Recycled aluminum dominated the material segment in 2024, capturing approximately 56.4% of market share. The segment's leadership is attributed to growing sustainability requirements and increasing emphasis on circular economy practices. Recycled aluminum significantly reduces energy consumption compared with primary aluminum production while maintaining material performance. Beverage companies are actively incorporating higher levels of recycled content into packaging to achieve environmental goals. For example, numerous global beverage brands have announced commitments to increase recycled aluminum usage across product portfolios. Strong regulatory support and expanding recycling infrastructure continue to strengthen demand for recycled aluminum materials.

Lightweight alloy aluminum is expected to register the fastest CAGR of 7.9% during the forecast period. Manufacturers are increasingly adopting advanced aluminum alloys to reduce material usage without compromising structural integrity. Lightweight designs lower transportation costs, reduce carbon emissions, and improve production efficiency. Beverage companies are investing in innovative alloy technologies to support sustainability objectives while maintaining premium packaging aesthetics. Future adoption is expected to increase as packaging manufacturers seek to optimize resource utilization and improve overall supply chain performance.

By End-Use

Alcoholic beverages represented the largest end-use segment in 2024, accounting for approximately 42.7% of total market share. Beer, ready-to-drink cocktails, and premium spirits increasingly utilize aluminum bottles to improve product differentiation and support sustainability initiatives. Beverage producers value aluminum packaging for its durability, branding flexibility, and ability to preserve product quality. Premium alcoholic beverage launches frequently feature aluminum bottle packaging to enhance visual appeal and consumer perception. Growing demand for craft beverages and premium alcohol products continues to support segment dominance across both developed and emerging markets.

Energy and functional drinks are anticipated to be the fastest-growing end-use segment, expanding at a CAGR of 8.3% through 2034. Rising health awareness, active lifestyles, and increasing demand for performance-oriented beverages are driving segment growth. Manufacturers are adopting aluminum bottles to position products as premium and environmentally responsible. Innovative packaging designs, coupled with strong branding opportunities, make aluminum bottles particularly attractive within this category. Continued product innovation and expanding consumer demand for functional beverages are expected to sustain robust growth over the forecast period.

Aluminum Beverage Bottles Market Segmentations

By Type

- Standard Aluminum Bottles

- Resealable Aluminum Bottles

- Customized Aluminum Bottles

By Material

- Recycled Aluminum

- Primary Aluminum

- Lightweight Alloy Aluminum

By End-User

- Alcoholic Beverages

- Bottled Water

- Carbonated Soft Drinks

- Energy & Functional Drinks

- Juice & RTD Beverages

Regional Analysis

North America

North America accounted for approximately 29.4% of the global aluminum beverage bottles market share in 2025 and is projected to grow at a CAGR of 6.8% through 2034. The region benefits from strong beverage consumption, established recycling infrastructure, and increasing demand for sustainable packaging solutions. Beverage manufacturers across the United States and Canada are actively replacing plastic packaging with recyclable aluminum alternatives. Growing demand for premium water, energy drinks, and alcoholic beverages further supports market expansion. Consumer awareness regarding environmental sustainability continues to influence purchasing decisions, encouraging beverage companies to invest in aluminum packaging technologies.

The United States remains the dominant country within North America. A unique growth driver is the rapid expansion of sustainable beverage packaging initiatives among major consumer brands. For example, several leading bottled water companies have introduced aluminum bottle product lines targeting environmentally conscious consumers. Retailers and stadium operators are also reducing plastic bottle usage and adopting aluminum alternatives. These industry trends, combined with strong recycling rates and investments in circular economy programs, continue to strengthen the country's leadership position within the regional market.

Europe

Europe represented approximately 24.7% of global market share in 2025 and is forecast to expand at a CAGR of 6.9% during the study period. The region's market growth is supported by strict environmental regulations, ambitious recycling targets, and strong consumer demand for sustainable packaging. Many European countries have implemented policies that encourage recyclable packaging materials and discourage single-use plastics. Beverage manufacturers are responding by increasing aluminum bottle adoption across water, soft drinks, and alcoholic beverage categories. The region also benefits from advanced recycling systems and strong regulatory support for circular packaging initiatives.

Germany is the leading country in the European market. A unique growth factor is the country's well-developed deposit return system, which encourages high recycling rates and supports aluminum packaging adoption. Beverage producers increasingly utilize aluminum bottles to align with sustainability objectives and consumer expectations. Premium beverage launches in Germany frequently feature recyclable aluminum packaging to enhance environmental positioning. The country's strong manufacturing base and advanced packaging technology ecosystem further contribute to market growth and innovation.

Asia Pacific

Asia Pacific dominated the aluminum beverage bottles market with a 38.1% share in 2025 and is expected to register a CAGR of 7.7% through 2034. Rapid urbanization, rising disposable incomes, and growing consumption of packaged beverages are key growth drivers. Expanding retail networks and increasing environmental awareness are encouraging beverage manufacturers to adopt sustainable packaging solutions. Demand for premium beverages, energy drinks, and bottled water continues to rise across major economies, creating substantial opportunities for aluminum bottle producers. Investments in regional recycling infrastructure are also supporting long-term market expansion.

China is the dominant country within Asia Pacific. A unique growth driver is the rapid expansion of premium ready-to-drink beverage categories. Domestic beverage companies are increasingly utilizing aluminum bottles to differentiate products and improve sustainability credentials. For example, premium tea beverages and functional drinks are increasingly packaged in aluminum formats. Government initiatives supporting waste reduction and resource efficiency further encourage adoption. Combined with strong manufacturing capabilities, these factors position China as a key contributor to regional market growth.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.9% of global market share in 2025 and is projected to grow at a CAGR of 6.6% over the forecast period. The market is supported by increasing beverage consumption, urban population growth, and expanding retail distribution networks. Demand for bottled water remains particularly strong due to climatic conditions and rising health awareness. Beverage manufacturers are gradually introducing aluminum bottle packaging to meet sustainability objectives and enhance product differentiation. Government initiatives promoting waste management improvements also contribute to market development.

The United Arab Emirates leads the regional market. A unique growth factor is the expansion of sustainable hospitality and tourism initiatives. Hotels, resorts, and event venues are increasingly replacing plastic beverage packaging with recyclable aluminum alternatives. For example, luxury hospitality operators have introduced aluminum bottled water programs to support sustainability goals. These initiatives are creating new opportunities for packaging suppliers and strengthening regional demand for aluminum beverage bottles.

Latin America

Latin America held approximately 3.9% of the global market in 2025 and is anticipated to grow at the fastest CAGR of 7.8% through 2034. The region is benefiting from increasing beverage consumption, growing environmental awareness, and expanding retail infrastructure. Beverage manufacturers are investing in recyclable packaging formats to align with sustainability trends and strengthen brand value. Rising demand for bottled water, soft drinks, and alcoholic beverages continues to support market growth. Improvements in recycling capabilities are also enhancing the attractiveness of aluminum packaging solutions.

Brazil remains the dominant country within Latin America. A unique growth driver is the country's strong aluminum recycling ecosystem. Brazil consistently maintains high aluminum recovery rates, supporting sustainable packaging initiatives across the beverage industry. Several domestic beverage companies have introduced aluminum bottle packaging to capitalize on consumer interest in environmentally responsible products. Growing retail penetration and expanding premium beverage segments are expected to further support market growth throughout the forecast period.

Competitive Landscape

The aluminum beverage bottles market is moderately consolidated, with several major packaging companies competing through innovation, sustainability initiatives, and geographic expansion. Ball Corporation remains the market leader due to its extensive aluminum packaging portfolio, strong manufacturing capabilities, and global customer network. The company recently expanded production capacity to support growing demand for recyclable beverage packaging.

Other significant participants include Crown Holdings, Ardagh Group, CCL Container, and Envases Group. These companies are focusing on lightweight bottle designs, increased recycled content, and strategic partnerships with beverage manufacturers. Investments in advanced manufacturing technologies and sustainability-focused product development remain key competitive strategies. Market participants are also expanding regional production facilities to improve supply chain efficiency and address growing demand across emerging economies.

Key Players List

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- CCL Container

- Envases Group

- Alucon Public Company Limited

- Exal Corporation

- Toyo Seikan Group Holdings Ltd.

- Nampak Ltd.

- Can-Pack S.A.

- Orora Limited

- Trivium Packaging

- Massilly Holding SAS

- Silgan Holdings Inc.

- Colep Packaging